VioletaStoimenova

Thesis

Kanzhun Limited (NASDAQ:BZ) has established a dominant position in job recruitment apps with its industry-leading recommendation engine, but I am most excited about its ~4mn-strong enterprise customer base, which could be exploited for growth areas beyond recruitment. I remain bullish on the company’s medium to long-term prospects given its unique positioning, growth potential, and highly profitable business model (20%+ Non-GAAP net margins already). My December’23 price target of $33 is derived by applying a 12x EV/S multiple to my FY23E revenue estimates.

BZ’s stock price movement (Seeking Alpha)

Why I remain Bullish on BZ?

Leading job recruitment app in China

Kanzhun is the leading next-gen job recruitment app in China with short form video features and recommendation engines to match job seekers with the most suitable open positions. The company differentiates itself through a direct recruitment model and an app with an instant messaging function, allowing job seekers to chat with hiring managers and making it a more efficient process by removing a layer of HR staff in the middle. BZ charges a monthly fee for some of the job postings (not all job postings pay a fee) until the vacancy is filled, providing hiring businesses with a clear ROI in their talent recruitment process. The benefit is obvious. Employers are able to quickly identify and hire the right person for the job.

This “dating” style of recruitment removes the HR middleman and increases the efficiency of the hiring or talent recruiting process. What also sets BZ apart from traditional job sites or apps is the way it monetizes. Instead of charging based on the number of CVs sent to hiring businesses or advertisements by hiring businesses, BZ charges a monthly fee for each job posted (bundled deals are common for larger enterprise accounts) once BZ determines such a posting should be fee-paying. Typically, the most sought-after jobs are free to post on BZ as a way to attract job seekers. The monthly fees terminate once the job is filled.

Market Opportunities

BZ operates in China’s recruitment industry which, according to a CIC report, was about ~RMB 171bn in 2020. It is estimated to grow at a CAGR of ~21%, reaching ~RMB 446bn by 2025.

While the TAM for online / mobile recruitment is substantial at RMB 54bn suggesting a long runway for BZ in terms of growth, I think BZ’s value proposition extends beyond job recruitment. Most internet companies in China are consumer-facing, and the few exposed to enterprise customers operate in selected fields such as the cloud. This makes BZ unique given its enterprise user base of 3.7m, a ready customer base for BZ once it starts to expand beyond job recruitment.

I believe in the future BZ will explore potential complementary fields. It is still early days, but I think possibilities include HR-related services such as payroll/ training, similar to a Workday-type model, or professional social networks, similar to LinkedIn. LinkedIn recently exited China after having achieved lackluster success in recent years. The leading social network “super app” in China is obviously Wechat. But Wechat tends not to be overly business-centric, and a Chinese version of a LinkedIn-like app could fill this gap. I believe BZ management is not planning on expanding beyond job recruitment in the next 2-3 years, but these new fields could offer meaningful growth options to BZ.

More than just recruitment as it taps into the enterprise sector

While the TAM for job recruitment in China is sizable at RMB54bn (as of 2020), BZ’s most valuable asset is arguably its ~4 million-strong enterprise and SMB paying customer base. China has an established internet industry, but few are enterprise-facing or have a large enterprise customer base, because there is no home-grown enterprise software or IT hardware industry. BZ is exploring expansion opportunities, and I believe management is evaluating new markets to leverage this enterprise “install base”, while it remains focused on its core offering (job recruitment) over the next 2-3 years. Potential avenues include other HR-related online functions such as training and payroll (think Workday) or professional social networks (similar to LinkedIn).

Pain points for the online recruitment market

The company has identified major industry-wide pain points that limit the efficiency of job matching between job seekers and employers. First, BZ believes the traditional search-based online recruitment model would naturally favor large enterprises and the highest-tiered candidates, leaving SMEs and average candidates behind. That is, search results would recommend SMEs to target top-tier candidates demanding a high level of compensation that only large corporations can meet, or average candidates for job openings from top-tier enterprises that they may not be qualified for. In other words, a search model is not the best solution for increasing the match rate on platforms. Additionally, BZ believes that the traditional recruitment process, which rarely includes managerial-level involvement (executives, middle-level managers, business owners) at the early stage, may cause suitable candidates to be overlooked due to a lack of understanding of the actual job requirements by HR personnel.

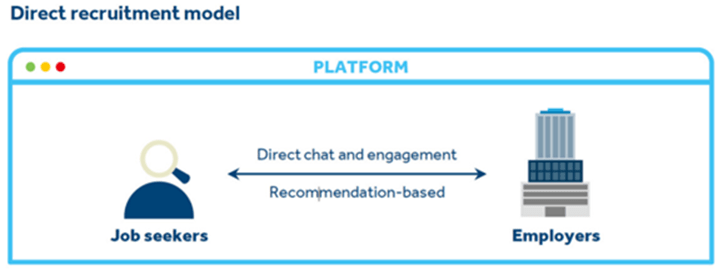

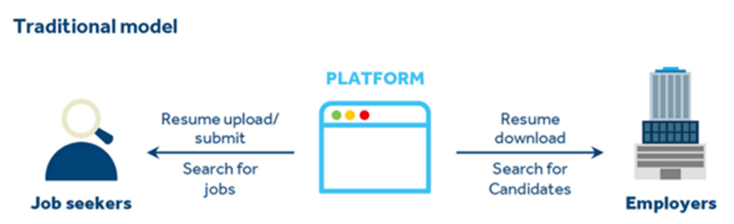

Direct Recruitment Model (Company Presentation) Traditional Model (Company Presentation)

BZ champions the direct recruitment model, which means 1) direct communication between job searchers and hiring managers, 2) the usage of an AI-based recommendation system to facilitate more direct matches between a candidate and an employer.

The essence of BZ’s direct recruitment model is that, although BZ acts as an intermediary between candidates and hiring enterprises, it believes it successfully reduces friction for all parties involved in the entire recruiting process. Through BZ, candidates and enterprise representatives would reach out via an in-app instant messaging system for preliminary conversations on the key issues without going through the traditional process of “sending and reviewing a resume, setting up time for a call, and having formal interview”, thus greatly speeding up the initial screening time needed for candidates and enterprises. Candidates can send their resumes and schedule further interviews after their initial chat.

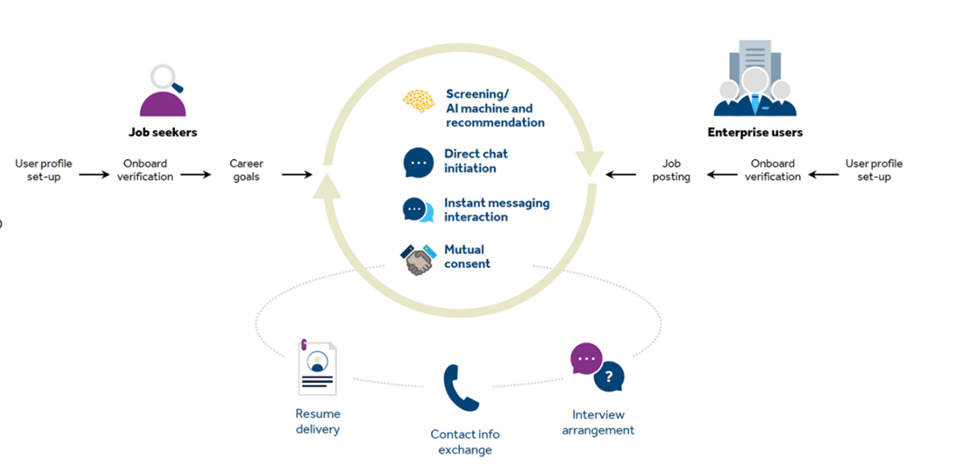

BZ’s recruitment model (Company Presentation)

Although BZ’s major competitors, such as 51Jobs and Zhaopin have recently adopted its unique features such as direct chat, the company argues that the biggest differentiator is its recommendation algorithms, which are used to proactively match candidates with enterprises, and solves the aforementioned imbalance among enterprises of different sizes and the candidate pool. BZ’s competitors on the other hand, have lagged in this functionality, and tend to rely on revenue generated from keyword bidding on their search engines.

Valuation

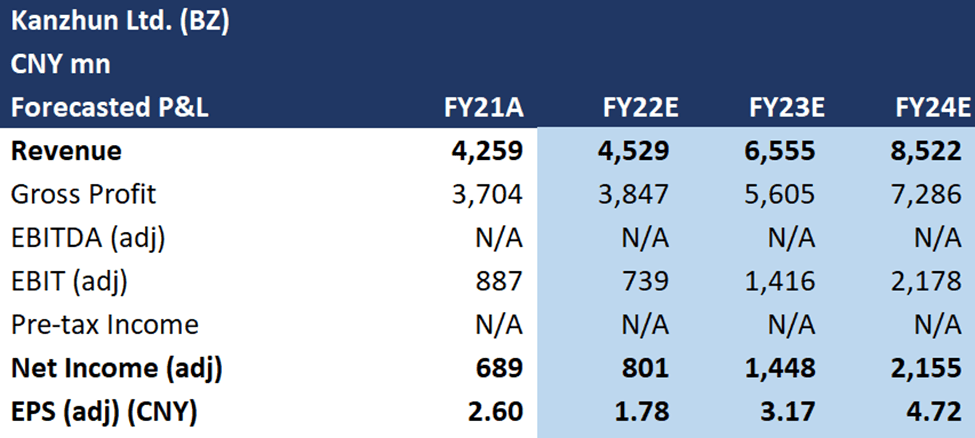

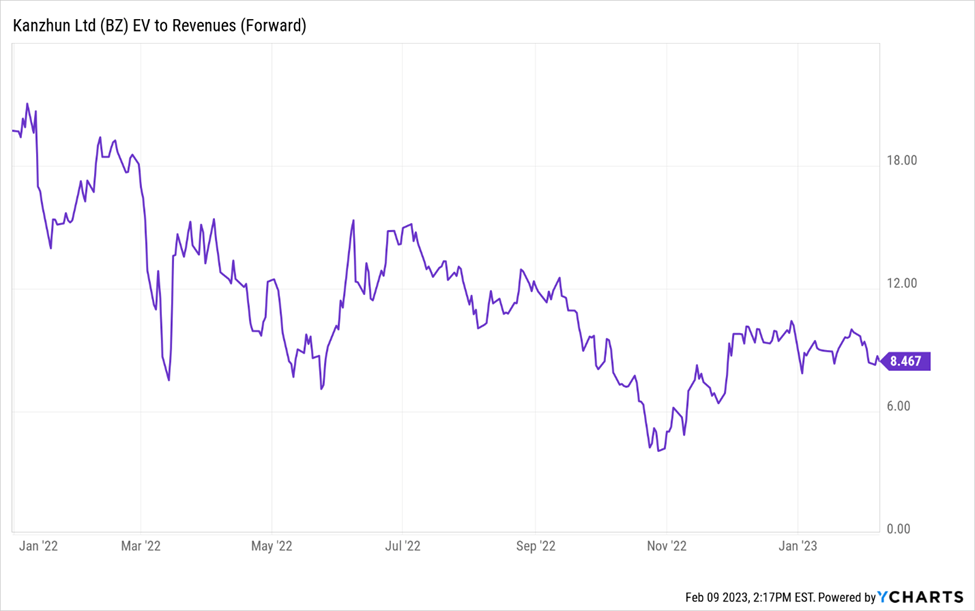

I am valuing BZ on a EV/S basis. Based on FY23E total revenue of RMB 6.6bn, EV of $7.9bn and my target EV/S multiple of 12x, I reach a target market cap of $14.3bn, or $33 per share. BZ has been trading at a premium to China Tech comp group due to its higher growth and steady profitability profile, and I think such a premium is likely to stay as the company manages to continue with its growth and maintaining its profitability level.

Additionally, BZ not only trades at a premium to the broader China Tech group, it also trades at a premium to its direct peers. The market has always given BZ a sizable valuation premium due to its higher growth and profitability profile. As I forecast BZ’s growth to re-accelerate to ~50% yoy going into FY23, I see this trend continuing.

BZ P&L Snapshot (my estimates) BZ Forward EV/Sales (Ycharts)

Final Thoughts

BZ is a mobile-focused online recruitment platform with an industry-leading user and enterprise user base that is poised to grow, leveraging its algorithm-based recommendation engine to match job seekers and employers with high efficiency. Opportunities to enter into adjacent online HR markets offer more growth options. I remain bullish on the company’s medium to long-term prospects given its unique positioning, growth potential, and highly profitable business model (20%+ Non-GAAP net margins already). My December’23 price target of $33 is derived by applying a 12x EV/S multiple to my FY23E revenue estimates.

Be the first to comment