It’s time to talk about one of the world’s largest aluminum companies. The Pittsburgh, Pennsylvania-based Alcoa Corporation (NYSE:AA) is almost 60% below its all-time high as it’s down 30% year to date. The company is warning that the tide is turning as prices and demand come down and (almost) crashing. In this article, we’re going to look into these challenges and, even more importantly, why I believe investors need to watch Alcoa closely. High energy prices are causing aluminum supply to fall, resulting in a situation where prices could be set to explode the moment demand expectations rebound. The situation is bad right now, no doubt, but I think patient investors can benefit from what should be another inflationary upswing as soon as the Fed allows the economy to breathe.

Now, let’s look into the details!

The Bad News – Demand And Pricing Issues

The Morgan Stanley 10th Annual Laguna Conference revealed some interesting – and mildly depressing – things regarding Alcoa’s outlook (access the transcript here).

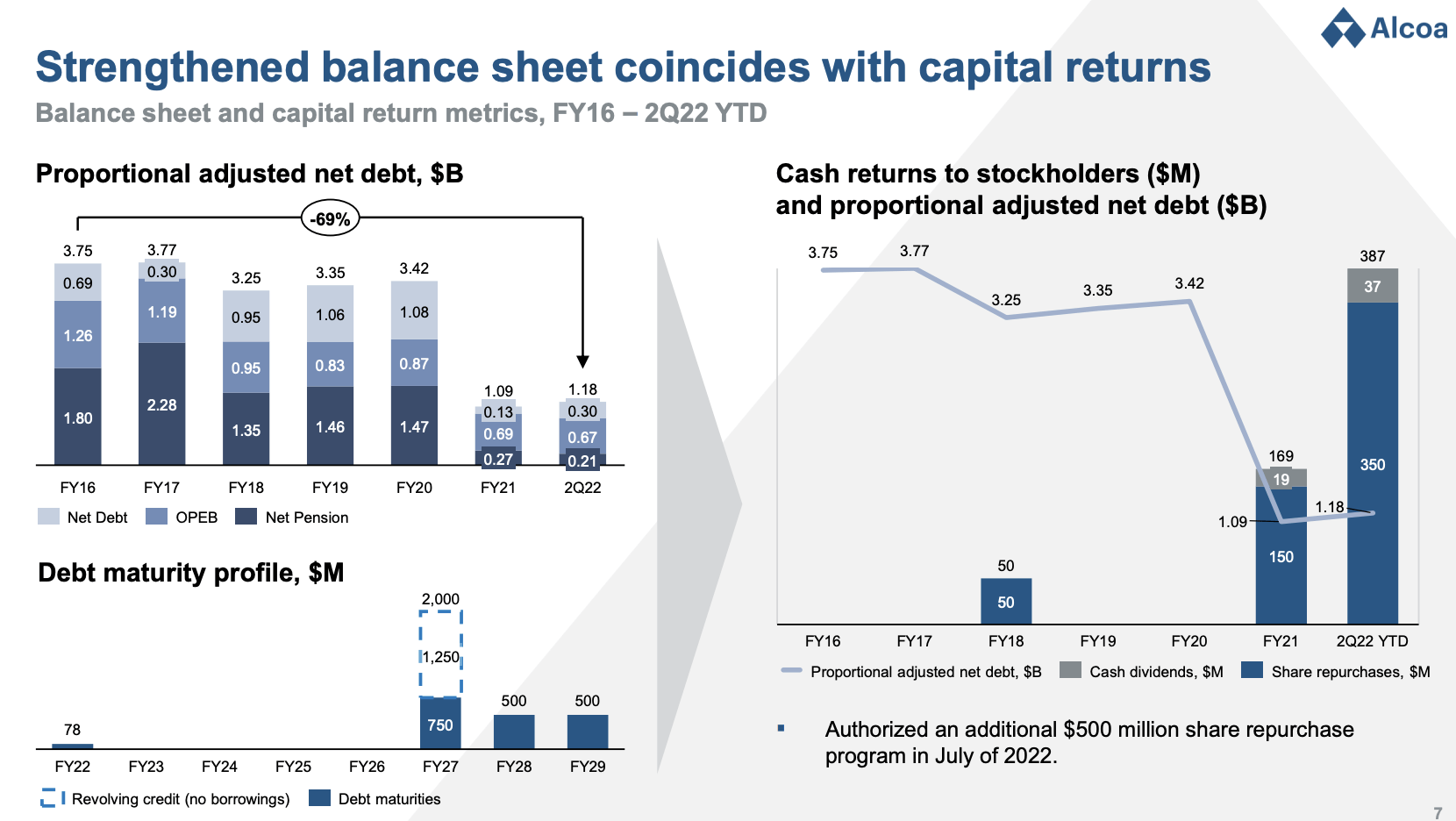

The conference started on a very positive note as the company mentioned the tremendous progress it had made after spinning off in 2016. Prior to 2016, the company also had exposure to aluminum products that went further down the supply chain. Now, the company is a pure-play aluminum/alumina/bauxite player. Since then, the company has reduced net debt from roughly $3.8 billion to $1.2 billion.

Alcoa Corporation

It’s also interesting to note that debt didn’t really come down until 2021. The same goes for shareholder returns, which didn’t really improve until 2021.

2021 was the first “post-pandemic” year if we define “pandemic” with the dramatic year of 2020 with lockdowns and no vaccination. Because industrial production and consumption were pretty much destroyed in 2020 due to imploding demand, almost all supply chains had to deal with significant pent-up demand in 2021. Inventories were not prepared for the surge in demand, mining activity was reduced, and metal prices exploded as a result of demand outperforming supply.

