Solskin

The iShares Global Healthcare ETF (NYSEARCA:IXJ) is self-explanatory. It is all healthcare exposures, many of which being biotech/pharma companies but some not. We think that the ETF is weighted towards some solid issues, and the ETF will benefit from an ongoing exceptional recovery in diagnosis rates coming off pandemic local lows. On top of that, the companies should be resilient to a recession. Overall, we think that the ETF is attractive to investors looking for resilience, but not necessarily for those looking for an aggressive value angle, because there isn’t one as far as the allocations in IXJ go.

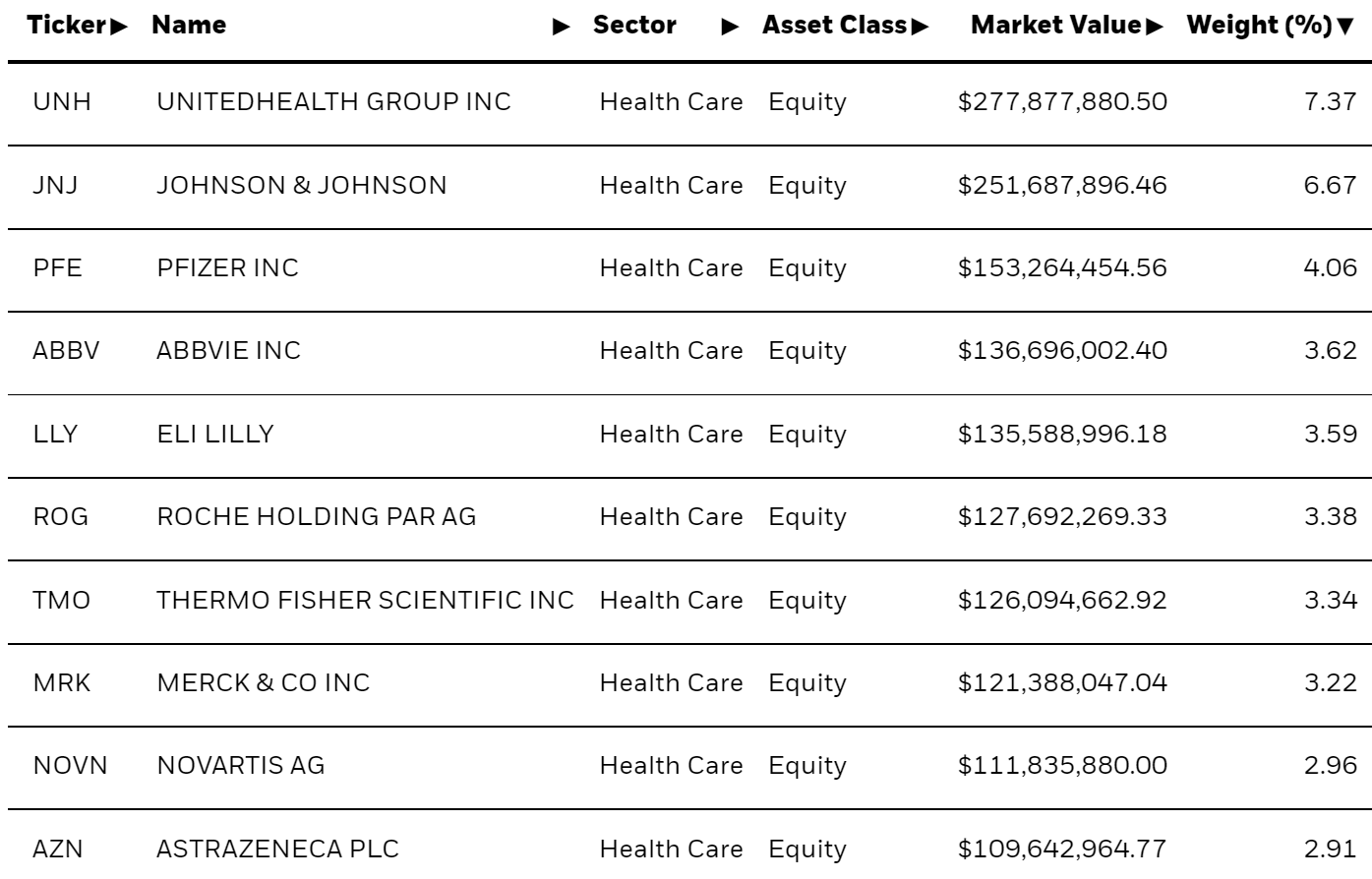

IXJ’s Holdings

The breakdown can be best approached by looking at some of the top holdings.

IXJ Breakdown (iShares.com)

While there isn’t an excessive skew, we do see a fair bit of allocation towards UnitedHealth (UNH). UnitedHealth is already a little bit of an outlier as far as healthcare exposures go, but not a bad one. Being an insurance company, its economics are of course quite particular but well suited to an environment where rates are rising and rolling over of maturities of bonds in the regulatory portfolio against claims will provide higher returns. Moreover, cash-generative insurance businesses are definitely more attractive now that cash is becoming more expensive.

Conclusions

Besides UnitedHealth at a 7.4% allocation, the rest are more straightforward tech exposures. A lot of big pharma companies with strong franchises across several treatment areas. Of course, there’s Pfizer (PFE) which has its COVID-19 franchise, but also other pediatric vaccines and a decent oncology platform. There’s AbbVie (ABBV) which is a bit more particular with the loss of exclusivity of Humira trying to be replaced with other drugs like Imbruvica. Solid franchises under Roche AG (OTCQX:RHHBY) as well as Novartis (NVS). Besides ABBV, which is a known quantity, there aren’t too many alarming cliffs or franchise over-reliance in the top holdings.

Moreover, the majority of these companies are going to be benefiting from a recovery in diagnosis rates. During COVID-19, hesitance to go to physicians and a focus of the public health system on COVID meant that a lot of other diagnoses slowed down. These will now be recovering, giving a bit of a boost to growth rates across treatment areas. Demographics also play in favor of most of these companies that have franchises that deal with the elderly, a greater proportion of our population. Finally, they’re all going to be rather recession-resistant.

The yield on the ETF isn’t great at 1.3%, and the fee eats away at that at 0.4%. Moreover, the average P/E across the ETF is 22x. There is no strong value angle here at all, and the portfolio is pretty broad across all sorts of healthcare exposures. But it is resilient. If you want to make a bit of a lazy resilience bet you might want to consider this, but you’d probably be better off chasing yield with a REIT.

While we don’t often do macroeconomic opinions, we do occasionally on our marketplace service here on Seeking Alpha, The Value Lab. We focus on long-only value ideas, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, us at the Value Lab might be of inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment