FangXiaNuo

JD.com, Inc.’s (NASDAQ:JD) asset-heavy model with self-owned inventory and logistics, as well as its proprietary logistics services, provides a competitive advantage. I believe that competitive advantage would allow the company not just to grow revenues but expand margins. I value the shares at USD 90 per ADS.

Strong Q3 2022 Financial Results

In November 18, 2022, JD reported strong financial results for Q3 2022, with net revenues of RMB243.5 billion, an increase of 11.4%. The net service revenues were RMB46.5 billion, an increase of 42.2% YoY. JD’s income from operations was RMB8.7 billion, an increase of 235% YoY. Non-GAAP income from operations was RMB9.9 billion, compared to RMB4.6 billion. Operating margin was 5.2%, an improvement of 120 bps. Operating cash flow for the twelve months ended September 30, 2022 was RMB45.8 billion, an increase of 12%. Free cash flow was RMB25.8 billion, a decrease of 9% . JD also reported a 6.5% growth in annual active customer accounts to 588.3 million. During October, China’s zero-COVID-19 policy had an impact on JD’s business model but JD’s CEO said that he believed the worst is basically over on the Q3 earnings call.

JD’s Asset-Heavy Model and Logistics Network: A Competitive Advantage

To disrupt China’s retail industry, JD has been offering genuine products at competitive prices with a focus on prompt delivery. Unlike Alibaba (BABA), JD has an asset-heavy model with self-owned inventory and logistics. JD’s increasing scale is expected to grant it bargaining power towards suppliers and volume-based rebates. As JD shifts towards a higher-margin third-party platform business and gains efficiency from scale, its margins are expected to increase. Also JD’s management is currently investing heavily in supply chain management, integrated warehouses, and delivery services to penetrate less developed regions. JD’s proprietary logistics services provide a competitive advantage in the e-commerce market.

JD Logistics’ Expansion into High-Frequency FMCG Categories Drives Revenue Growth

In Q3 2022, JD Logistics maintained its revenue growth by providing integrated supply chain solutions and partnering with leading players in various industries such as FMCG, home appliances, furniture, apparel, and fresh produce. The company’s upstream and downstream industry partnerships enabled them to support enterprise customers by mitigating risks and optimizing cost and efficiency. Therefore, JD Logistics’ potential to maintain growth through partnerships and supply chain solutions may positively impact its future financial performance.

The CEO, Lei Xu, elaborates on this during the earning call:

Despite the challenging environment, JD Logistics continued to provide up- and downstream industry partnering with reliable integrated supply chain solutions, supporting enterprise customers to mitigate risks, respond to rapid external challenges and optimize cost and efficiency. In Q3, JDL also expanded the depth and breadth of collaborations with a variety of leading players in FMCG, home appliance, furniture, apparel, 3C, automobile and fresh produce industries. As a result, JDL maintained a resilient revenue growth in this quarter.

The company’s expansion into high-frequency FMCG categories has proven to be a successful strategy, with JD becoming the largest supermarket in China. These categories have also allowed JD to attract new customers from less developed areas, creating an opportunity to drive sales of other categories.

Valuation

Based on my analysis, I have arrived at a fair value of USD 90 per ADS. I anticipate that JD’s revenue will continue to grow at a high rate of ~20% until 2027, after which I expect it to slow down to high single digits. This growth is supported by JD’s omnichannel strategy. Moreover, I believe that JD’s margin will expand due to its asset-heavy business model, JD direct sales, and marketplace. Also, the company’s entry into logistics may have a medium-term impact on margin expansion. In the long run, I expect JD’s gross margin to reach mid-11%.

The USD 90 per ADS value is based on a DCF using a cost of capital of 11.4% and an unlevered beta corrected for cash of 1.33.

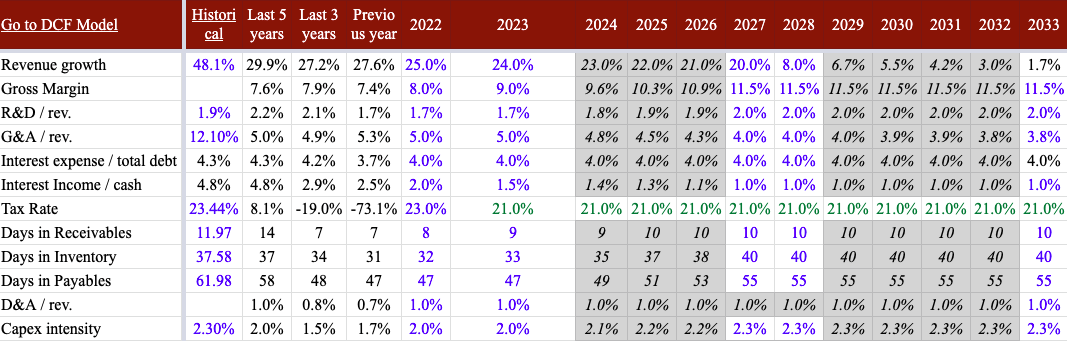

Below are my main financial assumptions used in the DCF:

Author estimates & Company filings

Risk and Uncertainties

Although JD has increased its share of China’s online retail sales, I expect competition from Alibaba and new players such as Pinduoduo to intensify. JD’s margins could be negatively impacted by new opportunities such as community group purchase and borderless retail, which may require costly fulfillment infrastructure to operate. As the company expands into lower-tier cities with lower disposable incomes and population densities, the cost of operating this infrastructure could become an even greater concern. Additionally, the increasing competition in the e-commerce industry could weigh on JD’s growth and profitability. The company will need to carefully manage these potential challenges in order to maintain its position as a leading player in the Chinese retail market.

Conclusion

JD has established itself as one of the largest B2C online retailers in China. With a wide range of authentic products and efficient delivery services, JD is a formidable competitor to other e-commerce giants in the region. JD’s competitive advantage lies in its extensive nationwide distribution network and its advanced fulfilment capacity, which would be challenging for competitors to replicate. As JD’s first-party business continues to grow and gain scale, its cost advantage would lead to lower sourcing costs and higher margins. Overall, JD’s strong distribution network, coupled with its focus on high-frequency categories, positions the company for continued growth and success in the e-commerce industry. My fair value of $90 per share offer a 73% upside from current levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment