Astrid Stawiarz/Getty Images Entertainment

If I had been asked a year ago to name the first thing that came to mind in connection to the clothing brand Wrangler, I no doubt would have said something like “blue jeans” or “denim,” and in fact I have at least one pair of Wrangler jeans in my closet. But about a year ago, my wife found some Wrangler thermal shirts on sale at our local Walmart (WMT), and sent me back to look for one in a different size. What I found pleasantly surprised me – I picked up several Wrangler branded thermal shirts for myself and my family that I absolutely love for cold-weather running or just as a base layer for any outdoor cold-weather activity, and now I associate those shirts as much or more with the brand than I do denim products.

The Wrangler brand, along with the Lee brand, are the primary assets of clothing company Kontoor Brands (NYSE:KTB), an investment I currently hold a long position in dating to February 2021 with additional purchases off and on since then, as recently as October 2022. Although I have written about Kontoor on some other occasions, I have not followed-up in over a year, and it is well worth checking-in again.

What’s New At Kontoor

There are several developments that in the past few months that deserve attention. On an international note, the Lee brand has a solid track record of popularity in China, and Wrangler has established its own direct retail presence in China as of November 2021. However, management noted in November 2022 on the Q3 earnings call that China reopening was going more slowly than hoped. Since then, the process of reopening in China seems to be speeding up, after lifting the zero-Covid policy. This step should help get sales back to a baseline for more meaningful measurement.

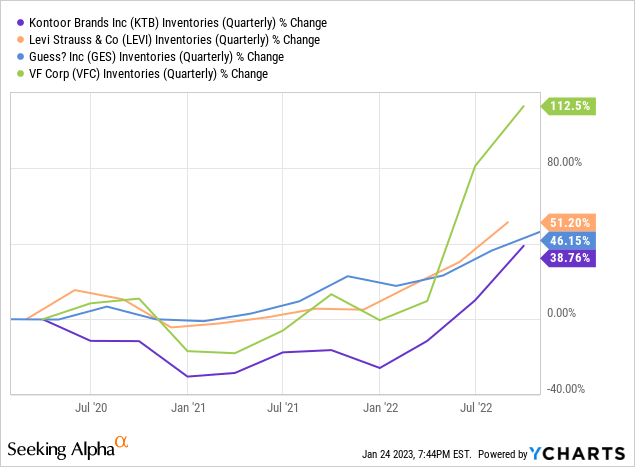

The situation in China may also help relieve pressure on inventory that has been a challenge for multiple clothing brands. Inventory values have risen broadly since Covid-19 first entered the scene, but credit to Kontoor Brands for managing their working capital better than some others, with inventory up merely 39% since January of 2020, the lowest out of a small selection of peers like its most direct competitor, Levi Strauss (LEVI), as well as less direct competition like Guess Inc (GES), with denim generally priced higher than Kontoor’s offerings, and former Kontoor parent company V.F. Corp (VFC) that owns workwear brand Dickies, amongst other clothing brands.

What they all have in common, however, is major upticks in inventories since January of 2022, which will eventually need to find an outlet to reach the consumer somewhere in the world. Between China reopening and broad industry concern for the inventory glut, there is some logical hope that inventories will fall back to much more normalized levels over the results from Q4 of 2022 and through the first half of 2023. In Kontoor’s case, the inventory value as of 9/30/22 was $678.2 million, compared to just $409.1 million a year earlier, and just $363.0 million starting 2022, an 87% increase in 9 months. To be fair, the end of Q3 is often when retail dependent names will have their peak inventory leading into the critical Q4 holiday shopping quarter, and the end of Q4 should be lower, but this is the highest inventory level ever recorded for Kontoor.

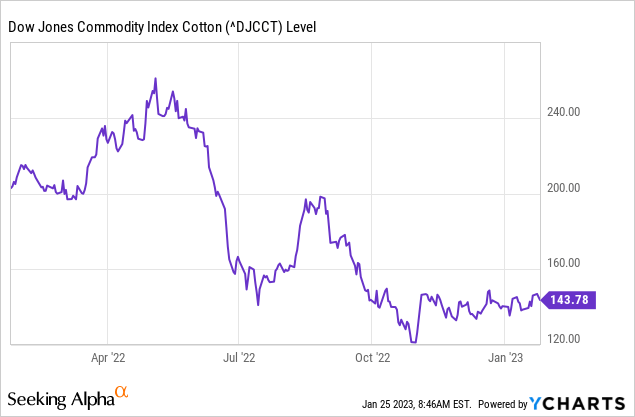

Another common threat has been the supply chain challenges and input costs, both in terms of raw materials like cotton, but the higher cost of labor as well. Kontoor’s supply chain leadership based in Mexico is currently highlighted on their website, which I think speaks to the recognition that it is a critical responsibility. Kontoor did invest in upgrading its ERP capabilities, making those CapEx choice plans in 2019. It has taken a couple of years to fully implement, but now the company is starting to realize the benefits. On the cost of cotton, the pressures are easing up, with costs coming down over the last year and holding steady for the last three months.

Gross margins should see the benefit, though pricing could be under some pressure until inventories are balanced again. Gross margins peaked at just over 46% in the first half of 2021, but have drifted down around 250 basis points since (dollar amount in chart below is in millions of USD).

Kontoor Brands Gross Margin Trends (Author’s spreadsheet; data from Seeking Alpha)

Kontoor, like its peers generally, has been raising prices where it can, helping to keep margins from eroding further, and if the pricing power can be held steady, then hopefully in time the margins will fully recover.

Recent Results and Outlook

Management’s past practice for releasing full year results has been timed to very early March, and I expect the same for this year, meaning the world will have to wait another 5 weeks or so for the 2022 numbers. So investors are left with evaluating three quarters of last year’s results so far and try to interpret the direction things are likely to be going.

Through 9 months of 2022, total sales have been $1,899.8 million, compared to $1,794.9 over the same period in 2021. Those results are pretty solid given how tightly closed the Chinese sales channels have been over that same stretch. Earnings per share for 2022 through September were $3.60, handily beating the consensus view expecting $3.12. At the same time, the balance sheet has seen some deterioration, with cash and equivalents sitting at just $58 million, due in part to the cash consumed in the inventory figures referred to earlier. That cash balance is down from $185 million at the start of the year, and long-term debt obligations, after falling for several quarters, did turn higher, ending Q3 at $824.8 million, versus $791.3 million in January.

The board does not seem to be too concerned about the balance sheet trends, as it approved an increase to the previous dividend, from $0.46 to $0.48, although the use of cash to fund the dividend is partially offset from a lower shower count, with total shares outstanding decreasing about 3.5% on a trailing twelve month basis through Q3. With the bump, a new investor would be coming in at a yield of 4.1% The dividends run around $106.5 million per year at the new rate, but Kontoor has been patiently buying back shares, spending slightly more on those repurchases over the last five quarters at $153.2 million, part of a $200 million authorization approved in mid 2021. The pace of buybacks slowed to a crawl for Q3, at only $1.6 million, but could pick up again when the cash flow supports it sufficiently.

It was a fluid situation as the 3rd quarter closed in terms of how the year might end. Levi’s just reported a strong quarter in terms of earnings, beating consensus figures; I believe this bodes reasonably well for Kontoor Brands. Interestingly for Levi’s, its inventory continued to grow in the quarter from $1,292.3 million to $1,416.8 million while its cash & equivalents declined by $100 million (Levi’s reporting year ended November 27, 2022). Without Q4 figures to know for sure how the year ended, one can just listen to CEO Scott Baxter’s comments on what he is seeing as of November 2022, and decide if it is convincing given data available since then. On the call, he spoke to his reasons for optimism for a good end to 2022:

we are assuming that inflation in subsequent tight monetary policy weighs on demand, resulting in economic conditions remaining challenged over the near term. So . . . why are we planning revenue sequentially accelerate in Q4? A few points here. First, we base our outlook on the combination of still strong domestic POS share gains and new business development. Second, while certain US retailer inventory levels remain challenged, the significant rebalancing efforts from select retailers has materially improved with aggressive actions taken early from many of our key retail partners with open to buy dollars opening back up and accelerating into Q4. Based on this second point, our quarter to date US orders and shipments have been strong, but we want to be prudently conservative given the uncertainty in the current environment.

I do believe the key relationship to monitor when final results are released will be the working capital tied up in its inventory levels relative to its overall cash. If Kontoor can get that straightened out within one or two quarters, then I expect the debt figures to start coming down once again.

Valuation

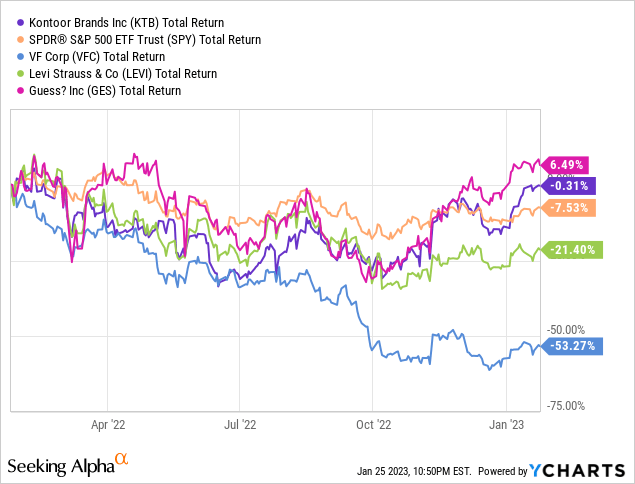

Kontoor’s shares on a total return basis, though slightly negative, have nevertheless done better than the broad S&P 500 (SPY) index over the last year, as well as outperforming peers like V.F. Corp and Levi’s.

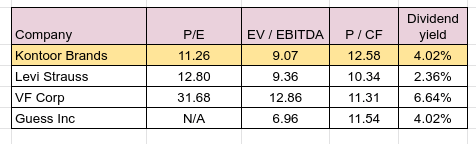

Looking at several metrics relative to some competitors, including P/E and EV / EBITDTA, Kontoor Brands holds its own is overall in-line with its peers, though some have clearly been through a significant valuation adjustment in the market.

Kontoor Brands and Select Peers Valuation Measures (Author’s spreadsheet; data from Seeking Alpha)

My only observations on valuation are these: first, V.F. Corp, the former owner the Kontoor Brands assets, has managed to deliver very poor shareholder returns over the last year and still have the appearance of being overvalued, so credit to Kontoor Brands’ management for doing much better on their own. Secondly, Kontoor has closed some of the previously existing valuation gap between itself and Levi’s, in which for some time the market was willing to give Levi’s a bit of a valuation premium relative to Kontoor. By and large that difference has been erased, for the moment at least. All in all, I think both are priced fairly for being in a mature, slow-growth industry.

Risks & Conclusion

For all of the concern about, inflation, the Federal Reserve, recession and consumer discretionary spending softness, this morning’s Q4 initial GDP report for the United States painted a fairly rosy picture for economic growth. I do believe there is ongoing risk for recession and consumer weakness in 2023, the signals at this point remain mixed enough in my view that the best I can say is that if we enter a recession, I expect it to be relatively mild. Assuming that Kontoor Brands gets its balance sheet in order again, then I think the worst reasonable outcome to be a slight decrease in its sales in 2023. However, given the evidence from Levi’s in which its cash declined and inventory continued to increase, it is still a wait and see story for me with Kontoor. I am long the shares, and holding for the dividend, but consider it a hold for the time being.

Be the first to comment