Muhammet Camdereli/iStock via Getty Images

The iShares MSCI Brazil ETF (NYSEARCA:EWZ) is once again trading at bargain levels. The ETF has been hammered over the past month due to the drop in iron ore and oil prices, which have hit the two largest stocks, Vale and Petrobras, hard. These stocks now yield 15% and 28% respectively, which has sent the yield on the MSCI Brazil index above 10%, and forward estimates put the yield above 11%. At this yield, the market appears to have already priced in the risks stemming from the upcoming election and a possible global recession.

The EWZ ETF

The EWZ tracks the performance of the MSCI Brazil index and charges an expense fee of 0.57%. The ETF holds 50 companies at present and is heavily weighted towards commodities. The Materials sector accounts for 21% of the index, thanks to iron ore giant Vale, which has an 18% share. The Oil & Gas sector accounts for an additional 18% due to oil major Petrobras. Due to the high degree of volatility of the Brazilian currency, the EWZ’s performance has tended to be driven as much by the BRL as it has by the stock market itself. However, the key underlying driver of both markets is the price of commodities, as higher export prices benefit both local earnings and the appetite for local currency in dollar terms. The EWZ’s dividend yield is currently an impressive 6.1% and this should rise over the coming month as ETF payments track the underlying MSCI Brazil index, whose dividend yield now sits at a huge 10.3%.

Cheaper Than At The Global Financial Crisis Low

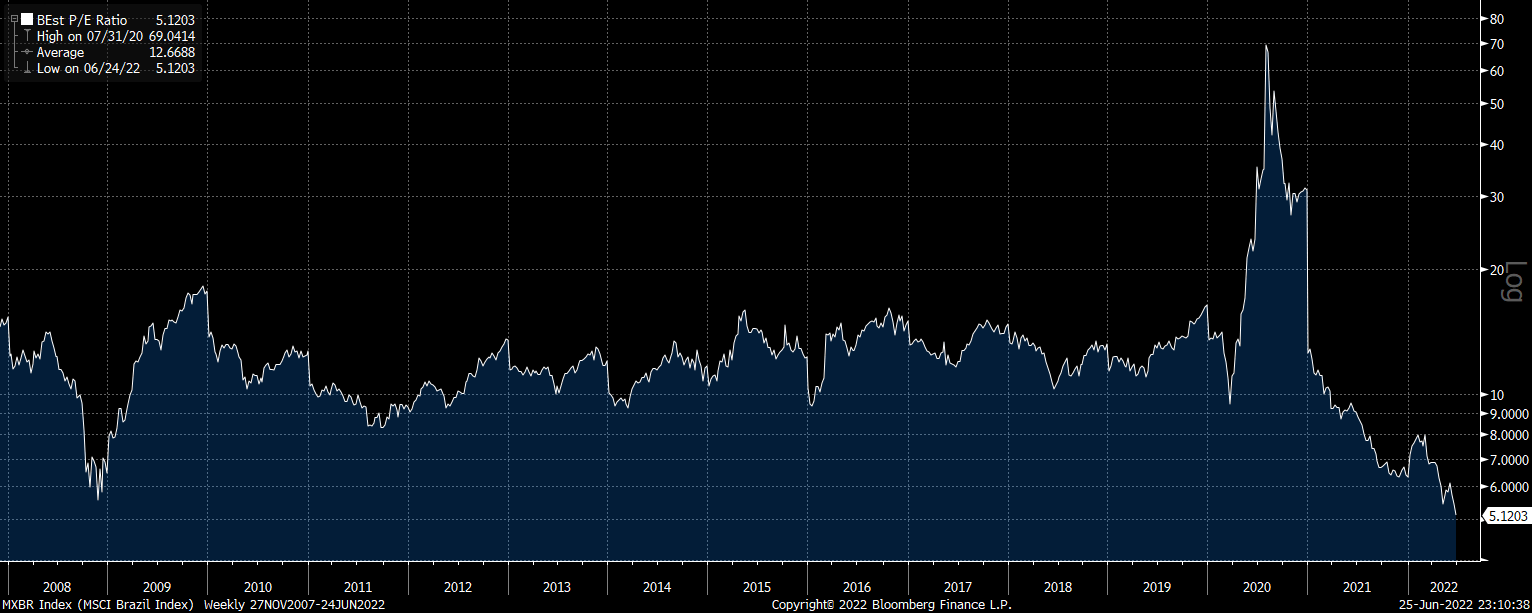

The MSCI Brazil index now trades at a forward PE ratio of 5.1x, which is below the nadir seen at the height of the Global Financial Crisis in 2008, when the index hit a valuation low of 5.5x. In total return terms, the index has delivered 5% annual returns since then even though valuations have fallen to new lows.

MSCI Brazil Forward PE Ratio (Bloomberg)

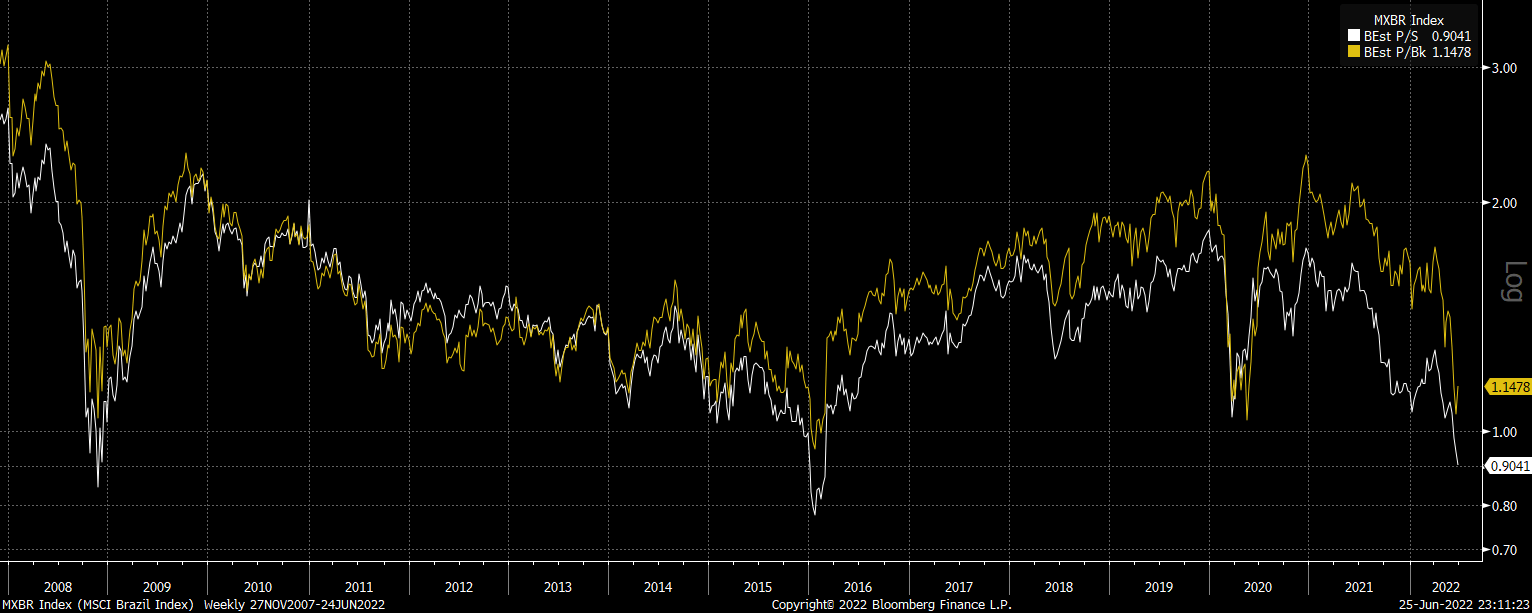

While this 5.1x forward PE partly reflects elevated profit margins and returns on equity, which should be expected to mean revert lower over the long term, both price/sales and price/book ratios are also historically cheap, trading around their 2008 crisis lows.

MSCI Brazil Forward PS And PB Ratios (Bloomberg)

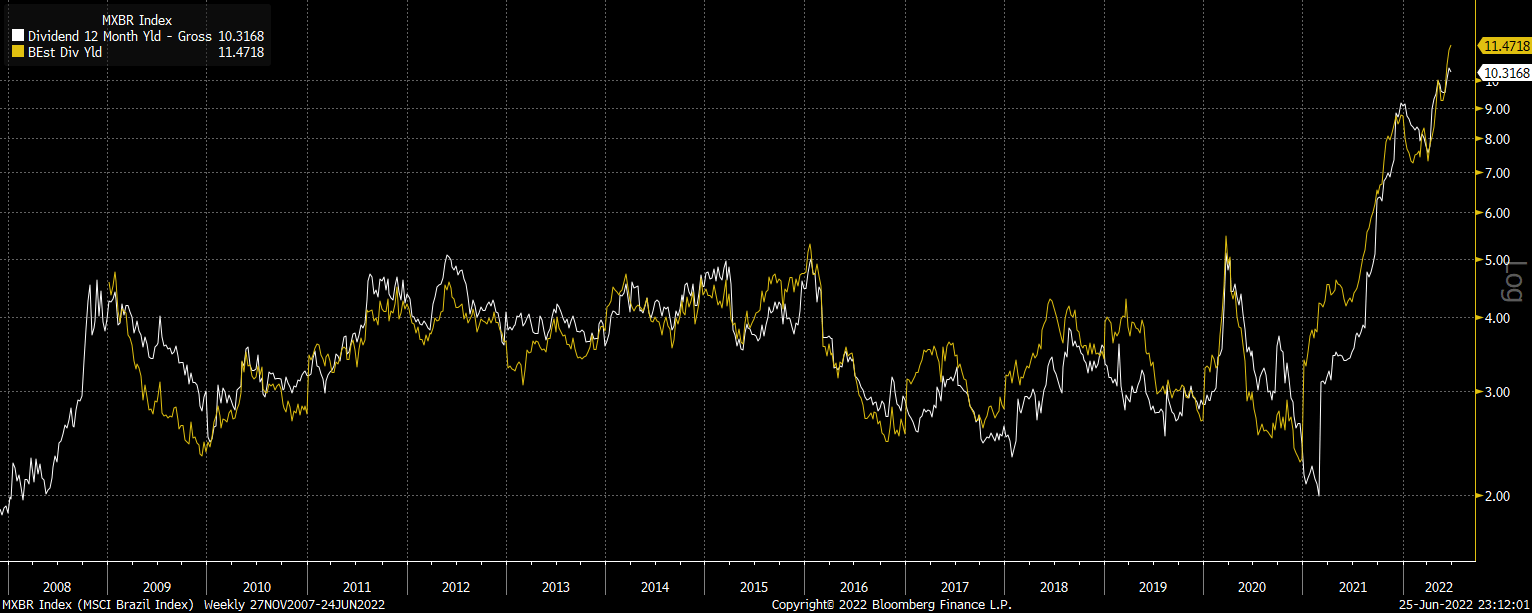

Furthermore, the dividend yield is incredibly high. Even with a trailing dividend yield of 10.3%, analysts expect payouts to rise over 10% over the next 12 months, putting the forward yield at a whopping 11.5%, which is more than double the yield seen at the GFC low. As I argued, this largely reflects the high yields on Vale and Petrobras, which make up 18% and 14% of the index respectively, but even excluding these two the index’s yield is above 5%.

MSCI Brazil Trailing And Forward Dividend Yield (Bloomberg)

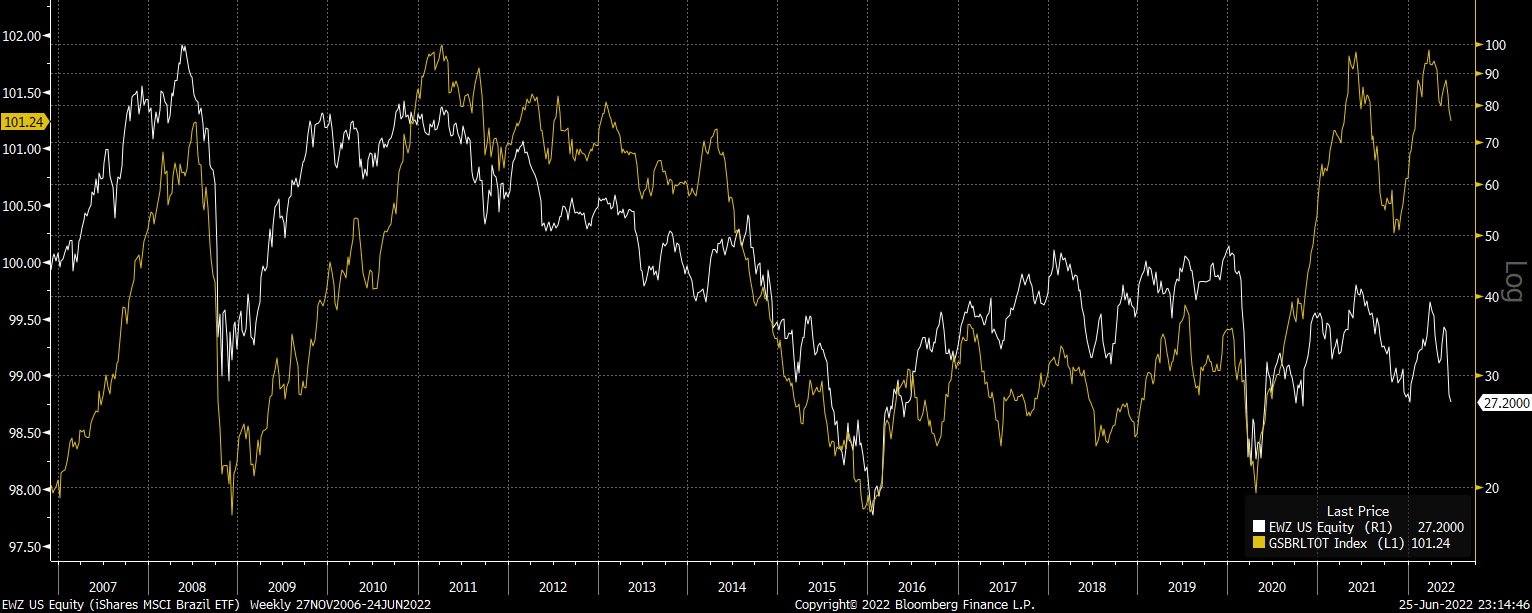

Valuations are also at odds with the country’s still-strong terms of trade picture. Even after the recent fall in iron ore prices, Brazil’s exports remain highly priced relative to exports, which again contrast greatly with the situation that occurred at the last valuation low in 2008. High levels of reserves and positive terms of trade both suggests that the currency does not face any major downside risk that could undermine the EWZ.

EWZ Vs Brazil Terms Of Trade (Bloomberg, Goldman Sachs)

Election Risks Appear More Than Priced In

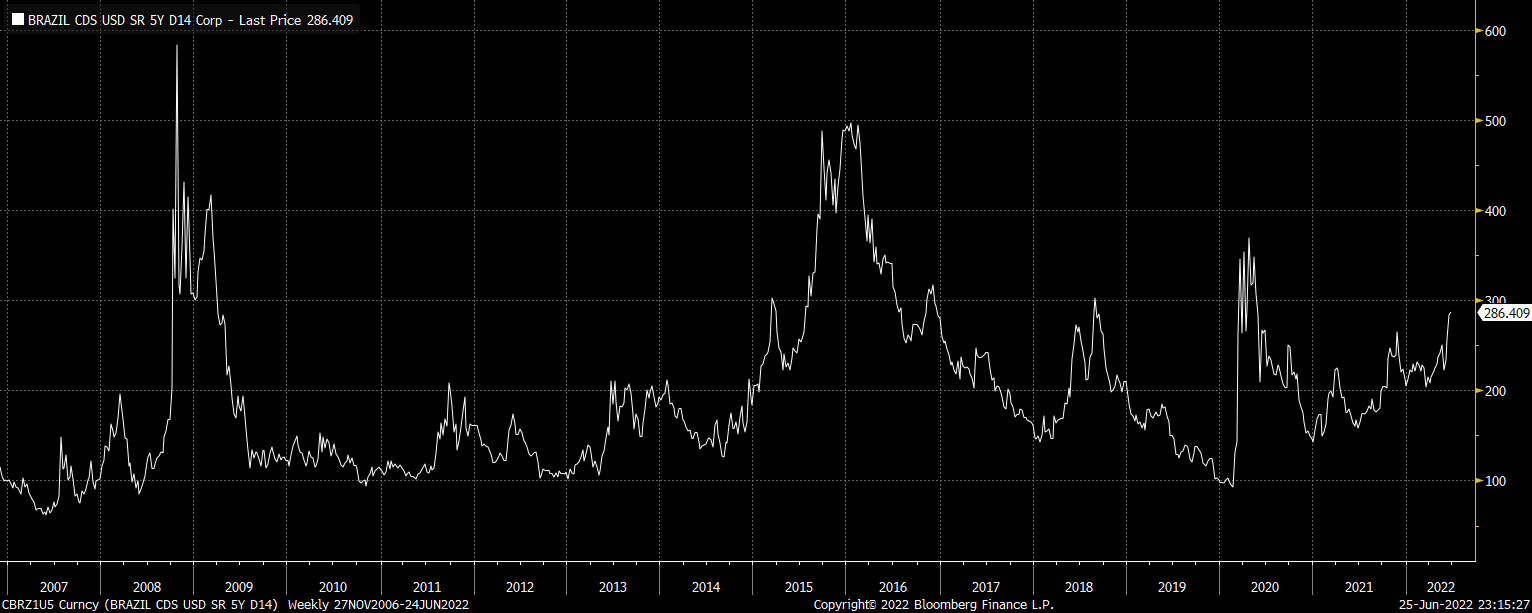

The only factor that seems to partly justify such extremely low valuations on Brazilian stocks is the looming threat of a return to power of Left-wing former President Luiz Inacio Lula da Silva or a coup led by President Jair Bolsonaro and a return to military dictatorship. With Lula leading the polls by a wide margin and Bolsonaro threatening to not accept the election result if it goes against him, it is fair to say that Brazilian stocks should trade at a discount to their emerging market peers. However, such incredibly cheap valuations contrast with the relatively low degree of country risk, as shown by the low credit default swap spread. Even after the recent spike, the 5-year CDS is just 286bps, which is less than half the level seen at the height of the GFC. This suggests that election risks are more than priced into current equity market valuations.

Brazil 5-Year CDS (Bloomberg)

Summary

Brazilian stocks are incredibly cheap, having taken a beating over the past month amid falling commodity prices and rising election risks. However, the country’s terms of trade remain positive, and credit default swaps show that country risk remains relatively mild. These factors suggest that the EWZ is a great buy, and I believe investors will be rewarded with double-digit long-term returns for buying at these levels.

Be the first to comment