viper-zero/iStock Editorial via Getty Images

In August 2023, I analyzed Japan Airlines (OTCPK:JAPSY) (OTCPK:JPNRF) stock and I issued a Hold rating on the stock because putting the projections for Japan Airlines together I could not find a compelling investment case. Separately, I had also analyzed the prospects of ANA Holdings and from that analysis, I concluded that compared to ANA Holdings, Japan Airlines had less favorable revenue trends in their cargo business. Both airlines are marked a hold and I think the fact that ANA Holdings is better has also shown in the stock price performance. ANA lost 4% while Japan Airlines lost 9.3% of its value.

So, Japan Airlines lost more of its value and in this report, I will discuss whether that stock price decline combined with potential changes in forward projections and realized results provides a reason to alter my view on Japan Airlines stock.

Japan Airlines

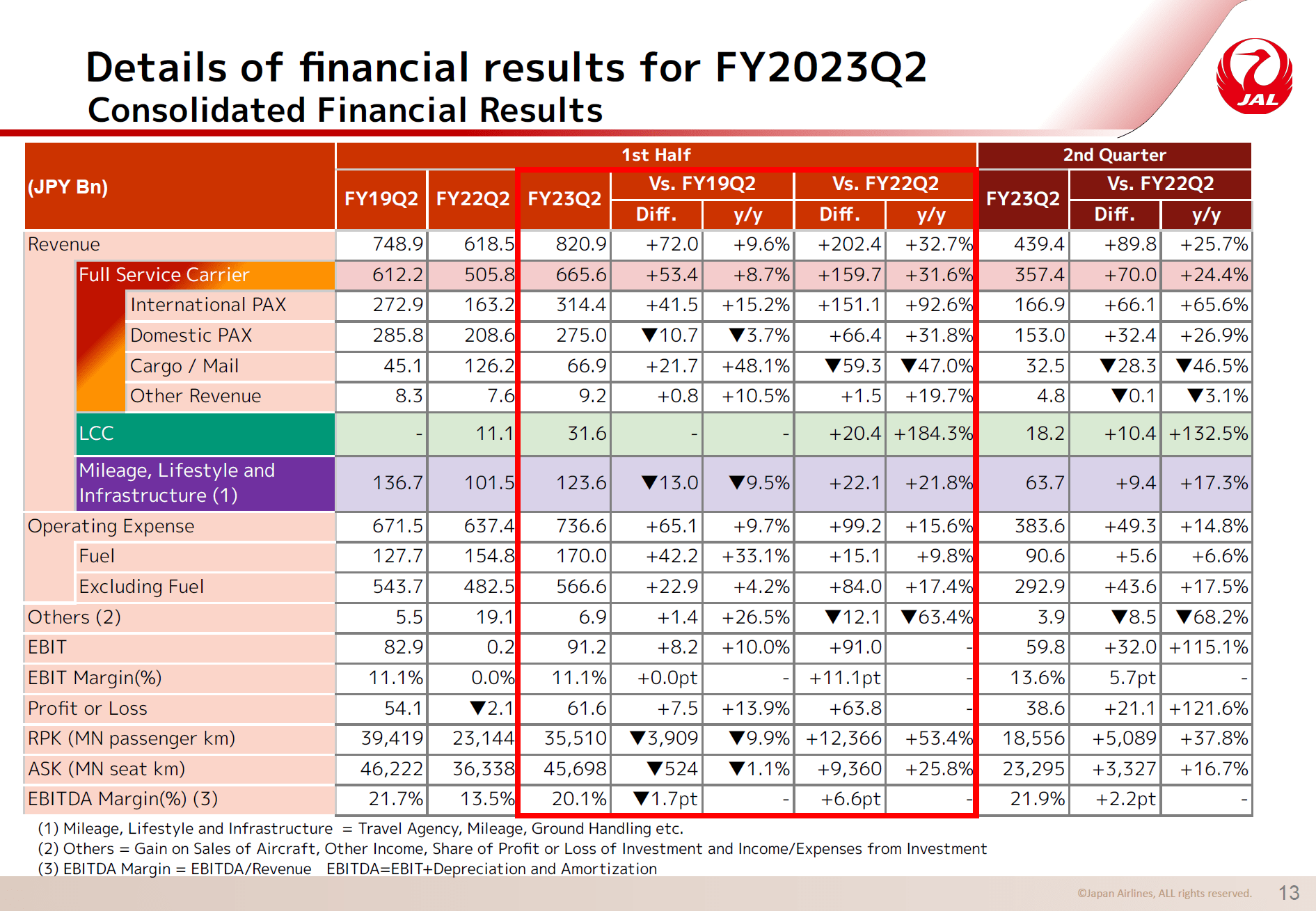

The first half results show that total revenues grew 9.6% compared to prep-pandemic while capacity was down 1.1%. The full-service carrier saw revenues 8.7% higher compared to pre-pandemic driven by 48% growth in cargo/mail revenues while international PAX revenues grew 15.2% and Domestic Pax declined 3.7% and other revenues increased 10.5%. The LCC business has no comparable period in 2019 as that is a business that Japan Airlines is currently scaling. Mileage, Lifestyle, and Infrastructure revenues were down 9.5% compared to pre-pandemic.

In total, we saw the Full Service Carrier and LCC revenues grow 14% on a capacity being down 1.1% so from a capacity perspective, the revenues are running quite a bit ahead. That is driven by international capacity unit revenues being up 35% while capacity is 85% recovered. The international business is seeing strength in the North American market with capacity 5% above pre-pandemic levels but revenues are nearly 50% higher. Similarly, Europe and Asia/Oceania are only 85% recovery in terms of capacity but generate revenues that are 21 and 16 percent higher than pre-pandemic. The challenged markets are China where capacity is only 62% recovered but we see stronger unit revenues which are down only 23% and Hawaii is down 44% in capacity and 31% in revenues. The Hawaiian market overall seems to be tough for any airline operating it and that is driven by a slow revival of tourism to Hawaii.

The domestic business is more pressured with capacity being 96% recovered but unit revenues are more or less flat. So, the international passenger business is performing very strong and has some capacity recovery potential ahead while the domestic passenger business seems to be more saturated with few opportunities to add more capacity without cracking unit revenues.

The cargo business saw around 50% growth in revenues. This was driven by 70.5% growth in international cargo revenues while capacity was down 5.1%. The reason why the revenues performed strongly despite lower capacity compared to pre-pandemic is the share of high-value goods that drove the revenues per ton up. On the domestic market, revenues were down 6% on 4.2% lower capacity further pressured by less cargo carried but partially offset by better revenue per ton. Previously I looked at the cargo revenues on a year-over-year basis, but that might not be fully descriptive as we are seeing normalization in the cargo market which was to be expected coming out of the pandemic and more international capacity being added while at the same time e-commerce demand is on the softer side as Europe is coping with a recession.

As mentioned earlier, the low-cost operations have no pre-pandemic comparable period but it is generally a new line of business with Zipair targeting low-cost long-haul operations and Spring Japan is more regionally focused. I view the low-cost business as a growth opportunity that could complement growth where the full-service carrier eventually might be more saturated and most noteworthy in the domestic market. So, it is not a huge part of the business at just 4% of revenues but I see it as a growth opportunity.

Japan Airlines Guides Higher On PAX Revenues, Lower on Cargo

Japan Airlines

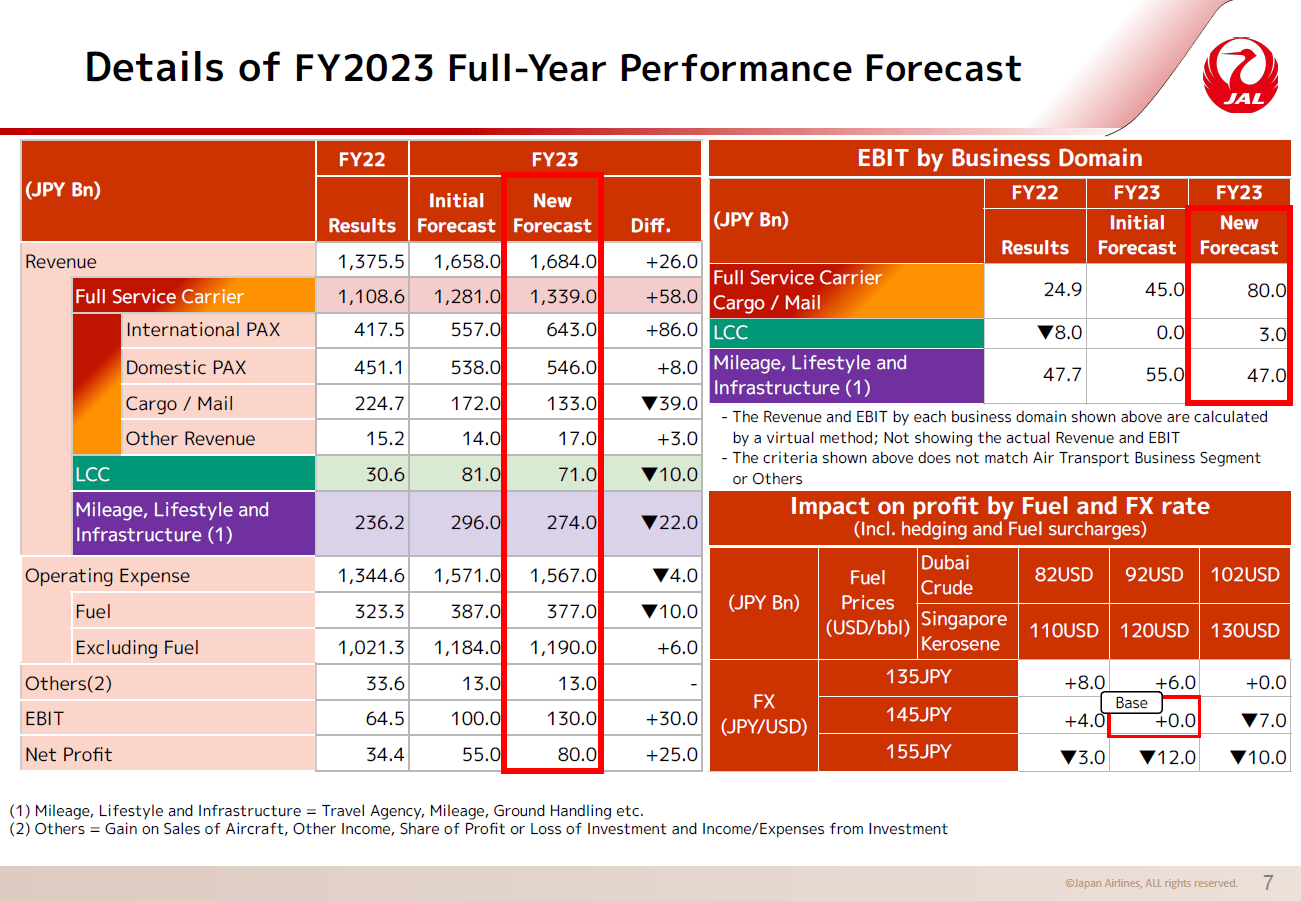

Looking at the updated guidance from Japan Airlines, we see that the airline has significantly increased its expectations for International full-service passenger revenues and modestly for domestic revenues which I believe makes sense as the domestic market is one that needs to be operating with care while the international market has significant capacity space for recovery. Japan Airlines expects international demand to be 74% recovered which is 5 percentage points higher than initially anticipated while domestic demand is expected to be 97% recovered compared to 95% initially anticipated. These strong expectations for demand recovery allow for upward pressure in revenue per passenger.

While full-service passenger revenues have been guided up, the guidance for Cargo revenues came down and that is to be expected. The market remains soft, and as international services expand, there is more belly freight capacity coming online which pushes down the unit revenues. LCC operations will have around JPY 10 billion lower revenues while Mileage, Lifestyle, and Infrastructure revenues have been guided down by JPY 22 billion. On the EBIT level, expectations have increased by 30% pointing at Japan Airlines more than doubling its EBIT driven by better profitability for the full-service carrier and the LCC business actually being more profitable despite guiding lower on revenues.

