Denis_Vermenko

Consumer staples are a good way to shield oneself from an economic downturn, as households should continue to gravitate towards familiar brands in good times and bad. That’s why I hold undervalued players like Unilever (UL) in a diversified income portfolio.

This brings me to Kraft Heinz (NASDAQ:KHC), which is once again trading below $40. In this article, I highlight why KHC is once again in buy range and is a worthy holding for an income portfolio, so let’s get started.

Why KHC?

Kraft Heinz is the third-largest food manufacturer in North America, with iconic brands such as Oscar Mayer, Heinz Ketchup, Velveeta, and Kraft Mac & Cheese. The company has a strong presence in both developed and emerging markets, with over 200 brands in its portfolio and sales in 190 countries.

While the company has been faces some challenges in recent years, including an unsuccessful attempt to merge with Unilever in 2017 and an accounting scandal in 2021, it has made progress on its turnaround plan. Kraft Heinz has divested non-core businesses, and is focused on driving growth in its core categories.

The company’s results have been mixed in recent quarters, but there are signs that Kraft Heinz is starting to turn the corner. In the most recent reported quarter, Kraft Heinz reported better-than-expected earnings and revenue, with organic sales growth of 6.8% YoY and 5.3% CAGR on a 2-year basis. This was driven by strong performance in the company’s core U.S. business as well as Emerging Markets, which grew organic sales by 7% and 10% YoY, respectively.

Kraft Heinz is also making progress on its cost-saving initiatives, which should help to boost margins and bottom-line growth going forward. The company has targeted $2 billion in cost savings by 2024, and is on track to achieve this goal. This, combined with price increases, could go a long way in helping the company to weather and at least stay in line with inflation.

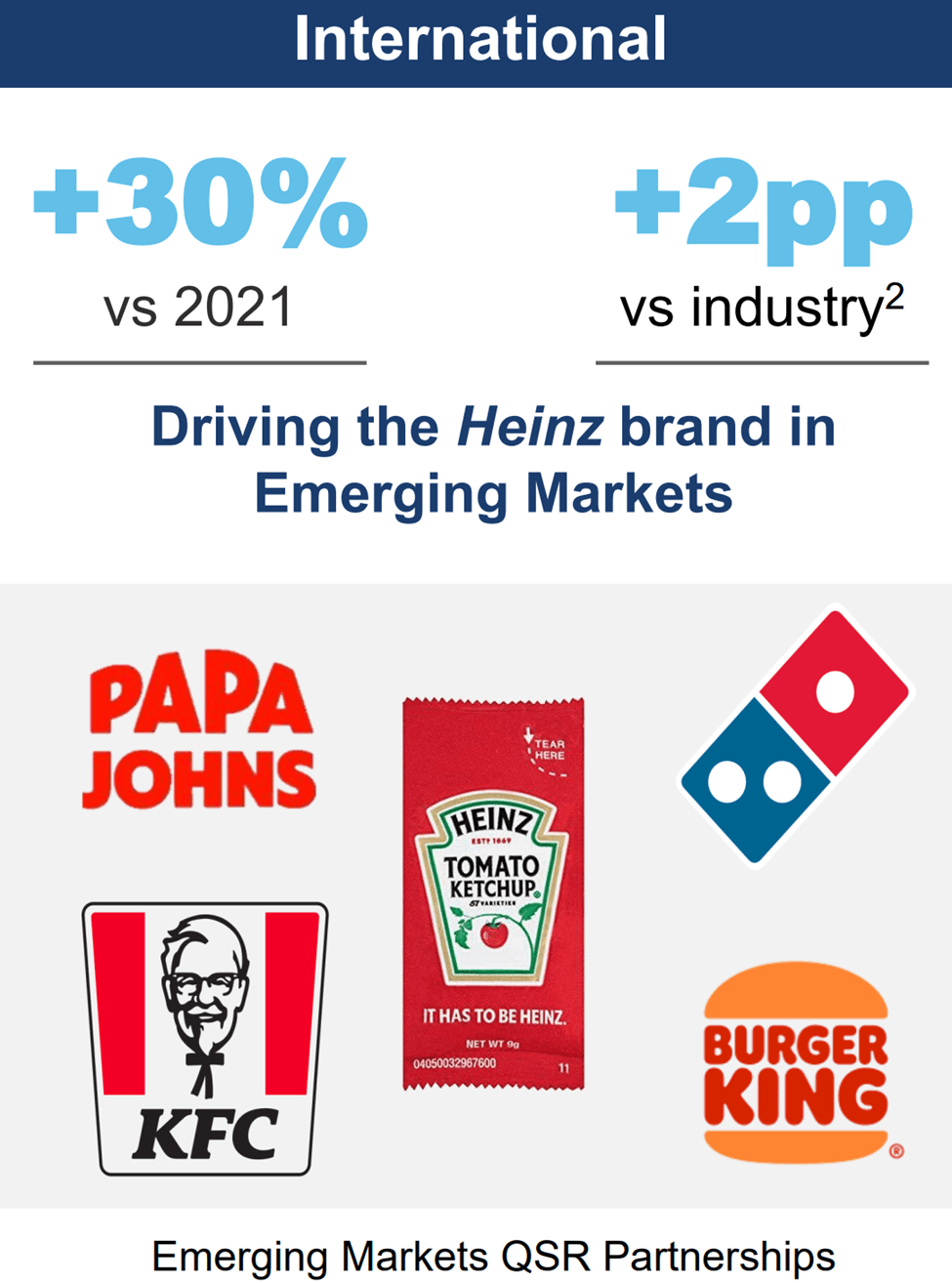

Looking forward, management seeks to grow its business through its fast-growing foodservice category, which is seeing U.S. growth in the high teens with expanding partnerships with quick service restaurants, including its Jack in the Box partnership. As shown below, KHC is also partnering with top QSR brands in international markets, which is seeing an even faster rate of growth.

KHC Foodservice Growth (Investor Presentation)

KHC also appears to be actively taking steps towards enabling faster, localized decision-making and streamlining the organization to take advantage of its scale, as highlighted by management during last month’s Bank of America (BAC) Global Consumer Conference:

We learned from mistakes that we made in the past. I think for the company, if I were to highlight one aspect, it was very siloed. Like, we had aspects, many times supply chain and the commercial side, operating independently in many ways. Many of the business units within the U.S., but then countries as well, not taking advantage of the scale we have as a company. So that has changed a lot. It has changed with more than 50% of the leadership team coming from outside with experience in their functional areas

And then we’re really proud of ourselves of the agility that we operate. I mean, I think you could say we are not a company with a lot of bureaucracy, probably one of the least if not the least, among peers, letting the decision on the execution be done on the local level, either in the U.S. or across international, which is very important, really for the agility of the decision-making. So taking advantage of this agility at scale, it’s something very important for us, and we are living this on the day-to-day.

Meanwhile, KHC maintains a BBB- investment grade credit rating, and has taken steps to deleverage its balance sheet, with a net debt to adjusted EBITDA ratio of 3.3x, sitting below the 3.6x and 4.5x in early 2021 and 2020, respectively. This lends support to the respectable 4.2% dividend yield, which comes with a low 57% payout ratio. I see room for a dividend bump down the line with further deleveraging of the balance sheet.

Risks to KHC include potential for supply chain disruptions with high energy prices, and a tight labor market. Moreover, increased pressure from private labels could hurt profitability in KHC’s premium priced brands.

Nonetheless, I see value in KHC at the current price of $38.37 with a forward PE of 14.2. Sell side analysts have an average price target of $43.67 and Morningstar has a fair value estimate of $51. This implies a potential one-year return in the 18% – 37% range, including dividends.

Investor Takeaway

Kraft Heinz appears to be actively taking steps towards enabling faster, localized decision-making, and has targeted $2 billion in cost savings by 2024. The company is also partnering with top QSR brands in international markets, which is seeing an even faster rate of growth. I see value in KHC’s stock at the current price for long-term investors, while getting paid a well-covered dividend during the continued turnaround.

Be the first to comment