KanawatTH

Introduction

The labor market is dragging growth stocks and growth exchange-traded funds (“ETFs”) lower. Here’s how.

In November 2022, the U.S. economy added 263,000 new jobs, exceeding economists’ forecast by 63,000. Also, wages were up 5.1% year-over-year in November. So what? Well, with wages going up and more jobs, labor costs for companies have also gone up. These costs have been passed onto customers like you and me by raising the prices of goods and services. And that’s how we get to the buzzword of the season; inflation.

Higher inflation essentially forces the U.S. Federal Reserve to drive interest rates higher to control and curb it, lest the economy loses faith in its currency. The one side-effect of this that I am sure everyone is watching is how weak the demand environment will get and the subsequent impact on corporate balance sheets and profitability. This is especially important for small cap growth stocks, which often have less resilient business models to weather a recessionary storm.

IWO: A Basket of Small-Cap Growth Stocks

The iShares Russell 2000 Growth ETF (NYSEARCA:IWO) tracks U.S.-based small-cap growth stocks in the S&P500. Here is what the composition of this ETF looks like:

IWO ETF Composition

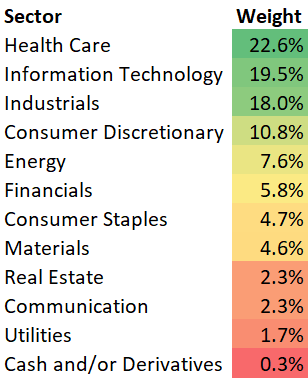

Sector Composition

Zero or low cyclicality sectors make up most of the IWO index:

IWO Sector Exposure (IWO Website, Author’s Analysis)

IWO’s heaviest weights are in healthcare and information technology, with a combined 42.1% exposure. This profile is quite similar to that of the S&P500 (SP500), which also has 42.1% exposure in these two sectors. That’s a bit of a coincidence. I didn’t expect such a close match!

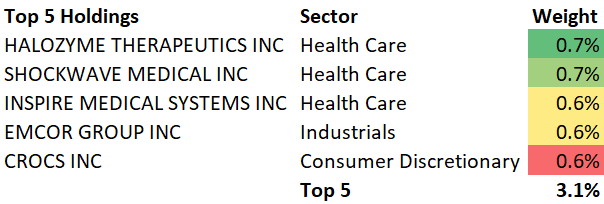

Top 5 Holdings

From a top 5 holdings perspective, IWO is extremely diversified:

IWO Top 5 Holdings (IWO Website, Author’s Analysis)

The top 5 holdings make up a mere 3.1% of overall exposure. The top 5 include Halozyme Therapeutics (HALO), ShockWave Medical (SWAV), Inspire Medical Systems (INSP), Emcor Group (EME), and Crocs (CROX).

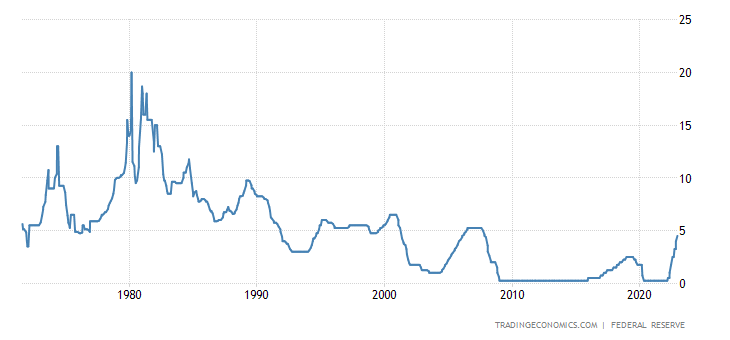

There’s No Convincing the US Federal Reserve on Interest Rate Decisions

US Fed Interest Rate (Trading Economics)

In its December 2022 meeting, the U.S. Federal Reserve increased rates by an additional 50 basis points and confirmed that it planned to sustain its rate hike campaigns, although at a much lower rate. For the same reasons as was discussed in prior articles, this is a key headwind for IWO due to its growth-oriented exposure.

Furthermore, Fed officials have revised their previous peak interest rate of 4.6% to 5.1% in 2023, a 0.50% hike. This comes as Fed Chairman Powell argues that the Fed needs to see “substantially more evidence” before it can shift its stance on rate hikes.

Read of Relative Money Flow

IWO Technical Analysis (TradingView, Author’s Analysis)

If this is your first time reading a Hunting Alpha article using technical analysis, you may want to read this post, which explains how and why I read the charts the way I do, utilizing the principles of Flow, Location, and Trap.

As growth stocks go through a rough patch, the IWO/SPX500 pair recently marked a sharp plunge to a 12-year low. This sharp reversal came after a mega-sized bull trap in early 2021. That said, the bearish descent lost steam at the higher monthly support, where a pullback ensued.

This pullback is expected to last a little longer before returning to the tested monthly support. My assessment of the pair is leaning bearish (sell) bias, but I have yet to see a near-term bull trap. This creates a window for a fake out to the upside and hence trap confirmation.

Read of Absolute Money Flow

IWO Technical Analysis (TradingView, Author’s Analysis)

On a standalone basis, the IWO ETF remains equally bearish after suffering rejection from the $232.53 monthly resistance. The ETF has struggled and failed to breach this barrier for several months now, weakening its prospects of returning above it any time soon. The possible price movement from here, as highlighted in the chart above, is down to the $180.82 monthly support. Thus, I am bearish on IWO and anticipate a retest of the immediate monthly support.

Summary

As I deduced in my recent IVW and IWY analyses, growth assets are in for a bearish tide. Essentially, I foresee a bearish persistence in the iShares Russell 2000 Growth ETF and the IWO/SPX500 pair. With the Federal Reserve bent on keeping the interest rate fire burning, the bearish pressure acting on the IWO is unlikely reverse in the medium-to-long term.

Note that although I am bearish, I am not going to short this ETF. This is because I believe I have much more compelling shorts already. For example, I currently have shorts on a mortgage REIT ETF (MORT) and a mortgage REIT stock (PMT).

Be the first to comment