Leonid Sorokin

A wise man told me – “you don’t fight the Fed.” As the Federal Reserve expanded its balance sheet, reduced interest rates, and implemented other easing measures, the central bank decreased borrowing costs, stimulated growth, and flooded markets with ultra-cheap capital. If you were short stocks or didn’t go long the market during this post-2008 ultra-easy monetary environment, you fought the Fed and probably missed out on years of stellar gains. However, we want to remember that the market goes both ways, and just as you don’t want to fight the Fed when it’s easing, you also don’t want a fight with the Fed when it’s tightening interest rates. Many market participants recently learned this lesson the hard way, but the class is not over yet.

While the S&P 500/SPX (SP500) has dropped by 25% from its top, more downside is probable as the Fed continues tightening. Fundamental, technical, and psychological factors are converging, which support lower stock prices into the fall and winter months. My S&P 500 base-case bear-market-bottom target-range remains at 3,200-3,000. However, the market could overshoot and drop into a lower range (2,800-2,400).

The Technical Image – There Is A Chance

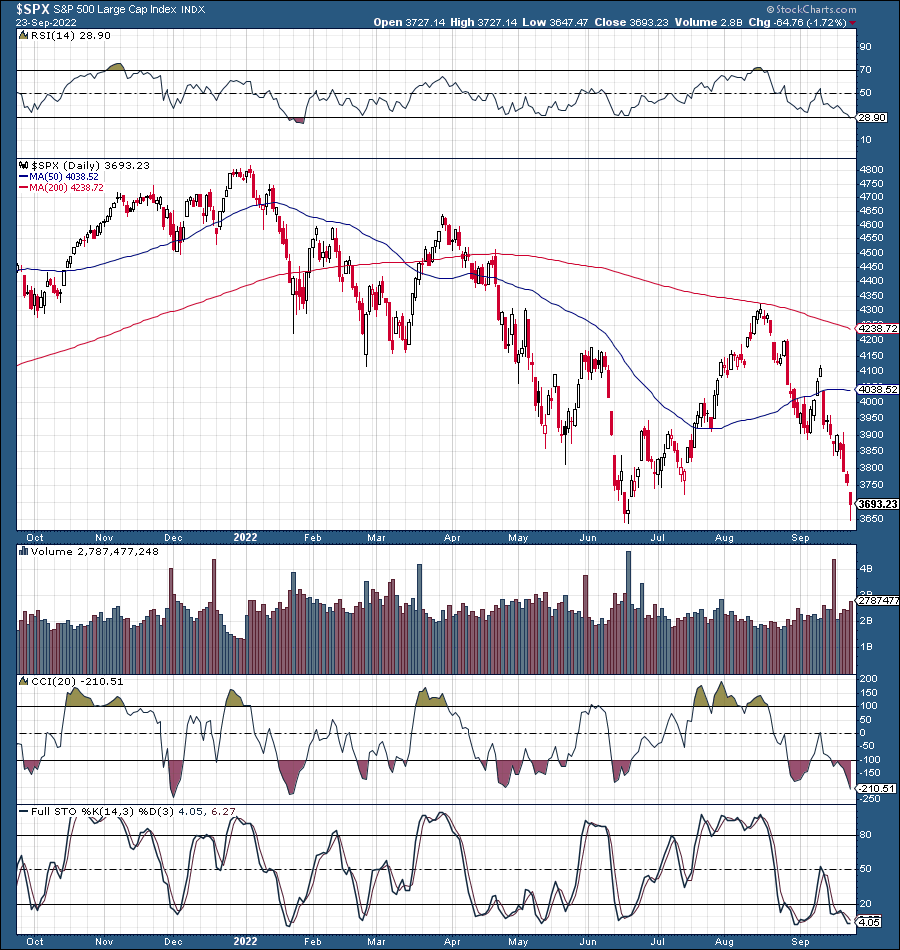

SPX (StockCharts.com)

There’s a relatively low probability that the SPX will put in a sustainable double bottom around the 3,650 level. However, while there’s a chance, the likelihood of a long-term bottom here is very low. We could see a short-term rebound to about the 3,800-4,000 resistance zone, but selling pressure should resume after that. While the market is modestly oversold here, we still have not seen any of the hallmark signs of a true long-term bottom. It will probably require panic-like, capitulation-style selling before a bear market low forms.

