Andrew Burton

I upgraded JD.com (NASDAQ:JD) to “Buy” in early October, saying that even with its struggles the stock had gotten too cheap and that its Logistics Unit was solid. Since then the stock has reported mediocre Q3 results, while earlier this week founder Richard Liu said in an internal memo that part of the company’s problems was mismanagement. Given that the first step in making a change is acknowledging mistakes, this is a positive. With the stock down about -5% since then, let’s catch on the name.

Company Profile

As a reminder, JD operates as both a marketplace and an online retailer in China. It also owns some offline retail brands such as JD Mall and the 7FRESH food market.

The company’s logistic unit trades separately on the Hong Kong Exchange and runs a logistics and fulfillment network with over 1,500 warehouses throughout China. Other areas of business the company is involved in include property development, healthcare, AI, and cloud computing.

Q3 Results

JD saw its sales rise 1.7% to $34.0 billion, topping the consensus by $60 million when it reported its Q3 results last month. Adjusted EPADS came in at 92 cents, beating analyst estimates of 81 cents.

Operating income in the quarter was $1.3 billion, up from $1.2 billion a year ago.

Adjusted EBITDA rose 12.4% to $1.8 billion. The company generated $2.3 billion in free cash flow.

Gross margins came in at 9.5%, an improvement from 9.0% a year ago.

Its JD retail unit’s revenues were essentially flat at $29.1 billion. Electronics and home appliance sales were flat at $16.4 billion, while marketplace revenue jumped 3.0% to $2.7 billion. General merchandise sales were down -2.3% to $10.4 billion, as it said the grocery category is still recovering. However, it did say it was starting to see higher shopping frequency and increased order volume.

Retail operating income came in at $1.51 billion versus $1.54 billion a year ago but was up slightly in RMB currency.

The company has been trying to woo customers and merchants to its platform through a large $1.4 billion (RMB10 billion) subsidy program. This quarter, the company turned to not only low prices but also expanded its free shipping program. JD lowered its free shipping minimum order from RMB99 to RMB59 for all users, which is the equivalent of going from $13.82 to $8.24. Meanwhile, it began offering its JP Plus members unlimited free shipping on all of its own merchandise.

On the marketplace side of the business, the company has rolled out a number of cost reduction measures and operating tools to support third-party merchants onboarding and operations. JD said this led to a substantial increase in its active third-party merchant base in the quarter. While commissions were down as a result of these actions, third-party advertising revenue grew by double digits.

Its JD Logistics segment saw revenue grow 19.3% to $4.5 billion. Meanwhile, operating income rose from $36 million to $39 million. The company said external customers accounted for 72% of the segment’s revenue in the quarter.

Its Dada segment, which does local on-demand delivery, saw revenue rise about 20% to $393 million, while its operating income was a loss of -$7 million, a big improvement from its loss of -$42 million a year ago. New business revenue fell -24% to $523 million as it scaled back its international business. The segment recorded a loss of -$20 million.

On its Q3 earnings call, CEO Sandy Xu said:

“I want to clarify some of the market misunderstanding here. JD is now shifting our focus away from our core competency in branded products, or serving the top tier market. On the contrary, we are further enhancing this strength by improving our price competitiveness. Also, we will never allow any bad quality or counterfeit products on JD’s platform, while we provide low price. Our low price commitment does not mean to pursue absolute low prices at the expense of other aspects of user experience, such as product quality and service. Why we need to improve our price competitiveness? Price competitiveness is the most important value proposition for retail business, and one of the most important pillars of JD’s customer centric philosophy. Our focus on price competitiveness drives us to continually strengthen our 1P supply chain capabilities, improve the efficiency and sharpen our ability to foster a prosperous platform ecosystem where healthy competition among merchants and suppliers are encouraged. All these drives better user experience, which is key to our long-term success. Both our 1P and 3P marketplace play a critical role in this.”

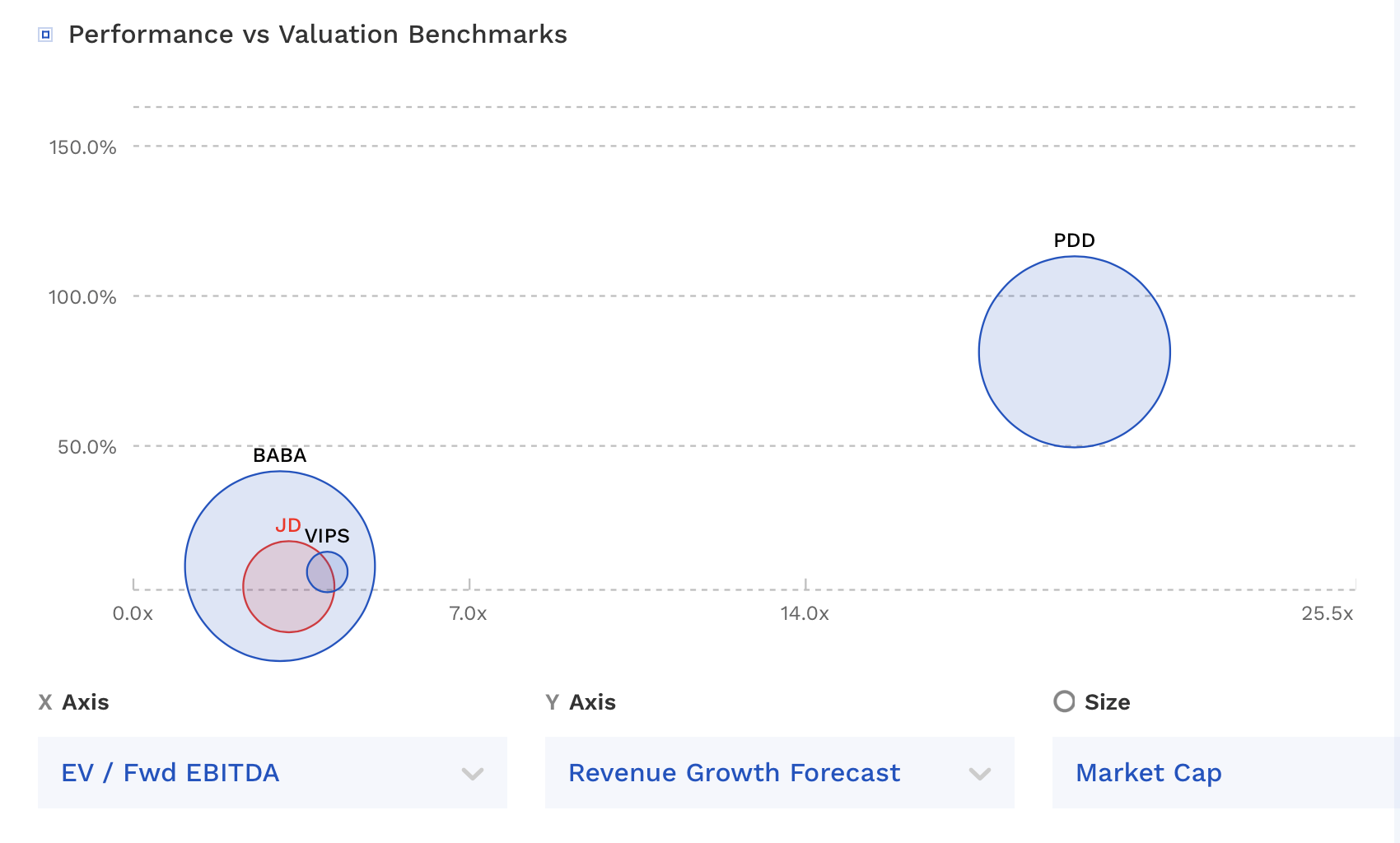

When it comes to the Chinese online retail landscape, there is a huge dichotomy between the faster-growing PDD Holdings (PDD) and seemingly everyone else, including JD. While the latter is growing rapidly, the rest of the sector has seen modest growth as PDD seemingly continues to gain share.

JD has been fighting to make in-roads, including through its third-party subsidy program, and more recently expanded free shipping, although the progress of trying to reignite growth is slow. JD it appears is trying to have higher standards for its offerings, while PDD has been highly criticized for spying on customers and for the practices of its international platform Temu. However, in Chinese online retail, PDD is considered the current winner, and everyone else is losing in the minds of investors.

As for the quarter itself, one positive is the expansion of gross margins that JD has been able to achieve in its fight to keep prices low in order to compete. With most of its sales coming from its own merchandise, JD has structurally lower margins than a pure third-party platform company. Its overall gross margins are slim, so even being able to raise them a little bit is a positive given the large volume of sales it has.

Year to date, the results from JD have been ho-hum, and Q3 didn’t really change that trend. However, I like that the founder internally has admitted that the management has made mistakes and that the company has become bloated and inefficient. This should be the first step towards change.

Valuation

JD trades at 3.2x the 2023 EBITDA of $5.84 billion and 2.8x the 2024 EBITDA consensus of $6.64 billion.

On a PE basis, it trades at 9x EPS estimates of $2.99. Based on the 2024 consensus for EPS of $3.30, it trades at 8.1x.

It’s projected to grow revenue 3% in 2023 and 7.5% in 2024.

The stock trades at a similar valuation to its Chinese e-commerce peers outside PDD, which is growing much faster than its peers.

JH Valuation Vs Peers (FinBox)

Outside of PDD, Chinese online retailers seem materially undervalued in my view. For a U.S. comparison, I’ll look at Target (TGT), which has been struggling and is expected to see flattish revenue growth this year and next. It trades at nearly 9x EBITDAR. We’ll use EBITDAR to make it more apples-to-apples.

I’ll give JD a discount for being a Chinese company, but I think a 6x multiple still seems more appropriate. That would value the stock at $40. Even if it were to come up short of those estimates and not grow at all next year, it would still be a $35 stock at that multiple. When I upgraded the stock in October, I did not place a target price on the stock.

Conclusion

At its current valuation, it’s hard to imagine not seeing JD’s stock price move higher from here over the next 5 years, barring a major black swan event such as China invading Taiwan. The company isn’t hitting on all cylinders, but it is making some improvements and it should benefit if the Chinese consumer begins to improve. I like that its founder has admitted that the company is having issues and looking to fix them. It will take time but a bloated firm can be fixed. Watch for cost-cutting measures and some improved innovation to see if the company is turning the corner.

A global recession that impacts China is a risk, but the company just got through a major Covid lockdown, so it should be able to handle it. At the same time, the company has done a nice job of keeping its prices low while improving margins. As such, I continue to rate JD a “Buy” with a conservative $35 target.

Be the first to comment