BrilliantEye

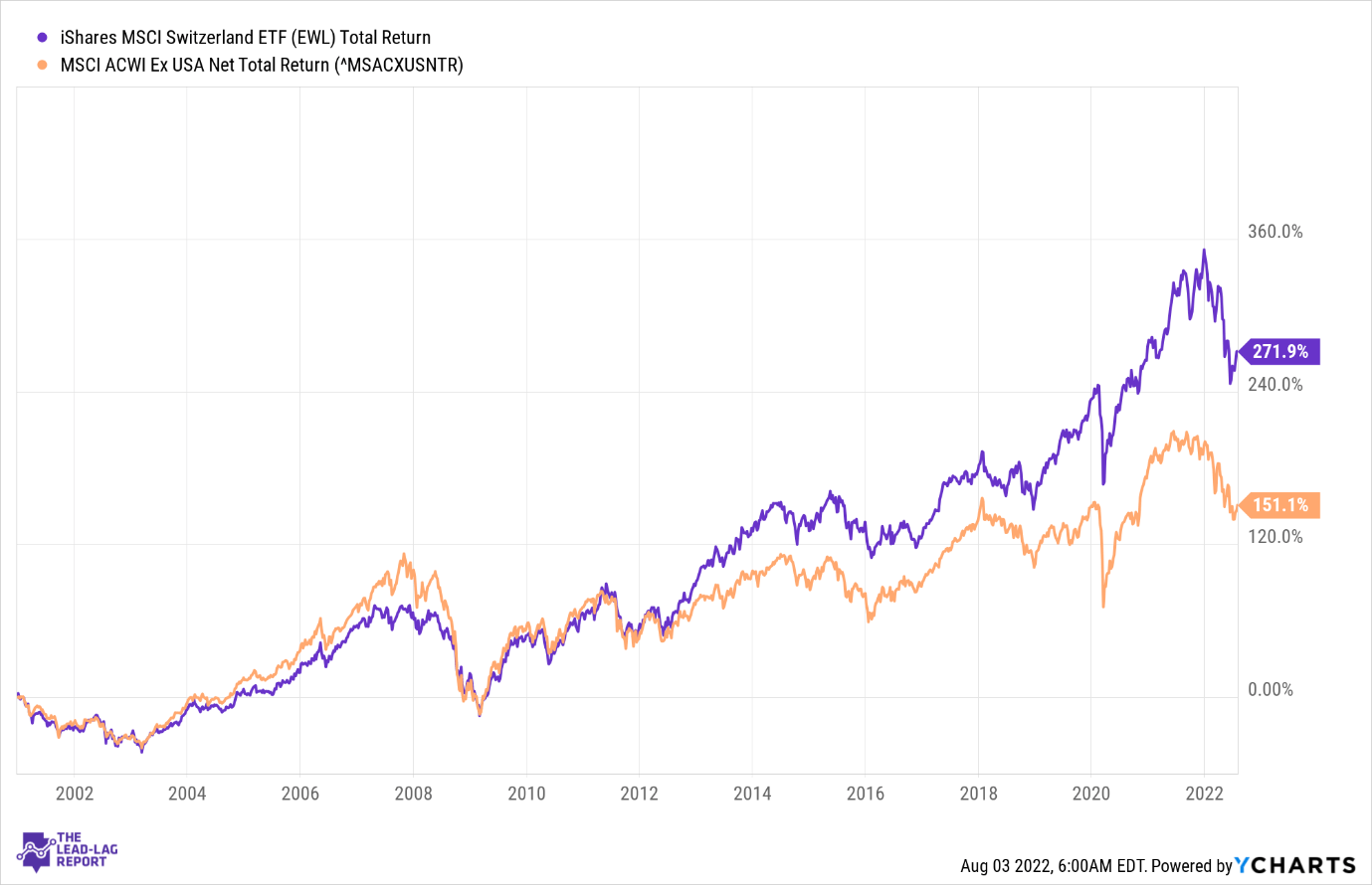

The iShares MSCI Switzerland Capped ETF (NYSEARCA:EWL) with nearly $1.5bn in assets, and a trading history of close to 27 years, has built up a solid name for itself in the ETF world. Over its long history, it has proven to be an outstanding alpha-generator, delivering returns that are 1.8x the MSCI All Country World Index (ex-US).

YCharts

Should you be getting on board with an ETF of this sort, and is now a good time? Well, here are some of my thoughts that could help you make a decision.

Major Themes

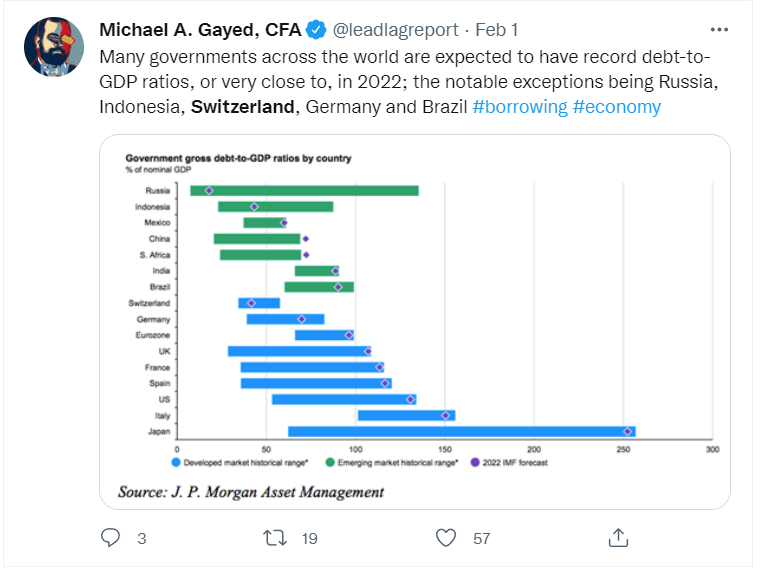

Subscribers of The Lead-Lag Report would note that I’ve been very critical of economies that leverage the system with inordinate levels of debt. The US has been one of the chief paragons of this uncomfortable scenario, with national debt to GDP at around the 130% mark. In contrast, Switzerland is one of those economies you’d find at the opposite end of the debt spectrum.

Earlier this year, I had put out some content on the timeline of The Lead-Lag Report, highlighting how Switzerland was one of the economies that were better positioned to cope with excess leverage as its debt to GDP levels remains fairly well-controlled at around the 40-43% mark. At a time when rates across most places across the world are being lifted (adding to debt servicing concerns), Switzerland remains relatively well-positioned.

Twitter

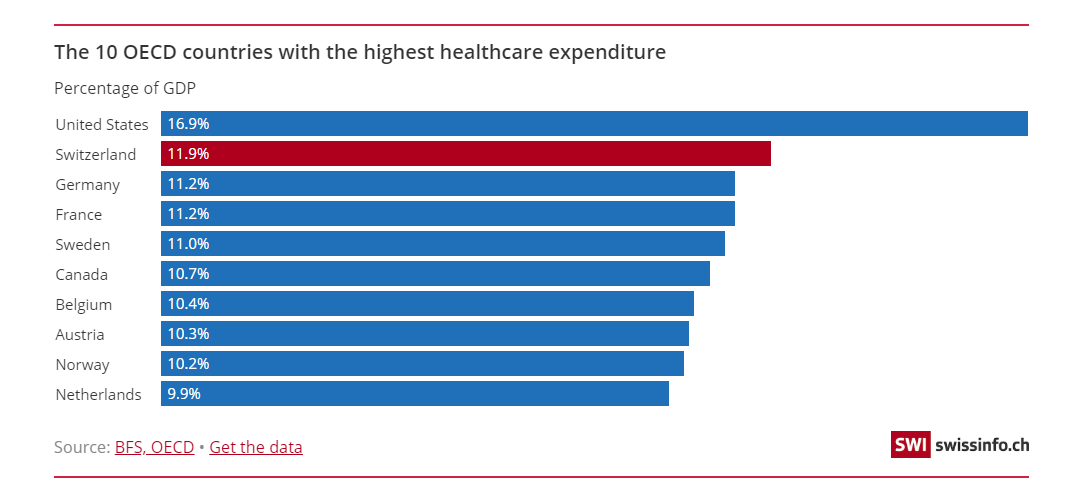

The other thing to note is that the Swiss healthcare system is a very lucrative business for those involved (this works well for EWL as more than a third of the portfolio are stocks from the healthcare sector). Outside the US, no other OECD economy (out of 37 other nations) spends more on healthcare than the Swiss (almost 12% of GDP). Recent reports show how insurance premiums are relatively high and have been steadily increasing over time.

Swiss Info

The affordability quotient could be flagged if per capita income levels were low, but that certainly isn’t the case with Switzerland which has the second highest per capita GDP in the world ($86850, source: IMF). Supplementing all this, it’s an economy that will likely attract a lot of foreign capital on account of the ecosystem it facilitates for innovation, reportedly one of the best in the world, as noted in a tweet on the timeline of The Lead-Lag Report.

Twitter

Speaking of flows, I believe the prospects for the Swiss Franc have improved markedly in recent weeks. Inflation last month came in at 3.4%, the fifth successive month where it has been above the Swiss Central Bank (SNB)’s target range of 0-2% (according to BAK Economics, by the end of FY222, inflation will still be over the comfort range at 2.6%). A lot of this inflation is imported inflation and coming from the trade channels, and to counter the effects of this, they’ve sought to make the Swiss Franc a lot more competitive. In June, rates were hiked by a mammoth 50bps and caught a lot of people off-guard. Whilst the cash rate is still in negative territory at -0.25%, I don’t believe it will linger there for too long. In fact, market expectations point to another 50bps hike in September and another 25bps hike in December.

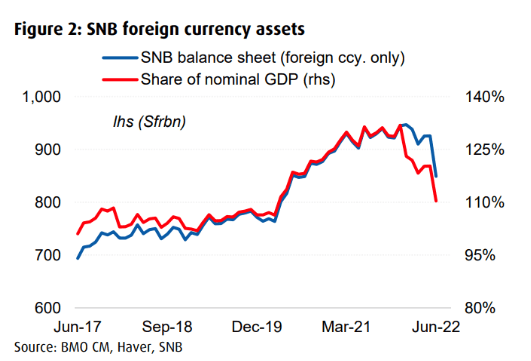

Crucially, what one must also consider is that the Swiss Bank has been unloading its massive FX warchest off late to help augment currency dynamics. According to BMO Capital Markets, foreign currency assets on the SNB’s balance sheet have now declined by 10% since the start of the year. The bank still has ample elbow room to use this lever, as foreign currency assets still account for a heightened figure of 110% of nominal GDP.

BMO Capital Markets

Conclusion

Finally, as noted in the ‘Opening thoughts’ section of The Lead-Lag Report, I’ve been paying a lot of attention to the flattening of the yield curve, which shows that investors are shifting to defense and taking risks off the table. If a recessionary environment were to take hold of global markets, I suspect EWL’s defensive nature could come to the fore. Notwithstanding the allure of the Swiss France as a safe haven, you also have to consider that EWL is innately a very defensive portfolio, with 57% of the weighting attributed to the healthcare and consumer staples stocks. And the cherry on the cake is that forward valuations also look a lot more appealing than what they were around a year ago. Currently, you can pick up EWL at 16 forward P/E, whereas a year ago, it was in the 22-25 range.

Anticipate Crashes, Corrections, and Bear Markets

Anticipate Crashes, Corrections, and Bear Markets

Sometimes, you might not realize your biggest portfolio risks until it’s too late.

That’s why it’s important to pay attention to the right market data, analysis, and insights on a daily basis. Being a passive investor puts you at unnecessary risk. When you stay informed on key signals and indicators, you’ll take control of your financial future.

My award-winning market research gives you everything you need to know each day, so you can be ready to act when it matters most.

Click here to gain access and try the Lead-Lag Report FREE for 14 days.

Be the first to comment