Ian Tuttle

Roblox (NYSE:RBLX) plunged double-digits after releasing third quarter earnings. While the company finally delivered growth in bookings, free cash flow remained negative and growth disappointed expectations. RBLX had initially surged in mid-October after the company disclosed solid September growth, but October growth proved more modest. Even after the 75% decline since all time highs, I explain why the stock remains expensive here – both as compared to tech peers as well as in its own right. RBLX continues to remain a dangerous investment here.

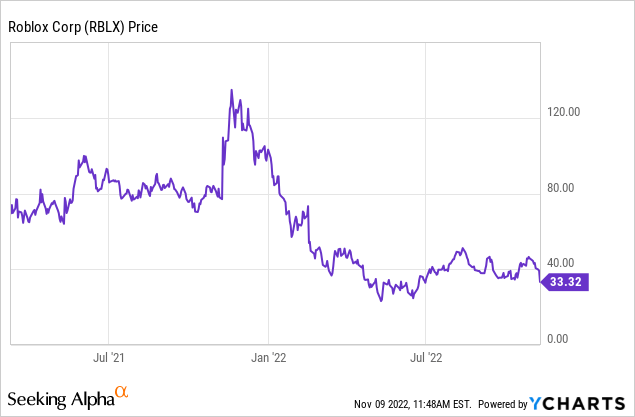

RBLX Stock Price

RBLX initially came public via much fan-fare, but the metaverse bubble has popped.

I last covered RBLX in August and the stock has declined 20% since. There, I recommended avoiding the stock due to the valuation being still elevated. The decline since then and improving fundamentals have helped somewhat, but the upside return potential is still not nearly enough to justify the significant risks.

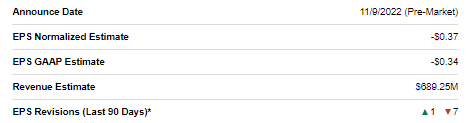

What Were Roblox’s Expected Earnings?

Wall street consensus estimates called for $689.25 million of bookings (note: it appears that analysts are using bookings in place of revenue) and for the company to lose $0.34 in GAAP earnings.

Seeking Alpha

Did Roblox Beat Earnings?

RBLX ended up beating slightly on bookings but lost $0.50 in GAAP earnings per share. I suspect that investors, however, were hoping for a larger beat on the top-line growth front.

RBLX Stock Key Metrics

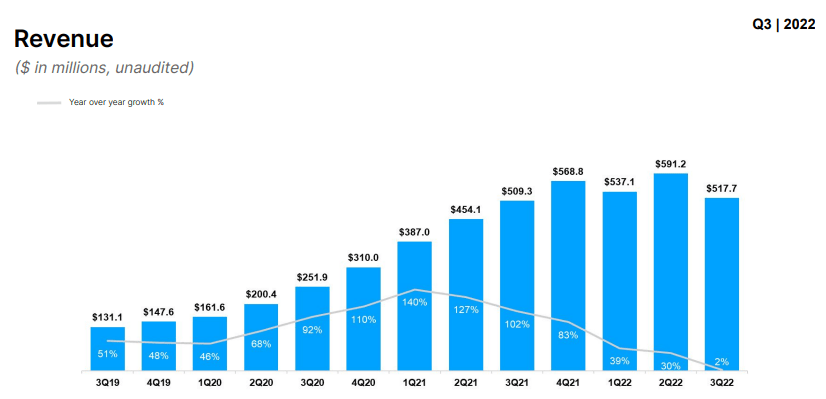

In the quarter, revenue growth plunged, as the 2% growth rate was lower than the 30% growth rate posted in the second quarter and far lower than the 102% growth rate posted in the prior year.

2022 Q3 Presentation

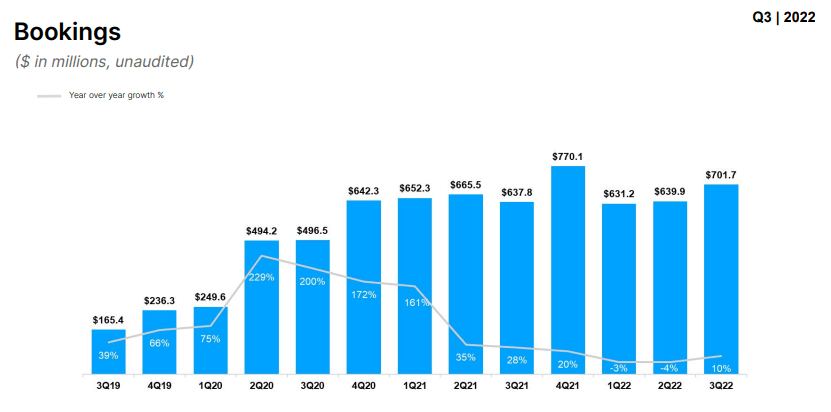

Bookings growth accelerated to 10% – still not nearly enough in the current market, but a sizable improvement from the declines posted in recent quarters.

2022 Q3 Presentation

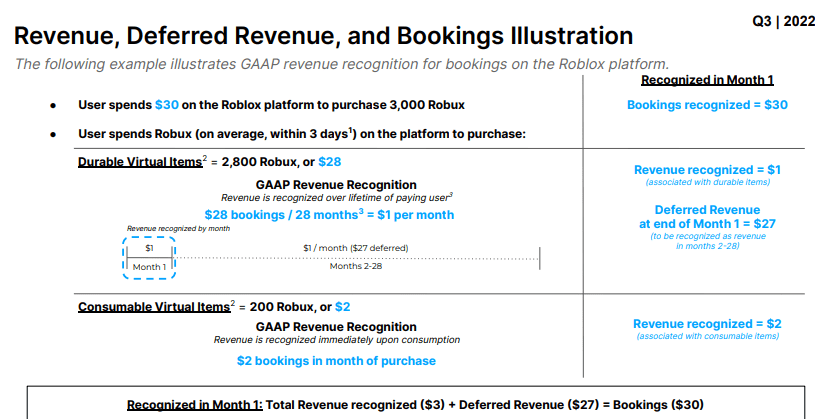

As a refresher, the difference between revenue and bookings is that bookings can be considered like pre-paid or deferred revenues that occur when users load money in the system, and revenue occurs when the user actually uses that currency in game play. Based on that definition, I question whether analysts should be using bookings in place of revenue, but at least over the long term the two metrics might trend in the same direction.

2022 Q3 Presentation

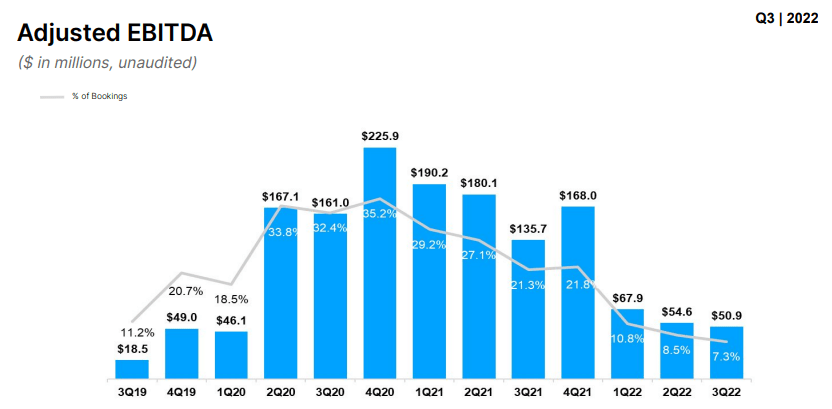

Adjusted EBITDA shrank to just 7.3% of bookings – this is no longer the same company that was generating 30+% adjusted EBITDA margins as it did during the pandemic.

2022 Q3 Presentation

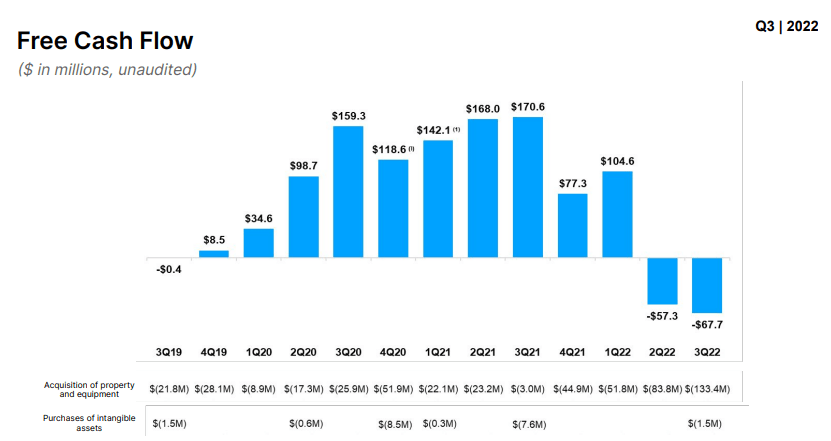

Because RBLX spent more on capital expenditures than what was recorded on depreciation & amortization, free cash flow ended up being negative in spite of the positive adjusted EBITDA.

2022 Q3 Presentation

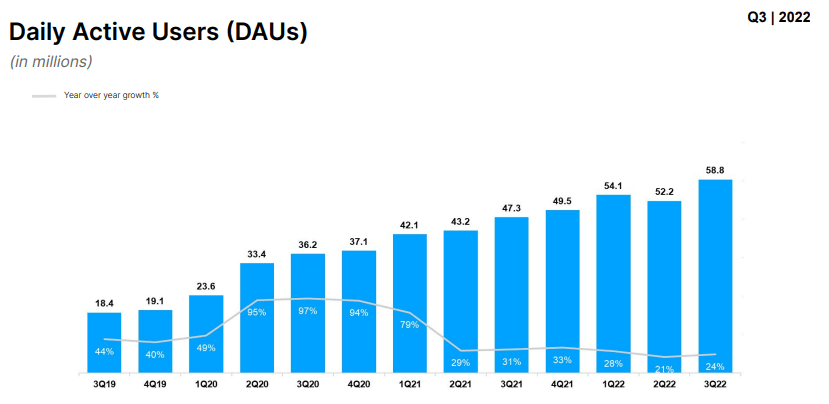

On a bright note, RBLX saw a return to sequential daily active users growth.

2022 Q3 Presentation

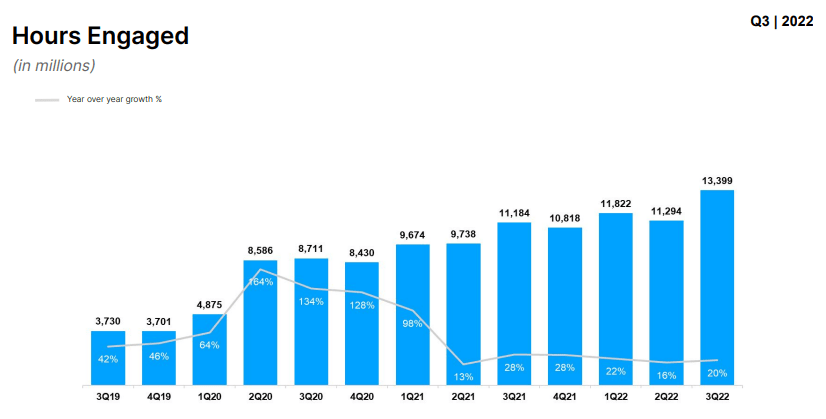

Hours engaged also increased sequentially after declining in the second quarter.

2022 Q3 Presentation

RBLX ended the quarter with $3 billion of cash but I note that the company also had $1 billion of long term debt and $2.8 billion of deferred revenue. The company’s cash burn profile is modest, so the cash position looks adequate to reduce liquidity risk, at least in the near term.

What To Expect After Earnings

Looking ahead, management appeared bullish for the fourth quarter, citing that they expect to reach new highs in DAUs, hours of engagement, and bookings, though they did not provide concrete numbers in the shareholder letter.

Looking beyond 2022, RBLX notes that it is seeing the fastest DAUs growth among users between the ages of 17-24 which is a positive observation considering that its primary user base had previously been those under 13 years of age. RBLX notes that its core US and Canadian markets are above peak-COVID levels yet are still growing “well.” RBLX sees its greatest growth opportunity as being in Western Europe and East Asia (which it calls its “Strategic markets”) due to having low rates of user penetration and better monetization than the “Opportunistic regions.” Investors may need to wait until the next quarter before receiving concrete guidance for 2023.

Is Roblox A Good Investment Long-Term?

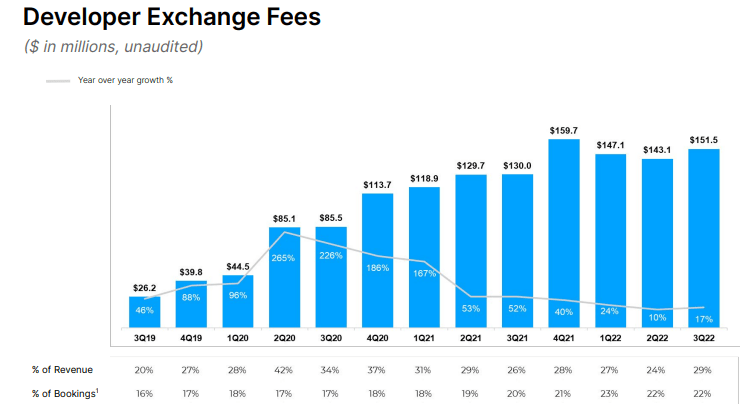

RBLX has long been touted as a play on the metaverse and for that reason it may always be considered a long-term investment opportunity. But investors may be over-estimating the projected profits that the company may produce in the long term due to two primary reasons. First, just like any other tech company, RBLX must pay for iOS and Android cost of revenues as well as employee headcount costs (like R&D). But besides those typical cost buckets, RBLX also must pay “developer exchange fees” to the developers of the games on the platform.

2022 Q3 Presentation

While there is always the possibility that RBLX can realize operating leverage in this bucket over time, I expect this to represent incremental costs as compared to other tech peers.

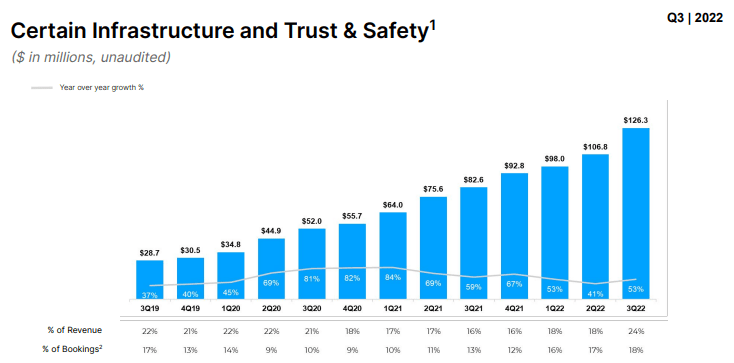

What’s more, due to RBLX catering largely to pre-adult users, RBLX will have to continually invest in “trust & safety” costs.

2022 Q3 Presentation

These realizations are important in determining a fair valuation for the stock as they may prove to be headwinds on long term margin expansion.

Is RBLX Stock A Buy, Sell, or Hold?

Consensus estimates have RBLX trading at 7x “revenues.” I noted earlier that analysts seem to be using bookings in place of revenues. Bookings currently materially exceed revenues and in my opinion revenues are a better measure of income generation – but we can continue to use bookings in the analysis below to prove my point.

Seeking Alpha

The investment thesis in the stock seems to have been based on a recovery in growth rates, at least for the past several quarters at least. Consensus estimates expect growth to return to the 17% range. Many other tech stocks like Okta (OKTA) or Twilio (TWLO) are trading at 2x-4x sales yet are expected to see revenues decline to that range or higher. That already is an indication that the current 7x revenue multiple at RBLX may be too high, but in the above section I discussed why long term margin assumptions will be lower. I typically project 30% long term net margins for tech companies, but for RBLX I project 17% long term net margins. Applying a 1.5x price to earnings growth ratio (‘PEG ratio’) and assuming a recovery to 17% growth, fair value might stand at around 4.3x sales – representing over 40% potential downside. Wix (WIX), another stock that investors are hoping will recover to the ~20% revenue growth range, is currently trading at around 3.5x sales. RBLX appears to be benefiting from “hype support” but arguably should be trading closer to the 3x-4x sales range. I continue to find RBLX highly dangerous here, as there is even a possibility that the stock does not participate in a broader tech rally due to the stock still trading richly. I rate the stock a “hold” not “sell” mainly due to the stock being a dangerous short, as there are enough reasons to not be surprised by periods of irrational exuberance. I have discussed with Best of Breed Growth Stocks subscribers that a diversified basket of beaten-down tech stocks may be the best way to take advantage of the tech crash, but being beaten-down is not enough – RBLX still trades richly in spite of the fall from all time highs.

Be the first to comment