PrathanChorruangsak

Investment Thesis

Since its IPO, Root, Inc. (NASDAQ:ROOT) has dropped by almost 99% of its value. The company has gone on aggressive cost-cutting to mitigate the cash burn, and the efforts have shown in its financial data. If the company can stabilize its earnings and navigate through the challenges ahead, it could turn the page. But for now, we want to see more sustainable improvement on both the top and bottom lines before participating.

Company Overview

Root, founded in 2015 and headquartered in Columbus, OH, is a full-stack consumer-facing insurance technology company that uses big data and algorithms to offer personalized insurance policies and premiums based on an individual’s risk profile. The company has auto and renters insurance segments.

Strength

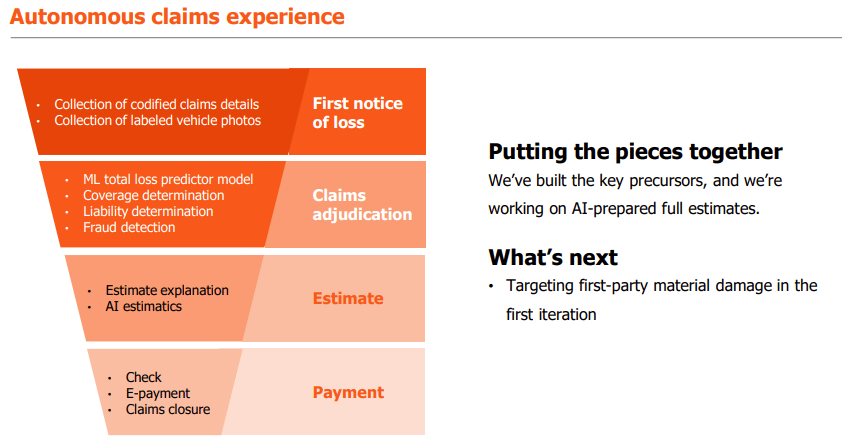

Root strives to provide a car insurance underwriting process based on the wealth of data it collects directly from the customers under permission, such as driving habits, location, and other personal information, then use AI to calculate the possible loss function and premiums to compensate for the risks. The advantage of using data and AI predictive models are making the decision process faster and more accurate as it uncovers the hidden patterns of either fraud or flags, and overall, it cuts cost and improves profitability while being all the fairer at the same time.

Root’s Autonomous Insurance Claims Experience (Root, Investor Presentation)

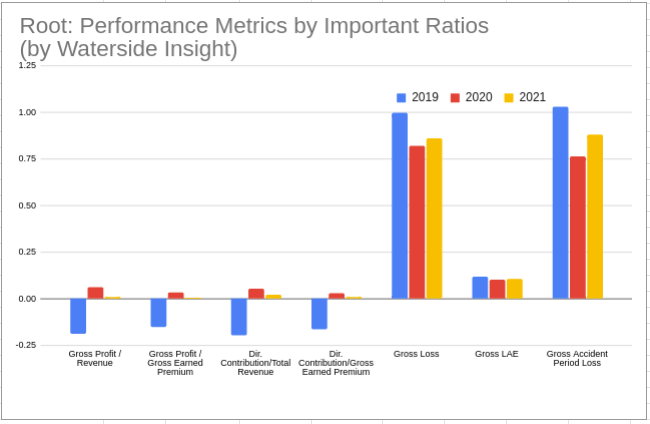

But AI isn’t perfect in predictions. It has embedded bias from either the sample or the models. And every iteration to improve could take more data to get better results, especially when the scenario it’s judging becomes complicated. But as Root grows and accumulates more data and training for the models, it should help improve performance. It seems to be the case. From the chart below, we can see Root started with less profit and more losses but has improved on all metrics since 2019, although there seemed to be some bounce back in 2021. For investors, it is important to see if there is a persistent trend of improvement.