Japan Airlines Deserves An Upgrade To Buy

The Aerospace Forum

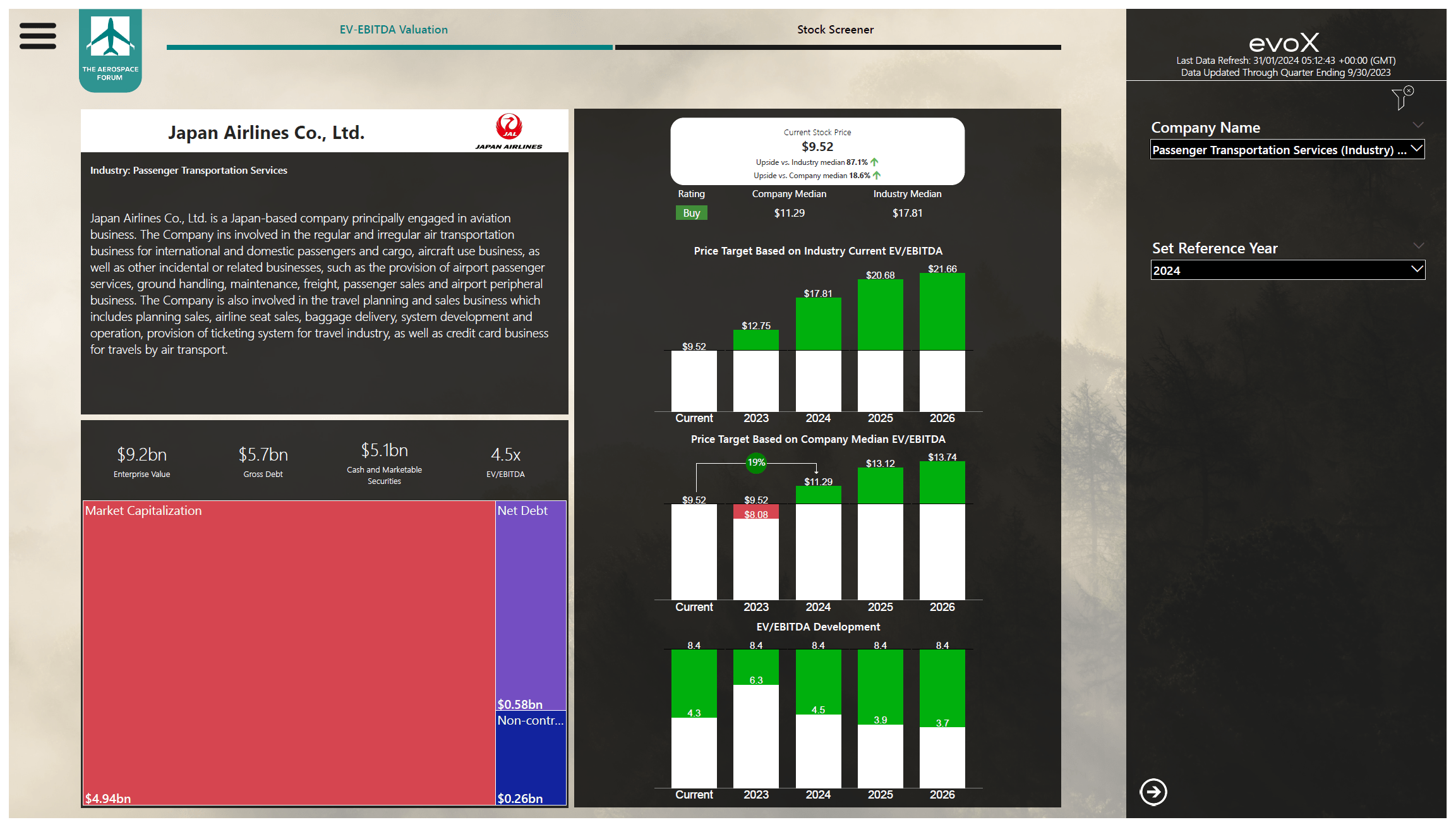

After analyzing Japan Airlines’ most recent result, I see strong execution with an upside on international traffic results, prudent execution on the domestic market as well as better profit performance at the low-cost carriers despite lower revenue expectations. Combining this with the balance sheet data and forward projections by analysts, I do think that it is fair to upgrade Japan Airlines stock to a buy with a $11.30 price target representing a 19% upside and this provides a relatively conservative valuation on the condition that the airline meets expectations as the peer group trades at significantly higher multiples.

Conclusion: Japan Airlines Navigates Well

I believe that Japan Airlines has navigated a relatively difficult environment rather well. There is a lot of potential for recovery of international traffic but there are some weak spots such as China and Hawaii while the domestic market seems to be lacking strong growth prospects. At the same time, Japan Airlines is trying to capitalize on the low-cost carrier trend which I believe could provide growth that the domestic market cannot provide. All things considered, I do believe that Japan Airlines is a buy at this point.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment