MichaelRLopez

As the world moves towards autonomous vehicles and robots, Knightscope (NASDAQ:KSCP) offered one of the most promising investment options in the space. Unfortunately, the company came out extremely promotional while lacking contracts in scale to build a meaningful business. My investment thesis is shifting Neutral on the company following the announcement of a long list of new contracts.

Long Contract List

Knightscope is a leading developer of autonomous security robots [ASR], but the company was struggling to produce just $1 million in quarterly revenues when the company came public. The business model at the time didn’t match the valuation, especially when the stock soared to $20 initially.

At the time, Stone Fox Capital made the following statement:

Based on the numbers from the SEC filing, Knightscope might only generate up to $8K in monthly revenue from this highly announced deal. While these deals are promising, the company needs deals for multiple ASRs of at least 10 robots to make the investment story far more interesting. Even at the midpoint of the stated monthly MaaS contracts, an order for 10 ASRs might only contribute $500K in annual revenues.

Since Knightscope has followed up our research with a strong list of new contracts, the stock deserves a second review. When an ASR only generates ~$5K in monthly revenues, the company needs to announce deals for multiple ASRs with multiple customers.

The autonomous security robot company has announced the following set of contracts since Thanksgiving alone:

- Jan. 6 – 4 new contracts for 8 machines

- Dec. 29 – 4 new contracts for 7 machines

- Dec. 22 – 6 more congrats for 8 machines

- Dec. 21 – 5 new contracts for 8 machines

- Dec. 15 – 1 new contract for 3 machines

- Dec. 13 – 2 new contracts for 16 machines

- Dec. 7 – 3 new contracts for 16 machines

- Nov. 30 – 5 new contracts for 22 machines

While Knightscope did shift from announcing deals for only 1 ASR, a lot of the new deals include orders for the Blue Light Tower and Blue Light Emergency Phones that provide additional security to compliment an ASR. Though, the tower and phones acquired via the CASE acquisition provide limited revenues.

Source: Knightscope

As an example, the November 30 deal for 22 machines via 5 contracts include a Texas hospital ordering 4 K1 Blue Light Towers and 8 K1 Blue Light Emergency Phones to expand communication options. The deal details aren’t as impressive once focusing on the actual ASRs.

Accelerated Growth, But Still Small

Knightscope reported 2021 revenues of $3.4 million and the acquired CASE produced $5.4 million in revenues for a combined $8.8 million in 2021. The company targets a revenue run rate in the $12 to $14 million range prior to announcing all of the above new contracts.

Knightscope offers a Machine-as-a-Service (MaaS) business model for their ASRs. The company originally listed charging anywhere from $3,300 to $8,150 per robot per month with an hourly cost below $9 per hour.

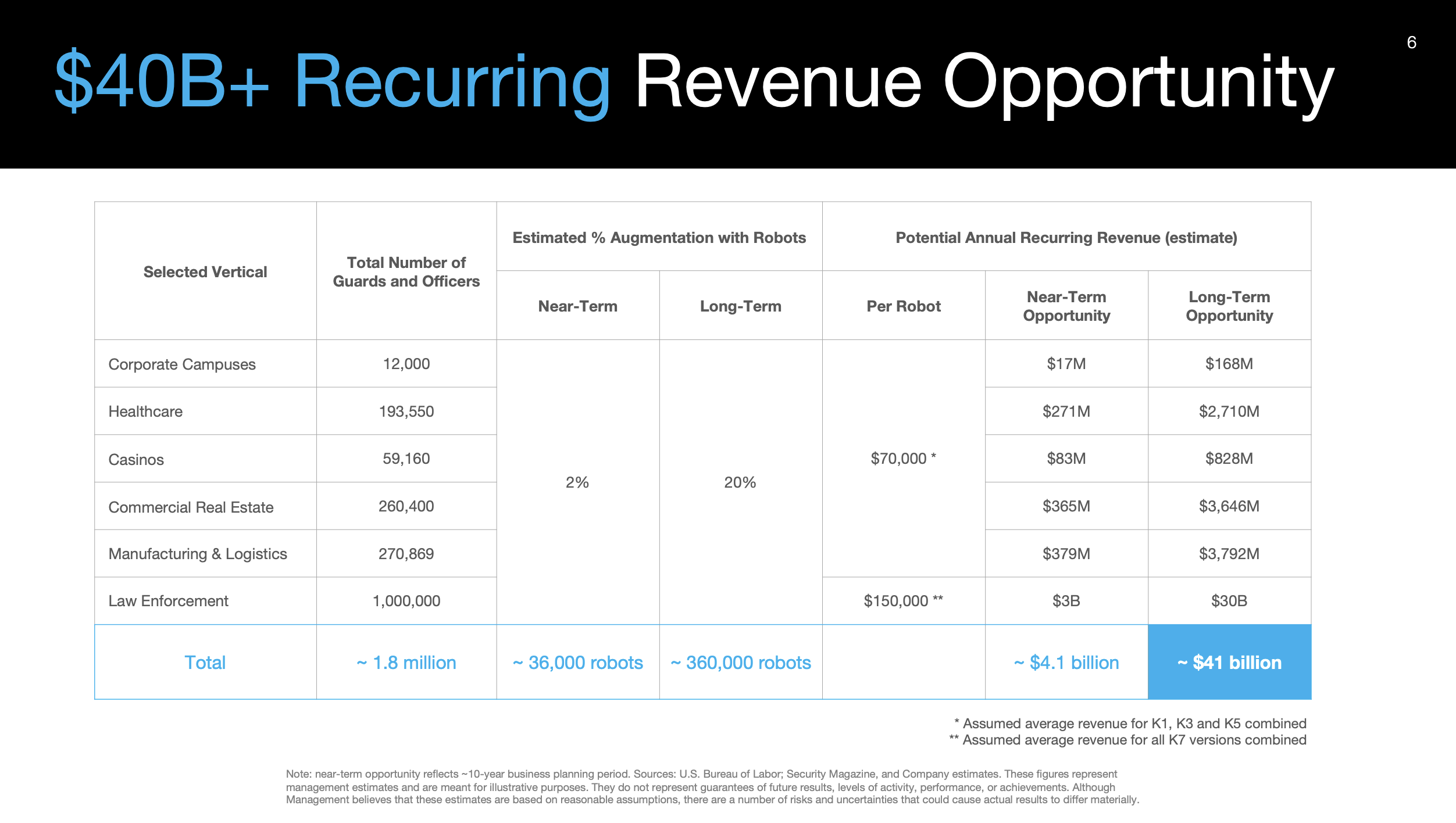

In a 2022 presentation, Knightscope listed the recurring revenues at $2,038 to $6,570 per month in a reduction of the monthly fees. The company lists a market potential for 36,000 ASRs to only replace 2% of security guards leading to a recurring revenue market opportunity topping $4 billion.

Source: Knightscope presentation

The MaaS covers the ASR rental, maintenance, service, support, data transfer and access to the Knightscope Security Operations Center. Knightscope recently launched a remote monitoring service for clients without 24/7 security staff.

As of November 2 following the CASE acquisition, the company only had a backlog of $3.9 million. The backlog included 289 machines with 240 attached to CASE at a backlog of only $1.4 million. The more valuable ASRs were only limited to 49 machines for a value of $2.5 million.

Naturally, Knightscope doesn’t exactly want a large backlog, but the company needs a larger revenue base and a requirement is for a contract to first be announced and either enter revenue or hit the backlog. The backlog should naturally jump with the long list of orders above announced since just Thanksgiving alone, with additional orders in November.

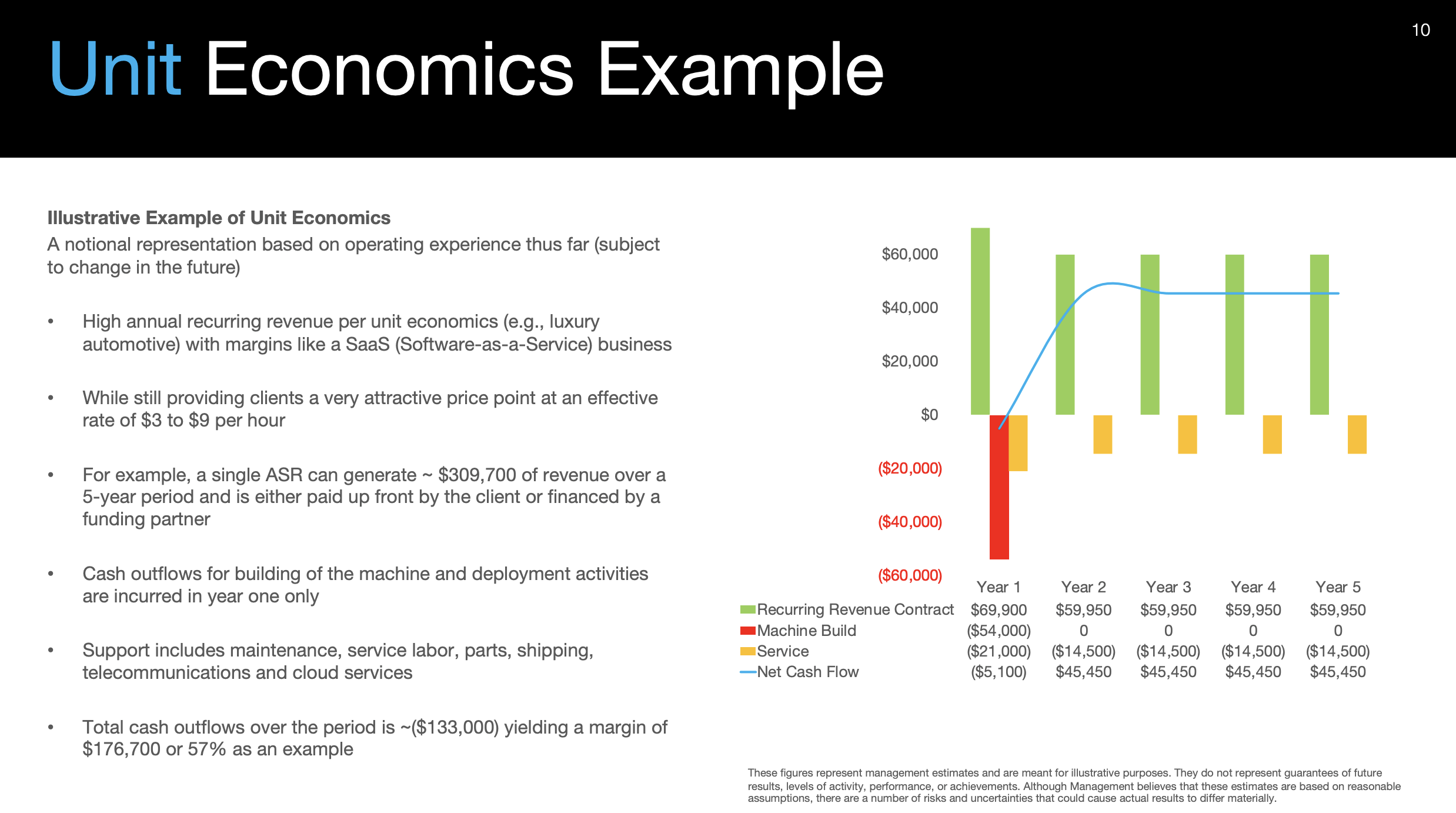

As an example, the largest contact in company history was announced on December 13 with contracts consisting of 12 K5 ASRs, 2 K1 Blue Light Towers and 2 K1 Call Boxes. At a $70K annual recurring revenue rate, the 12 ASRs only generate $840,000 in revenues in the first year.

Source: Knightscope presentation

The contract is nice, but not massive by the normal market trades. The biggest problem with the contract is the $54,000 estimated cost to build the machine leads to a $648,000 upfront cost for the 12 ASRs alone.

Knightscope ended September with a cash balance of $11.1 million. The company needs additional cash to build ASRs for recurring contracts with customers.

Over a 5-year period, the ASRs generate nearly $310,000 in revenues while only costing $54,000 to build. Once factoring annual service costs for $14,500 and an initial cost of $21,000, Knightscope would produce $176,700 in positive cash flows from each autonomous robot over a 5-year period.

The economics of these machines would be very positive once an ASR enters the second year of work. Knightscope just doesn’t have many machines under such scenarios and the current cash balance isn’t enough build the thousands of robots needed to become a large business.

Investors need to expect substantial share dilution in order to fund growth. Knightscope has 37 million shares outstanding as of Q3’22 and the amount will only grow with the stock trading below $2. In fact, the company has 27 million in potentially dilutive shares outstanding already.

Source: Knightscope Q3’22 10-Q

On a fully diluted basis, the market cap reaches $128 million while only projecting revenues in the $13 million range.

Takeaway

The key investor takeaway is that Knightscope is intriguing with a focus on autonomous security robots and related security products. The CEO is very promotional which hurts when the business is struggling, but the public visibility could boost the stock in future periods.

If the company can exceed financial targets and start producing positive cash flows from operations, the stock becomes appealing.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment