We Are

Thesis

Janus Henderson B-BBB CLO (BATS:JBBB) is a new exchange traded fund from Janus Henderson. The vehicle IPO-ed only recently, namely in January 2022. The fund focuses on investment grade BBB rated CLO tranches, and the structure is done via the exchange traded fund format. That means there is no concept of premium/discount to NAV as observed in CEF vehicles.

I like this name because it represents the same risk profile as some of the leveraged loan CEFs covered by Binary Tree. I will explain in more detail shortly, but let us have a look at BBB rated CLO tranches:

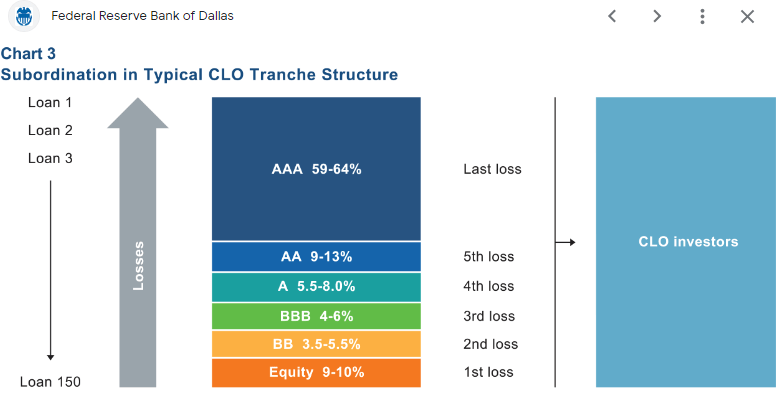

CLO Structure (The Fed)

BBB CLOs are the lowest rated investment grade paper issued by a CLO. Losses in such a structure work via the subordination, with equity absorbing the first loss, followed by BBs and then BBBs. Historical losses for BBB CLOs are extremely small:

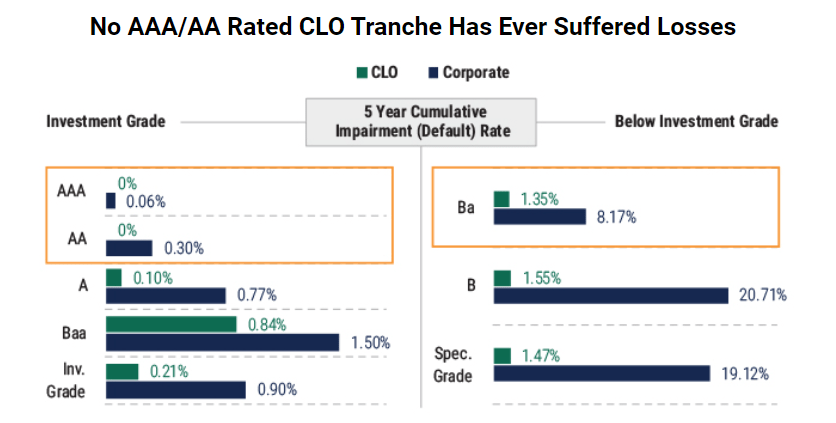

Historic Default Rates (PineBridge)

We can see from the above graph that 5-year cumulative default rates for BBB CLOs came in at 0.84%, which is lower than pure corporate paper rated BBB. That is an extremely small number, and to put it in perspective, it means that the structure would see just an 84 bps shave in all-in yield if that default rate would occur in this vehicle with zero recovery rates.

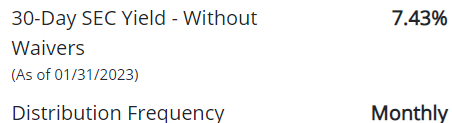

JBBB has a low duration and a 7.4% yield currently:

Yields (Fund Website)

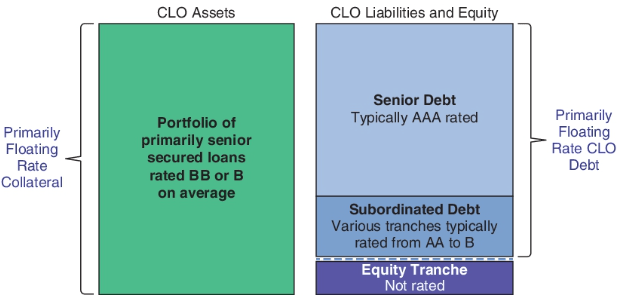

I view this name as holding a very similar risk-profile as the more popular floating loan CEFs VVR or JSD. Why? Because a leveraged loan, CEF basically represents a mezz and equity position in a pool of leveraged loans:

Simple CLO slicing (SEC filing)

In a CEF structure, the funding provider (either banks via TRSs or the preferred shares placed) represents the AAA tranche. If the CEF collateral goes south, all cash flows are going to be used to pay the funding provider first. As a shareholder in the CEF, you represent the Subordinated Debt as highlighted above. JBBB is much more honest about it – it just aggregates mezz debt directly. We can actually see from the ‘Performance’ section below that JBBB had an equivalent/slightly better performance in 2022 when compared to VVR and JSD.

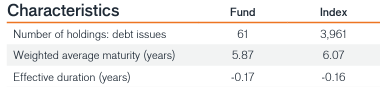

With a very low duration profile, the fund is a good pick for a rising interest rate environment:

Characteristics (Fun)

We can see from the above table the fund virtually runs no duration, and its portfolio is fairly small at only 61 names.

JBBB is a good fund, and I do not think default rates are going to spike for BBB paper in 2023, making it an attractive play. However, I believe we are nearing another top here in the market and would wait for a slight sell-off before entering this name.

Holdings

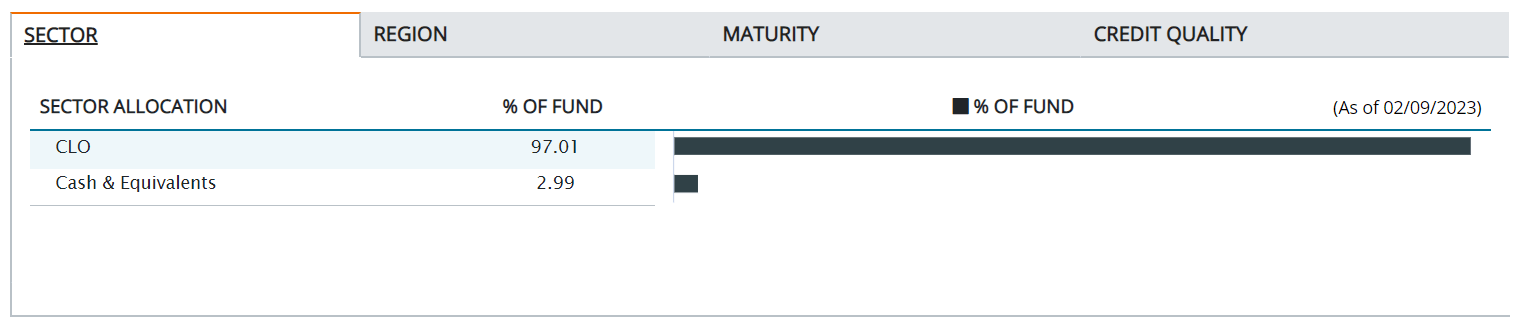

The fund holds only CLOs and cash:

Collateral (Fund Fact Sheet)

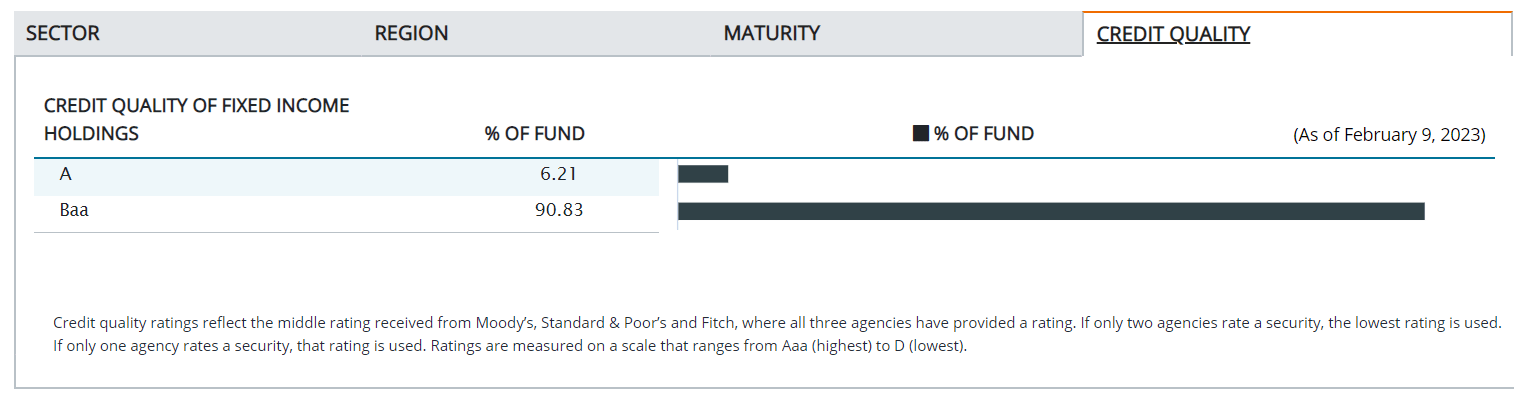

The vast majority of the portfolio is composed of BBB CLO slices:

Ratings (Fund Fact Sheet)

Credit rating migration can always occur, especially if a recession is around the corner, so we might see some of the BBBs turn into ‘BB’ in the future. The fund is as of now entirely investment grade, though.

Performance

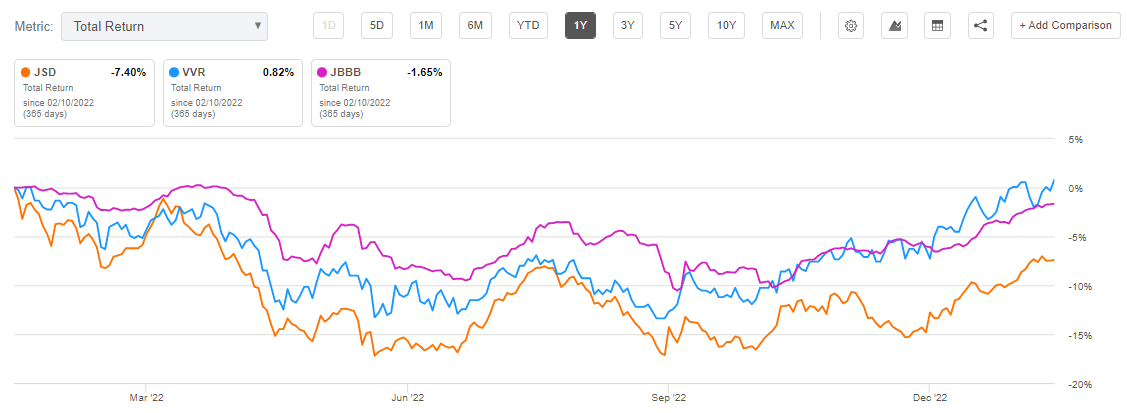

The fund has a shallow 2022 draw-down, which came in at only -10%:

Total Return (Seeking Alpha)

I am comparing JBBB to VVR and JSD here, two leveraged loan CEFs, because ultimately the structures are very similar – they both represent leveraged takes on floating rate loans. The CEF structure basically represents the mezz and equity part of a CLO (the funding providers are the AAAs there), while JBBB just outright owns leveraged pieces. As we can see from their total return graphs, the profiles are quite similar. The only difference to keep in mind is that JBBB does not really trade at a discount because it is an ETF.

JBBB IPO-ed in the beginning of 2022, so the history here is fairly limited for now.

Conclusion

JBBB is a fixed income exchange traded fund. The vehicle focuses on BBB rated CLO tranches, and represents the highest-yielding piece of investment grade debt in a CLO structure. The fund now offers a 7.4% yield paid monthly and is well set up for a rising rates environment via its duration profile. BBB CLO tranches have extremely low historical default rates, which in the worst-case scenario are only expected to shave off 84 bps from the fund’s carry profile. Think about JBBB in the same format as investing in the likes of VVR. They utilize different structures, but ultimately the risk is fairly similar, and we can see that from their 2022 return profiles. Being an ETF, JBBB does not trade at a discount to NAV. Expect the next leg down in this structural bear market to start accumulating a position here.

Be the first to comment