imaginima

Investment thesis

AT&T Inc. (NYSE:T) is a stable company in the telecommunications sector, ranking first among competitors in terms of revenue. Nevertheless, we do not see significant prospects for AT&T right now, as the market valuation of the stock is fair, and soon the communications sector, as well as many others, will suffer from inflationary pressure.

Tariffs and consumer demand

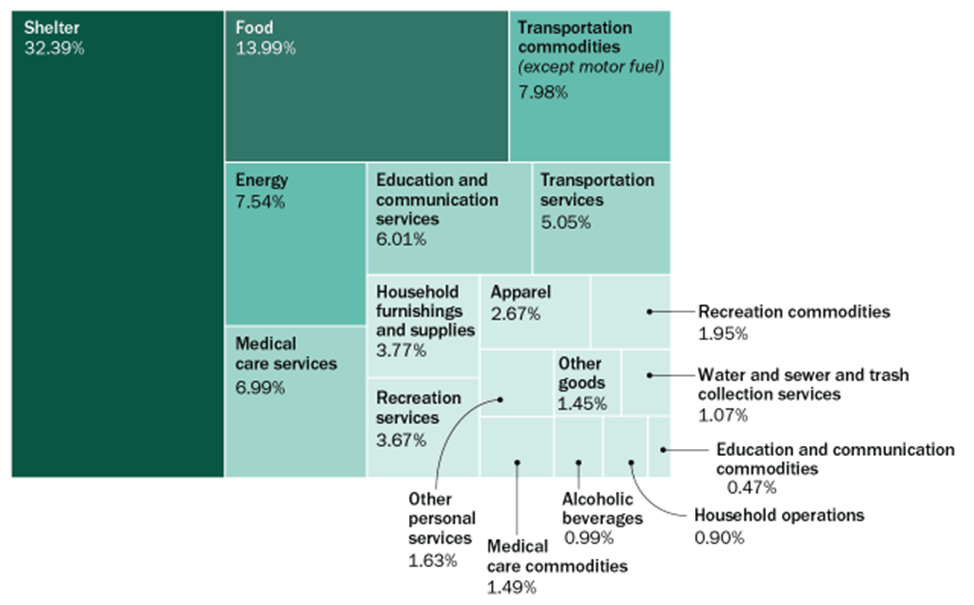

Telecommunication has always been a protective sector. Telecom companies have high pricing ability and are stable in terms of consumer demand, as mobile communication and Internet access in developed countries have now become basic services. In the U.S. consumer basket, spending on communication, together with education, accounts for about 6% of the average total household’s expenditures.

Source: US Bureau of Labor Statistics

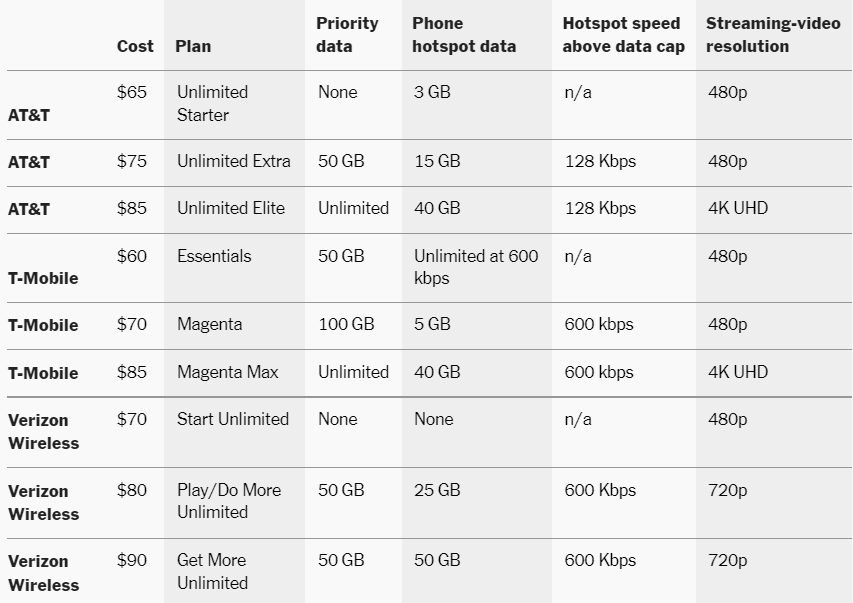

The sector is very competitive, mainly due to the quality and volume of services available by subscription. Although there is distinction among the tariff plans, there is no significant difference for the consumer as in the average monthly income (about $5 700) all unlimited tariffs make up about 2%.

The most important thing for the consumer remains the quality of the services provided, and it is impossible to distinguish the best operator as all have their advantages and disadvantages. For example, T-Mobile (TMUS) is not the company with the largest mobile network coverage, second to Verizon (VZ) and AT&T, though outperforming its competitors (source: NYT) in the 5G segment and in terms of the download speed.

Source: New York Times, Wirecutter

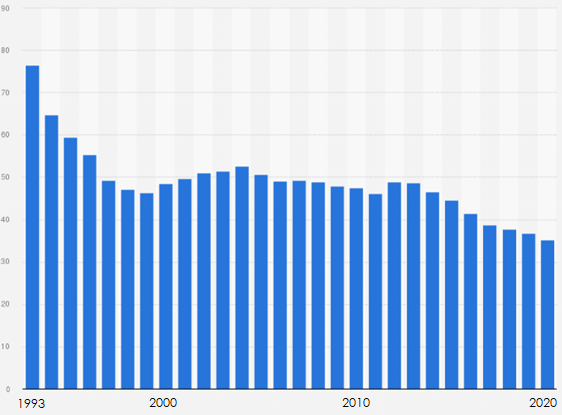

Nevertheless, due to the development of infrastructure and increased availability of communication services in the sector, there is a stable trend to lower ARPU.

Source: Statista

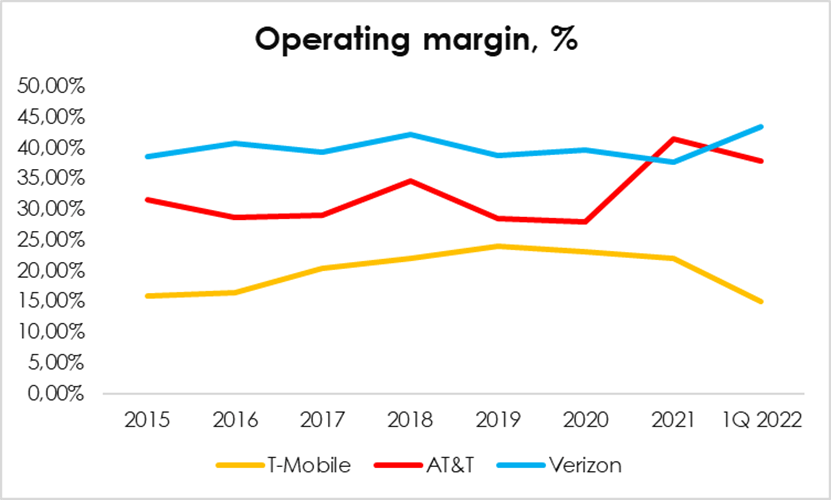

Despite ARPU decline, companies’ operating margins remain fairly stable, as part of the services’ prime cost also becomes cheaper with the development of infrastructure.

Source: companies’ data, AT&T report

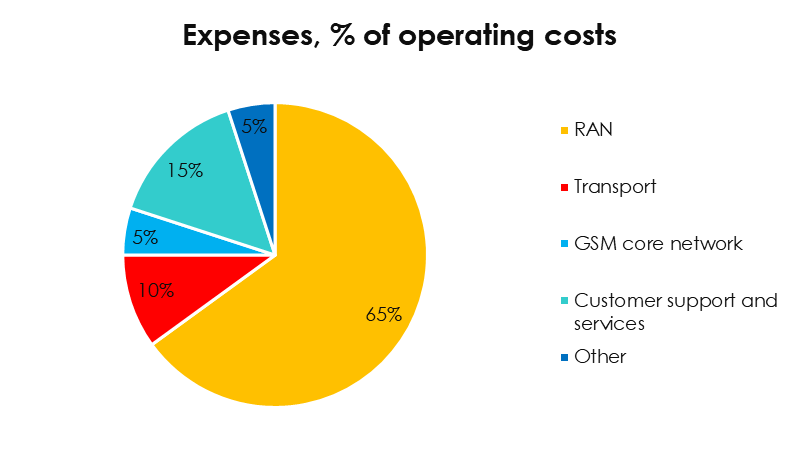

Expenses of the telecom companies

Expenses of communication sector companies mainly consist of equipment installation and maintenance, software renewal, and licensing. This also includes standard expenditures on labor, rent, utilities, etc.

Source: 3G4G

The emerging open RAN technology is a subset of virtual radio access networks with open interfaces. The main driver for the transition to open networks is the shift to 5G network architecture and services. They provide the ability to mix and match components from different suppliers, which will allow communication companies to save significantly on network maintenance.

Therefore, the ARPU reduction trend will continue to be balanced by lower costs of telecom companies, allowing them to keep the margin of the major players within the competitive environment.

In the short term, however, the telecom business may experience effects of general inflationary pressure. The sharply increased cost of components and labor cannot be quickly offset by higher tariff costs. As noted above, the telecom market is competitive, so players need to make smooth transition to more expensive tariffs, adhering to the dynamics of competitors in order not to lose market share abruptly.

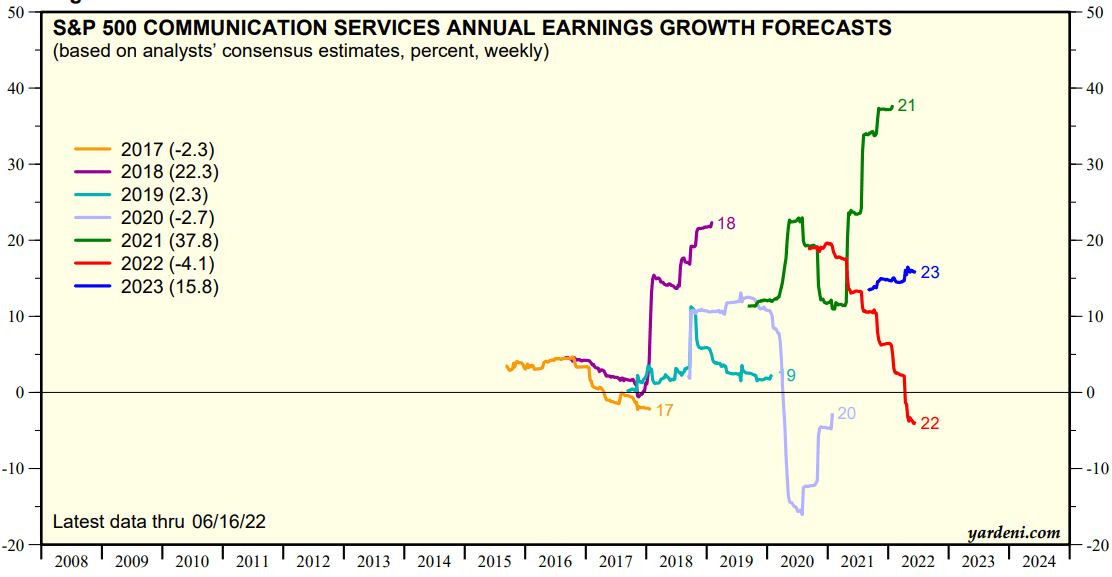

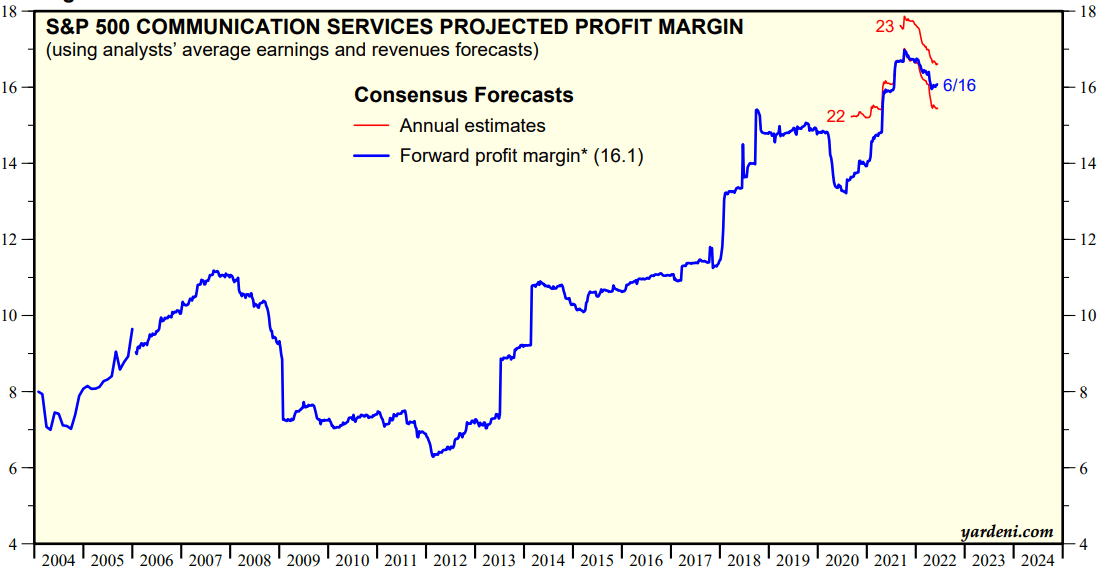

Wall Street analysts have already included the factor of the expected decline in the sector’s margin, so the 2022 consensus forecasts for EPS growth have shifted into the negative zone.

Source: Yardeni Source: Yardeni

Conclusion

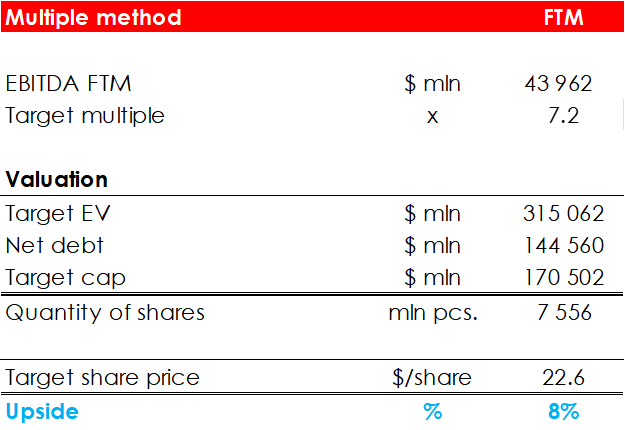

Our coverage of the telecom sector includes only AT&T, for which the investment idea was opened with a target price of $22.6.

Source: calculations by Invest Heroes

Over 7 months, including dividend payment and the sale of Discovery (WBD) shares, the total yield amounted to 23.11%.

According to our calculations, at current prices the upside is only 8%. Considering all the risks, we believe that the company is not attractive for long-term investors now, as the investment will not bring much profit. Therefore, we change our rating from BUY to HOLD and believe that it is good moment for taking the profit.

Be the first to comment