Nataliya Rodina/iStock via Getty Images

Summary

Following up on my previous coverage of Krispy Kreme (NASDAQ:DNUT), I recommended a buy rating due to my expectation that DNUT will continue to be successful in implementing its business model and find success in increasing its market presence in newly identified markets. This post is to provide an update on my thoughts on the business and stock. I reiterate my buy rating for DNUT, as I think the fundamentals remain strong despite the share price movement. Management continues to execute well on DFD (Delivered Fresh Daily), and I expect it to continue growing given the market opportunities available.

Investment thesis

It’s another wile ride with DNUT as the share price took a deep dive since the earnings results release. Stock price volatility has become part of life when investing in DNUT. However, I believe investors should focus on the business performance as it is what drives long-term shareholder returns. In the United States alone, sales of $267 million fell just short of the $269 million expected by the Street, despite organic growth of 12.7%. Prices, discounts, and the popularity of DFD’s specialized donuts all played a role in the growth. When viewed in the context of the economy as a whole, a growth rate of 12.7% looks excellent, in my opinion. Further, the number of DFD accounts in the United States has increased from 4,137 in F20 to 6,320 in 2Q23, an increase of roughly 50%. This expansion, coupled with the operating leverage DNUT will achieve from its fixed costs (its drivers and trucks), should continue to lead to a rise in the company’s profit margin. Given the current pace, I anticipate that management will keep making investments in order to take advantage of the DFD opportunities currently available. In the call, management mentioned they have already added 87 from start of the year to date, and expect similar additions for 2H23. The subtle clues provided add to my growing sense of assurance. For instance, they discussed how opening up new doors is just as good in performance, as the opening comes with new customers and channels.

Interestingly, the new doors, we’re finding they are at least as good. In fact, many of the new doors are better sales performance right now. Partly, we think that’s because we’re expanding with new customers, new channels. 2Q23 earnings results call

The potential ahead is substantial, with management expressing confidence in their ability to swiftly utilize current hubs and strategically introduce fresh production hubs, facilitating an expansive network surpassing the initially aimed 15,000 access points across the US. Remarkably, among the 15,000 objective, 12,000 can be attained through existing hubs, negating the necessity for new investments in hubs for the foreseeable future, thereby yielding incremental growth with elevated profit margins. Moreover, there’s potential for the 12,000 benchmark to exceed projections, considering management’s indication that the newly established hubs are purposefully designed with automation and additional production lines to cater to demand, thus enhancing capacity.

I mean, if we wanted to add on top of that 12,000, let’s say, another 8,000 to 10,000 over the years to come as we meet the DFD demand, we think that still only requires a 10% to 15% increase in production hubs itself because we’re learning how to make production hubs purpose built with automation, with more production lines to meet this kind of demand. 2Q23 earnings results call

Finally, the specific category I maintain a positive outlook on is Insomnia. This brand, catering to a predominantly youthful consumer base accounting for approximately half of its sales, continues to shine within the US sector. The expansion of store presence remains robust, with the brand concluding 2Q23 with 244 stores and a projected growth to 427 stores by FY26. Crucially, the financial feasibility remains appealing, with incremental margins exceeding 20% based on incremental EBITDA over revenue since FY22.

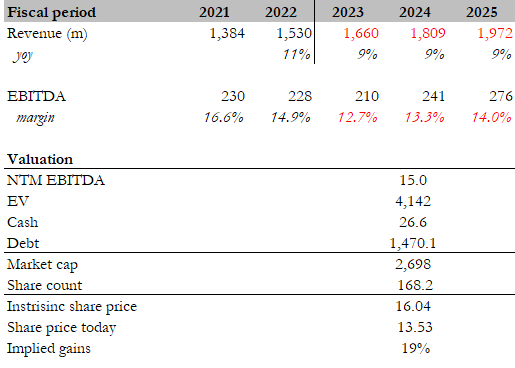

Valuation

Own calculation

I continue to believe the fair value for DNUT based on my model is in the range of $16. My model assumptions are the same as what I assumed previously, with growth momentum following the FY23 guidance and margins gradually improving to 14% (FY22 levels). DNUT has historically traded at 15x forward EBITDA on average, and I expect this multiple to move towards this as DNUT continues to execute and grow as planned.

Risk

Donuts are not a healthy food by all metrics, which is an inherently permanent headwind that donuts will have to endure as time goes by. Especially with the younger generations paying more attention to health (eating salads and what not), demand for donuts might slowly taper over time.

Conclusion

I reiterate my recommendation to buy DNUT. Strong fundamentals persist, underscored by successful execution of the DFD model and expansion into new markets. Despite a recent dip in share price, focusing on long-term business performance remains crucial for sustained returns. The US segment displayed organic growth of 12.7%, showcasing resilience in uncertain economic conditions. Expansion of DFD accounts, coupled with operational leverage, should drive profit margins higher. Management’s strategic approach to utilizing existing and new hubs indicates potential for substantial growth beyond the 15,000 access point goal.

Be the first to comment