DINphotogallery/iStock via Getty Images

iShares U.S. Basic Materials ETF (NYSEARCA:IYM) offers exposure to a basket of principally large-cap stocks from the GICS materials and industrials sectors.

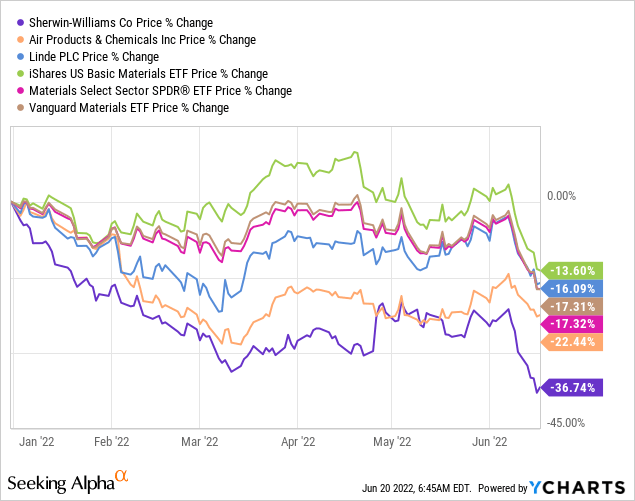

Basic materials players have been in the limelight earlier this year as persistent inflation maintained its tight grip, so investors have been flocking to companies deemed capable of sustaining margins and improving the top line simultaneously when the CPI changes are touching decades’ highs. However, I am opting for a more cautious view here, as I believe the inflation beneficiaries thesis does not look that resilient anymore as bears will be flexing the capital scarcity narrative. Additionally, I warn investors against extrapolating the fund’s performance prior to September 2021 since the index change led to pronounced shifts in exposure, thus impacting its risk/reward profile; this change also partly explains why IYM has marginally outperformed peers this year, though does not guarantee segment-leading returns going forward.

Investment strategy: key holdings, sector, industry exposure

With more than $1 billion in net assets, IYM is one of the largest passively managed investment vehicles with a focus on U.S. basic materials, though its portfolio is far from being the heaviest one amongst peers, with the Vanguard Materials ETF (VAW) and Materials Select Sector SPDR Fund (XLB) sporting larger AUMs, $6.5 billion and $3.4 billion, respectively. The duo is also cheaper, with expense ratios of just 10 bps vs. IYM’s 41 bps.

In September 2021, IYM underwent a deep investment strategy recalibration, abandoning the Dow Jones U.S. Basic Materials Index replaced by the Russell 1000 Basic Materials RIC 22.5/45 Capped Gross Index.

Though the depth of exposure did not improve significantly, with the fund now long 37 equities vs. 35 in January 2021, this change did have a profound impact on the portfolio composition, as the heaviest allocation Linde plc (LIN), an around $146 billion industrial gases market heavyweight, which accounted for approximately 18.4% as of January 13, 2021, as illustrated by the iShares webpage saved by the Wayback Machine, was ousted.

For investors choosing between XLB and IYM, it is worth noting that the former is still long LIN, with ~17.5% of the net assets allocated to it. This is also the case with VAW which has an ~13% of the net assets parked in the Linde stock. So for the LIN bulls, XLB or VAW should be better at the current juncture.

As Linde was shown the door, Air Products and Chemicals (APD), its closest peer and another key player in the industrial gases market, climbed to the top spot, now accounting for ~8.9%.

Though both have seen rather soft 2022 to date, APD is much deeper in the red.

Another difference between IYM, XLB, and VAW is that the latter two both have exposure to The Sherwin-Williams Company (SHW). SHW had seen its price bolstered by investor enthusiasm stemming from the elevated demand for DIY painting products, a pandemic-driven one-off tailwind. As the pandemic abated and buying patterns started to normalize, the market has been gradually removing this factor from valuation, with SHW down by close to 37% YTD. Again, IYM was immune since it has no exposure to the stock; this is more likely behind its marginally better performance compared to its peers. On a side note, even after such a precipitous decline, SHW looks expensive.

Overall, we see a ~6.7% allocation to the industrial sector, with Fastenal (FAST), a wholesale distributor of fasteners (including bolts, nuts, screws, and studs, to name a few) being the largest one, with a 4.5% weight; the rest is deployed to materials.

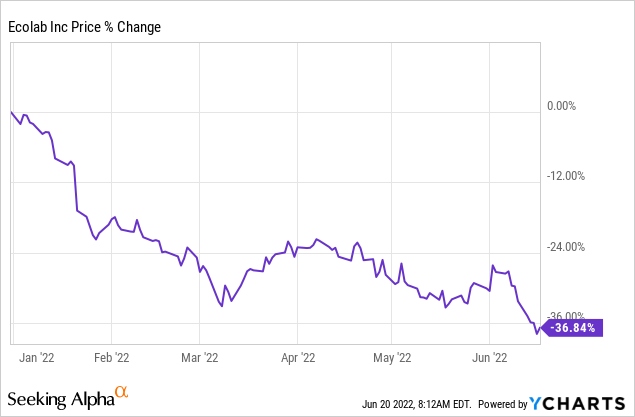

In terms of industries, IYM is heavy in specialty chemicals (over 21%); Ecolab (ECL), a company with a portfolio of water, hygiene, and infection prevention solutions, is the largest SC player with a weight north of 6%. 2022 has been choppy for this generously valued stock, as the market removed close to 37% from its price.

What is causing my skepticism

In my view, the market is currently switching from worrying about inflationary pressure to the capital shortage issue. That is to say, previously we have seen names that benefit from exposure to commodities that more or less protect their margins amid the CPI advancing at its fastest pace in decades appreciating consistently, and those with generous growth premia (the broad tech universe) declining, now, investors are becoming increasingly concerned about how higher rates will impact growth prospects and balance sheets.

The Fed has recently made a historic decision and increased the rate by 75 bps, in the most aggressive move since 1994. Certainly, the cycle is far from being closer to a peak, as similar steps are due in the coming months to balance demand and supply. There are even more hawkish voices. Bill Ackman, a hedge fund billionaire, is of the opinion a 100 bps rate increase is needed, with the terminal rate between 5% and 6%.

In my view, even with a TR marginally below 4%, the repercussions are on the wall. First, the economy can end up in a recession. And while the recession prospects are clouded and this hopefully can be still avoided, even without the GDP contraction the most capital-intensive industries will suffer.

Specifically, this can eat into profit margins and FCF due to interest payments becoming more complicated to cover. For basic materials that are by definition capital-intensive, typically burdened with hefty debts, the prospect of growth projects becoming trickier to finance is a worrisome one.

I can be wrong here, but if I am right, that means the IYM holdings are not immune to further share price depreciation should the market continue its foray into the bear market zone. What can exacerbate this issue? A valuation matter can add to difficulties easily.

The ETF is by no means trading at frothy levels. The IYM website shows a Price/Earnings of 11.7x vs. the iShares Core S&P 500 ETF’s (IVV) 18.1x. But this is the tip of the iceberg.

Above, I have already flagged ECL has overstretched multiples. The issues are not that serious if put into context, but anyway, ~33% of the IYM portfolio have a Quant Valuation grade of D or worse. A similar allocation to cheaper stocks (a B- grade or better) makes a mix a little more balanced but does not eliminate risks completely. It is not to be missed that IYM’s large-cap, top-heavy basket (61.6% allocated to the key ten stocks) has a close to excellent quality, with those having an at least B- Profitability grade accounting for 88.6% as the size and quality factors are intimately intertwined.

To corroborate, the median market capitalization amongst those industrial and materials players with a D+ Profitability grade or worse (268 names in total; I used the dataset downloaded from the screener) is $371 million, indicating that size heavily influences a stock’s quality characteristics, a phenomenon I have discussed a few times already.

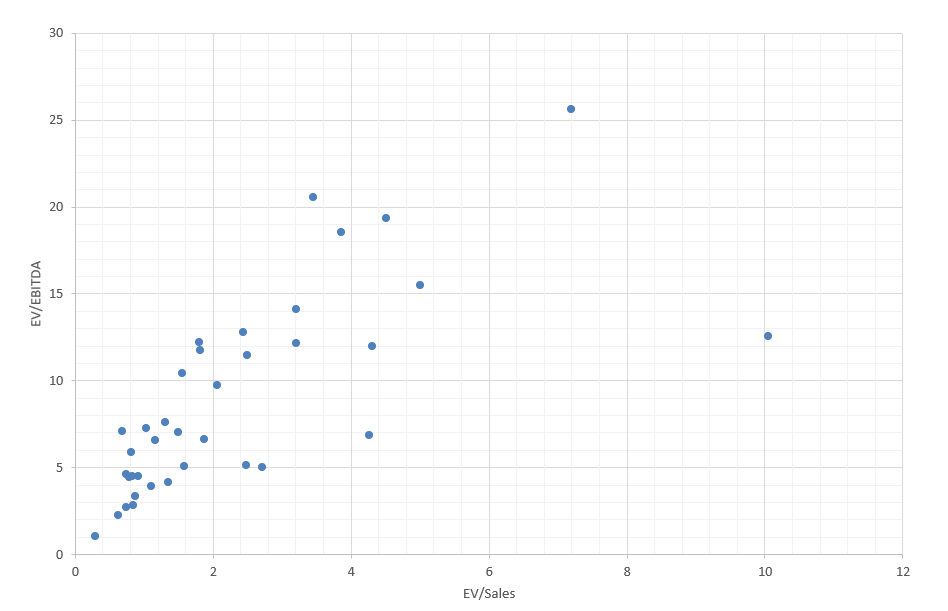

Still, there is something to be wary of. The weighted-average EV/EBITDA (yes, all the players have positive EBITDA) of the IYM portfolio is ~9.9x; the materials sector median is just around 7x. Besides, the WA EV/Sales is ~2.79x, while the median for the sector stands at 1.5x. Yes, the premium is observable.

For better context, the scatter plot below shows the spectrum of the EV/EBITDA and EV/Sales multiples the IYM holdings are trading with.

Created by the author using data from Seeking Alpha and the fund

Final thoughts

In sum, IYM has seen its price going sharply up earlier this year, gaining almost 11% from January 1 to April 19, bolstered by the inflation narrative and commodities back in vogue. But as of writing this article, the fund is down ~12.9%.

With capital becoming scarcer, the prospects for materials are less rosier. In this regard, I opt for a more conservative outlook, assigning IYM a Hold rating.

Be the first to comment