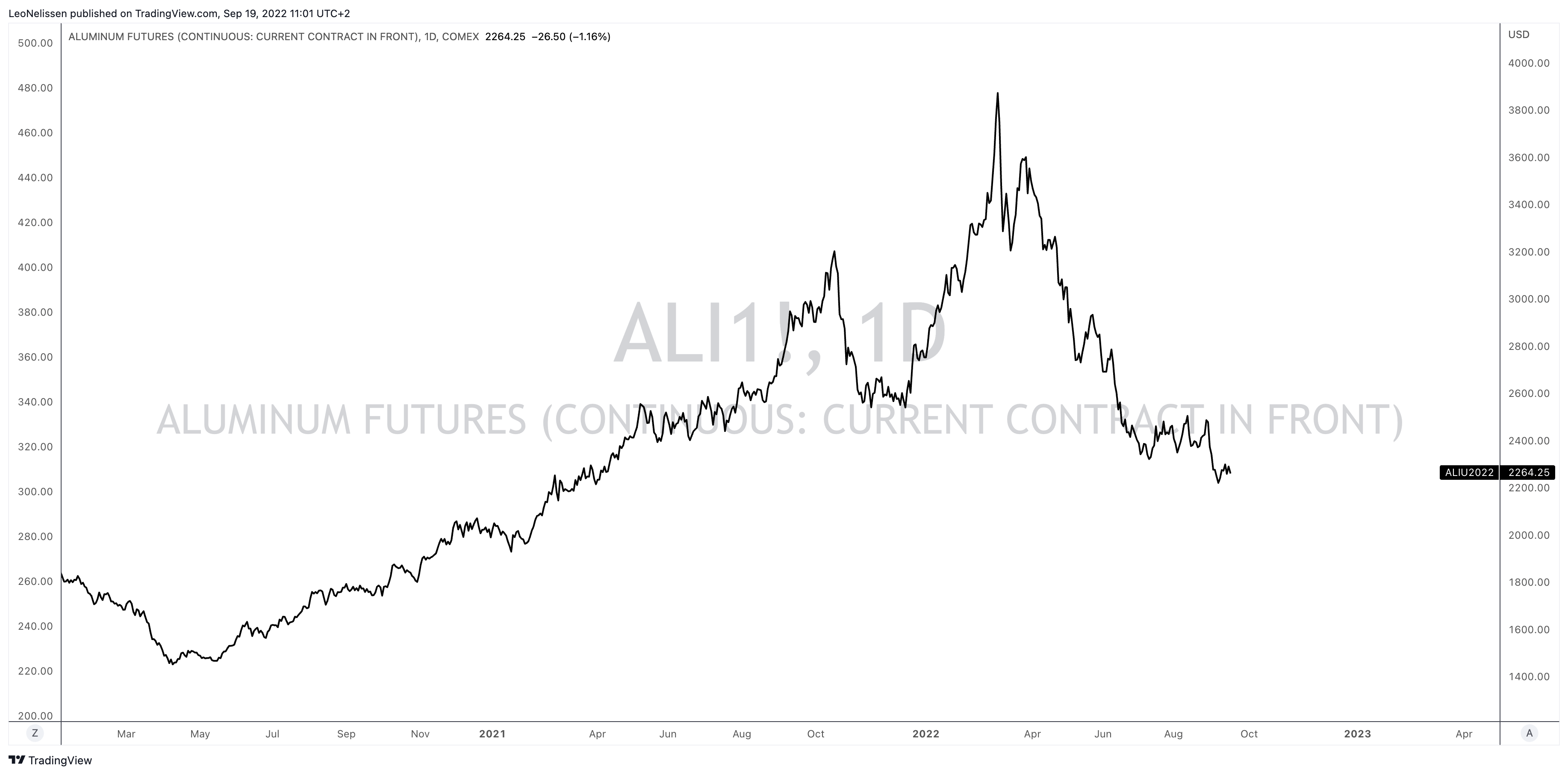

COMEX aluminum futures rose from roughly $1,500 per ton during the pandemic lows to $3,200 during the October peak in 2021. It was followed by another surge going into 2022 resulting from the war in Ukraine, but more on that later in this article.

TradingView (COMEX Aluminum)

The company had near-record earnings in the second quarter of this year with close to $1 billion in EBITDA. The company initiated a dividend and accelerated shareholder distributions as the first graph/screenshot of this article shows.

So far so good.

However, then the company commented on the third quarter:

Third quarter is shaping up to be a tougher quarter for us. Metal prices and alumina prices versus the second quarter have come down fairly sharply. At the same time, raw material prices have stayed stubbornly high. We, along with many other players in the industry are seeing significantly higher energy costs specifically in Europe.

The chart below shows the Philadelphia and NY Fed business conditions indices compared to industrial production. Industrial production is a coincident indicator, meaning it is lagging behind leading indicators like the NY and Philly Fed manufacturing indices (based on surveys). What we see below is a significant weakness in economic sentiment. It is only a matter of time before industrial production comes down into negative territory.

Wells Fargo

Moreover, inflation remains high, which means the Federal Reserve remains dedicated to combating it.

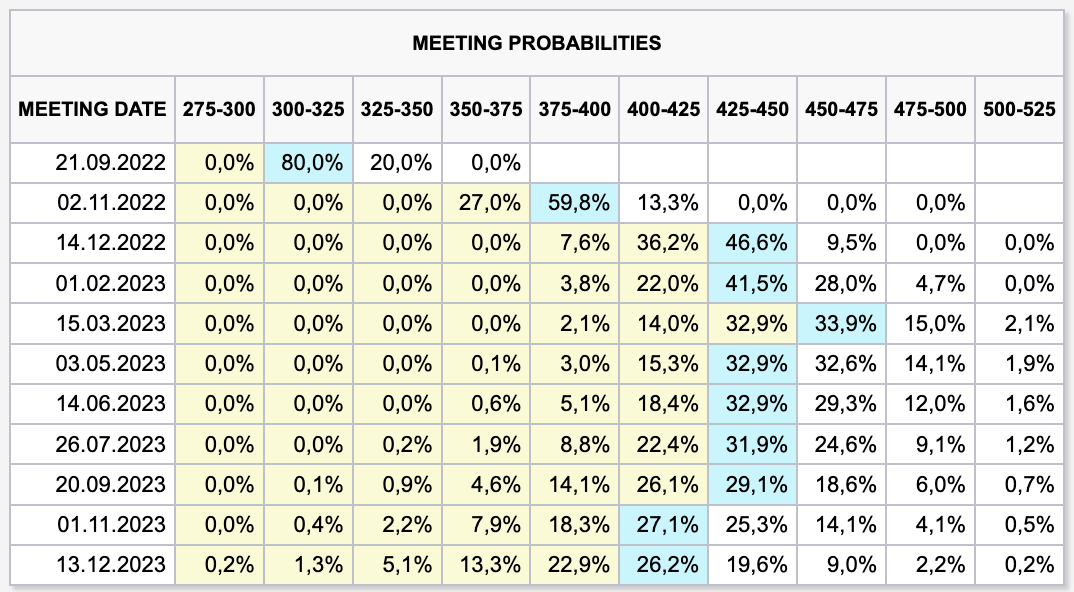

Unlike in (most) prior cycles the market is not counting on the Fed stepping in to prevent the economy from slowing too much as Powell made clear that he needs to impact demand to slow inflation. After all, impacting the supply side of the economy is nearly impossible for the Fed. Hence, despite economic weakness, it looks like the market is pricing in an increase in the federal funds rate to at least 425 basis points.

CME Group

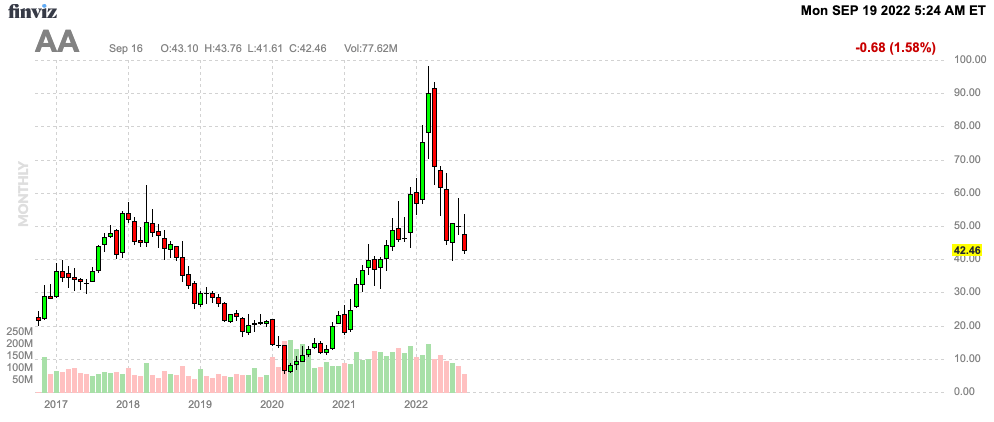

With that in mind, it is no surprise that the company is now suffering. Pricing and demand are no longer tailwinds.

FINVIZ

However, there is good news on the horizon.

The Good News – Supply Issues

In this case, please let me clarify that “good” is relative. The things we are discussing are very bullish for Alcoa shares in the longer term, but bad news for consumers and citizens of industrial nations in Europe.

Not all of the company’s comments were bad. Alcoa also highlighted an issue I brought up in a recent Century Aluminum (CENX) article:

We think that the fundamentals for the aluminum industry are as good — or better than they’ve been in decades. Why do we say that, with the sum of the supply limitations that we see around the world with the Chinese 45 million metric ton cap with the drive towards better ESG performance in the industry.

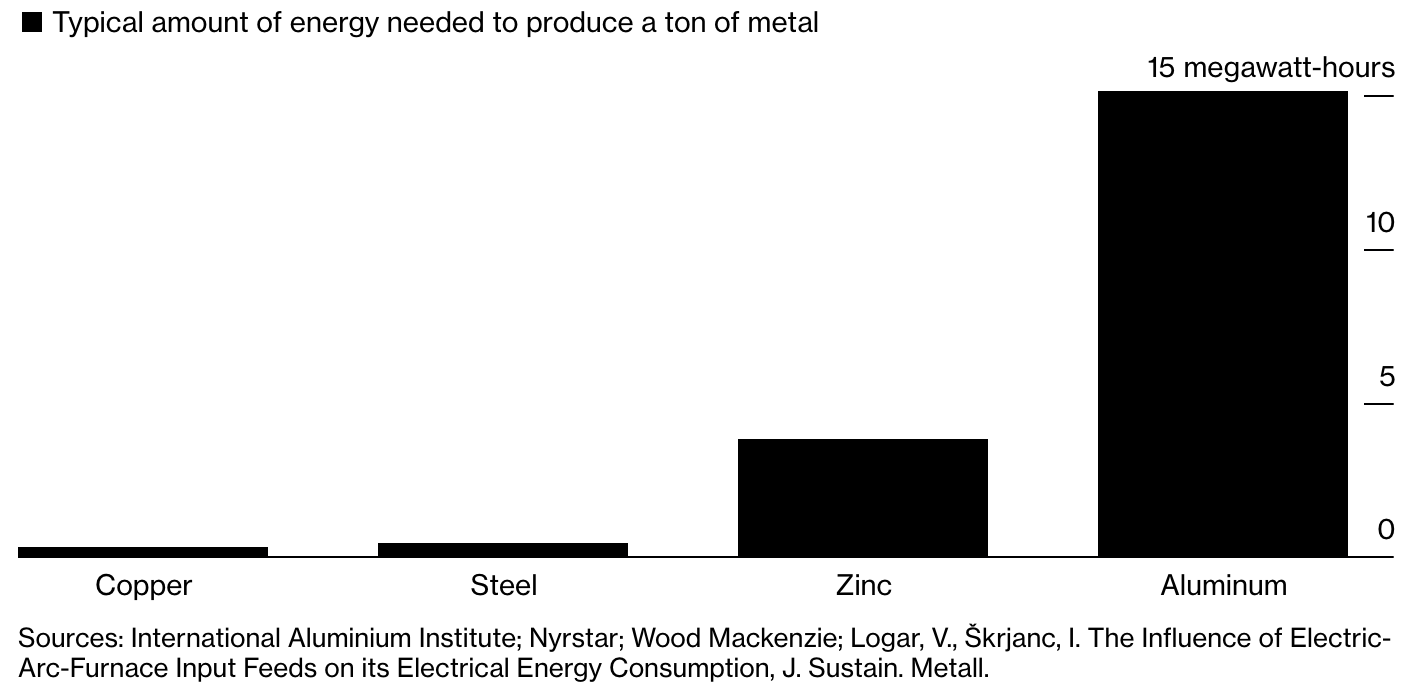

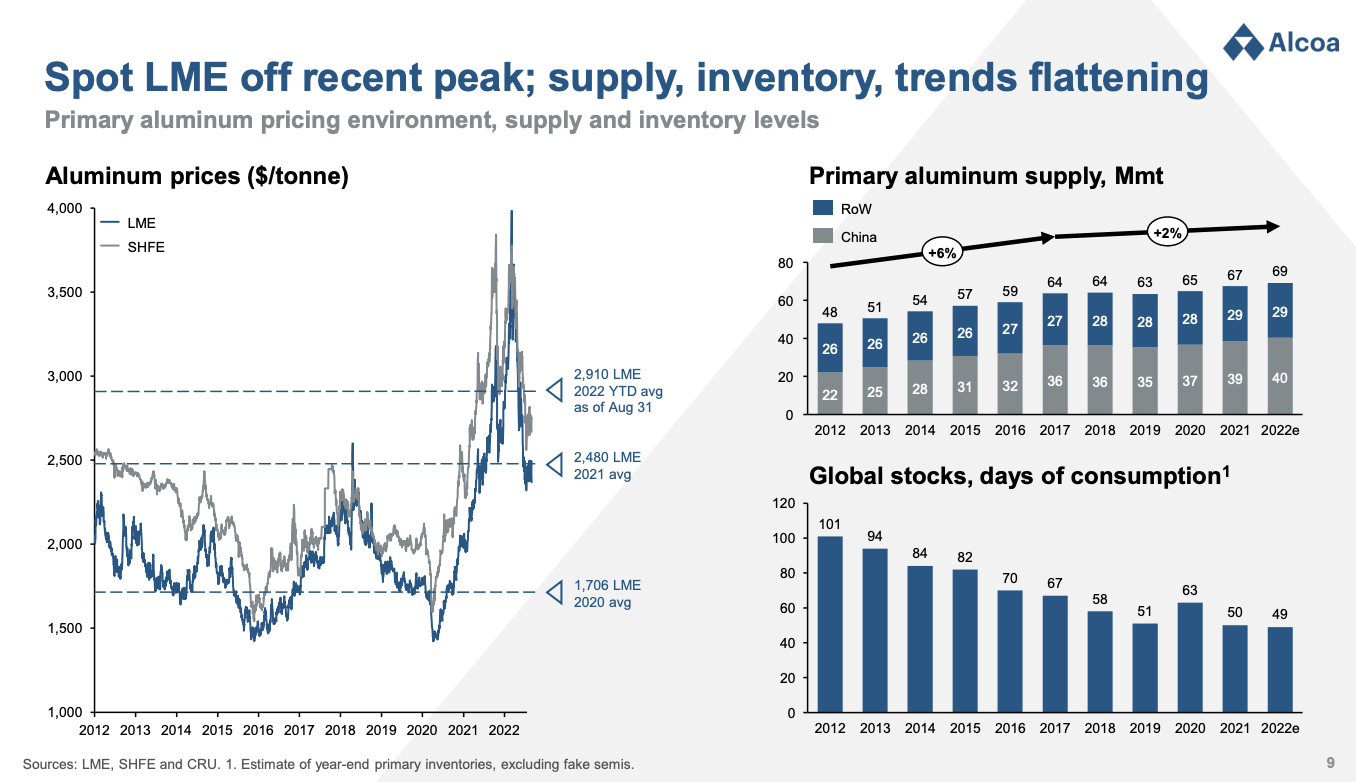

Because of high (global) energy prices, the aluminum supply is coming under pressure. While metal production is energy-intensive, in general, aluminum production beats all other major metals when it comes to energy intensity as the graph below shows.

Bloomberg

Imploding gas flows from Russia to Europe have made what is currently a global energy crisis much worse on a local level, causing aluminum plant production to be cut by 22% so far. With more to come.

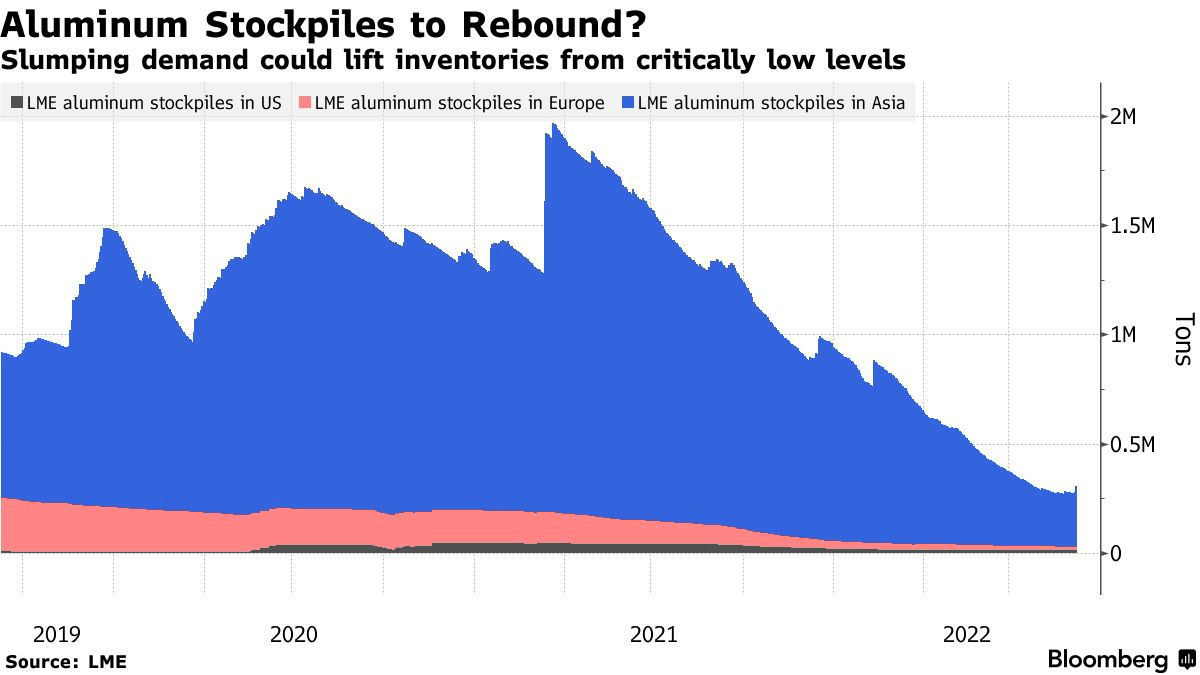

That’s bad in general, however, the situation is even worse when we incorporate falling global aluminum inventories since 2020.

As I wrote in my CENX article:

While Asia (mainly China) has always been the major driver of inventories, LMT inventories in Europe are pretty much at zero as a result of the energy crisis that started in 2021. Even Asian stockpiles have declined from roughly 1.5 million tons to roughly 250 thousand tons.

LME/Bloomberg

Right now, supply is increasing a bit as a result of weaker demand. However, supply levels won’t come back roaring.

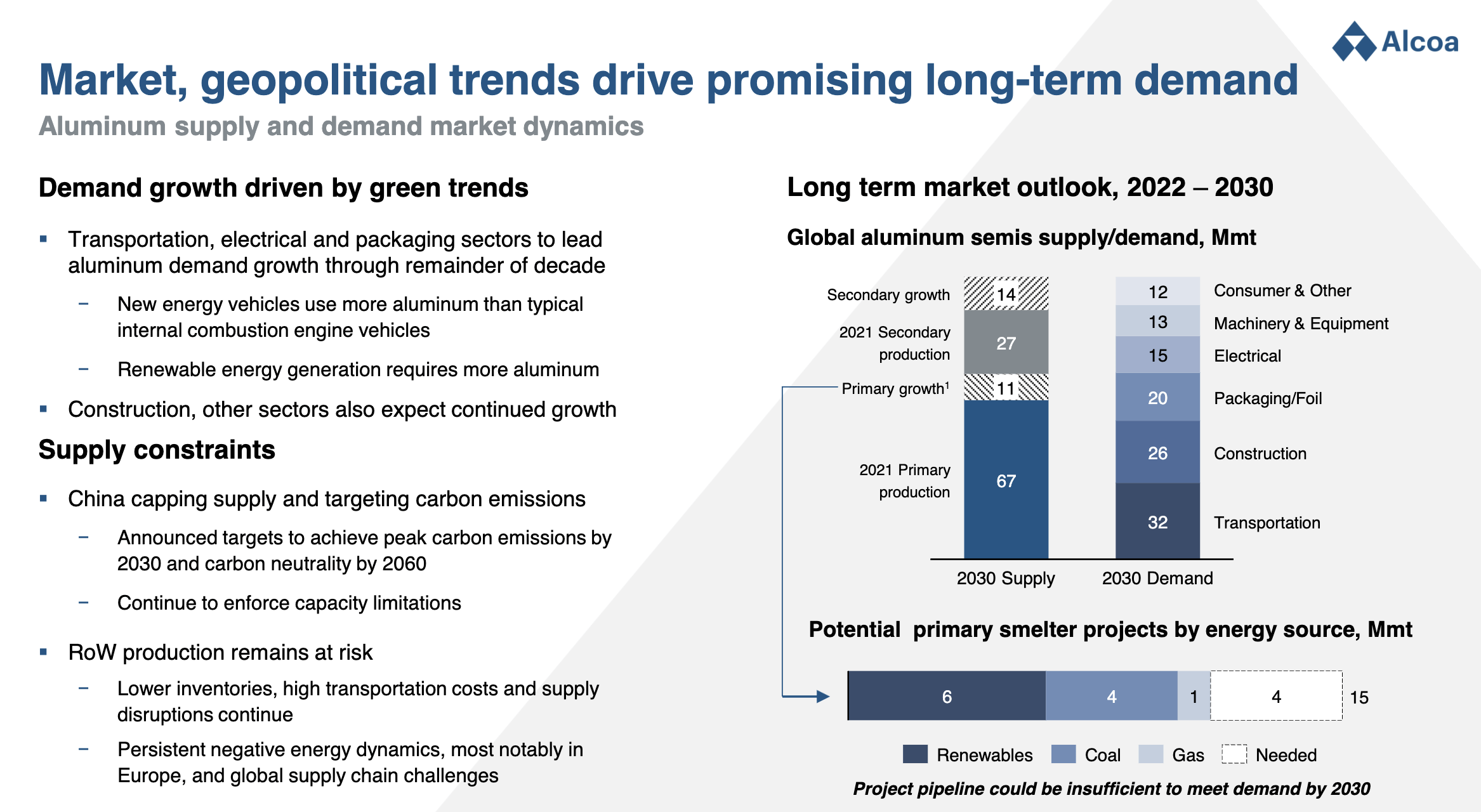

First of all, China is trying to fight pollution. They are not taking it as seriously as other nations, but at this point, it’s a serious health hazard in a lot of industrial regions. Alcoa estimates that supply in 2030 will see significant shortages and I assume these numbers do not take the current energy crisis into account as these developments became more dominant in the third quarter. Moreover, the energy crisis is hitting China as well, as fossil fuels become more expensive, making it harder to remain the world’s go-to place for cheap metals.

Alcoa Corporation

In Europe, the situation is worse as I already briefly highlighted. Companies are shutting down production at an accelerating rate. Just recently a major German producer reduced its output by 50%. According to WELT (translated):

The Speira aluminum company is drastically reducing production at its Rhine plant in Neuss due to high electricity prices. The company announced in Neuss on Wednesday that it had decided to reduce production of primary aluminum to 50 percent until further notice, and thus to just 70,000 metric tons per year. This is a consequence of rising energy costs.

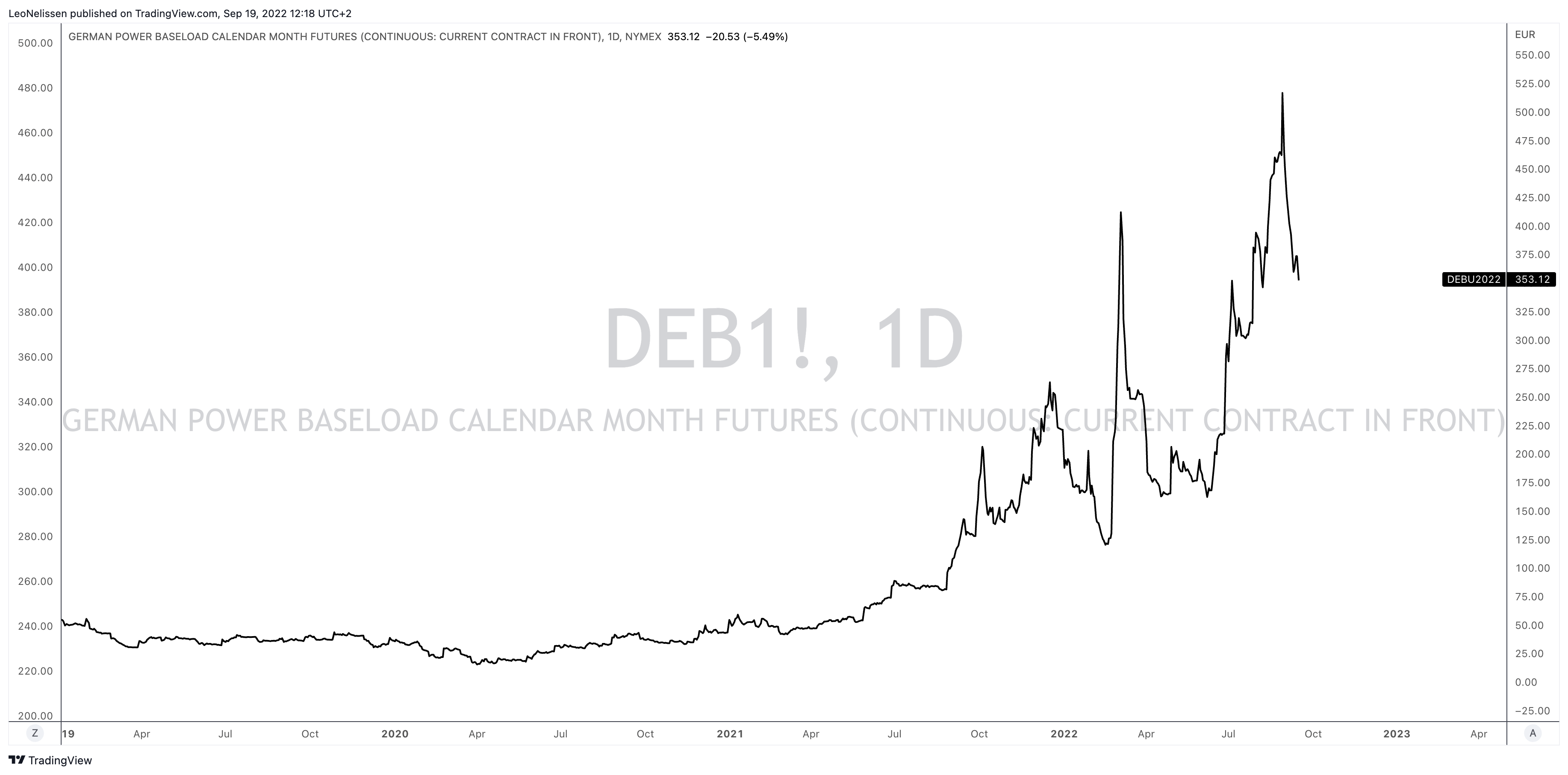

While prices have come down, baseload electricity prices in Germany are still close to 10x higher compared to pre-crisis levels.

TradingView (Germany Baseload Power Futures)

Even prior to the energy crisis, I warned that Europe was on a path of dangerous deindustrialization as a result of “green” initiatives that will make competitive production even harder. After all, China mainly uses cheap coal to produce aluminum, the US is home to the world’s lowest-cost oil and gas basins. Europe is shut off from Russian natural gas and unwilling to boost domestic gas production. That’s a toxic mix.

What It Means For Alcoa

Even if we look beyond the energy crisis, Alcoa showed that supply growth slowed significantly after 2017 as annual supply rose by 2% per year. Prior to 2017, supply growth was much higher at 6%, on average.

Alcoa Corporation

By 2030, the project pipeline will be insufficient to meet demand, according to Alcoa. Shortages could be as high as 4 million tons.

Alcoa itself has curtailed its Spanish smelter for at least 2 years due to terrible spot energy prices. This 2-year deal has been made with unions. I hope that production can restart in 2024, but we’ll see how bad things will be at that point.

Major short-term uncertainties include Chinese stimulus programs, Russian exports, and energy-driven curtailments. If the company is able to deal with these efficiently, it is setting itself up for what I expect to be a violent rebound when demand expectations rebound.

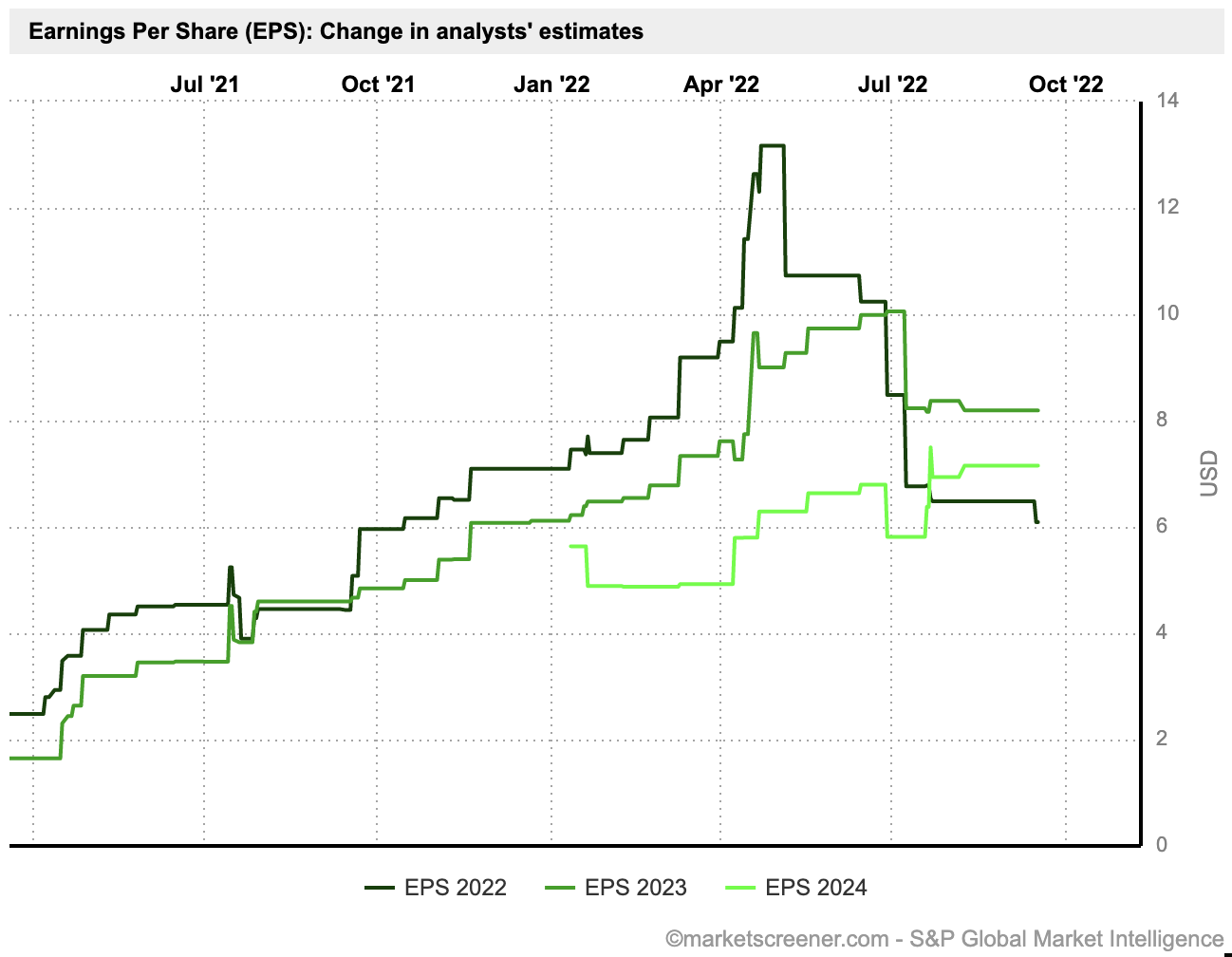

For now, analysts have started to downgrade 2021 EPS expectations as a result of high energy prices and the implications this has on demand.

MarketScreener

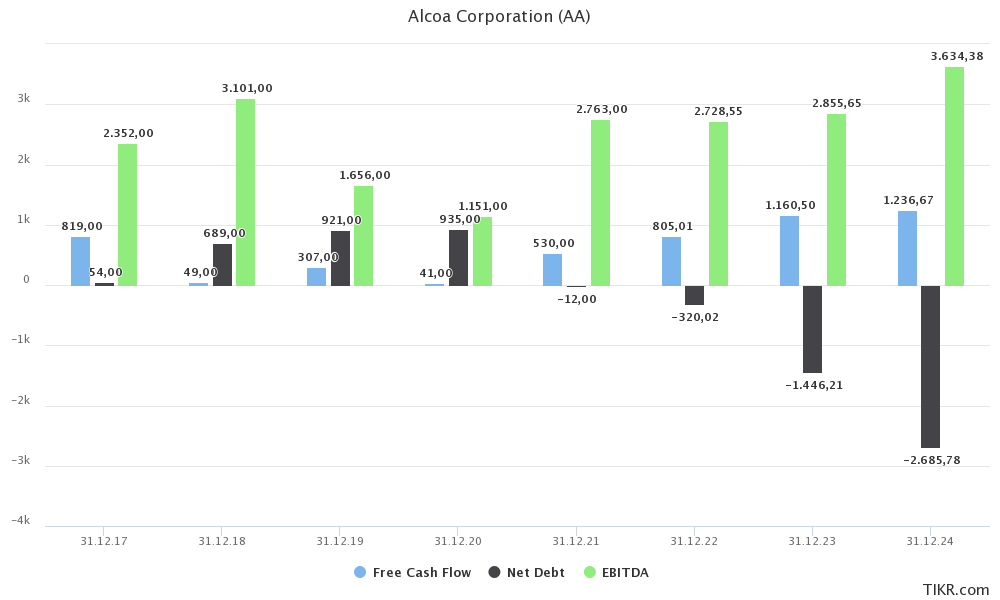

Despite challenges, Alcoa is now expected to do at least $1.2 billion in annual free cash flow after 2022. That’s 15.7% of the current $7.6 billion market cap. It is expected to push net debt into deep negative territory. As the company has no plans to grow through major acquisitions or to meaningfully boost production, the company remains in a good spot to boost shareholder returns.

TIKR.com

The company’s preferred method to distribute cash is indirect via buybacks. I expect this to remain the case as this makes more sense for a cyclical company like Alcoa. Its dividend will be raised consistently in the base case, but buybacks will be the main source of distributions.

Currently, AA shares pay a $0.10 quarterly dividend. That’s $0.40 per quarter per share or roughly 1.0% of the stock price. There’s clearly room for improvement here.

Moreover, the company has authorized an additional $500 million in share repurchases with $150 million remaining under its previous authorization. That’s a total of $650 million outstanding. That’s 8.5% of the company’s market cap.

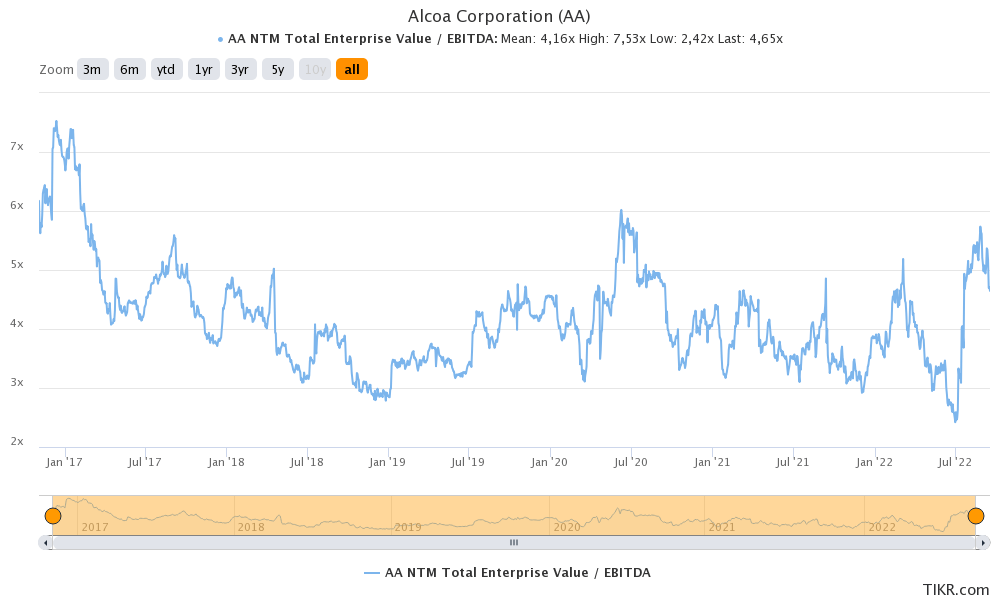

Given that the company is not expected to suffer for long, in my opinion, the valuation has become quite attractive. The company is now trading at 3.1x 2023E EBITDA of $2.9 billion. That’s based on an $8.8 billion enterprise value consisting of its $7.6 billion market cap, $1.5 billion in expected 2023 net cash (negative net debt), $1.6 billion in minority interest, and $1.0 billion in pension-related liabilities.

Even if expectations come down further – we need to be aware of the high likelihood that this happens – the company is very attractively valued. Since its spin-off, the company has traded at 4x NTM EBITDA most of the time.

TIKR.com

I believe that even under these circumstances, the company is at least 40% undervalued.

If demand rebounds – as measured by economic indicators like the Empire State/Philly Fed, I expect aluminum prices to rapidly accelerate, providing a similar upswing the stock experienced after the 2020 lockdowns.

Takeaway

Alcoa is in a tough spot, two years after one of the strongest bull cases in recent history started. The company is now seeing pressure on demand, lower pricing, and high input costs related to the global energy crisis.

However, Alcoa is in a different space. While lower economic estimates hurt its stock price, the company has a much healthier balance sheet and a much stronger outlook.

I expect demand expectations to rebound as soon as the Fed takes the foot off the gas pedal, which could be in the first half of 2023. At that point, we will probably see a demand rebound while supply remains subdued. This is poised to cause another steep surge in aluminum prices similar to the one after the 2020 lockdowns. However, this time, I expect it to last a bit longer than 2 years.

If that happens, Alcoa will be one of the biggest winners in the industry. It has efficient operations, a healthy balance sheet, and the ability to boost free cash flow to sustain close to 10% in annual shareholder distributions.

Moreover, even without that bull case, Alcoa shares remain undervalued.

The best way to play this is to buy a small AA position and to add gradually on weakness. However, make sure to not go overboard. AA remains very volatile and I do NOT recommend anyone to go overweight cyclical stocks. Especially given that we’re still in a very uncertain phase of the economy.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment