G0d4ather

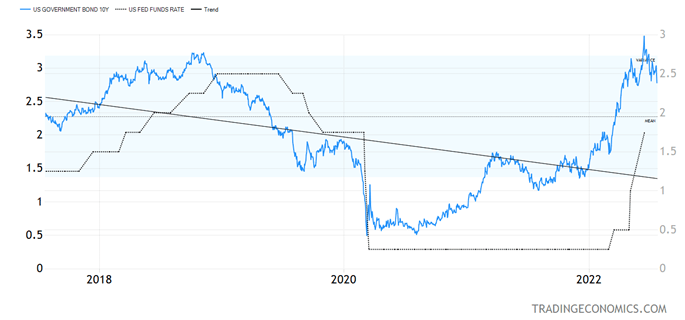

On Friday, the 10-year Treasury yield closed at 2.78%. The 2-10 spread has been inverted for a while, and if the Fed is hell-bent on front-loading rate hikes this summer, the 3-month/10-year Treasury spread will invert soon. There is some support in the 2.70-2.75% range, but taking that range to the downside may put Treasuries in a situation where we may not revisit the 3.50% level (which we touched in June) for years, similar to the way rates topped out at 3.25% in November 2018 and did not see that level until June 2022.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

The Federal Reserve can cause a recession with rapid rate hikes in an economy that carries way too much financial leverage. In my view, it was a big mistake not to intervene against the Biden administration’s fiscal expansionary policies in early 2021 in a recovering economy – the same way the Fed intervened against the Trump administration’s fiscal expansionary policies in 2018. Now the Fed is behind the curve.

Having a mild recession is not that big a deal, as it will cool off the inflation picture – and the stock market may be done with most of its decline, but for the stock market to have a firm bottom, we need a clear path to the end of the hostilities in Ukraine, and a dovish Fed pivot, neither of which are visible yet.

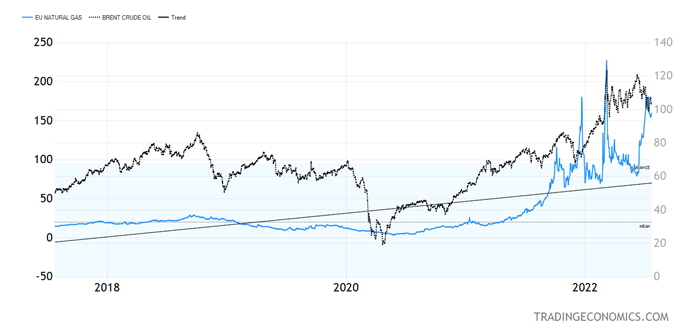

Vladimir Putin is already using his leverage on Europe with reduced natural gas flows, and I would not put it past him to use even more leverage as the winter months approach.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

Just as the war in Ukraine started, EU natural gas futures contracts reached an oil price equivalent of close to $400 per barrel. It is entirely possible that they reach that same absurd territory this year, as there is no LNG capacity that can fill the gap for Russian natural gas. This can create a deep recession in the EU and push the euro closer to 90 cents, well below parity with the U.S. dollar.

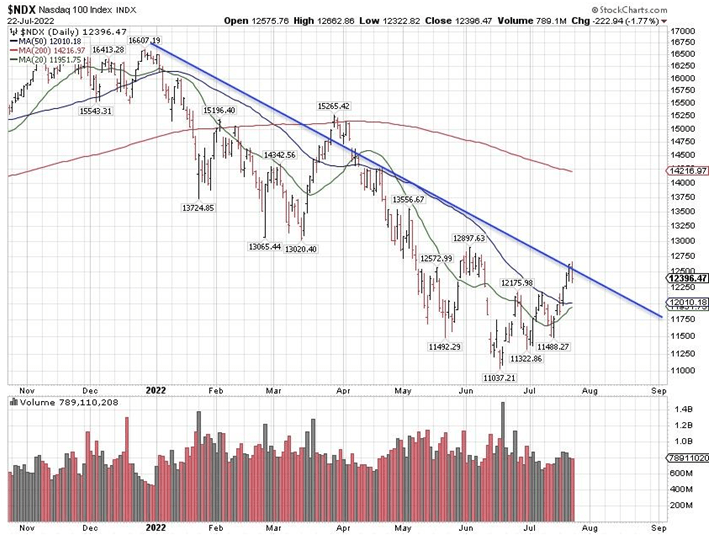

The Nasdaq 100 Index Shows a Bearish “Engulfing” Pattern

Friday’s high on the NASDAQ 100 Index is above the high from Thursday, and the low from Friday is below the low from Thursday. In other words, we had a bigger range of trading on Friday, on both sides, and by closing near the lows of the day, the NDX Friday range “engulfed” the NDX Thursday range.

One day does not establish a trend, but such bearish engulfing patterns tend to mean trend reversals.

Graphs are for illustrative and discussion purposes only. Please read important disclosures at the end of this commentary.

We also have an FOMC meeting this week. In the last two FOMC meeting days, the market had a good close on the day of the Powell press conference, followed by vicious selling the next day. This would be something to consider when going into tomorrow’s FOMC press conference afternoon trading session.

In theory, both the S&P 500 and the Nasdaq 100 can rally into their respective 200-day moving averages, which I would consider a best-case scenario. The worst-case scenario is we top out near 4,000 on the S&P 500, and head for a retest of the June lows. I think we will know which scenario it is by the end of the week. How the market trades post-FOMC will give us clues as to the fate of this rebound off June lows.

All content above represents the opinion of Ivan Martchev of Navellier & Associates, Inc.

Disclosure: *Navellier may hold securities in one or more investment strategies offered to its clients.

Disclaimer: Please click here for important disclosures located in the “About” section of the Navellier & Associates profile that accompany this article.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment