monzenmachi/iStock via Getty Images

Elevator Pitch

I have a Hold investment rating for Xerox Holdings Corporation’s (NASDAQ:NASDAQ:XRX) shares.

I have a mixed view of XRX as a potential dividend stock. On the positive side of things, Xerox’s dividend yield of 7% is very attractive, and the company’s current dividends should be sustainable. On the negative side of things, XRX isn’t a good dividend growth stock as it has other capital allocation priorities limiting its capacity for future dividend growth. Moreover, there is a risk of permanent capital losses (stock price decline) in the long term if Xerox fails to diversify its revenue base.

In a nutshell, Xerox isn’t the perfect dividend stock (good yield but limited growth), and this supports a Hold rating for XRX.

XRX Stock Key Metrics

It is wise to review Xerox’s share price and business performance, prior to evaluating whether XRX is a good dividend stock.

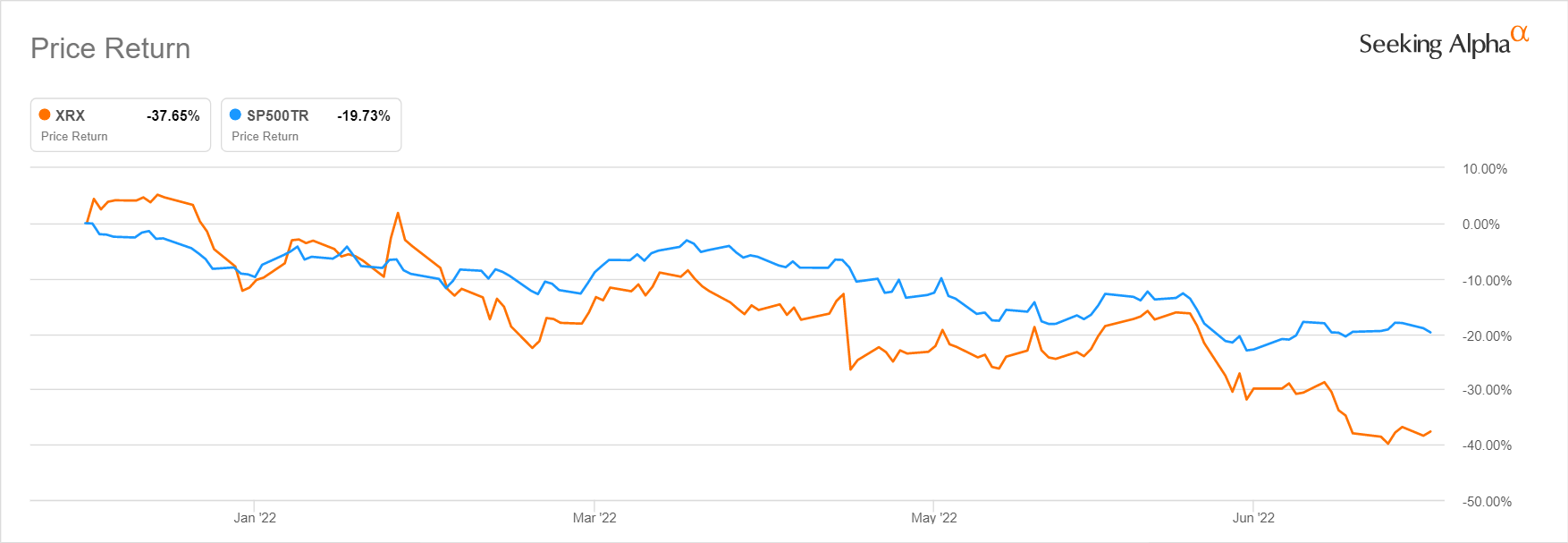

Xerox’s shares have underperformed in 2022 thus far. On an absolute basis, XRX’s share price fell by -37.7% year-to-date. On a relative basis, Xerox has done far worse than the S&P 500 which has suffered from a relatively narrower -19.7% decline in the same period as per the chart presented below.

XRX’s Stock Price Chart For The 2022 Year-to-Date Period

Seeking Alpha

Assuming XRX’s negative share price momentum continues and the company can still maintain its current dividend payouts, investors can be patient and accumulate the company’s shares at lower prices which translate to higher dividend yields. On the flip side, the drop in Xerox’s stock price might imply that investors expect the company’s cash flow and dividends to be lower going forward, and this negative view is supported to some extent by XRX’s poor Q1 2022 financial performance.

Xerox posted flattish revenue growth on a YoY basis in Q1 2022, with its top line decreasing marginally by -0.7% adjusted for foreign exchange effects. It was XRX’s first quarter bottom line that really disappointed the market. Xerox turned from a positive non-GAAP adjusted earnings per share or EPS of +$0.22 in Q1 2021 to a non-GAAP net loss of -$0.12 per share in Q1 2022. The Wall Street analysts had previously anticipated that XRX will achieve a positive EPS of +$0.13 in the first quarter of 2022, so a loss had come as a major negative surprise.

XRX explained at its Q1 2022 investor call on April 21, 2022 that “inflationary pressure across our cost base and the growth in supply chain costs” were worse than what the company had expected, and this led to losses for Xerox. Looking ahead, Xerox noted in its first quarter results presentation slides that “we are seeing an acceleration of inflationary pressure on costs throughout our business” and stressed that “the realization of that (guided QoQ margin) improvement will largely depend on macroeconomic factors.”

Xerox’s Q1 financial metrics and forward-looking management commentary suggest that there is significant uncertainty relating to the company’s near-term financial performance.

I touch on XRX’s dividends in the next section.

What Should Investors Know About Xerox’s Dividend?

In deciding whether to invest in Xerox as a dividend play, investors should know these three key things.

Firstly, XRX has made a strong commitment to returning a significant proportion of its excess capital to shareholders at the company’s Investor Day on February 23, 2022. Xerox emphasized at its 2022 Investor Day that it will ensure that “at least 50% of free cash flow” is “being returned to shareholders” going forward. More importantly, XRX stressed that “we plan to continue paying our $1 (annual) dividend (per share).”

Secondly, the $1 per share in annual dividend is reasonably safe. An annual dividend per share of $1 translates into dividends of approximately $155 million. As per S&P Capital IQ, the Wall Street analysts see XRX’s free cash flow contracting from $561 million in fiscal 2021 to $392 million in FY 2022. But Xerox’s $155 million in dividends only represent a reasonable 40% of its FY 2022 free cash flow. In other words, XRX’s dividend of $1 per share is very likely to be sustained this year, even though 2022 is a challenging year especially in relation to inflationary cost pressures. More significantly, Xerox offers an appealing dividend yield of 7% based on its current dividend and its last done share price of $14.19 as of July 12, 2022.

Thirdly, XRX is unlikely to increase its dividends (above the $1 per share payout) in the foreseeable future, as the company has other capital allocation priorities. Apart from returning excess capital via buybacks as well, Xerox mentioned at its 2022 Investor Day that it “will pursue value-accretive M&A” and “be targeting an investment grade rating over time.” In other words, Xerox will also be allocating a proportion of its capital to acquisitions and deleveraging. In addition, Xerox is currently trading at an inexpensive consensus forward next twelve months’ normalized P/E multiple of 8.3 times as per S&P Capital IQ. As such, it is natural that Xerox might choose to prioritize buybacks over dividends when deciding on the means of capital return.

In conclusion, Xerox is a safe high-yield dividend play, but it is not a good dividend growth stock.

How Often Does Xerox Stock Pay A Dividend?

For investors relying on dividends as a source of regular passive income, the frequency of dividend payments is as important as the absolute dividend yield.

In that respect, Xerox is similar to most other US-listed companies, as it pays out a $0.25 per share dividend every quarter.

Is Xerox A Good Long-Term Investment?

In analyzing any equity investment, one needs to consider the potential for both capital appreciation and shareholder capital returns.

In the case of Xerox, the stock boasts an attractive 7% dividend yield, but future dividend growth is unlikely. Also, there are long-term risks associated with XRX, which could potentially lead to permanent capital losses (structural share price decline) rather than capital appreciation for the company’s shareholders. As such, I don’t think Xerox is a good long-term investment.

Before the COVID-19 outbreak, a lot of companies have already undergone substantial digital transformation, resulting in a significant reduction in paper usage and print volumes. The pandemic has accelerated the process of digitalization for most corporates, and also drove certain companies to move towards a hybrid work model (also implying less paper usage and print demand). These headwinds have hurt Xerox’s core print business, and this is reflected in XRX’s numbers with the company suffering from top line contraction in every single year between FY 2012 and FY 2020.

This means that an investment in Xerox for the long term is a bet on the company’s successful transformation into a more diversified company. At its 2022 Investor Day, XRX highlighted that “new businesses will comprise as much as 25% of our revenue by 2024”, while noting that its core print business is still expected to account for around 90% of its top line in 2022.

M&A is one of the key revenue diversification drivers for Xerox, and the company’s recent deals include the acquisition of “a UK-based print and digital marketing and communication services provider” and a “Canada-based IT services provider” as per its July 2022 and February 2022 media releases, respectively. However, M&A is a relatively risky growth strategy (as compared to organic growth), and there is no guarantee that XRX won’t overpay and post-deal integration will be smooth.

Is XRX Stock A Buy, Sell, or Hold?

XRX stock is a Hold. After assessing factors such as dividend yield, dividend growth, P/E valuations, and the company’s long-term business risks, I have a Neutral view of Xerox which translates into a Hold investment rating.

Be the first to comment