Higher Interest Rates Are Approaching

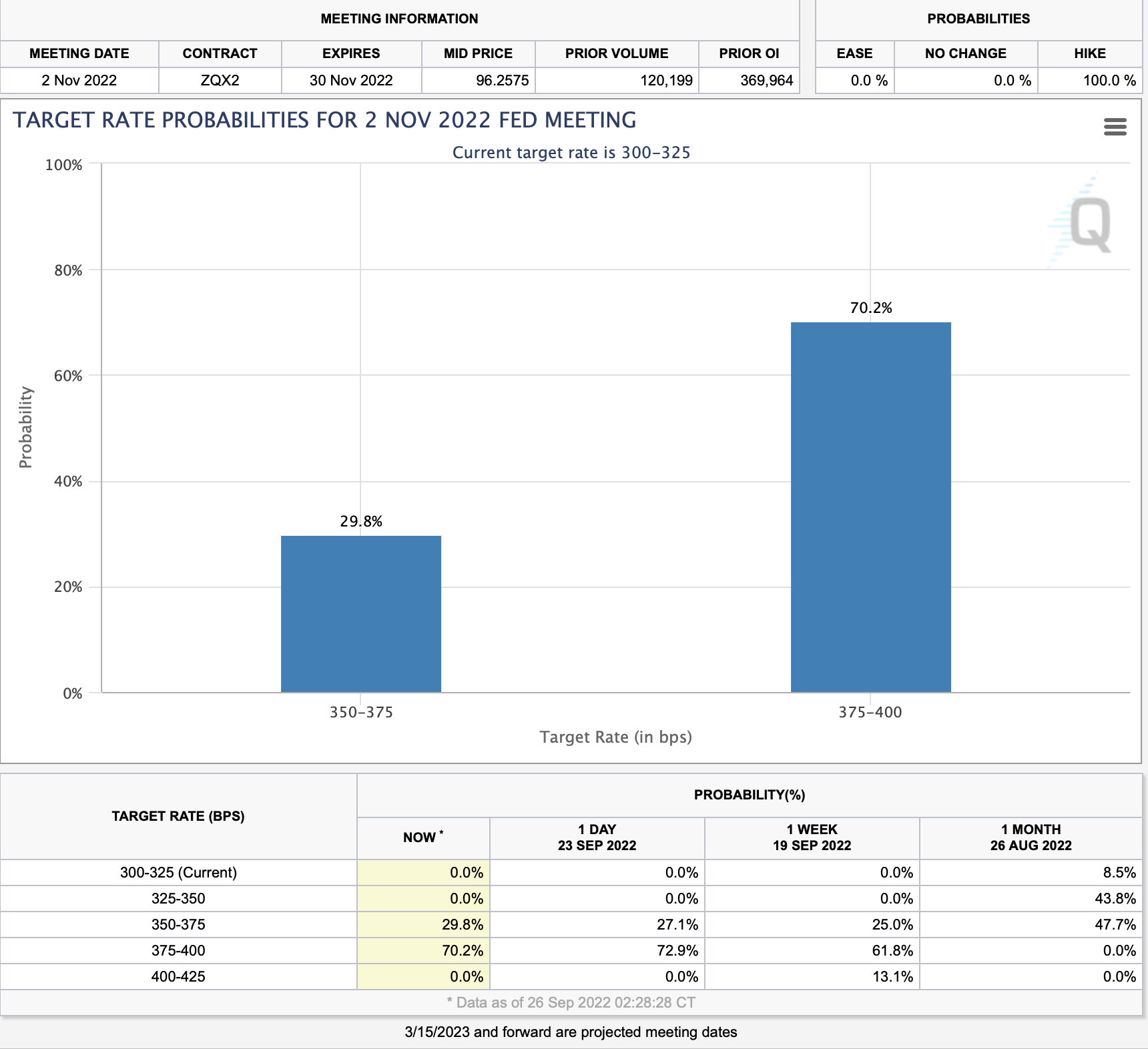

As anticipated, the Fed raised the benchmark rate to 3-3.25%. This rate increase elevates rates to a relatively high level, which could exacerbate the economic slowdown in the coming months. Increased pressure on the consumer due to rising borrowing costs and inflation should lead to worsening consumer confidence and spending. Also, as rates rise, corporations should face higher expenses due to inflation and increased borrowing costs. Moreover, the Fed is not done yet. There’s a high probability that we will see another 75 basis point increase at the November FOMC meeting. We should see the benchmark at about 4% going into year-end.

Fed Watch (CMEGroup.com)

It may not be easy to fathom, but rates are heading even higher from here. The benchmark will probably increase to around 4% at the November meeting. Moreover, the Fed may keep the benchmark at about 4-5% throughout 2023. Elevated rates should continue driving up borrowing costs, constricting the economy as we advance in the coming months. The economy is not accustomed to such high-interest rates, and we should see the slowdown worsen as we move into the fall and winter months.

Upcoming Earnings – A Big Concern

A primary concern is the upcoming earnings season. Q3 earnings will kick off around mid October, and while we’ve seen some downward revisions, we may see steeper revenues and EPS declines than we’d hoped. Inflation and higher borrowing costs lead to margin compression and lower profitability, while worsening consumer spending could lead to revenue declines. Additionally, companies will likely need to adjust forward guidance due to higher rates, persistent inflation, and the increased slowdown effect. Therefore, we could see a higher percentage of misses, leading to more stock price drops. Furthermore, the uncertainty regarding the November interest rate increase should fuel volatility throughout the earnings season.

Valuations – Should Get Adjusted Lower

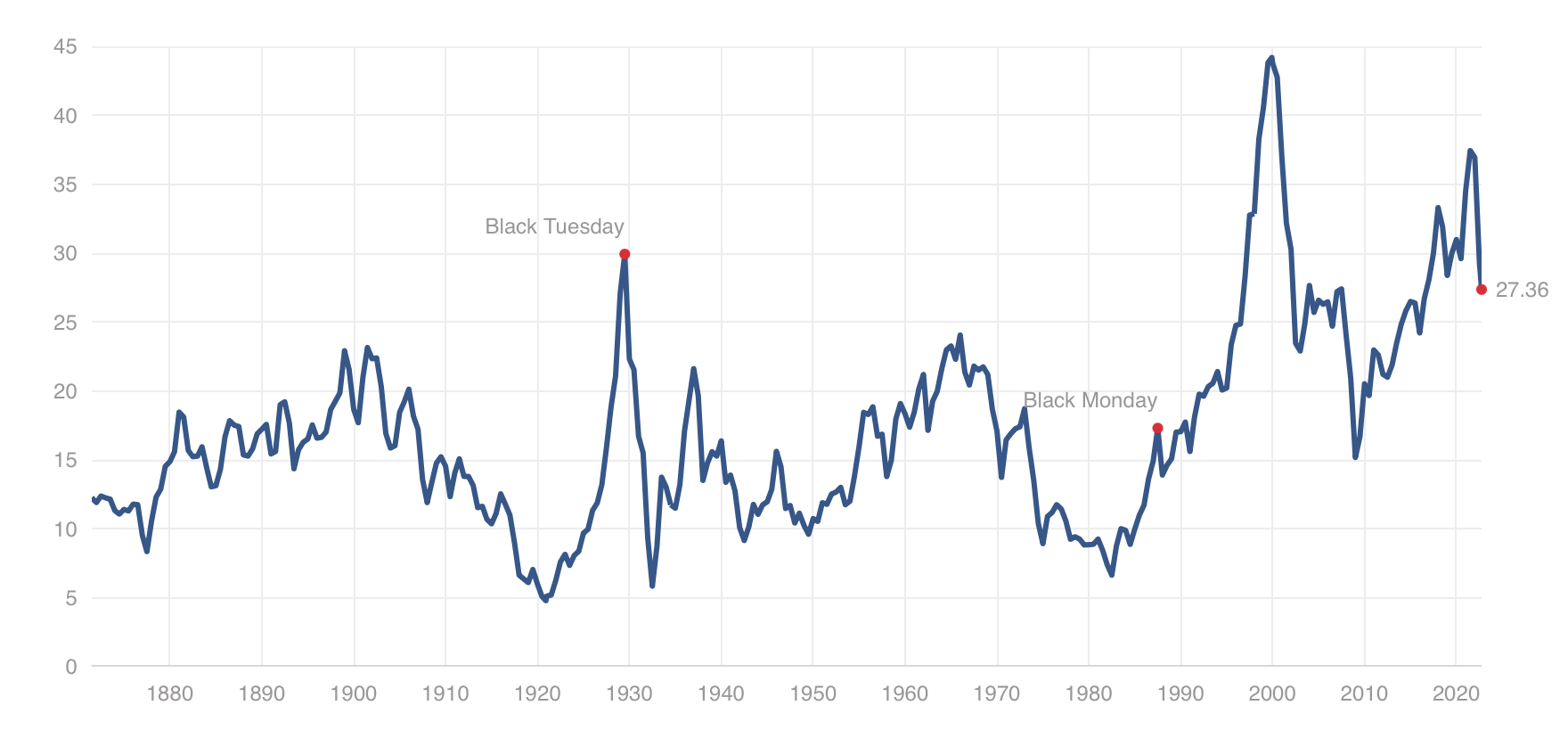

Shiller P/E Ratio

Shiller P/E ratio (mltpl.com)

Despite a recent drop from the highs, the CAPE P/E ratio remains relatively high, illustrating that valuations still likely have room to adjust lower. The S&P 500’s historical mean CAPE ratio is only around 17, roughly 37% below current levels. We should consider that earnings and earnings expectations could worsen considerably in the coming months, leading to widespread EPS and revenue estimate adjustments. Therefore, we could see the SPX’s Shiller P/E ratio fall to around the 22-20 range, implying a possible drop to about the 3,200-3,000 support level. However, in a bearish case scenario, if the market overshoots to the downside, the Shiller P/E ratio could revert to its mean of about 17, implying a crash to about 2,500 is possible.

Be the first to comment