Root Performance Metrics (Charted by Waterside Insight with data from the company)

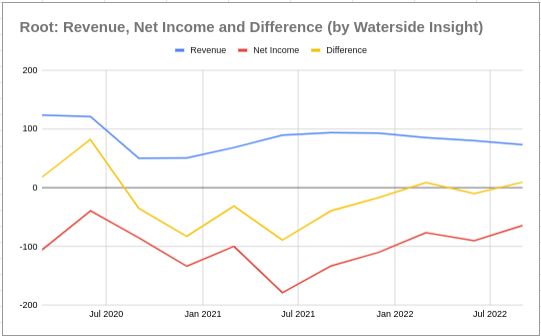

The difference between revenue and net income has risen up to slightly positive, mostly due to revenue holding steady while net income improved. This comes from two folds. The slight decline in the top line reflects its tighter underwriting in underperforming geographies and customer segments. For the improved earnings, it came from significant measures to reduce cash burn, including a 91% reduction of marketing spending YoY, due to which new business writing was reduced, and renewals made up 79% of gross earned premium. Its operating cash consumption has dropped 55% year-to-date by Q3 last year. Overall, we see Root’s efforts mainly concentrate on tightening standards, reducing premium leakage, and reducing expenses.

Root’s Revenue Vs Net Income (Calculated and Charted by Waterside Insight with data from the company)

Weakness/Risks

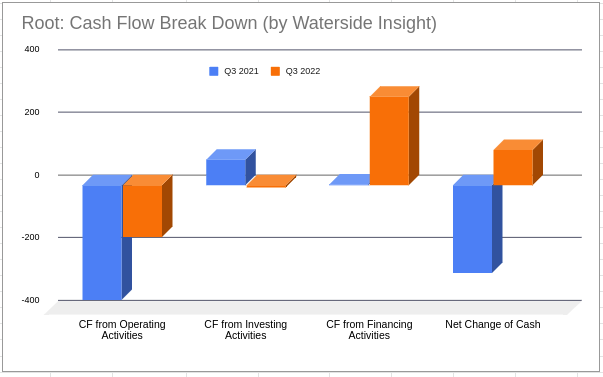

We applaud management’s decisive actions in mitigating losses and reducing expenses, Root’s free cash flow has been improving. Its operating cash flow loss was halved in Q3 last year, and the total cash flow net change was positive. However, the total positive contribution in cash flow came mostly from the debt issuance proceeds and related warrants of $286 million from financing activities.

Root’s Cash Flow Breakdown (Calculated and Charted by Waterside Insight with data from the company)

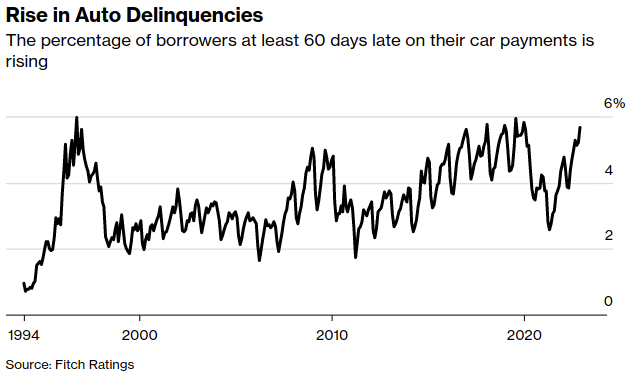

To truly improve its cash flow, Root will still need to grow its topline with a lean operation. But the macro headwind remains. The latest data suggested that auto borrowers have been late on their car payments. Could they still be keeping up with the car insurance payment or perhaps switch out to other lower payment offers in the market? There could be more impact on Root’s top-line growth this year. We think it will already be an achievement if the company can maintain a steady cash flow and earnings in 2023 on a YoY basis.

Rise in Auto Delinquencies (Fitch Ratings)

Financial Overview

Root Financial Overview (Calculated and Charted by Waterside Insight with data from the company)

Valuation

We summarize all the analysis above and use our proprietary models to assess the fair valuation of Root with a ten-year projection ahead. It is hard for us to see it coming out of the negative cash flow sustainably within five years due to its weak margin and lack of upside catalyst besides accumulative growth over time. When we add the macro headwind to the assessment, the company’s fair valuation is at $2.23, about half its current market price.

Conclusion

Root’s ambition of providing personalized, more fair insurance policies and premiums to overhaul the car insurance industry’s inefficiency and overcharging fees is applaudable and much needed. To take root with the consumers, though, the company needs to pull up its sleeves to make changes in more things than one, including calibrating its own algorithm to make it more efficient while fairer. Although we believe the longer it operates, the more its efficiency and profitability could improve due to its data-oriented AI models; its current state is not in an expansionary mode. We think the current price is still overvalued and the bottom isn’t exactly hit yet. We want to see more improvement in its cash flow sustainably before considering taking part. The stock could still have several bounce-backs since it has fallen so steeply, and some investors might go on bottom fishing. For now, we recommend a hold.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment