Angelika Heine/iStock via Getty Images

To many investors, there likely isn’t much that could be considered high-tech when it comes to food. But one company that begs to differ on this matter is John Bean Technologies Corporation (NYSE:JBT). By focusing on what it calls the FoodTech market, as well as having a nice niche carved out for itself in the aviation support market, the company has grown to be a rather interesting firm with a sizable market capitalization of $3.24 billion. Over the past few years, financial data reported by the company has shown some signs of weakness. Mixed financial results seemed to be the norm when it comes to this particular enterprise. In the long term, I suspect that the company would do just fine for itself. But for now, between its mixed financial data and how shares are currently priced, I believe that it makes for only a ‘hold’ candidate at this time.

Two businesses in one

According to the management team at John Bean Technologies, the company is comprised of two operating segments. The first of these is called JBT FoodTech and, as its name suggests, it has to deal with the intersection of with food and technology. Within the segment are three comprehensive solutions that warrant attention. The first management refers to as its Protein category. Under this, the company produces and sells primary, secondary, and further value-added processing, mixing, grinding, injecting, marinating, tumbling, portioning, packaging, X-ray, and a variety of other food inspection and safety solutions. Under the Diversified Food & Health category, the company focuses on offerings that include processing, preserving, and packaging for a variety of foods. They also aid in sterilizing, pasteurizing, concentrating, sealing, and other activities. And under the Automated Guided Vehicle Systems category, the company produces robotic systems for a wide variety of activities like manufacturing, warehouse storage, and more. Combined, this segment is responsible for about 75% of the company’s revenue and 85.2% of its profits.

The second, much smaller segment is called JBT AeroTech. This largely centers on solutions and services dedicated to domestic and International Airport authorities, passenger airlines, air freight and ground handling companies, defense forces, and defense contractors. Under this, the company has three main categories of products. The first would be Mobile Equipment centered around mobile air transportation, the second includes Fixed Equipment such as gate equipment for passenger boarding. And the final includes Airport Services that mostly revolves around the company maintaining and enhancing airport equipment, systems, and facilities. This segment makes up around 25% of the company’s revenue and 14.8% of its profits.

Author – SEC EDGAR Data

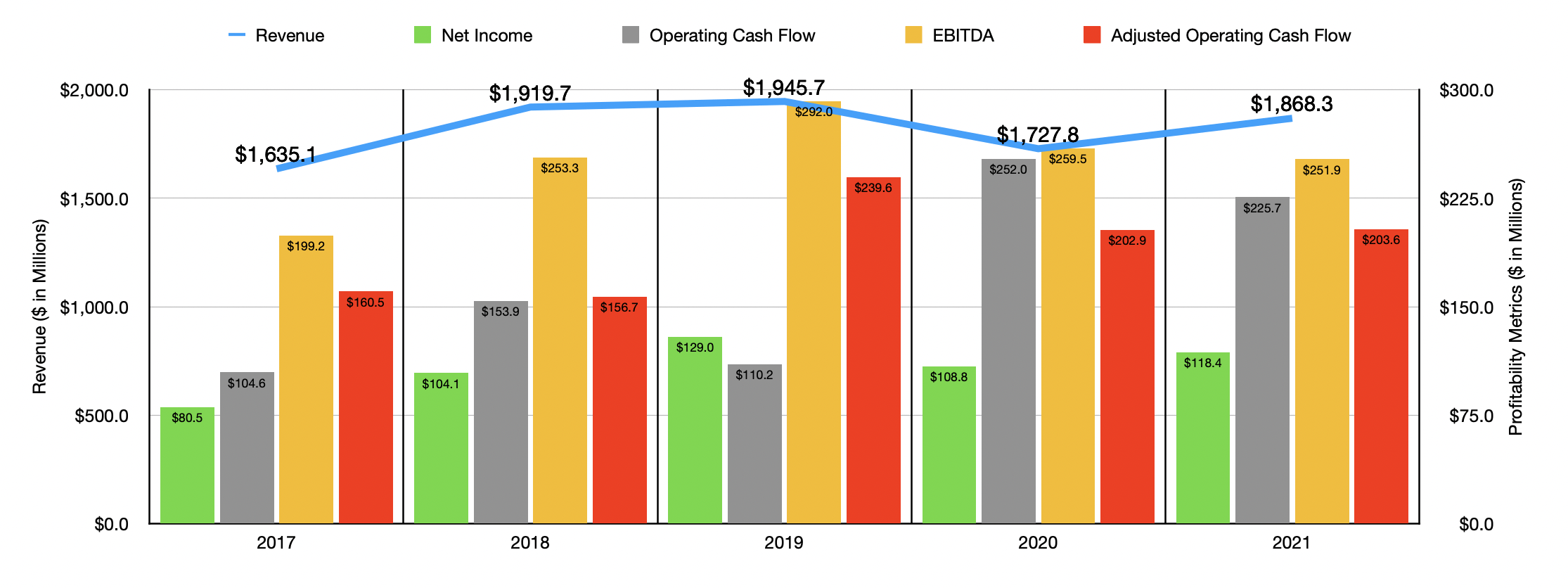

Over the past few years, the financial picture for the company has been rather rocky. Between 2017 and 2019, sales increased year after year, rising from $1.64 billion to $1.95 billion. The pandemic was responsible for pushing revenue down to $1.73 billion in 2020 before the company experienced a partial rebound to $1.87 billion in 2021. From 2020 to 2021, the roughly 8% increase in revenue was driven largely by a 5% rise in organic revenue. The company also benefited to the tune of 2% from acquisitions and a further 1% from foreign currency translation. Organic revenue, management said, was driven largely by higher equipment revenue from its FoodTech segment, some of which was offset by lower equipment revenue from the AeroTech segment that was caused by delays in shipments thanks to supply chain issues and labor shortages.

The trend for net income for the company has looked very similar to the trend for revenue. Between 2017 and 2019, profits rose from $80.5 million to $129 million. Profits then dropped to $108.8 million in 2020 before hitting $118.4 million one year later. Other profitability metrics have not been as stable. Operating cash flow, which is my personal favorite metric, actually bounced around in a fairly narrow range between 2017 and 2019, going from a low point of $104.6 million to a high point of $153.9 million. In 2020, cash flows surged to $252 million before dipping to $225.7 million in 2021. If we adjust for changes in working capital, operating cash flow would have actually peaked at $239.6 million in 2019. After plunging to $202.9 million in 2020, the metric inched up in 2021 to $203.6 million. When it comes to EBITDA, the picture looks last appealing. After hitting a high of $292 million in 2019, the metric fell to $259.5 million in 2020 before falling further to $251.9 million in 2021.

Author – SEC EDGAR Data

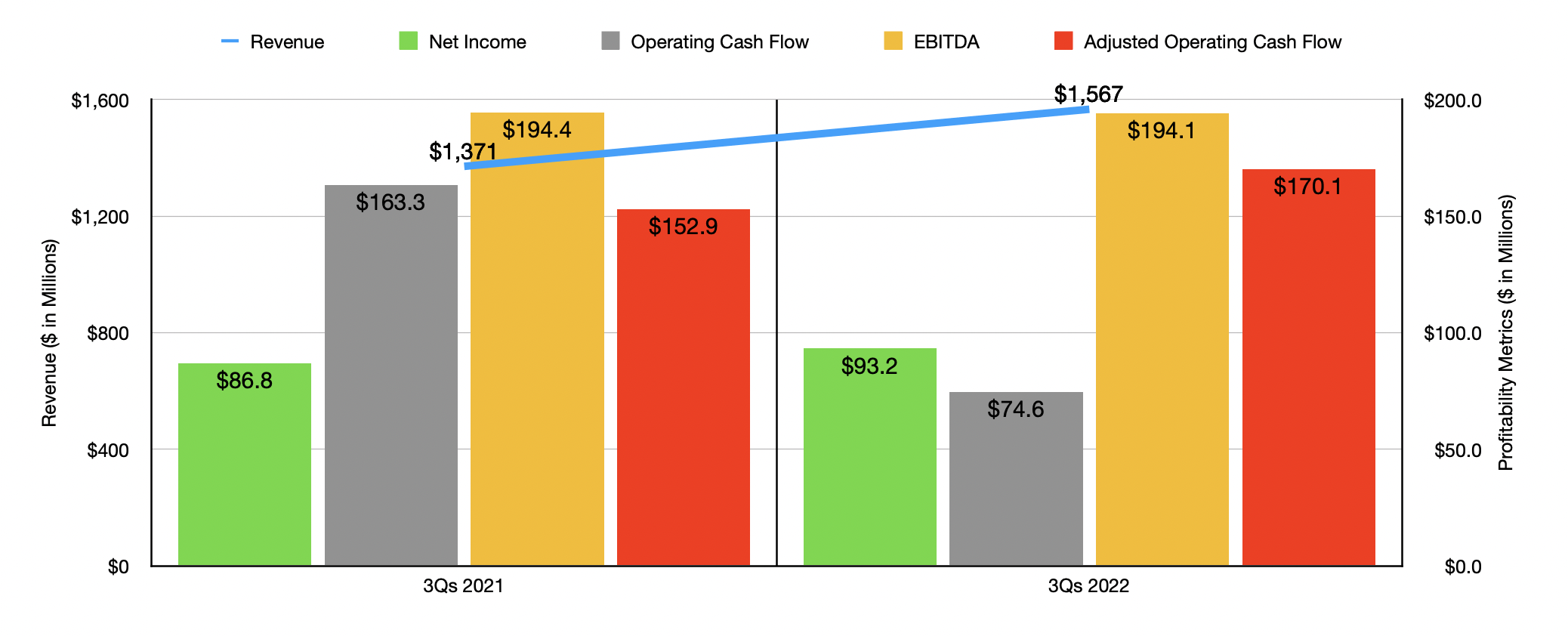

When it comes to the 2022 fiscal year, the picture has been something of a mixed bag. Revenue for the company surged, jumping to $1.57 billion for the first nine months of the year. That’s 14.3% higher than the $1.37 billion reported one year earlier. During this time, the company benefited from a $195.9 million increase in organic revenue. Acquisitions engaged in by the company added another $55.8 million to its top line. Unfortunately, sales were hit hard by a $55.5 million impact associated with foreign currency fluctuations. Had this not been an issue, revenue would have risen by 18.4% year over year instead of the 14.3% it ultimately did. On a percentage basis, the greatest growth for the company came under its JBT AeroTech segment. Revenue there jumped 23.2% thanks largely to a $52.5 million rise in sales associated with its mobile equipment business. This, management said, was driven by higher equipment sales to cargo and other customers, as well as higher aftermarket sales thanks to the aviation industry’s continued recovery from the COVID-19 pandemic. This is not to say that JBT FoodTech did not fare well also. Sales there jumped 11.4% year over year, with organic revenue adding $115.4 million to the company’s top line while acquisitions contributed $55.8 million. On the organic side, management said that recurring revenue was largely responsible for the increase.

On the bottom line is where things are somewhat mixed. Net income, for instance, rose modestly from $86.8 million to $93.2 million. But operating cash flow plunged from $163.3 million to $74.6 million. The good news here is that, if we adjust for changes in working capital, the metric would have actually risen from $152.9 million to $170.1 million. As for EBITDA, we saw a modest decrease from $194.4 million to $194.1 million. Clearly, the company suffered from a decrease in margins during this time. The segment operating profit margin for JBT FoodTech declined from 13.8% down to 12.8%. This was caused by continued supply chain disruptions and pressures resulting in inefficiencies that pushed material, freight, and labor costs all higher. We also saw the JBT AeroTech segment see its profit margin fall from 8.6% to 6.8%. This, management said, was driven higher by increased material, labor, and freight costs as well.

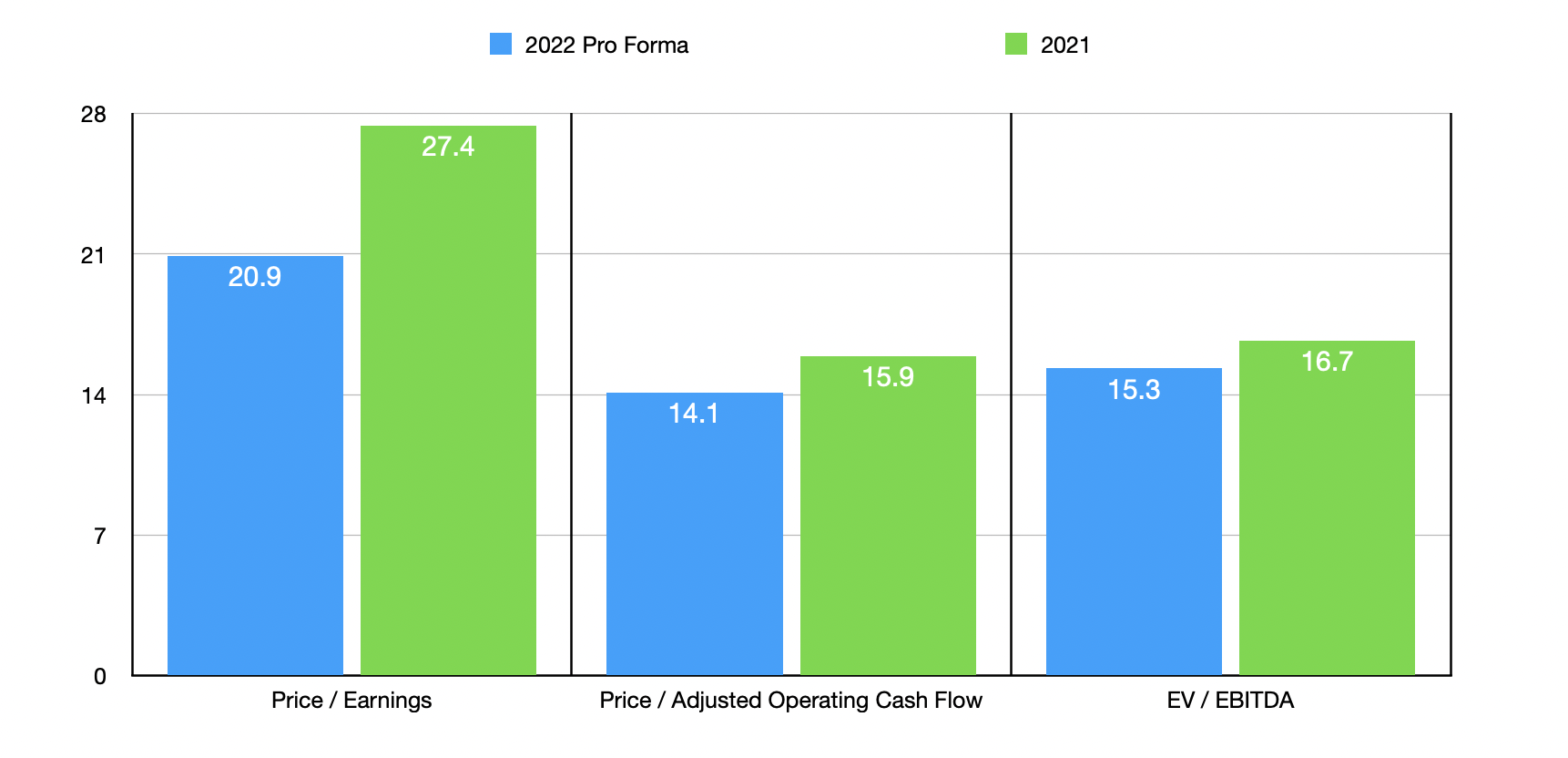

When it comes to the 2022 fiscal year in its entirety, the company is forecasting earnings per share of between $4.65 and $4.80. But it’s also important to note that the company recently completed its acquisition of a company called Bevcorp in a deal valuing it at $290 million. Revenue for that enterprise next year should be around $85 million to $90 million. And the adjusted earnings per share contribution toward John Bean Technologies’ profits should be between $0.08 and $0.12. Based on estimates from management, the EBITDA for that entity should be around $21 million. if we make some reasonable assumptions regarding this acquisition and factor that data into the company’s 2022 data to create a pro forma picture of the enterprise, we should anticipate net income of around $154.9 million, adjusted operating cash flow of $229.7 million, and EBITDA of $272.5 million.

Author – SEC EDGAR Data

Based on these figures, John Bean Technologies seems to be trading at an adjusted forward price-to-earnings multiple of 20.9. The adjusted forward price to operating cash flow multiple should be a bit lower at 14.1, while the adjusted forward EV to EBITDA multiple should come in at 15.3. For context, in the chart above, I also showed pricing for the company’s 2021 fiscal year. As part of my analysis, I also compared the company to five similar firms. On a price-to-earnings basis, these companies ranged from a low of 5.7 to a high of 94.7. And when it comes to the EV to EBITDA approach, the range was from 3.7 to 30. In both cases, three of the five companies were cheaper than John Bean Technologies. Finally, using the price to operating cash flow approach, the range was from 5.7 to 41.5. In this case, only one of the five companies was cheaper than our target.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| John Bean Technologies | 20.9 | 14.1 | 15.3 |

| SPX Technologies (SPXC) | 94.7 | 41.5 | 30.0 |

| Hillenbrand (HI) | 15.5 | 17.0 | 8.5 |

| Albany International (AIN) | 31.6 | 24.6 | 15.4 |

| Gates Industrial Corporation (GTES) | 18.2 | 19.2 | 10.6 |

| Mueller Industries (MLI) | 5.7 | 5.7 | 3.7 |

Takeaway

Based on all the data provided, I will say that John Bean Technologies seems to be recovering steadily from the COVID-19 pandemic. The firm still has some issues related to supply chain disruptions. But that’s to be expected. In the long run, I expect the company would do just fine for itself and its shareholders. On top of that, shares don’t look unreasonably priced compared to similar firms. But given where we are in the economic cycle and how shares are priced on an absolute basis, I think that the company makes for a much better ‘hold’ candidate today than it does a ‘buy’ one.

Be the first to comment