andriano_cz/iStock via Getty Images

Introduction: Why is Kone Stock Down?

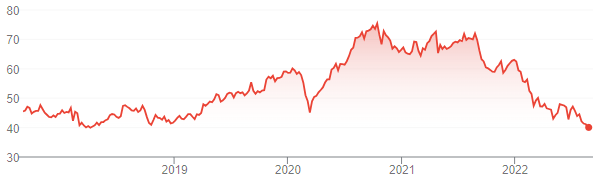

We review our investment case on Kone Oyj (OTCPK:KNYJY) after shares fell below €40 in Helsinki to a new 5-year low:

|

Kone Share Price (Last 5 Years)  Source: Google Finance (26-Aug-22). |

We initiated our Buy rating on Kone in June 2020. Shares have now lost 28% (after dividends) since our initiation, falling another 13% since Q2 2022 results on July 20, and are down 47% from their all-time high in October 2020.

Kone has been battered by the slowdown in Chinese construction and rising input costs. Q2 2022 results were poor, largely due to COVID lockdowns in China. The full-year 2022 outlook was cut again. However, orders grew and there were signs of progress in pricing and margins outside China. China remains the biggest unknown for identifying a bottom for Kone’s P&L, and much will depend on the construction sector there.

We now assume EPS will decline by 15% in 2022, but return to growing at 7% annually from 2023. With Kone shares now trading at 20.4x 2021 EPS, our forecasts indicate a total return of 58% (15.7% annualized) by 2025 year-end. Buy.

Kone Buy Case Recap

Kone is a top-3 player in the global elevator and escalator industry. We believe Kone and its peers to be high-quality businesses, thanks to the structural growth in demand from urbanization and taller buildings, recurring Maintenance and Modernization services (which generate most of the profits, except in China), a highly consolidated competitive landscape, and a capital-light manufacturing model that sources components from a network of suppliers.

Kone is the #1 player in China and a top-3 player in every region except North America (where it is #4). Its global market share is approximately 19% in New Equipment and 10% in Services; within the latter it is a joint #2 in Maintenance.

China had historically been a major source of profits and growth for Kone, where its large construction sector generated high-margin New Equipment sales. The country represented as much as 35% of Kone’s sales in 2021. However, the construction boom in China has now ended, and Kone has set out new growth targets at its 2022 investor day that rely much less on New Equipment sales:

- New Equipment sales to be “stable to low growth”

- Maintenance sales to grow at “mid to high single-digit”

- Modernization sales to grow at “high single-digit”

Kone also has a target of raising Adjusted EBIT margin to 16% (from 12.5% in 2021) As we described in our June 2022 review, the revenue growth targets, together with modest margin expansion (of, say, 35 bps annually), imply an approximately 7% annual growth in Adjusted EBIT.

In addition, Kone had historically not included automatic price adjustments in its backlog of contracts, which means COVID-related high inflation since 2021 has significantly impacted its profits. Management has been remedying this with price increases, new “dynamic” contract pricing terms, and cost savings.

Q2 2022 results were heavily impacted by COVID lockdowns in China, but showed progress in Kone’s self-help efforts.

Kone Q2 Heavily Hit by China Lockdowns

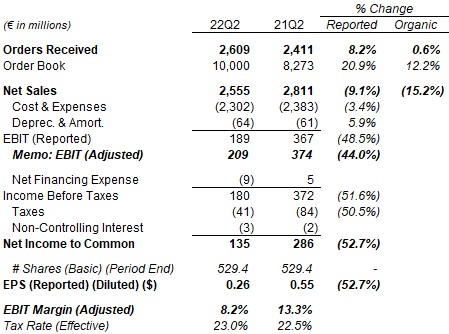

Q2 2022 was a poor quarter for Kone, with Net Sales down 9.1% (15.2% excluding currency), Adjusted EBIT down 44.0% (Adjusted EBIT Margin fell to just 8.2%) and Reported EPS down 52.7% year-on-year:

|

Kone Orders and P&L (Q2 2022 vs. Prior Year)  Source: Kone results release (Q2 2022). |

The culprits were COVID lockdowns in China and higher input costs. China alone was described as reduced Adjusted EBIT by “over €100m”. Supply chain issues and labour shortages in some markets also reduced sales.

Demand for Kone products remained healthy, with Orders Received up 0.6% and the Order Book up 12.2% year-on-year (excluding currency); management stated there was “strong growth” in Orders Received in the Americas, EMEA as well as in Asia-Pacific excluding China.

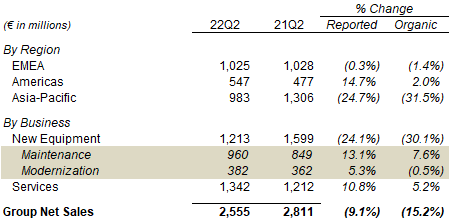

The reasons for Kone’s poor Q2 results are clearer if we look at Net Sales by region and by business:

The reasons for Kone’s poor Q2 results are clearer if we look at Net Sales by region and by business:

|

Kone Net Sales By Region & Business (Q2 2022 vs. Prior Year)  Source: Kone results release (Q2 2022). |

By region, excluding currency, Kone Net Sales were broadly stable in the Americas (up 2.0% excluding currency) and EMEA (down 1.4%), despite supply chain issues and labor shortages that delayed some projects and thus revenues. Asia-Pacific Net Sales were down 31.5% excluding currency, but this was entirely due to China Net Sales falling 40% year-on-year; Net Sales for Asia-Pacific excluding China grew year-on-year in Q2.

By business, excluding currency, Maintenance sales grew 7.6% year-on-year; Modernization sales were down slightly (0.5%), again due to supply chain and labor issues. New Equipment sales were down by 30.1% again entirely due to China; management stated that “New Equipment markets outside of China have actually been good” , with “clear growth” in most markets outside Central and Northern Europe.

The Chinese market was down more than 20% year-on-year in Q2, with COVID lockdowns delaying construction in many areas and also some property developers experiencing financial difficulties. Kone now expects the Chinese market to be down 15% for the full year. Lockdowns also closed down Kone’s factory in Kunshan entirely for several weeks in April and limited its production in May (June was back to normal). Kone’s 40% sales decline in China came from a combination of weaker volume, weaker price as well as a “slight” negative mix shift.

Kone EBIT Down 35% in H1

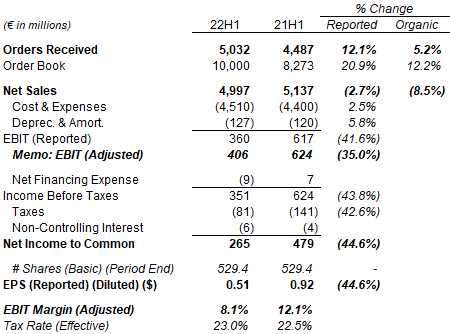

Across H1, Kone’s Net Sales were down 2.7% (8.5% excluding currency) and its Adjusted EBIT was down 35% year-on-year; Reported EPS was down 44.6%:

|

Kone Orders and P&L (H12022 vs. Prior Year)  Source: Kone results release (Q2 2022). |

However, Orders Received for H1 were 5.2% higher, again showing the strength of demand for Kone products.

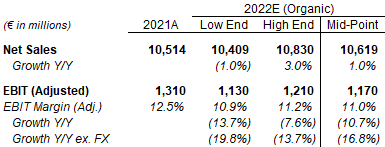

Full Year 2022 Outlook Cut Again

Kone reduced its full-year 2022 outlook. Management now expects:

- Net Sales growth to be -1% to +3% excluding currency (was +2% to +5%)

- Adjusted EBIT to be €1.13-1.21bn (was €1.18-1.28bn)

The Adjusted EBIT outlook includes expectations that:

- Input cost headwind to be €200m (was €150-200m)

- Currency tailwind to be €80m (was €50m)

At mid-point, Kone’s new outlook implies a year-on-year Adjusted EBIT decline of 10.7% (16.8% excluding currency):

|

Kone 2022 Outlook  Source: Kone results presentation (Q2 2022). |

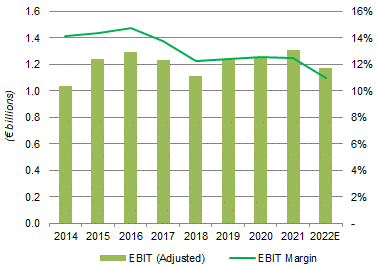

The outlook implies Kone’s Adjusted EBIT will fall for the first time since 2018 while its Adjusted EBIT Margin will be more than 3.5 ppt lower than its previous peak in 2016:

|

Kone Adjusted EBIT & Margin (2014-22E)  Source: Kone company filings. |

While these P&L numbers are disappointing, there are some signs of progress in Kone’s self-help efforts.

Progress in Self-Help Efforts Outside China

Q2 2022 results did contain evidence of progress in Kone’s self-help efforts, at least outside China.

Pricing progress was good in Maintenance and Modernization, where Kone was able to “almost fully transfer to prices the increased costs”. In New Equipment, Kone was “clearly up in prices outside of China so far this year”, having developed positively in Americas, Asia Pacific and Europe during Q2, though management acknowledged that price increases do not yet fully offset the increase in cost; New Equipment pricing is “more challenging” in China.

Cost savings on products continued to be identified, and at rates that were 2-3 times faster than before. As CEO Henrik Ehrnrooth stated on the Q2 earnings call:

Normally when we look at product cost actions that we take; we’ve seen maybe 2%, 3% decrease on an annual basis on product cost. As I said, now we’ve been able to see 2 times to 3 times that”

Margin on Orders Received increased sequentially again in Q2 2022, helped by the pricing and cost improvement described above. This marked the third consecutive quarter of such increases (starting from Q4 2021).

The higher expected input cost headwind of €200m may mark the ceiling of that number, because management now has more visibility over full-year costs and supply chain disruption has started to ease. Again as Ehrnrooth explained:

While the headwind continues to be very significant … we’re starting to see the first signs, I wouldn’t say anything concrete, but first signs of improvement in global supply chains, overall logistics, and perhaps, component availability …

From an input cost, logistics cost perspective, we have a pretty good visibility for the year of 2022 already. So we’re committed and also start to be have a quite a clear picture on – on the mix which countries and so forth. So there overall the cost headwind now is the €200 million and there’s less variability there.”

The result of all of the above is that management expects margin to start to recover in Q3:

If you think about the nature of the actions clearly we’ve seen now … margins for orders received starting to improve latter part of last year. Some of those start to be in delivery at the latter part of the year, so gradually contributing positively. Also, the product cost actions that we’ve talked about, they will gradually start to then impact also our manufacturing and be then impacting P&L. So gradually, I expect that the margins will then recover towards the latter part of the year, but we will start to see some of that slowly impacting then also Q3”

Ilkka Hara, Kone CFO (Q2 2022 earnings call)

China remains the biggest unknown, both because of its size and because all of the improvements observed at Kone so far have been outside China. The situation in China is also macro-driven – if the construction sector deteriorates further, New Equipment volume will fall again, and pricing will also likely get worse with manufacturers competing for an even smaller market. Our base case is that the construction sector in China will stabilize, as it is simply too important to the overall economy for the government to let it fail, and there have been recent signs of new state support.

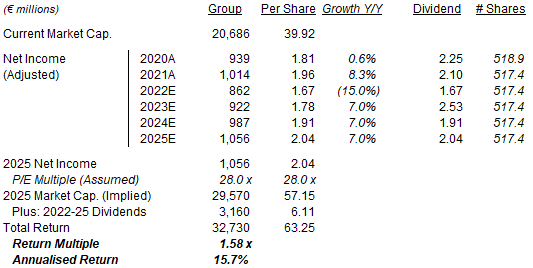

Kone Stock Forecasts

We cut our forecasts further to include an even larger EPS decline in 2022, but still assume the same return to 7% EPS growth in 2023. We now assume:

- 2022 Net Income decline of 15% (was 7.5%)

- From 2023, Net Income growth of 7.0% each year (unchanged)

- Share count to be flat (unchanged)

- Dividends to be on a Payout Ratio of 100% (unchanged)

- 2025 year-end P/E of 28.0x (unchanged)

Our new 2025 EPS forecast is 8% lower than before (€2.22):

|

Kone Illustrative Return Forecasts  Source: Librarian Capital estimates. |

With shares at €39.92, we expect a total return of 58% (15.7% annualized) by 2025 year-end.

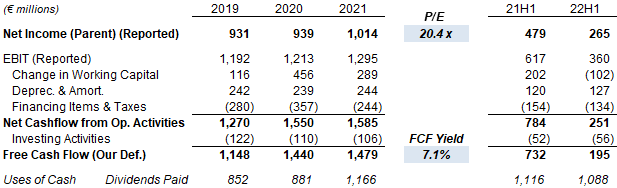

Kone Stock Valuation

At €39.92, relative to 2021 financials, Kone stock is trading at a 20.4x P/E and a 7.1% Free Cash Flow Yield:

|

Kone Earnings, Cashflows & Valuation (Since 2019)  Source: Kone company filings. |

Relative to the median of our new 2022 EPS forecast of €1.67, Kone stock is trading at a 24.0x P/E.

Kone paid a regular dividend of €1.75 per share and a special dividend of €0.35 per share for Class B shares in March 2022 (compared to €1.75 and €0.50 respectively the year before). This represents a 4.4% Dividend Yield. While the dividend has exceeded EPS in recent years, Kone’s FCF / Net Income cash conversion has often exceeded 100%, due to capital expenditures being lower than depreciation and working capital being a positive cash inflow.

Kone has consistently operated with net cash on its balance sheet. At €1.26bn at Q2 2022, this is equivalent to approximately 6% of the current market capitalization.

Is Kone A Buy? Conclusion

Kone has a good underlying business, but the investment case has continued to be complicated by the large exposure to construction in China.

We believe the construction sector in China will stabilize as it is simply too large for the government to let it fail.

In this base case, even assuming a 15% decline in EPS this year (several points worse than the latest outlook), provided 7% EPS growth resumes in 2023, investors can expect a total return of 58% (15.7% annualized).

We reiterate our Buy rating on Kone stock.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment