Matveev_Aleksandr/iStock via Getty Images

Snapshot- What’s To Like About NNDM?

The influx of 3-D printing has picked up in recent years, and Nano Dimension Ltd. (NASDAQ:NNDM) is likely to be a key beneficiary of this momentum, particularly in the landscape of 3-D electronics manufacturing. This company has been developing ample clout in the additive manufacturing space since 2014, an industry that is incidentally poised to grow at an impressive CAGR of ~30% through 2027!

Electrical engineers who design circuit boards would tell you how transformational Nano Dimension’s tech could be, both across the testing process and the associated productivity gains. Rather than spending weeks outsourcing things to third-party board manufacturers, engineers can immediately leverage NNDM’s IP, and translate their ideas into reality, in just a day’s time. When you can test things in-house quickly, you get the scale effects that help bring down costs.

One also needs to highlight how useful NNDM’s in-house prototyping tech could be for industries that work in a clandestine manner such as the defense sector, where you can’t have too many 3rd party middlemen involved in the manufacturing chain. Little wonder that Nano’s recent press releases have been dominated by wins in the defense space. As things stand, the company currently has 9 defense companies that make up its client base, including the national army, intelligence, and security institutions.

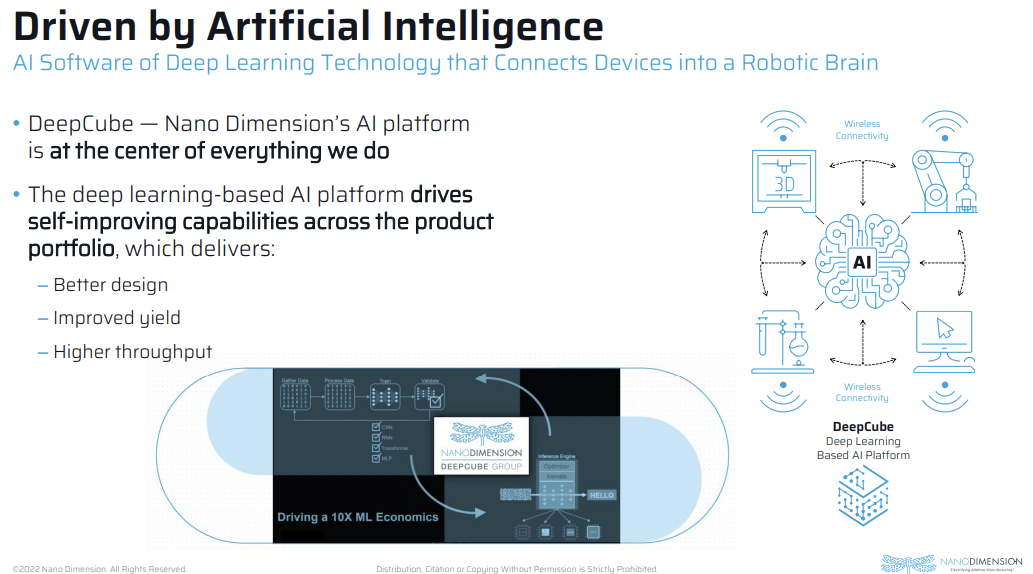

The other exciting opportunity involves leveraging the AI technology of DeepCube (a company that was acquired by NNDM in April 2021) to augment NNDM’s positioning in an industrial market that is becoming more digitized by the day. DeepCube’s tech is quite elite as its AI and deep learning solutions can potentially enhance memory reduction, dampen printing errors, and increase speed by 10x in real-time, giving you a supreme and unique class of edge devices that are not easy to find.

Investor Presentation Nov 2021

What Do The Valuations Look Like?

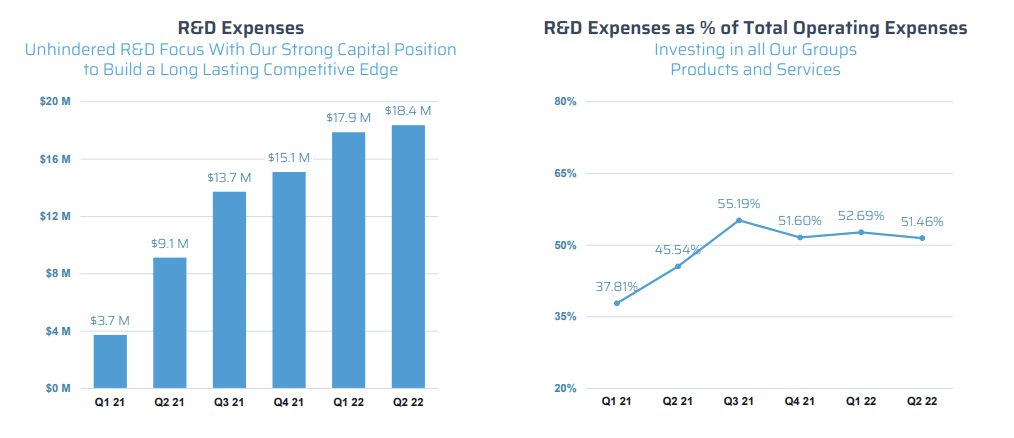

NNDM is not covered by the sell-side community so there are no forward estimates to augment the valuation picture. Also note that this is a company whose cost base is heavily inundated with R&D-related expenses (well over half the cost base) which have doubled from what it was a year ago.

Investor Presentation Nov 2022

The high R&D component shows how early the company still is in its lifecycle and puts it in a very difficult position to generate profits in the foreseeable future. In fact, investors need to consider that profit generation is probably something that will not happen until 2025 at the very least!

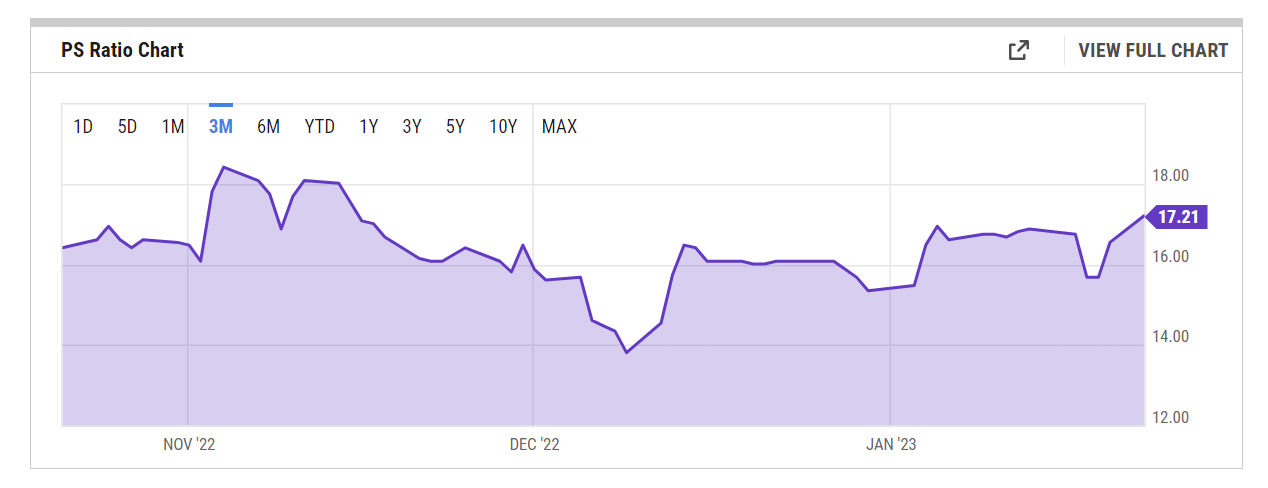

On a TTM basis, Nano Dimension has generated a little less than $40m of sales, and at the current market cap that would translate to ~17x of sales which would no doubt appear pricey to a fair few, particularly as the sector median P/S multiple is less than 3x.

YCharts

However, if one looks at the top-line growth you’re getting across recent periods (10x growth between 2020-2022, and 964% on a YTD basis, as of 9M-22), you may be tempted to alter your view. Those of you who attach importance to sequential developments may be concerned by NNDM’s slowdown in its Q3 revenue ($9.9m vs $11.1m) after 4 straight periods of q-o-q improvements. However, do consider that this is not lost revenue one is looking at, but rather delayed revenue on account of supply chain delays and the Russian-Ukraine conflict. If anything, one should consider looking at the order backlog which recently hit record highs of $9m, and which should provide a decent foundation for FY23 revenue growth.

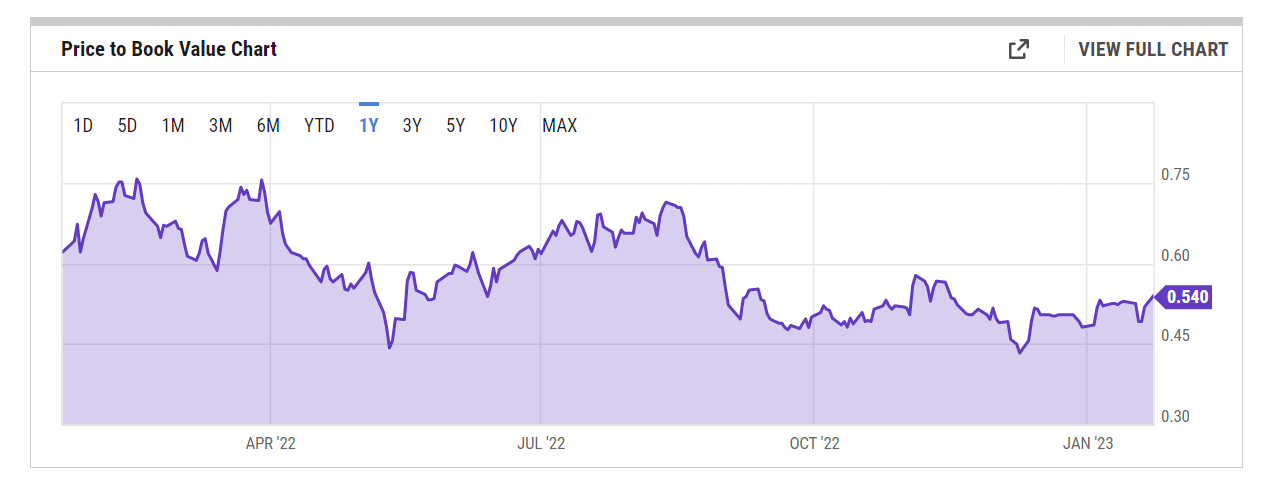

Crucially, it’s also worth pointing out that the company still has a substantial arsenal of cash and unrestricted bank deposits of over $1020m on its books (these items used to account for 94% of the total asset base as of March 2021, now it stands at 80%). Thus, with $23m of operating cash spend per quarter, you’re looking at an annual operating cash outflow of less than $90m per annum; NNDM’s cash and investment balance would cover that by over 11x! The cash balance would also comfortably support the company’s M&A ambitions at a time when valuation multiples have come down. All in all, not only do you have a stock trading well below a book value that is quality on paper, but the current P/BV multiple is a good 70% cheaper than the historical average!

YCharts

Combine Nano’s growing IP credentials and its comforting cash position, and you get a rather ripe acquisition candidate for larger players in this industry.

What Do The Technicals Say?

At a little less than $2.6 a share, I can see the inclination to take a punt on a stock whose fortunes are closely tied to the growing adoption of Additively Manufactured Electronic (‘AME’) technology (~77% of NNDM’s total R&D spend is towards AME initiatives). However, based purely on the intermediate technical picture, I’m not convinced it’s the best juncture to make an entry in the stock even though momentum traders may have a different take on things, considering that the stock is up by almost 10% in 3 days, after recently witnessing a double bottom hammer impression, at the sub $2.275 levels.

Investing

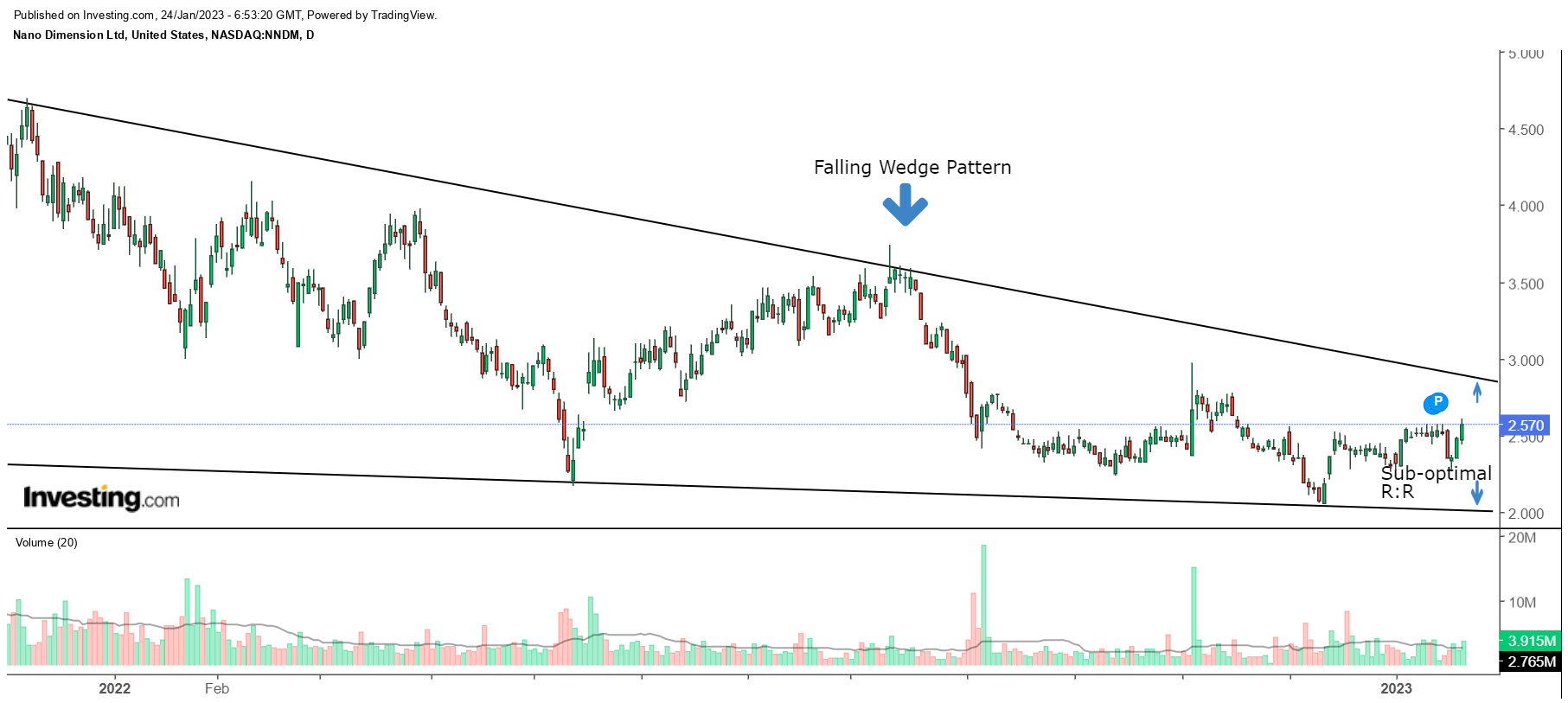

Nonetheless, if you look at the price imprints since late 2021, we can see that the stock has been forming a falling wedge pattern, with the lower boundary at around the $2 levels, and the upper boundary close to the $2.85 levels. The stock is currently closer to the upper boundary, implying sub-optimal reward:risk, of less than 0.5x.

Stockcharts

NNDM is also likely to come up as a prospective candidate for those fishing for promising opportunities in the innovative Israeli terrain. Admittedly, whilst the relative strength ratio of NNDM and the iShares MSCI Israel ETF (NNDM has a 0.35% weight in this product) is a long way from the mid-point of its range, do also consider that this ratio has just recently hit the upper boundary of the descending triangle, which is probably not the most ideal point for those rotating into NNDM.

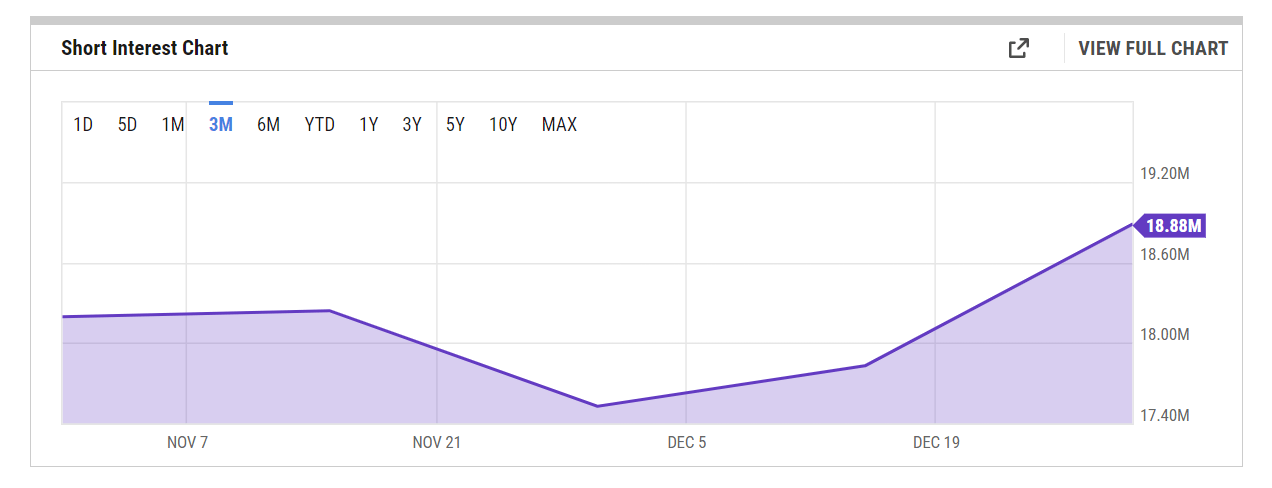

Investors should also be a little concerned by the fact that short-sellers who were previously exiting their positions in NNDM have turned a little more enthusiastic as of late. Data from YCharts shows that the number of shares that have been sold short has grown by ~8% over the last two reporting periods.

YCharts

All things considered, while I can get behind the Nano Dimension story, I would prefer to wait for a more suitable entry point to own the stock. NNDM is a HOLD.

Be the first to comment