Tyler Durdan/iStock via Getty Images

Korean Giant POSCO Signs MOU With Jindalee

Being that Lithium Americas (LAC) has won the first battle of the Thacker Pass court case, it might be time to explore Jindalee Resources (OTCQX:JNDAF) (JRL.ASX) as they are a neighboring project north of LAC. Evidently Korean company POSCO (PKX) agrees as they signed a non-binding MOU to conduct testing on Jindalee Resources lithium. In this article we will explore Jindalee and see if they make sense. If POSCO is exploring the asset we might need to also kick the tires to see if this company is a buy or not. First off where is the project located?

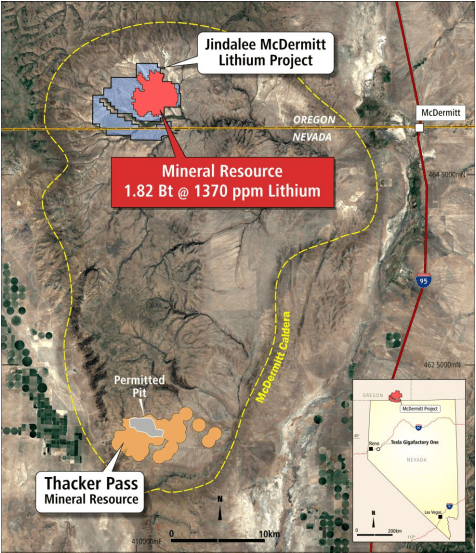

Lithium Americas and Jindalee Share the Same Extinct Volcano

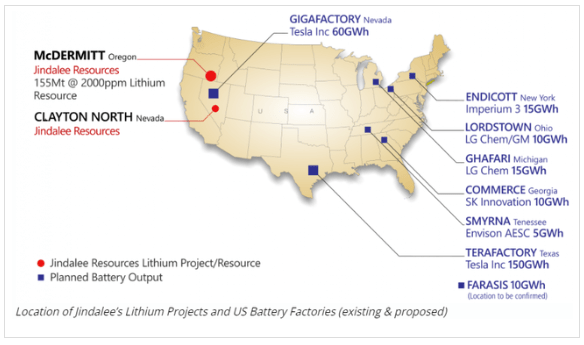

Jindalee has two projects in the United States.

Projects Overview (Jindalee Resources)

One is north of Clayton Valley where Albemarle (ALB) and Century Lithium (OTCQX:CYDVF) are located. The other is north of Lithium Americas and this is the one we will explore in this article.

Jindalee and Lithium Americas share the same caldera (extinct volcano). Granted I’ve been told by a geologist friend that the clay types are different for each company (with Jindalee having a harder one to work with) but maybe they can make it work. I’m sure POSCO will either determine if it is possible or not. Below we can see the location of the lithium asset. Do note Jindalee is advertising its total inferred and indicated resource size below in red (aka its guess and its probable estimate).

Jindalee Land Holdings (Jindalee)

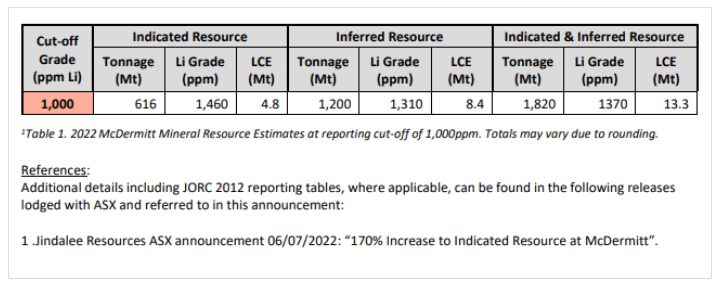

Jindalee Lithium Resource Estimate

Per below, note the resources are quite large for Jindalee.

Jindalee Resource Size (1,000 ppm cut off) (Jindalee 2/12/2023 PR)

Do note the 1,000 mg/l cut-off grade and the various estimations. The take-away is the company is sitting on a large and lithium-rich project.

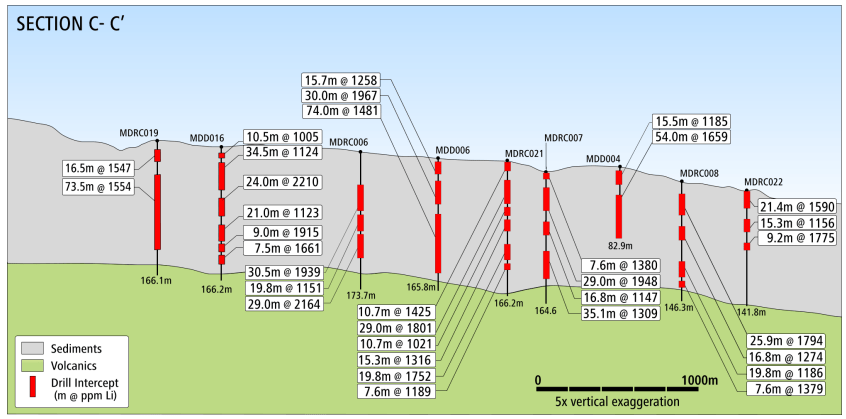

Jindalee Resource Depth

Having a potential resource is nice but can you actually get to it? Shallow is better as opposed to resources that are deep. Below we can see the depths of the resource are not too deep as they range from the surface and extend to 208 meters. Per the IR slide deck, we see different sections of the property:

Jindalee Depth of Mineral Resource (Jindalee)

and

Jindalee Depth of Mineral Resource (Jindalee IR Deck)

Logistics

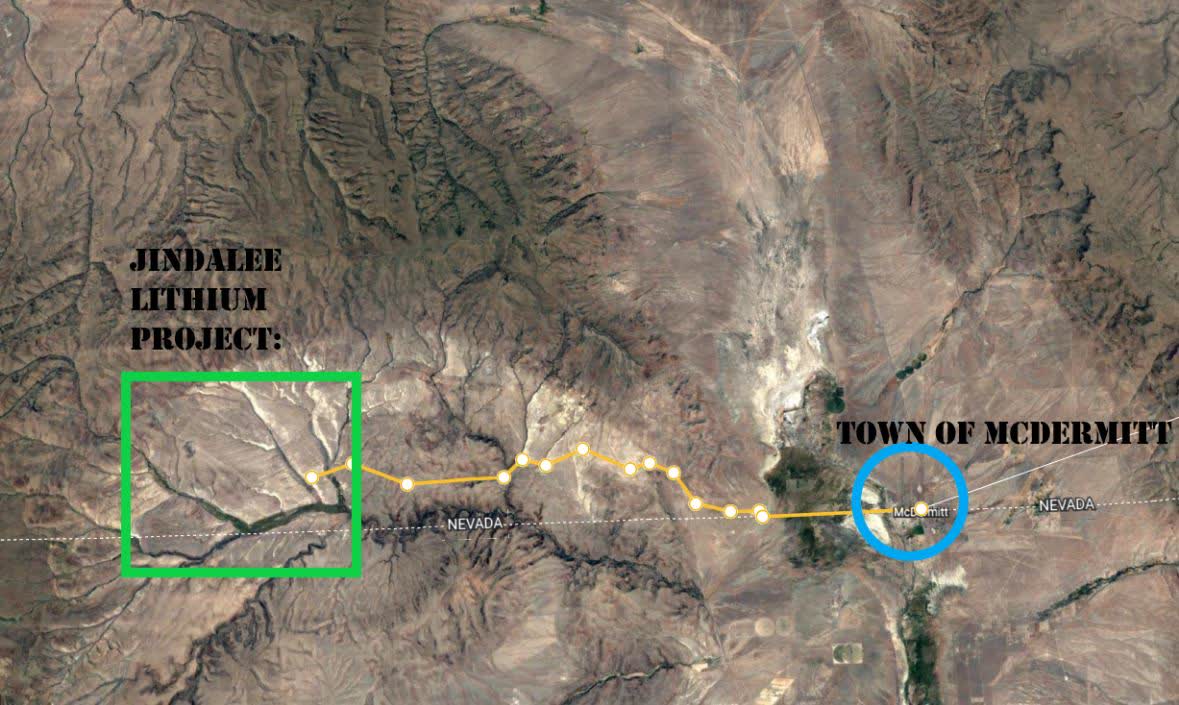

In the graphic below is the small town of McDermitt. At roughly 500-600 population it offers the basics. The yellow line is a simple dirt road for the majority of it before it hits a paved road. The green square is a rough projection of where the project will be per the author. Much like Thacker Pass, nothing is near this project which is both good and bad. Logistics wise, road and power sources will have to be built along with establishing a labor force.

McDermitt Lithium Project (text & graphics are the authors) (Google Earth)

McDermitt Lithium Project

For a project to work you must have a few things:

1. An actual resource. Higher the lithium grade the better.

2. Land, you need land that can support a pit and a tailings area. If your land mass is too small you may not physically be able to see a project go to production. Also, the resources being on flat land and / or near the surface are a bonus.

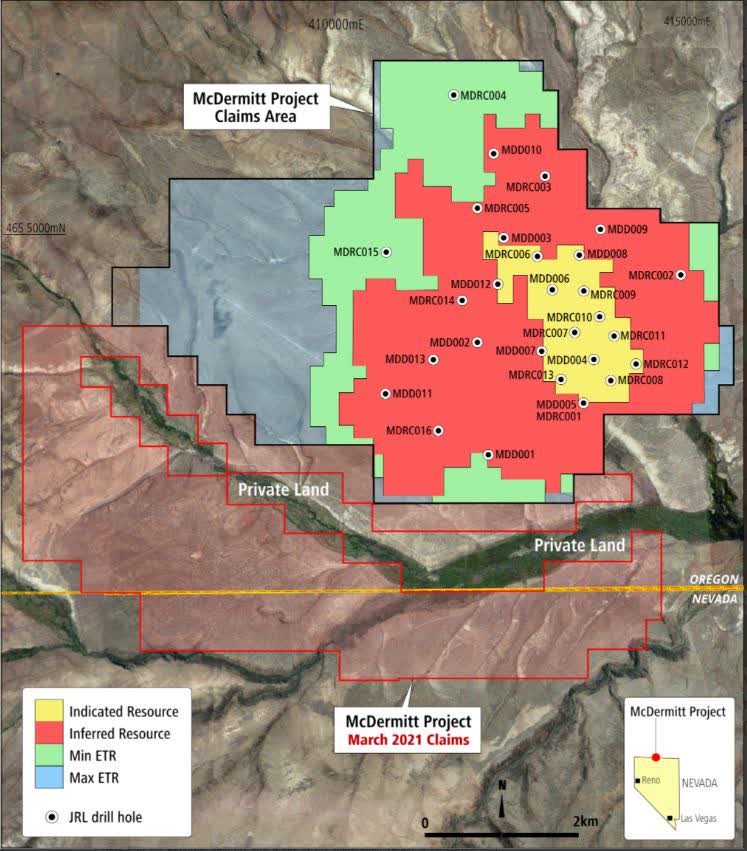

Looking at the McDermitt project below, we see they own quite a swath of land that borders the Oregon / Nevada border.

McDermitt Lithium Project (Jindalee)

Now large swaths of land by itself mean nothing. You can find tons of small-fry lithium plays that are advertising monstrous land holdings, but if that land has little-to-no lithium then they are in a pickle.

Continuing with our list of things you need for a property to work:

3. It is preferable that a project lacks endangered species.

4. Water rights: Those that lack water are at the mercy of those that possess water. It is that simple.

5. Favorable government: Oregon is a fractured state. Western Oregon is very liberal; eastern Oregon very conservative. Getting approval therefore is going to be more difficult than say in Nevada. Nevada offers a very mining friendly state government and the U.S. (from the federal side) is slowly improving in its support of domestic lithium efforts.

6. Funding. Without hard cold cash a project can linger in purgatory.

7. Infrastructure: A mining project needs power, roads, and a local work force. Lower elevations are preferable as opposed to 12,000+ feet (which some South American projects suffer from). Rail or a gas line is an added bonus. Without power, roads, or a local work force a project can incur much higher costs trying to evolve to a higher-mining lifeform.

The Success of Thacker Pass Might Rub off on Jindalee

As we discussed in our prior article, Lithium Americas subsidiary Lithium Nevada is moving forward in trying to obtain government loans. If the share price of LAC were to rise north in response to government funding, investors might look for related projects. Hence, Jindalee could benefit from the success of LAC.

Soaring Lithium Demand

Price of lithium has gone up quite rapidly. At some point you have to question at what point do additional big automakers break from the pack and buy a lithium miner or get in bed with one much like General Motors (GM) just did with LAC. Additional vertical supply chain integration would not hurt. Would this trigger other carmakers to secure supply? Perhaps.

Concerning prices and lithium: At this point carmakers simply have to bite the bullet and embrace electric cars or be left in the dust. They are doing this and passing some of the costs to consumers, but long term the lithium challenges will be resolved via a combination of new mines and lithium recycling.

Jindalee Risk

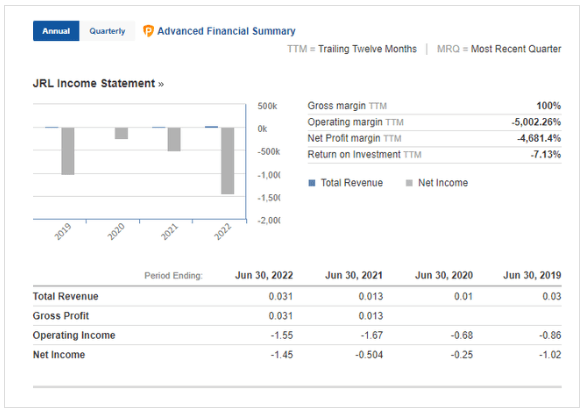

No project is without problems; Jindalee has a few. First, it is located in Oregon. Western Oregon is rather liberal while eastern Oregon is very conservative. However, Oregon politics are dominated by the liberals and this could pose an issue for mine permitting. The second issue is the stock trades in Australia (primarily): The US ticker symbol has almost non-existent volume. Last but not least, we should expect some sort of protesters if the project gets closer to permitting or production much like we saw with LAC. Another point we need to look at is how much cash and debt are on hand along with the burn rate. Per Jindalee the company has $3.3 million in cash and $4.5 million worth of share in two Australian companies. The burn rate was $1.45 million in 2022.

Jindalee Burn Rate (Investing.com)

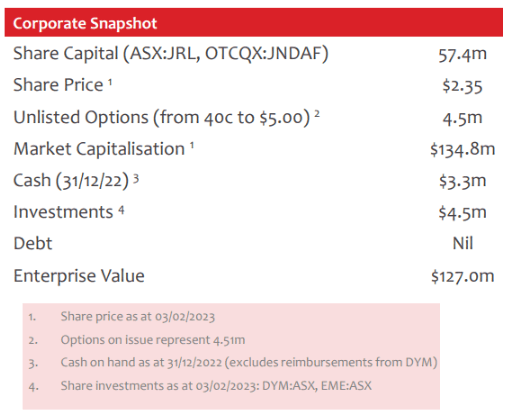

The cash on hand is enough to keep the lights on, and with a market cap of $127 million AUD they could raise additional capital if need be to conduct drilling programs. It is probable the company will raise additional capital by selling shares sometime in 2023. Historically this is how they have funded the operations. Debt is Nil.

Jindalee Cash and Debt (Jindalee )

Insider Ownership of Jindalee and Cash

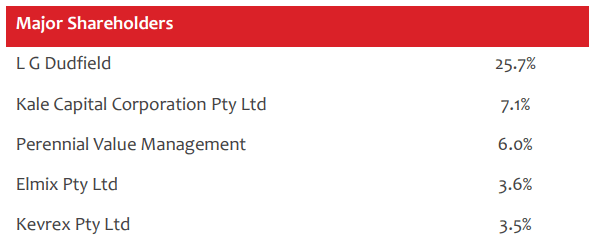

Seeing insiders own a percentage of a project is good or even if that value is low if you see insiders making purchases this can be a sign they believe in the direction of the stock. Granted sometimes they need to sell stock to offset options or pay taxes. The point is watch the insiders. In this case the CEO Mr. Dudfield owns a very large chunk of the company. That is skin in the game.

Major Owners of Jindalee (Jindalee)

Summary

While Jindalee indeed has massive resources, it is not without risk. I would currently rate this one as a speculative mild buy or a watch and hold based on a massive resource that has limited capital and maybe a tough clay to work with. The biggest problem might be the majority of the project is in Oregon. The company’s cash reserves are low as well. Yet considering the POSCO news, this might be one to watch with interest just to see what POSCO determines. Overall rating: Mild buy to watch and see.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment