Chung Sung-Jun

Elevator Pitch

I have a Buy investment rating for KB Financial Group Inc.’s (NYSE:KB) [105560:KS] stock. I highlighted the “multiple tailwinds” for KB in my prior article for the company’s shares published on May 2, 2022. I provide an update of my views regarding KB Financial in light of its recent Q2 2022 results with the current article.

I am encouraged by KB Financial’s above-expectations earnings and healthy NPL coverage ratio for the second quarter of 2022. KB’s second treasury stock cancellation for this year also gives investors confidence that the company will continue to return excess capital to its shareholders. KB Financial deserves a Buy rating, as its valuations are now at close to historical trough levels comparable to where the stock traded at during the 2008-2009 Global Financial Crisis.

KB Financial Beat Q2 2022 Earnings

KB Financial’s net profit attributable to shareholders grew by +8.2% YoY from KRW1,204 billion in Q2 2021 to KRW1,304 billion in Q2 2022, as indicated in its most recent quarterly results presentation slides. KB’s second-quarter bottom line beat the sell-side’s consensus net income projection of KRW1,274 billion by +2% as per S&P Capital IQ, as both its banking and non-banking businesses performed well in the recent quarter.

The bank’s net interest margin or NIM expanded from 1.56% in Q2 2021 to 1.73% in Q2 2022. KB Financial guided at its second-quarter results call that it is “expecting that in the second half of the year, we will have additional improvement in the NIM” of about “5 to 6 bps (basis points).” KB’s loans also increased by +1.2% year-to-date from KRW319 trillion as of December 31, 2021 to KRW323 trillion as of June 30, 2022.

Separately, KB Kookmin Card stood out among KB Financial’s non-banking businesses, as earnings for the credit card business rose by +14% YoY to KRW127 billion in the second quarter of this year. KB Financial also sought out opportunities to unlock value at the company’s non-banking subsidiaries; KB Insurance saw a KRW169 billion gain relating to the divestment of office properties in the recent quarter.

Treasury Stock Cancellation

In its Q2 2022 financial results presentation, KB Financial revealed that it is doing its second KRW150 billion treasury stock cancellation for this year. This is a significant move for two key reasons.

Firstly, there have been worries in the past that the financial regulators in South Korea won’t allow Korean banks to return more capital to shareholders in challenging times like these. However, the fact that KB Financial has just announced another treasury stock cancellation supports the bullish view that Korean banks in general are sufficiently capitalized and that regulators won’t interfere with their shareholder capital return decisions to a large degree.

Secondly, KB Financial has a good appreciation of how capital allocation can be used as a tool to unlock value for its shareholders. KB Financial stressed at the company’s Q2 2022 investor briefing that “the share buyback (and subsequent treasury stock cancellation)” is “the (relatively) better way (versus dividends) for us to go” taking a “mid- to long-term perspective” and considering its current valuations. Given that KB Financial’s valuations are depressed with the stock trading at a low single-digit forward P/E and a 60% discount to book value, it makes sense to prioritize buybacks (and treasury stock cancellation) over dividends on a relative basis.

KB Stock Price Weakness And Valuations

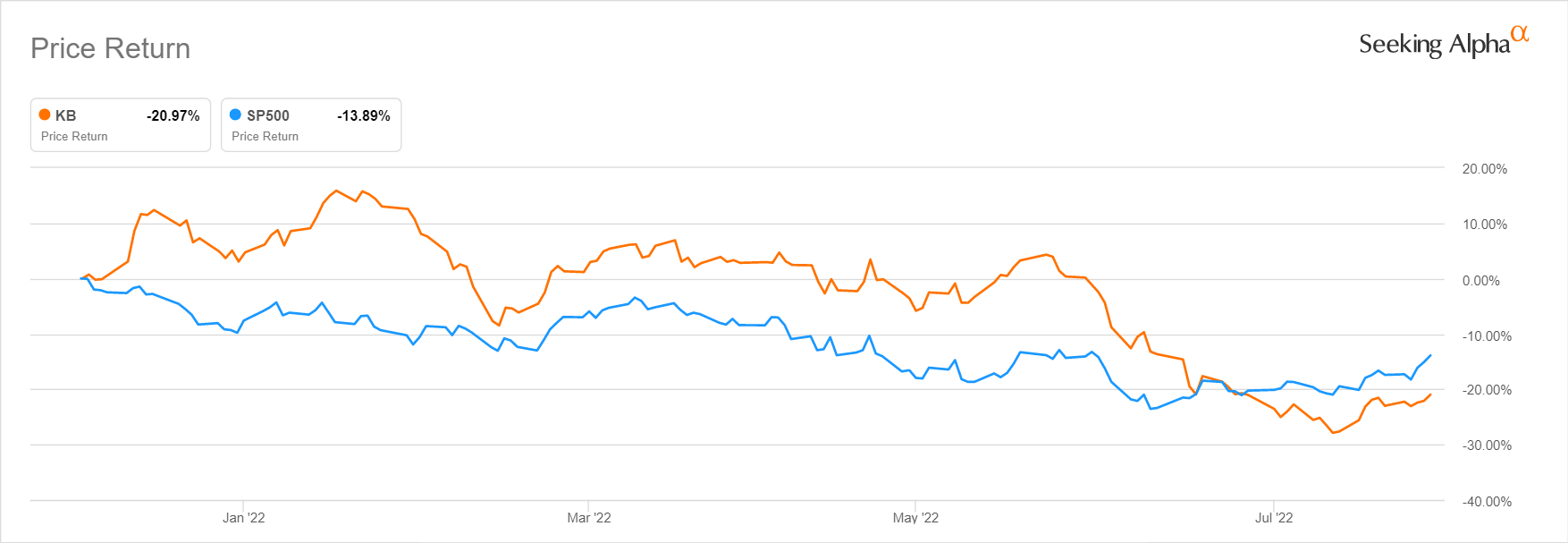

KB Financial’s shares have outperformed the S&P 500 for the first couple of months of 2022, but its stock began to underperform the broader market since late-June as per the chart below.

KB Financial’s Stock Price Performance For 2022 Year-to-date

Seeking Alpha

A July 4, 2022 commentary published in local media, The Korea Times, attributed the weak share price performance of KB Financial and its Korean banking peers to “fears of a recession and the heightened risk exposure of their asset soundness.”

In my opinion, such concerns appear to be overdone and also fully priced into KB Financial’s valuations.

KB Financial’s NPL coverage ratio, or calculated as loan loss reserves divided by non-performing loans, improved from 208.9% as of December 31, 2021 and 217.7% as of end-Q1 2022 to 222.4% as of the end of Q2 2022. At the same time, the delinquency ratios for KB Financial’s banking and card businesses remained low at 0.13% and 0.78%, respectively as of June 30, 2022.

A recent July 20, 2022 Korean banking research report (not publicly available) titled “Almost At Bottoming Out Point” published by NH Investments & Securities also noted that “delinquency rates are at historical lows, while NPL ratios and NPL coverage ratios are at historical highs” for South Korea’s banks as a group.

More importantly, KB Financial is already valued by the market at levels implying a financial crisis similar to the GFC (Global Financial Crisis which happened during the 2008-2009 period).

KB Financial currently trades at 3.8 times consensus forward next twelve months’ normalized P/E, based on valuation data obtained from S&P Capital IQ. KB also traded at below 4 times forward P/E in late-2008 during the GFC. Similarly, KB Financial is now valued by the market at 0.41 times trailing P/B, which is worse what the stock did during GFC when KB’s P/B valuation multiple troughed at 0.5 times. Separately, KB offers a consensus forward next twelve months’ dividend yield of 6.9%; KB Financial’s forward dividend yield exceeded 7% towards the end of 2008 in the GFC period.

Concluding Thoughts

KB Financial is a Buy. The stock’s valuations are back at crisis levels, even though it just delivered an earnings beat for Q2 2022 and announced a second treasury stock cancellation. While acknowledging that there is a risk of a recession which could hurt the performance of banks, KB Financial’s most recent NPL coverage and delinquency ratios suggest that the bears’ concerns might be overdone to a large extent. Furthermore, KB Financial’s valuations have already priced in a worst case scenario, so there could be positive surprises if actual economic conditions turn out to be better than feared.

Be the first to comment