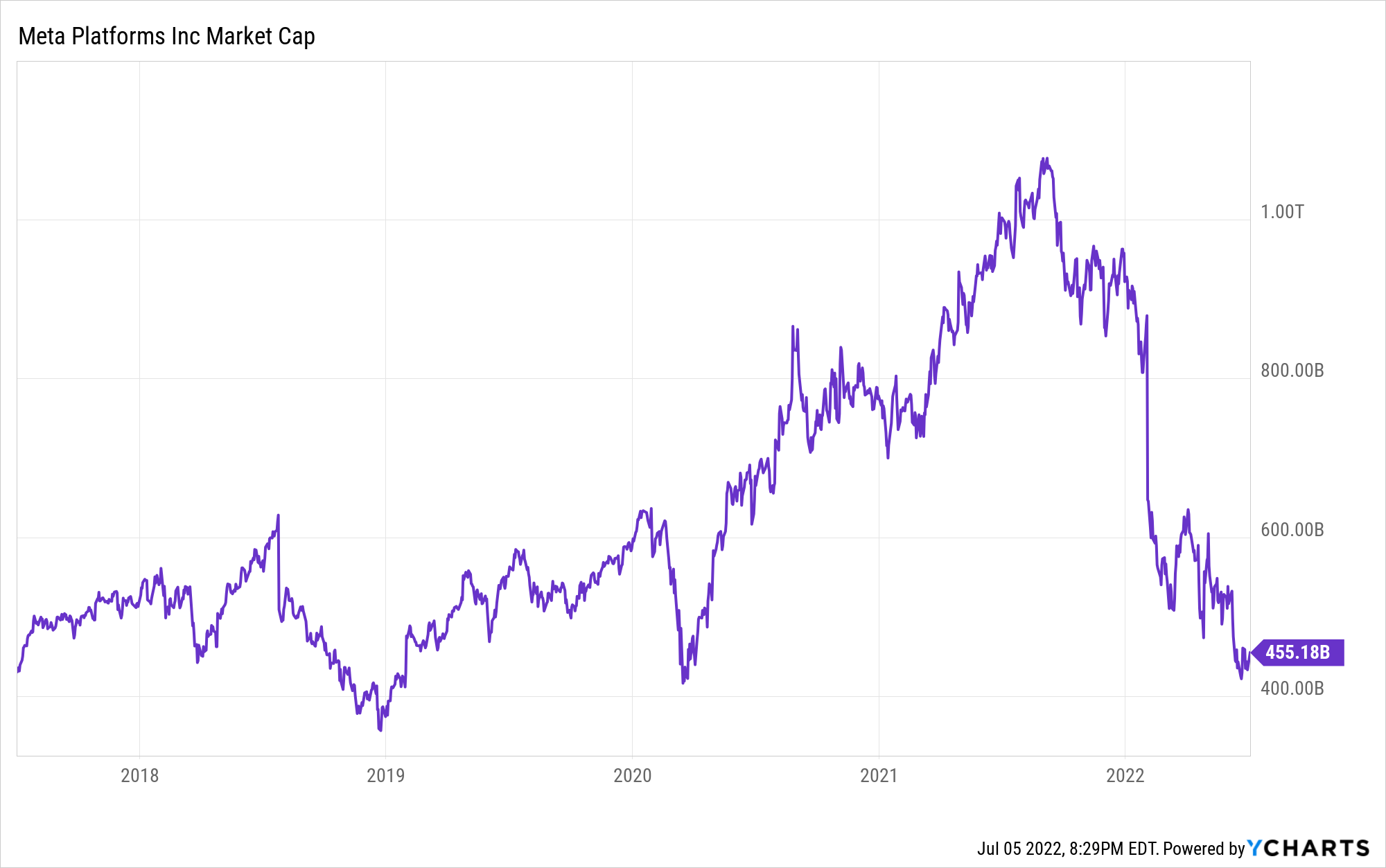

Being a Meta Platforms Inc (NASDAQ:META) investor has been a very, very painful experience over the last nine months. In this period, META’s valuation has dropped by ~$620B (or 57.4%). While long-term Meta investors are no strangers to large drawdowns, the sheer velocity and depth of this move is adequate to shake out most bulls from this counter.

YCharts

In today’s note, we will try to understand some of the factors driving the collapse of Meta’s stock and evaluate its ability to recover. Next, we will run META through TQI’s Quantamental Analysis methodology to determine if it is a good buy as a near-term, medium-term, and/or long-term investment. Lastly, I will share my fair value estimate and projected CAGR return for Meta.

But before we do all of that, I think we should discuss the idea of buying a stock amidst a crash or dip like what META is undergoing right now.

Is It A Good Idea To Buy Stocks During A Dip?

A very popular trading/investing adage goes something like this –

Don’t try to catch a falling knife

In equity investing, a rapidly-declining stock is analogous to a falling knife, and an investor trying to catch [buy] it is likely to get hurt. Now, if you are a short-term trader, then being a contrarian (i.e., going against the herd) may not be a wise move. However, if you are a long-term investor, then you are better off buying stocks with broken technical charts (if the fundamental story, business model, and investment thesis are not broken). Having time on your side is an advantage over most market participants that operate with shorter time horizons on their investing mandates.

Back in April 2022, I showcased in one of my articles – how bad technicals can be a boon for long-term investors, and in that research note, I used Meta Platforms as an example.

Here’s what I said at the time:

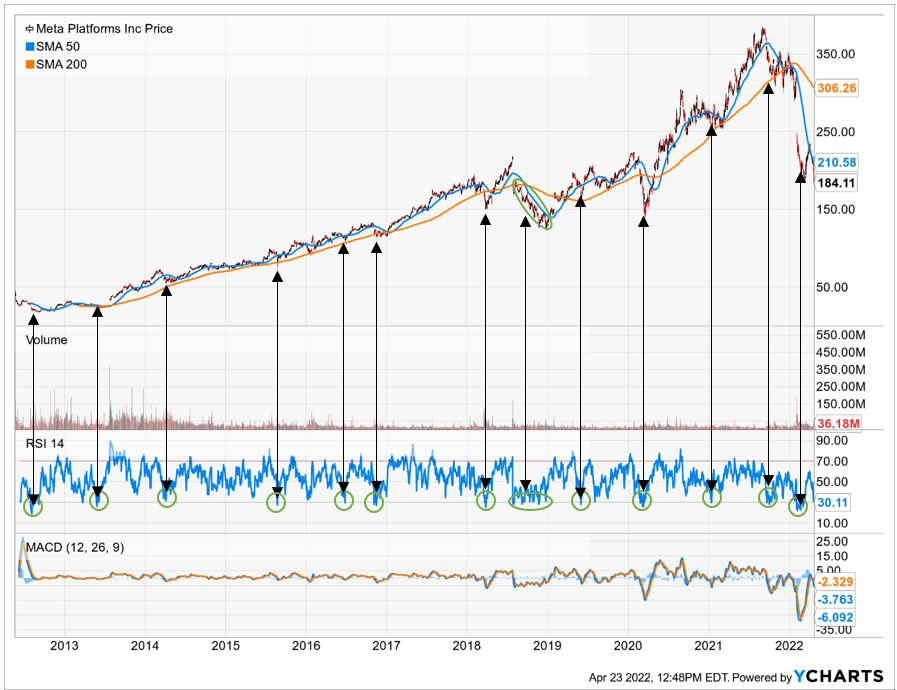

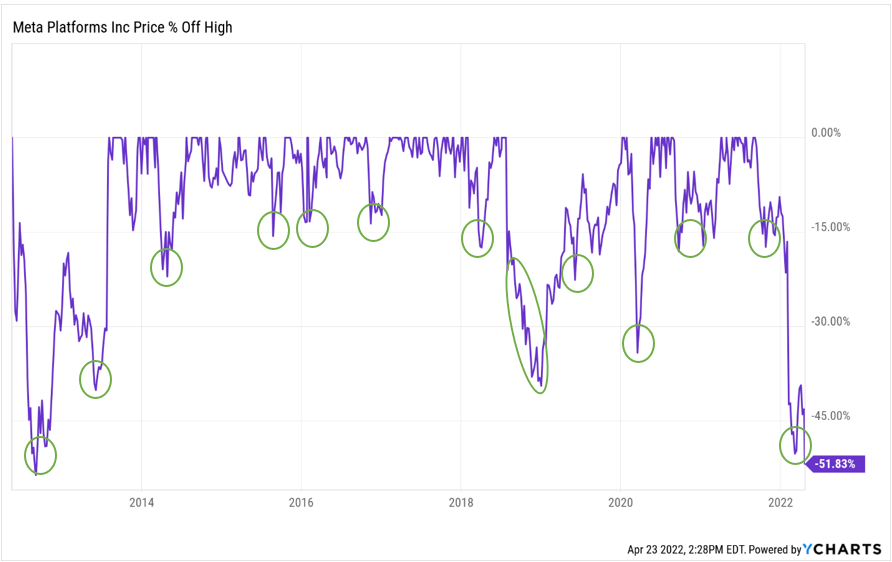

Well, if you are a short-term-oriented trader, don’t bother buying Meta here. However, if you are a long-term-oriented investor, Meta offers a spectacular entry point. In its ten-year history as a public company, Meta’s stock has pulled back by more than 15% from its highs on 12 separate occasions, with its 14-day RSI also hitting 30 (oversold territory), and every dip has proven to be a rewarding buy for investors.

YCharts, Author

YCharts, Author

Meta’s stock chart is filled with sharp drops and V-shaped rallies, and while Meta looks down in the dumps at this moment in time, it could stage a sharp reversal in the coming months and quarters as temporary headwinds subside, and price recalibrates to business fundamentals.

So far, my Meta buy from April is down ~8% (SPX is down ~9% in the same period). However, I took this position as a long-term investment with a 5+ year horizon, and being down ~8% is fine for me. I wouldn’t be fine being down so much if I were a short-term trader.

In investing, taking a contrarian (non-consensus) bet can lead to outsized gains, but this can happen if and only if you are right.

iq25

Legendary investor – Howard Marks – put this idea really well –

To achieve superior investment results, your insight into value has to be superior. Thus you must learn things others don’t, see things differently or do a better job of analyzing them – ideally all three.

History shows that buying stocks during dips is a rewarding exercise. However, in order to buy stocks during a dip, investors need to cultivate the right investment philosophy, be courageous, and have the stomach for near-term volatility. Nowadays, this phrase – “Buy and HODL (hold on for dear life)” – is pretty popular. The buy part is easy; HODLing (holding) is not [especially during vicious downdrafts]. We started with this question – “Is it a good idea to buy stocks during a dip?” – and my answer is that, if you are a long-term investor who’s done adequate due diligence on a business, then yes, catching a falling knife is not an issue, i.e., buying stocks during a dip is a fine idea (as long as you are confident about being right).

Here’s how I structure my due diligence on a stock that’s experiencing a dip:

Identify the factors or issues driving the downdraft.

Analyze long-term business fundamentals and valuations to make sure the investment thesis is intact.

Utilize quantitative and technical data analysis to limit near-term pain.

Now, some of you might say that why not wait for the bottom to buy. The idea of a bottom is fictitious, and nobody knows where the bottom is at any given point in time. A true bottom only becomes clear in hindsight. Hence, there is no point in trying to buy at the bottom; you are likely to miss it. I will discuss this idea in detail some other time.

If you are interested in studying my investment thesis for Meta in more detail, please feel free to read these research notes:

For now, let’s begin our due diligence exercise on META.

Why Did Meta Stock Dip?

As you may know, Meta’s business is facing several headwinds, including, but not limited to –

IDFA changes (from Apple (AAPL)) adversely affecting Facebook’s targeting capabilities (lower ROI for advertisers)

Increased competition from rivals such as TikTok (ByteDance), Alphabet (GOOG), Amazon (AMZN), and Snapchat (SNAP)

Lower Ad demand on the back of weak macro environment: multi-decade high inflation, rising interest rates, exploding commodity prices, and growing fears of recession (slowing economy).

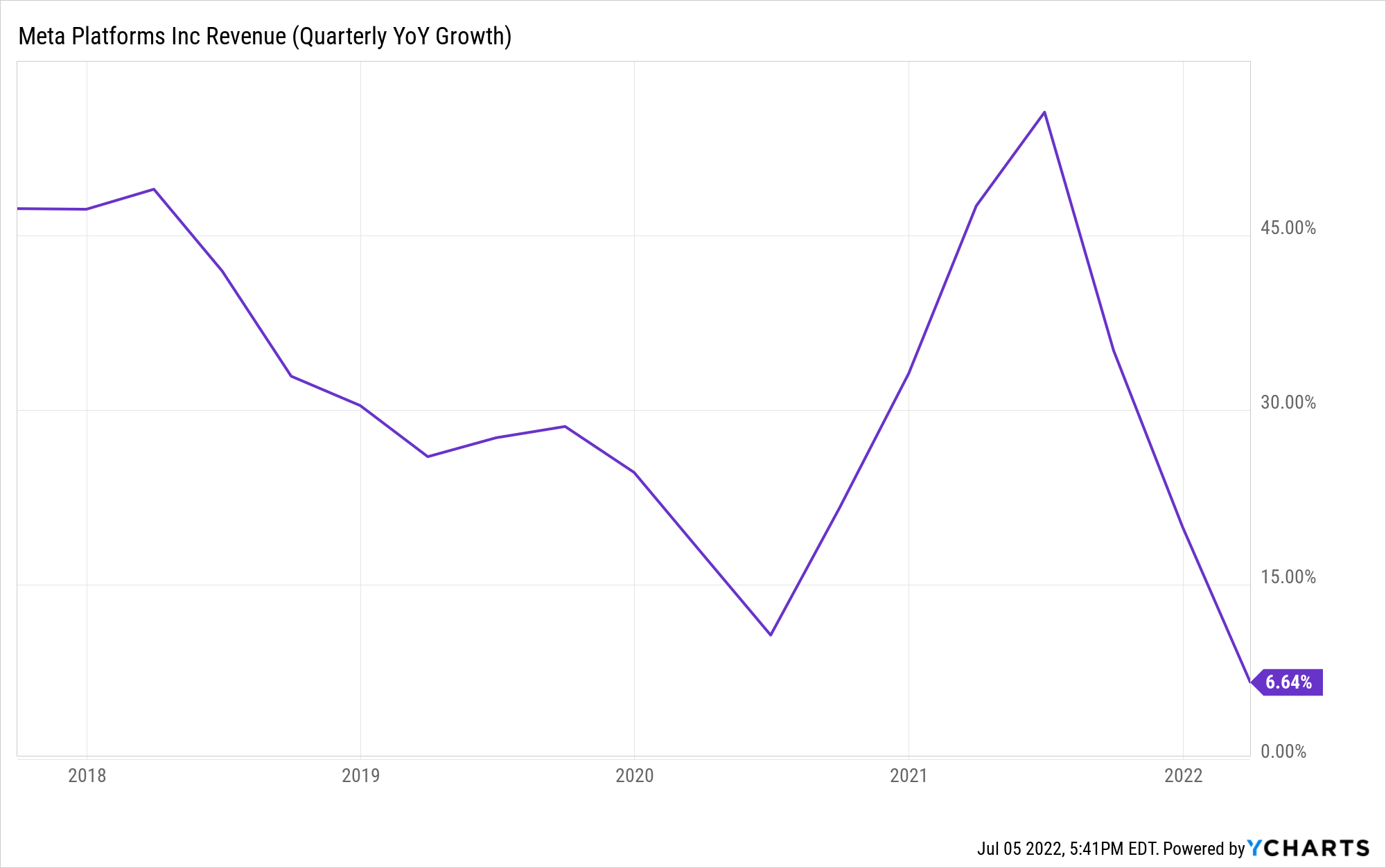

While these factors (and probably some others) are the likely fundamental drivers behind Meta’s bearish price action, I think the re-pricing in Meta’s stock boils down to the rapid deceleration in its sales growth rates in the post-pandemic era. Within a few quarters, Meta’s growth rate has fallen off a cliff from ~48% to ~6.6%. For 2022, Meta is expected to grow at just 6%, and if the economy worsens, we may see no growth at all.

YCharts

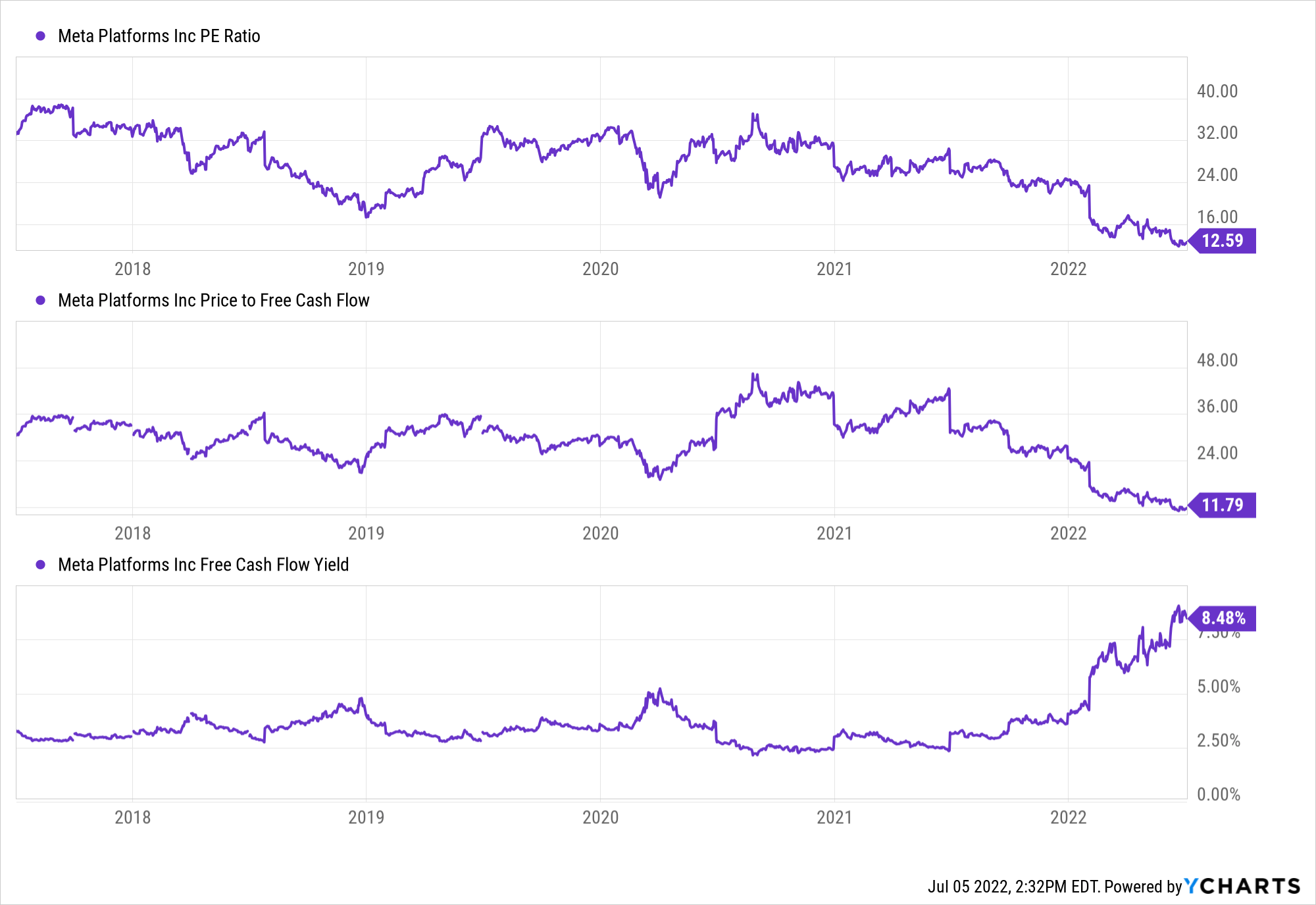

As growth grinds to a halt, Mr. Market is re-rating Meta as a value stock, which it is (based on its new financial reality). However, I firmly believe that the market has overshot to the downside (trading Meta down to 12x P/FCF), and there’s not an iota of doubt in my mind that Meta’s ~8.5% FCF yield is a rare buying opportunity, but more on that later.

YCharts

Let’s discuss some of Meta’s headwinds and the nature of these issues. If these issues are permanent, Meta may be a value trap. However, if these issues are just temporary setbacks, then Meta could be a killer investment at current levels.

1. Apple iOS policy changes

The impact of Apple’s IDFA changes is pretty well documented at this point. We even saw these changes negatively affecting Meta’s revenue last quarter. In simple terms, Apple’s iOS policy changes around IDFA (ID For Advertisers) have resulted in reduced ROI for Meta’s advertisers (due to severely limited targeted ad capabilities amid lesser data available to Meta). According to Meta’s management, the company could need multiple quarters before its AI could work (produce similar ROI for advertisers) without this key identifier.

2. TikTok and other competition

The astronomical rise of short-form video, led by TikTok, has hurt Facebook’s engagement metrics. Despite robust growth in the short-form video category via Reels, Meta is still chasing TikTok. Furthermore, Meta is facing competition from the likes of Amazon and Apple. With heightened competition, Facebook’s revenues and margins could come under pressure. Luckily, digital advertising remains a secular growth trend, meaning Meta could continue to grow revenue while losing market share.

3. Economy is turning bad

A slowing economy is driving advertising budget cuts, and Meta is facing the heat. We have seen heightened turnover at the C-suite level, and Meta’s CEO, Mark Zuckerberg, recently provided a very bleak outlook for the economy to employees:

If I had to bet, I’d say that this might be one of the worst downturns that we’ve seen in recent history.

Source: Mark Zuckerberg, reported by Reuters.

He further warned employees –

The company needed to crack down and work harder than it had before, and that I am “turning up the heat” on internal goals and metrics used to rate employees’ performance. I think some of you might decide that this place isn’t for you, and that self-selection is OK with me. Realistically, there are probably a bunch of people at the company who shouldn’t be here.

These sharply worded comments reflect the degree of difficulty that Meta is facing with its business. Considering all these negatives together, I guess Meta’s downdraft is not all that surprising as it is the perfect storm for the social media/advertising giant.

Can META Stock Recover?

In my view, all the major headwinds discussed in the previous section are solvable issues. Apple’s IDFA changes are hurting everyone, and not just Meta; however, with Meta’s scale and engineering talent, it is probably the likeliest “non-gatekeeper” tech company to find a workaround. According to Meta’s management, the company is already building AI/ML-based solutions to provide better ROI for advertisers in the post-IDFA (and cookie-less world). Mark Zuckerberg believes that it could be a few quarters before Meta gets around Apple’s IDFA changes; however, he expects Meta to emerge stronger on the other side.

While Meta can’t really do much about Amazon and Apple taking market share in the digital advertising share, it can certainly stop TikTok in its tracks. According to a recent report from Truist, Meta’s Reels are set to overtake TikTok in the short-video space within 18 months. A few years back, Meta had to grapple with Snapchat’s (SNAP) Stories, and we know the outcome. Throughout its history, Meta has shown incredible agility in business, and I am pretty confident that Zuckerberg and Co. will come out with flying colors this time too.

And if Meta can’t beat TikTok to the punch, US regulators could surely get it done. Brendan Carr, an FCC commissioner, recently asked Apple and Google to ban TikTok from their app stores for its “pattern of surreptitious data practices”:

TikTok is owned by Beijing-based ByteDance – an organization that is beholden to the Communist Party of China and required by Chinese Law to comply with PRC’s surveillance demands.

TikTok’s pattern of conduct and misrepresentations regarding the unfettered access that persons in Beijing have to sensitive U.S. user data violated Apple’s and Google’s standards.

TikTok collects everything from search histories to “keystroke patterns and biometric identifiers, including faceprints, and voiceprints,” as well as collecting location data, text, images and videos stored on the device’s clipboard.

TikTok is not what it appears to be on the surface. It is not just an app for sharing funny videos or memes. That’s the sheep’s clothing. At its core, TikTok functions as a sophisticated surveillance tool that harvests extensive amounts of personal and sensitive data.”

While Apple and Google have not responded yet, I think TikTok will get banned in the US (sooner or later). My thinking is simple; if Meta is not allowed to operate in China, there is absolutely no reason why TikTok should be allowed in the US. I know we pride ourselves on free markets, but protecting the data privacy of our people from the CCP is more important as this relates to national security.

The last headwind, i.e., stagflation in the economy, is out of Meta’s control. However, if I were asked to make a bet on the economy, I would always bet on the economic cycle to turn again (it always does). Due to decades of insane monetary and fiscal policies, we find ourselves in the midst of a vicious debt cycle that has rendered economic “booms and busts” a recurring theme. With our national debt at $30T, I am confident that this trend will continue for years and years to come.

In a nutshell, I can see some of Meta’s major business headwinds waning in the next 12-24 months, and Meta could emerge as a stronger company on the other side of these tumultuous times. Now, let’s do some number crunching.

Running META Through TQI’s Quantamental Analysis Methodology

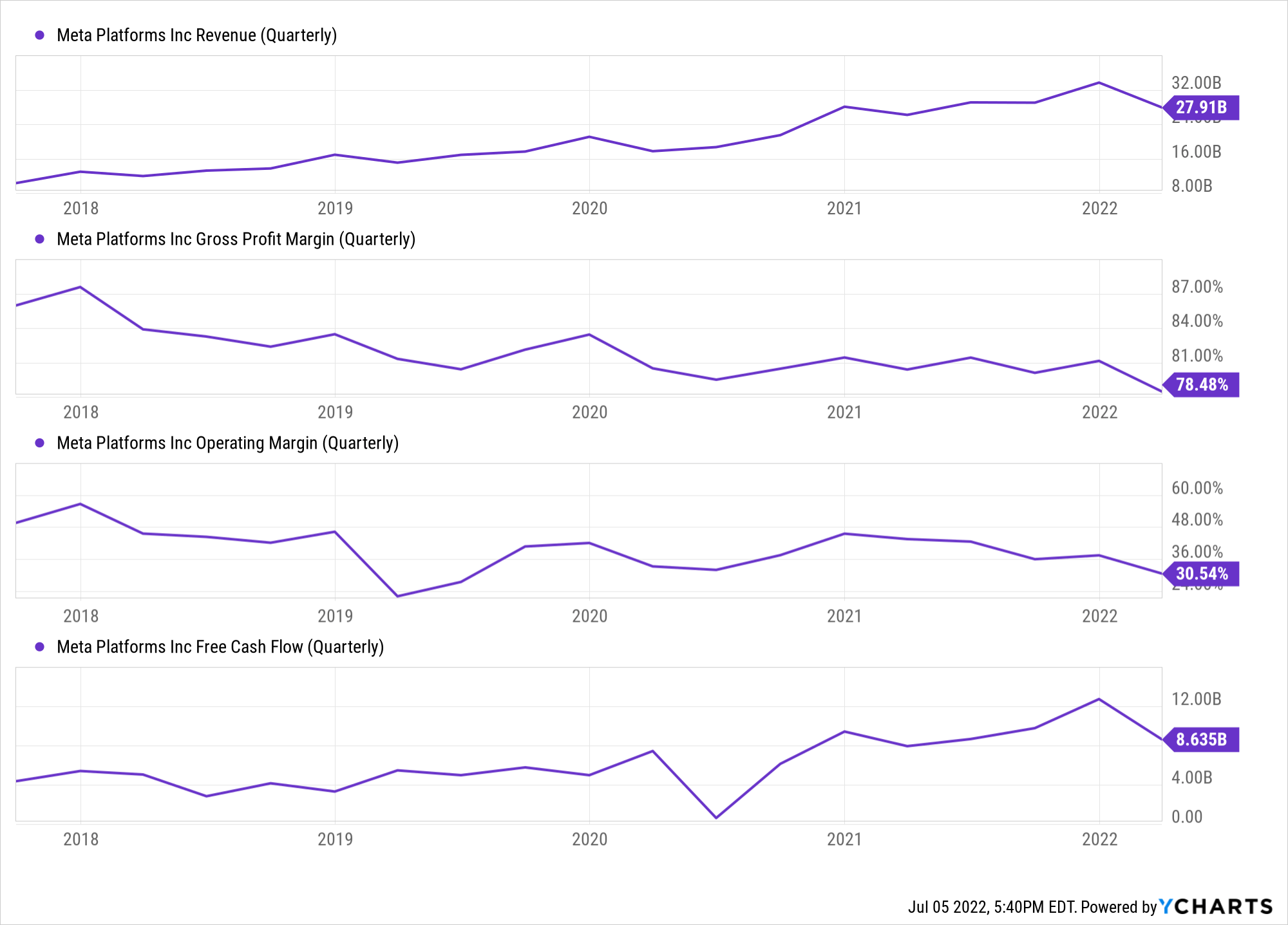

In the grand scheme of things, Meta’s revenues are still growing; however, margins seem to be coming under significant pressure as the company makes massive investments into building the infrastructure for the Metaverse. Despite moderation in margin profile, Meta still commands robust gross and operating margins of 78.5% and 30.5%, respectively.

YCharts

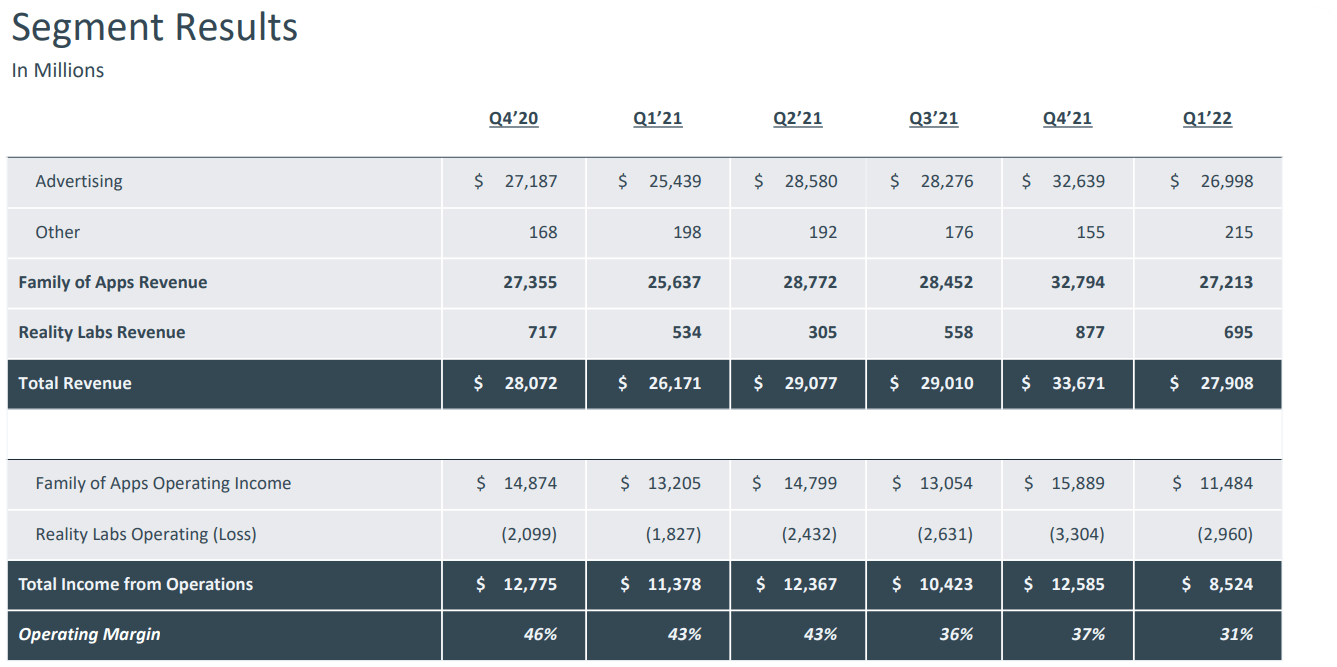

While Meta is investing (losing) ~$10B per year in Reality Labs, it continues to make tons of profits from its advertising business. In Q1, Meta generated $8.6B in free cash flow (30% FCF margin). However, the easily observable downward trend in operating margin is concerning. I understand that Meta is growing slower than management’s expectations, which is causing significant pressure on margins.

Meta Q1 2022 Earnings Presentation

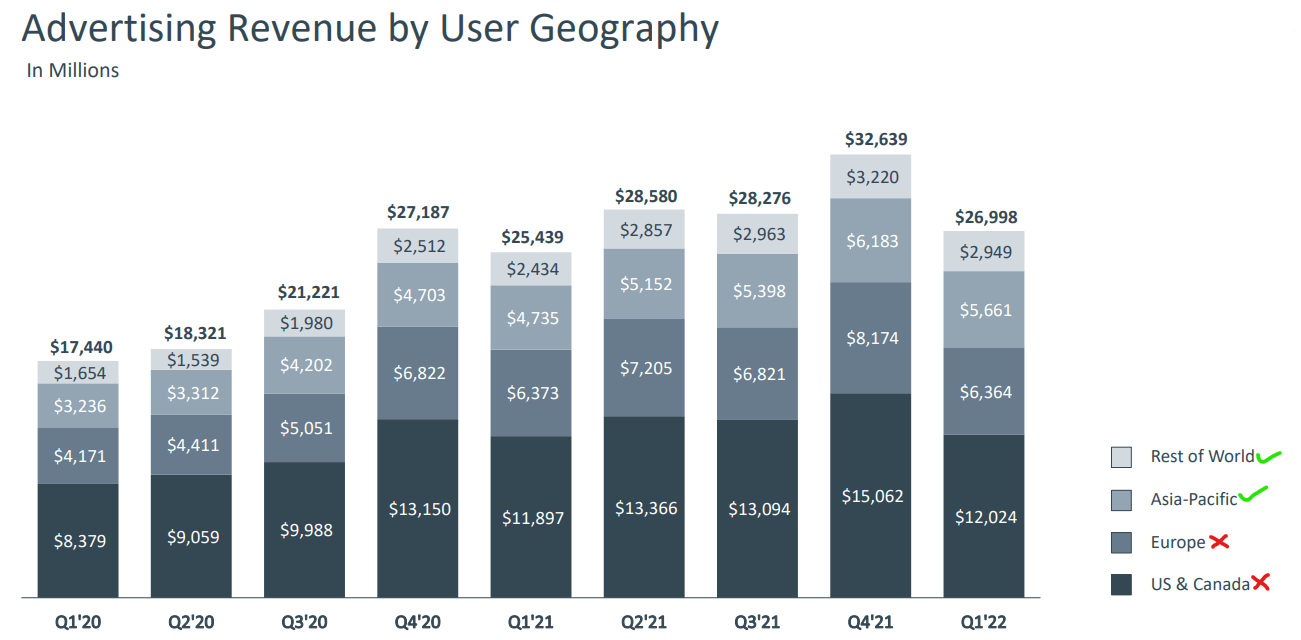

Meta’s growth rates have been falling off a cliff in the post-pandemic world, with particular weakness in Europe and US & Canada – regions where growth is nearly zero right now.

Meta Q1 2022 Earnings Presentation

While Meta is struggling for revenue growth, these struggles are directly related to user growth. In Q1, Meta surprised most people (including me) by reporting a gain in DAUs. While more users are great for Meta as the entire company is built on network effects, I think Meta’s Family-of-apps are deeply integrated into humanity. Hence, Meta is not going anywhere anytime soon. For Q2, we can safely expect Meta to lose DAUs as the Russia ban takes effect. However, Meta could probably amass ~4-5B users on its platforms over the next couple of decades (we are still at ~3B).

Meta Q1 2022 Earnings Presentation

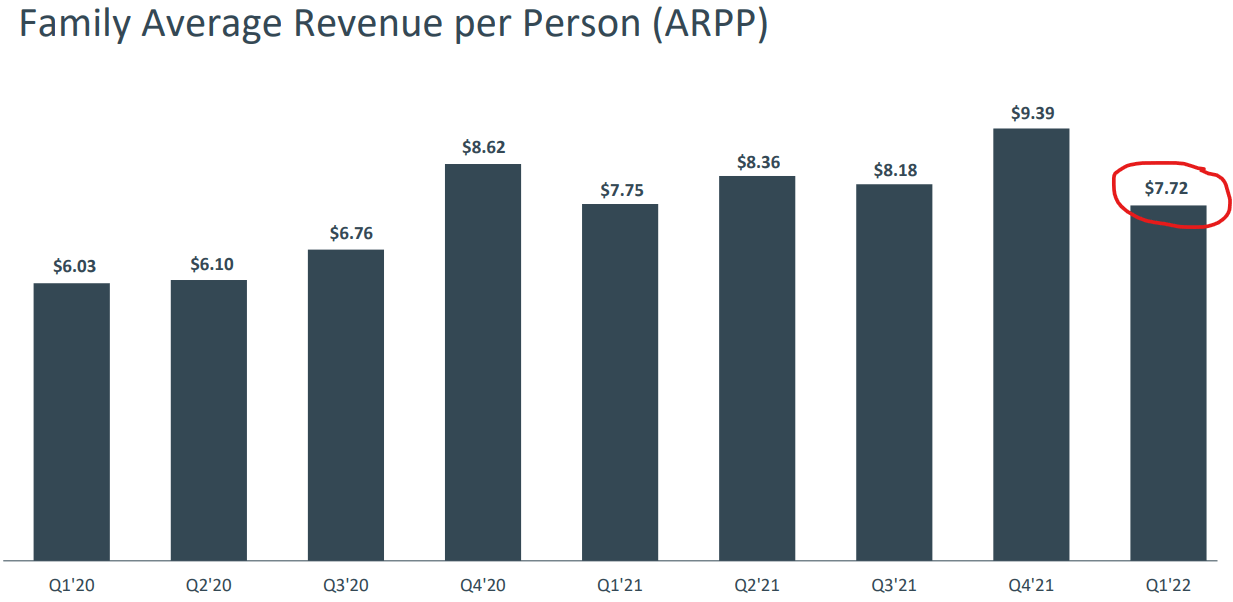

Interestingly, Meta’s ARPP declined slightly in Q1 (from $7.75 to $7.72). This anomalous development at the company could be a direct result of greater competition and an increased number of under-monetized active users on Meta’s platform (the former is more likely).

Meta Q1 2022 Earnings Presentation

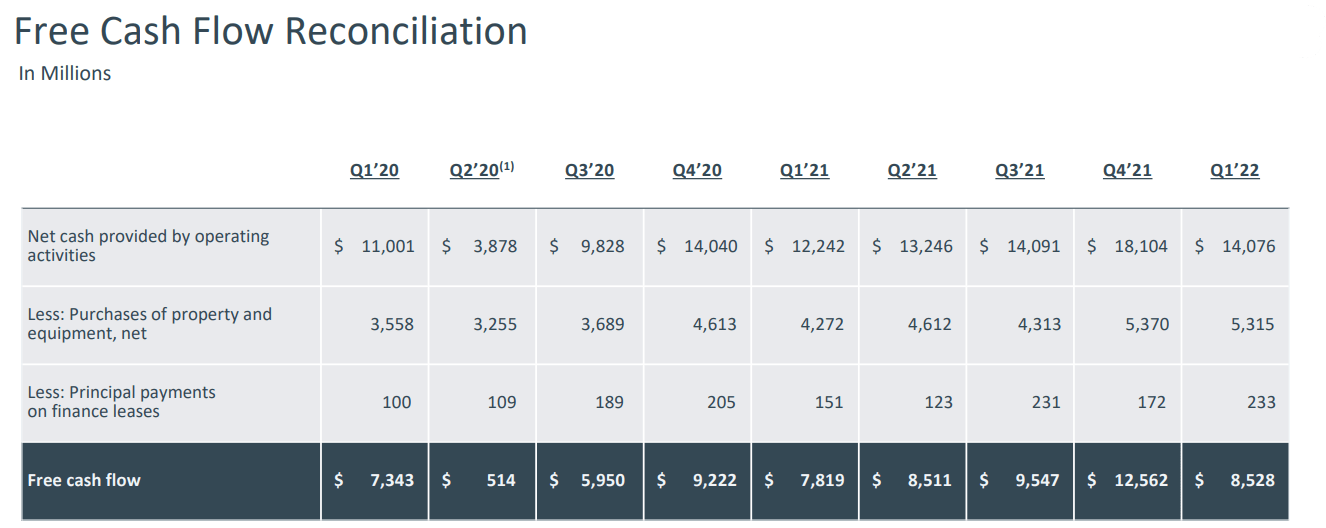

While several business headwinds are impacting Meta negatively at this given point in time, the company has still managed to produce massive amounts of free cash flow. As monetization from Reels and WhatsApp improves, I expect Meta’s FCF (and FCF margin) to rise over the coming years. Despite reporting a ~$2.9B operating loss in the Reality Labs business segment (Metaverse) for Q1 2022, Meta still made $8.5B in free cash flow.

Meta Q1 2022 Earnings Presentation

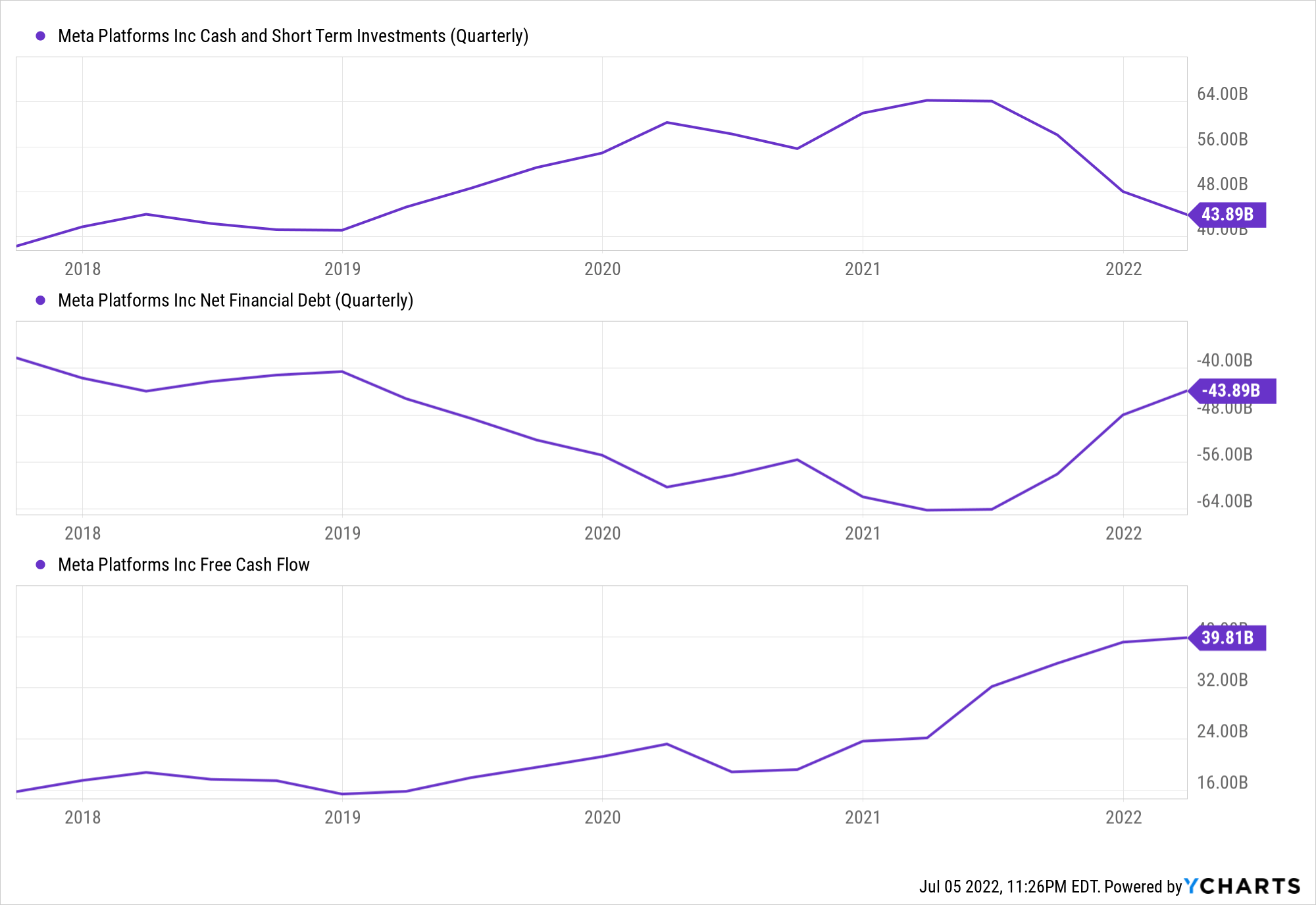

A solid balance sheet can do no harm to a business, and Meta’s balance sheet is as rock-solid as they come. With ~$44B of cash & short-term investments on its balance sheet (along with an additional $104B of long-term assets) and no financial debt, Meta is in a very strong financial position.

YCharts

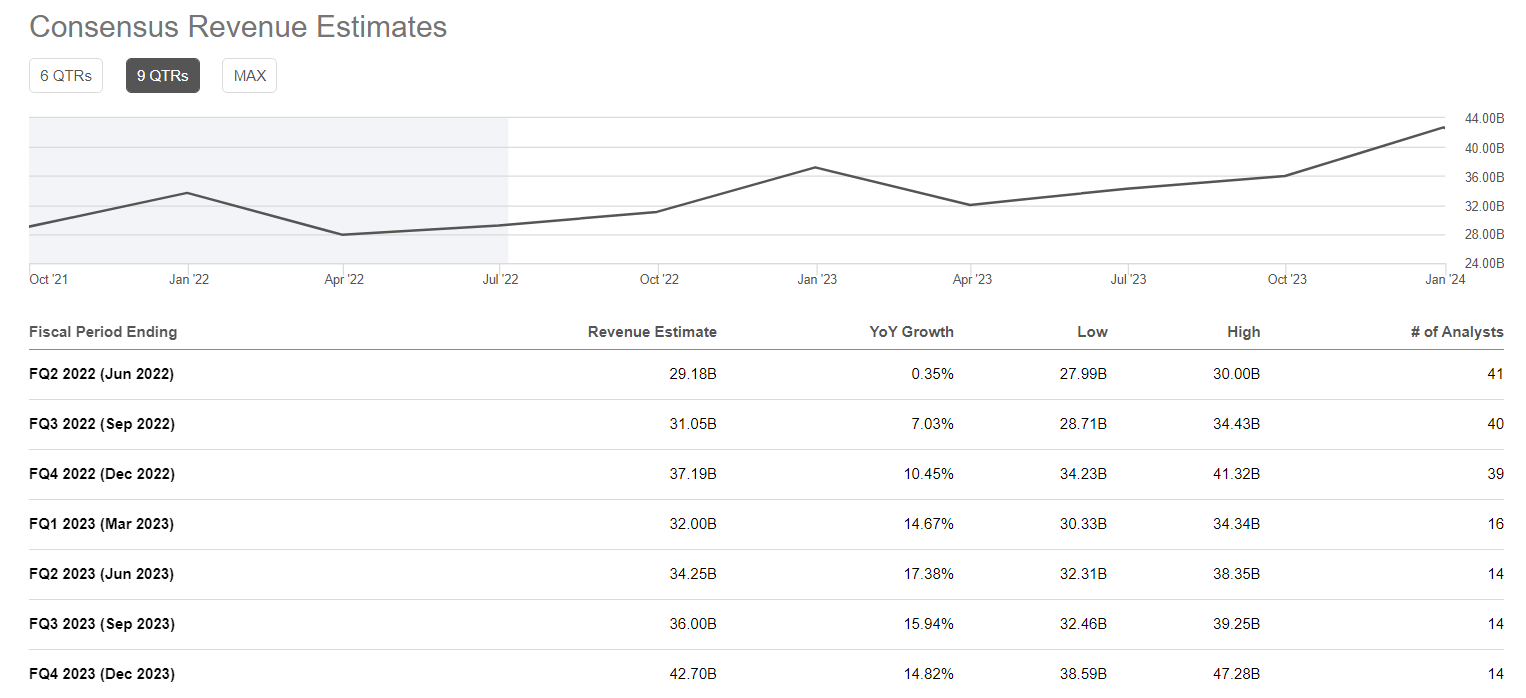

Despite facing several headwinds, Meta is still expected to grow revenues in 2022, albeit at an excruciatingly slow pace of 6%. Meta’s management has been providing a weak outlook for the last two quarters, and the upcoming Q2 earnings report is projected to be the worst quarter for Meta throughout its history in terms of growth (flat revenues and a 25% y/y decline in EPS). With all of this being said, the medium and long-term outlook for Meta remains positive among analysts.

Seeking Alpha

Seeking Alpha

From a fundamental perspective, Meta looks like a fantastic mature stage company to own for Value and GARP investors with its 8.3% yield.

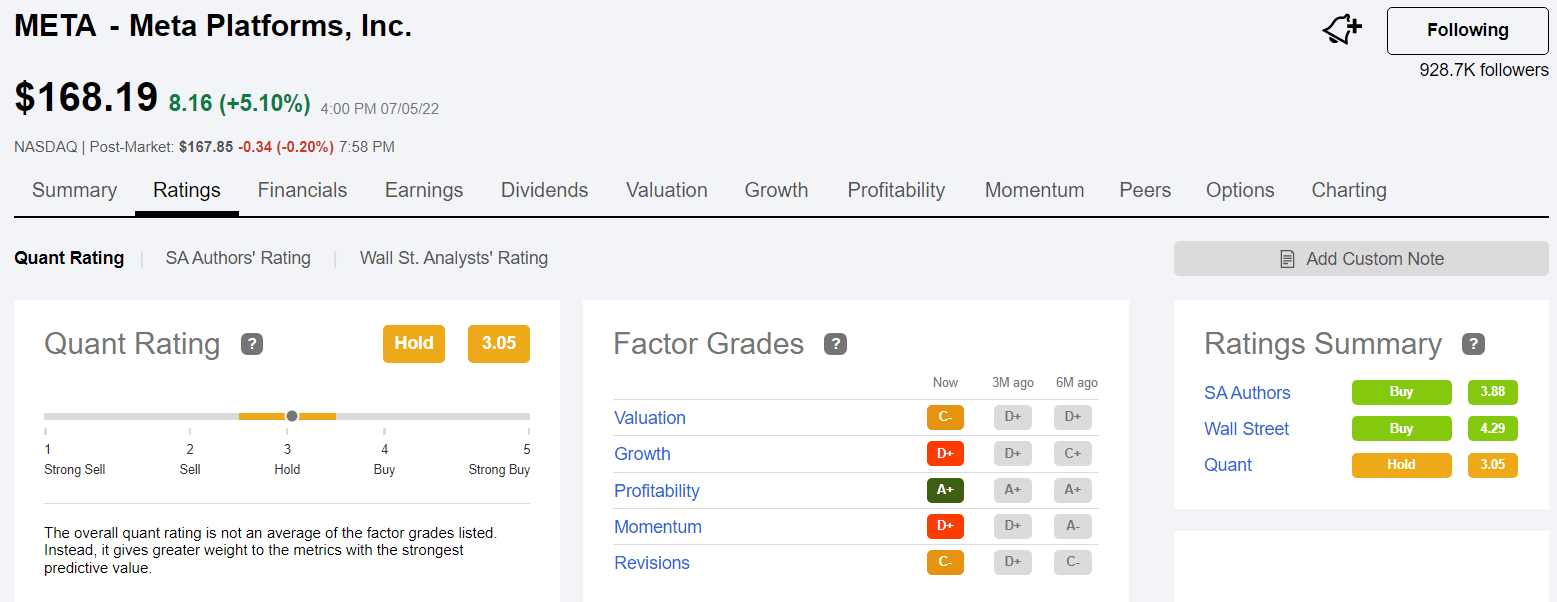

Furthermore, Seeking Alpha’s Quant Rating system rates Meta at “Hold” with a score of 3.05 (up from April rating of 3.04). While Meta scores an A+ on profitability (due to its best-in-class gross and net profit margins), it has a D+ rating on growth (slowdown) and momentum (bearish price action). Additionally, Meta’s Valuation and Earnings Revisions factor grades have improved to “C-” each (downward). Overall, quant factor ratings for META at ‘3.05’ are neutral.

Seeking Alpha Quant Ratings

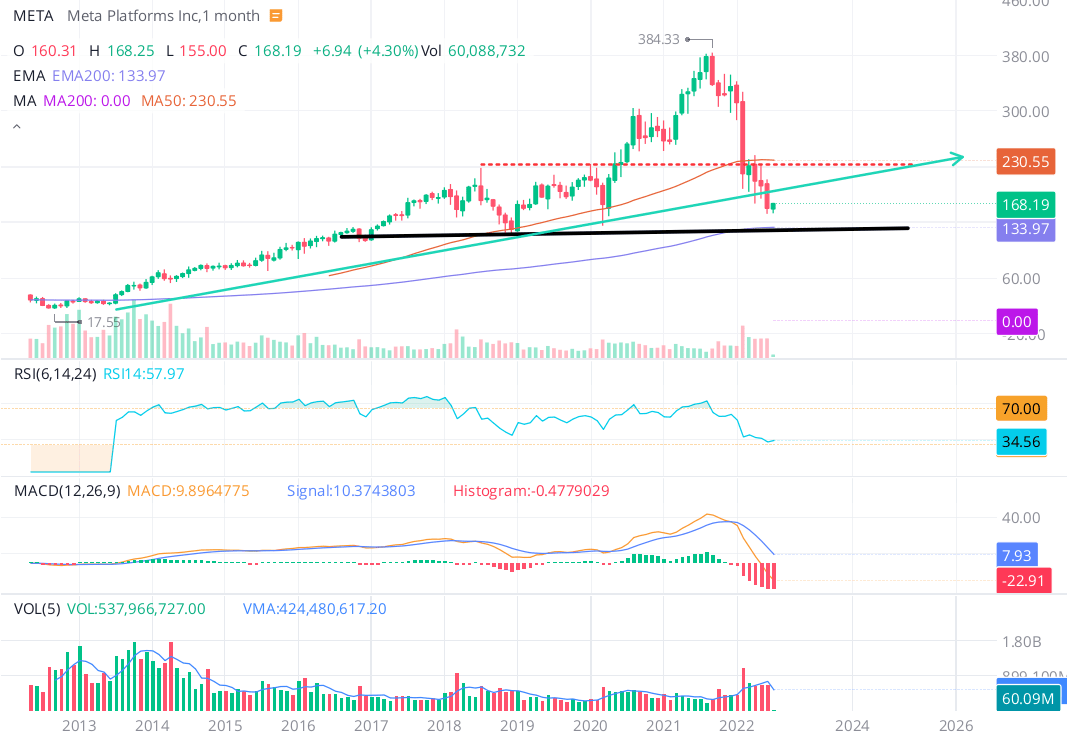

There is no space for indecision at TQI; however, Meta’s technical charts tell me that the stock is currently trading in no-man’s land. After sliding through its long-term bullish trendline (marked in a green arrow on the chart), Meta’s stock is trying to bounce back up.

WeBull Desktop

With this being said, Meta’s technical chart is broken (the business is not), and it could easily test the $133 support zone, which also happens to be Meta’s 200-EMA level. Hence, if you are looking for a near-term play, skip Meta. However, if you are looking for a long-term buy, Meta is a fantastic buy.

Is META Stock A Buy, Sell, or Hold?

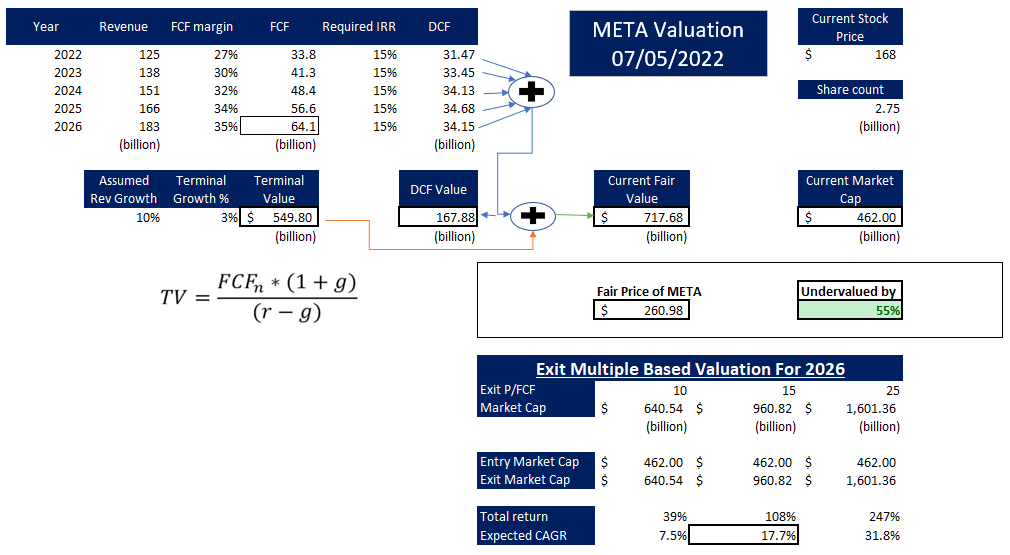

There’s only one way to find out: determining Meta’s fair value and expected returns. To do so, we will use a simple discounted cash flow model with the following assumptions:

2022E revenue

$125B

Forward 5-Yr Revenue Growth Rate (%)

10%

Terminal Growth Rate (%)

3%

Optimized FCF Margin (%)

27-35%

Discount Rate / Required IRR (%)

15%

Exit Multiple [P/FCF] (bear, base, and bull case scenarios)

10x,15x & 25x

Before we look at the results, I would like to clarify some of my assumptions. Meta Platforms is a broadly followed company, and we are unlikely to see significant surprises to consensus analyst estimates. However, I am opting for a lower CAGR revenue growth rate to implement a margin of safety in my model.

Seeking Alpha

Furthermore, I am starting with an optimized FCF margin of 27%, lower than what the company is set to do (~30%) for 2022. Again, the goal is to implement a margin of safety (considering Mark Zuckerberg’s repeated warnings on the economy and the effect of Apple and TikTok on Meta’s business). All other assumptions are pretty straightforward, but if you have any questions, please share them in the comments section below.

Results:

TQI Valuation Model (Author)

As you can see above, META’s fair value is ~$717B ($261 per share). With the stock trading at ~$168, it is currently trading at a discount of 55% to its fair value. According to TQI Valuation Model, META’s stock appears to be massively undervalued. However, what sort of returns could one expect in the future by buying Meta at current levels?

After getting re-priced as a value stock, META is now trading at a P/FCF multiple of ~10-12x with 2022 expected revenue growth of 6-7%. While this may seem like a fair multiple based on current y/y growth numbers, I don’t think Meta is getting enough credit for a potential re-acceleration in growth from Family of Apps (Reels and WhatsApp monetization), let alone the Metaverse. If Metaverse turns out to be the next-gen computing platform after mobile, Meta Platforms could emerge as a big winner considering its early leadership in this nascent market. We could have years and years of growth left in the tank at Meta, but let’s skip the Metaverse piece for today – if it works, great; if it fails, fine. Meta is a tremendous business to own even without the Metaverse (Reality Labs); some might argue it’s better without the Metaverse. However, I am with Mark Zuckerberg on this one – META needs to be a gatekeeper in the next generation of computing platforms.

After years of rapid growth, Meta is entering a period of slower sales growth (10-15% per year). Meta’s margins could also come under pressure due to a poor macroeconomic backdrop, lower advertising ROI (Apple’s iOS policy changes), and heightened competition (from TikTok, Amazon, Apple, and others). With this information in mind, let’s figure out Meta’s potential share price in 2026.

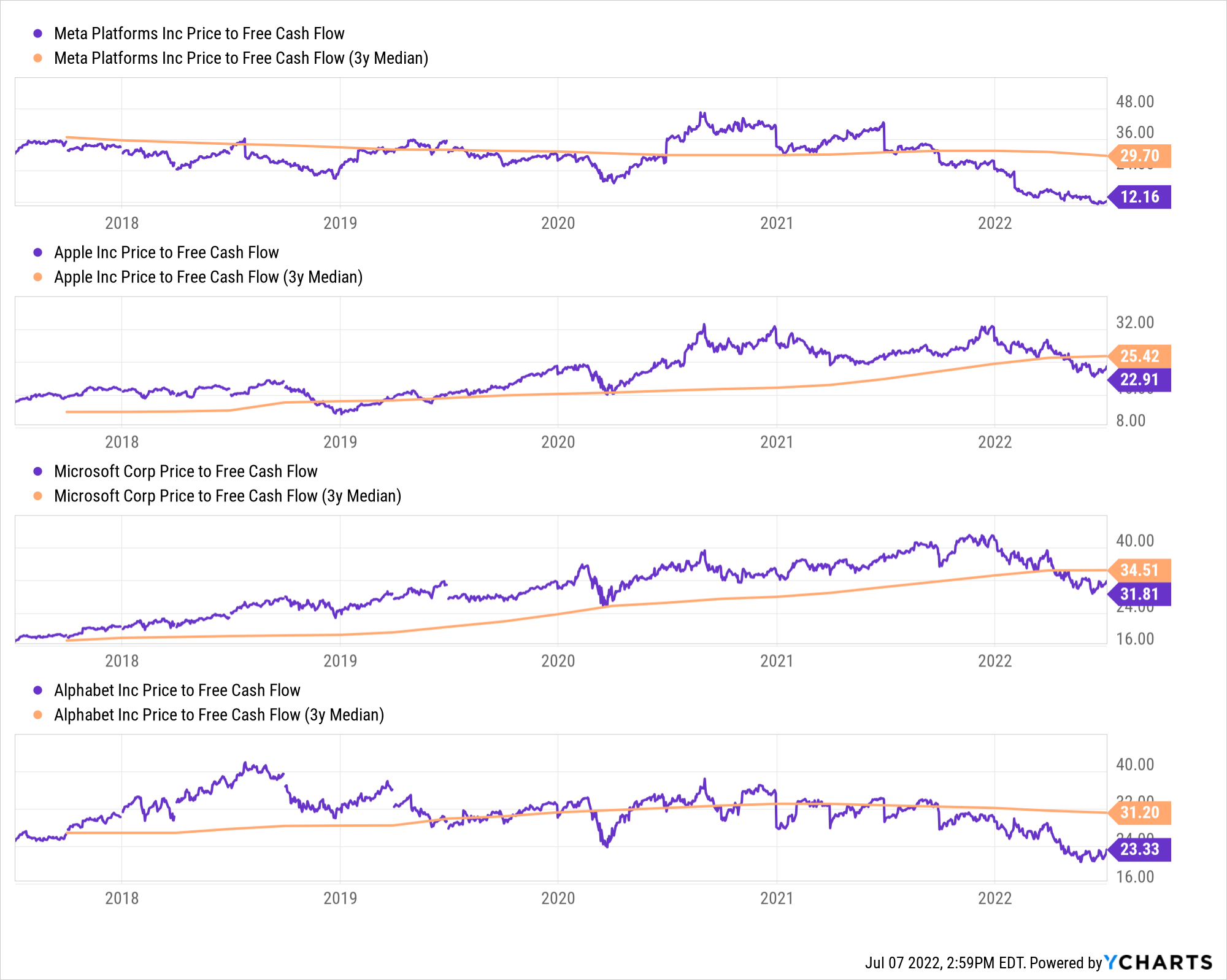

To find a reasonable range for an exit multiple, I looked at some of Meta’s median P/FCF multiples and that of peers (i.e., big tech giants like Apple, Microsoft, and Google). Interestingly, all of them are trading below their 3-yr median P/FCF multiples.

YCharts

Meta has a history of trading below its median P/FCF for extended periods; however, each time, it has successfully mean-reverted back up to the median. Will history repeat itself? I can’t say for sure, but if it does, META’s stock would be ~2.5x of current levels (just by multiple expansion).

In 2026, META would be growing at around 10-15% per year, with operating margins of ~35-40%. While the exact multiple is a function of risk-free rates, I believe that if the risk-free rate were at 3-3.5% (where it is today), META’s FCF yield could be 4-5%, i.e., an exit P/FCF multiple of ~20-25x. In the case of a calamitous economic reset (higher interest rates: 6-8%), META’s yield may need to stay at 8-10%, which would mean an exit P/FCF multiple of ~10x. In the model I shared above, I used an exit P/FCF multiple of 15x, which in my view, is very conservative and provides an ample margin of safety. Assuming an exit P/FCF multiple of ~15x, I see META’s stock trading at $349 per share at the end of 2026, which implies a ~17.7% CAGR return over the next 4.5 years.

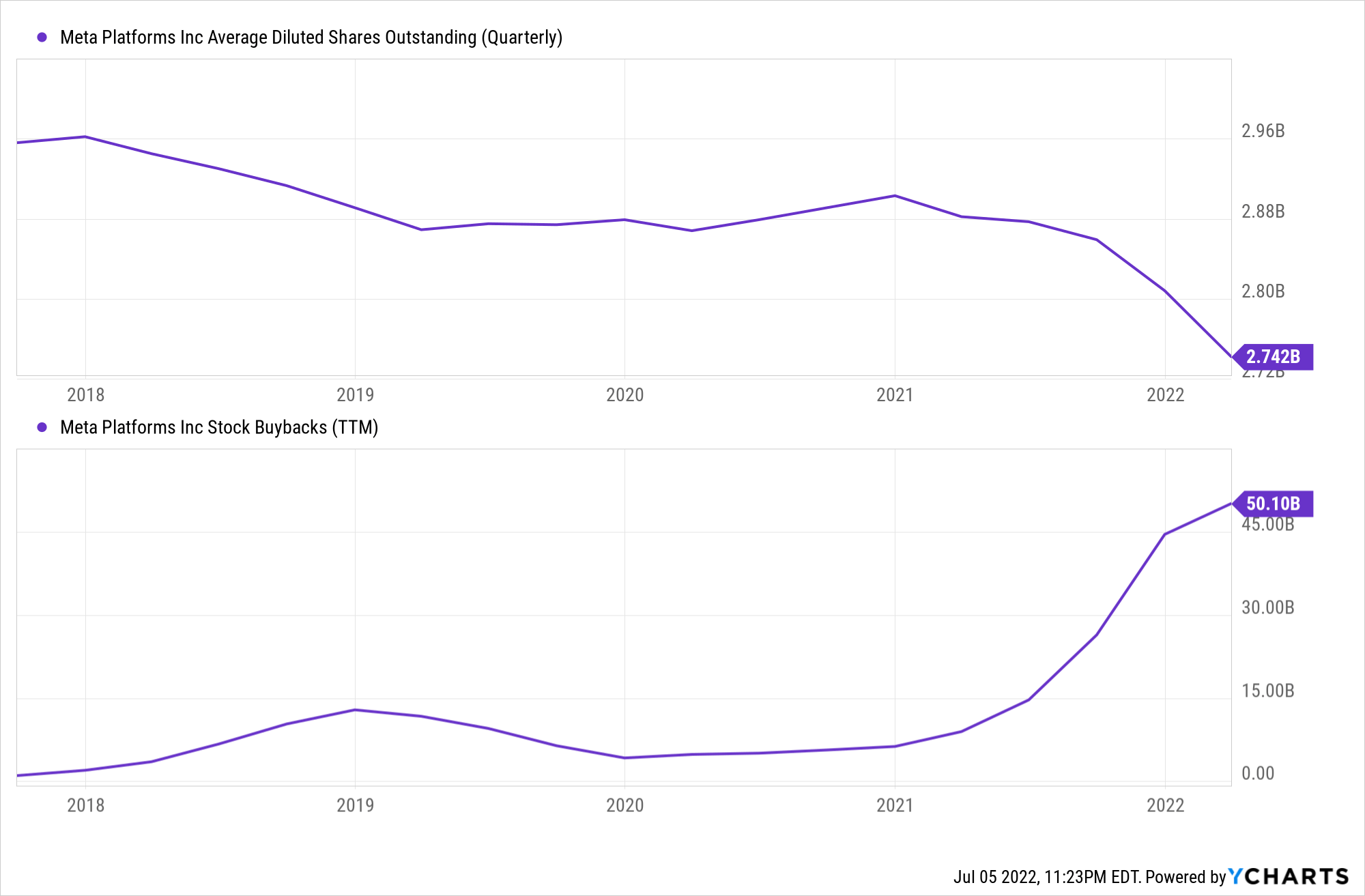

Now that we have valued Meta based on its future free cash flow stream and determined our base case return expectation for the stock, I think we are in the right frame of mind to think about the impact of Meta’s capital allocation strategy on shareholder returns. As you may know, Meta has tons of cash ($43B), no debt, and it is producing massive amounts of free cash flow (despite the massive ~$10B per year spending on Reality Labs). And nearly all of this cash flow is being returned to shareholders via stock buybacks.

YCharts

Over the last 12 months, META bought back $50B worth of its stock, and it will likely buy $20B more in H2 2022. By 2026, I expect META to buy back ~23% of its shares outstanding (spending $240B in 4.5 years). This ain’t rocket science; asset prices are a function of demand and supply. If META reduces the supply of its stock by 23%, the stock price is very likely to go higher.

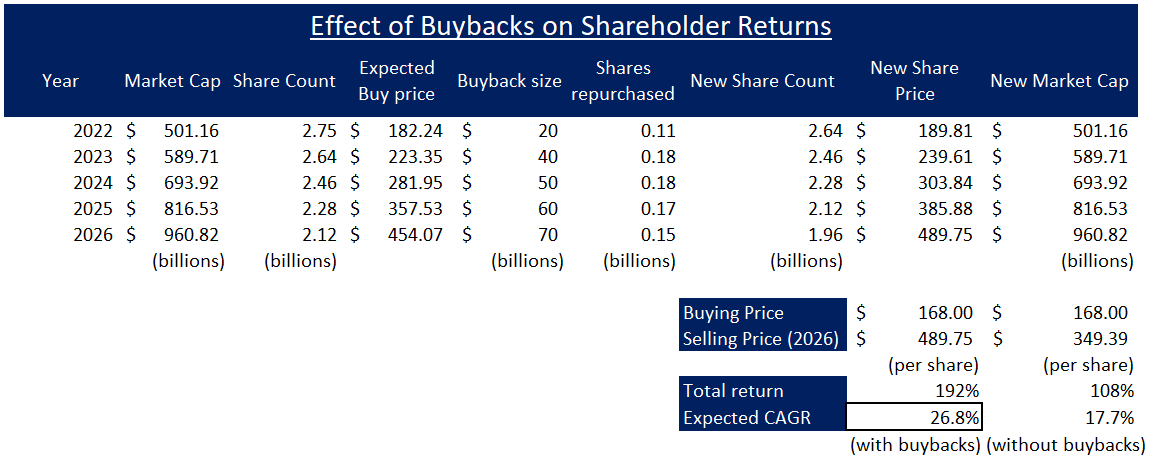

Let’s visualize the impact of Meta’s potential buyback program:

TQI Valuation Model (Author)

As we saw earlier, META investors could generate 17.7% CAGR returns (from current levels) till the end of 2026 (4.5 years). However, if we factor in an aggressive buyback program (along the lines of what META’s management has been using over the last couple of years), then investors could end up generating significantly better returns (26.8% CAGR). This is the power of financial engineering that META’s management could apply to boost shareholder returns.

Concluding Thoughts: Is Meta Platforms Stock A Good Long-term Pick?

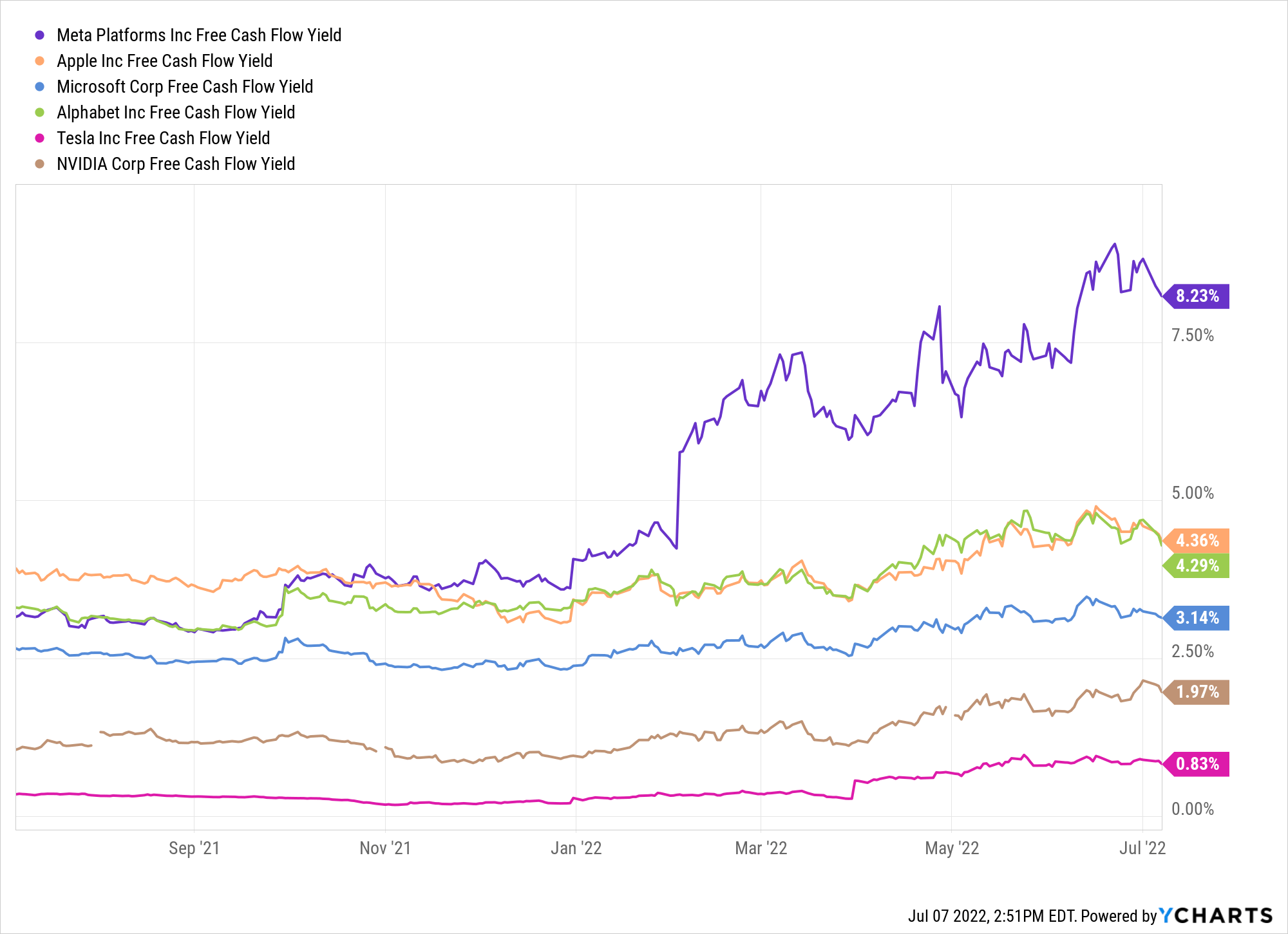

Among its big-tech peers, Meta is an outlier with its FCF yield of 8.2%. At this point, the market is basically betting that Meta’s free cash flow is set to fall by ~50%. With millions of businesses depending upon Meta’s Family-of-Apps to connect with billions of users across these platforms, I don’t think Meta’s free cash flows can drop by 50% even in a bad economy. Furthermore, if you are following Zuckerberg’s commentary, you would know that he is tightening up the belt at Meta, and the company is willing to prioritize short-term financial goals at the cost of some (non-essential) longer-term projects.

META is an outlier (YCharts)

In my view, META is the perfect setup for alpha generation via financial engineering. We are likely to see a period of slower growth from the social media giant, i.e., depressed valuation (10-15x P/FCF) could stay around for some time. However, robust FCF generation and aggressive stock buybacks will drive EPS, FCF/share, and the stock price higher. We have seen this playbook result in outsized gains in Apple (AAPL) [+576%] and Microsoft (MSFT) [+789%] (over the last decade). And I think Meta has a very good chance of emulating the stellar performance of these aforementioned tech stocks over the next decade.

Comparing current day Meta to Apple from 2013:

Apple (Mar 2013)

Meta (Mar 2022)

Low starting valuation

9-9.5x P/FCF

12.22x P/FCF

Net cash on balance sheet

$39.14B

$43.89B

Robust free cash flow

$44B

$39.81B

Sales Growth (%)

11%(was ~1% next Qtr)

6.64%

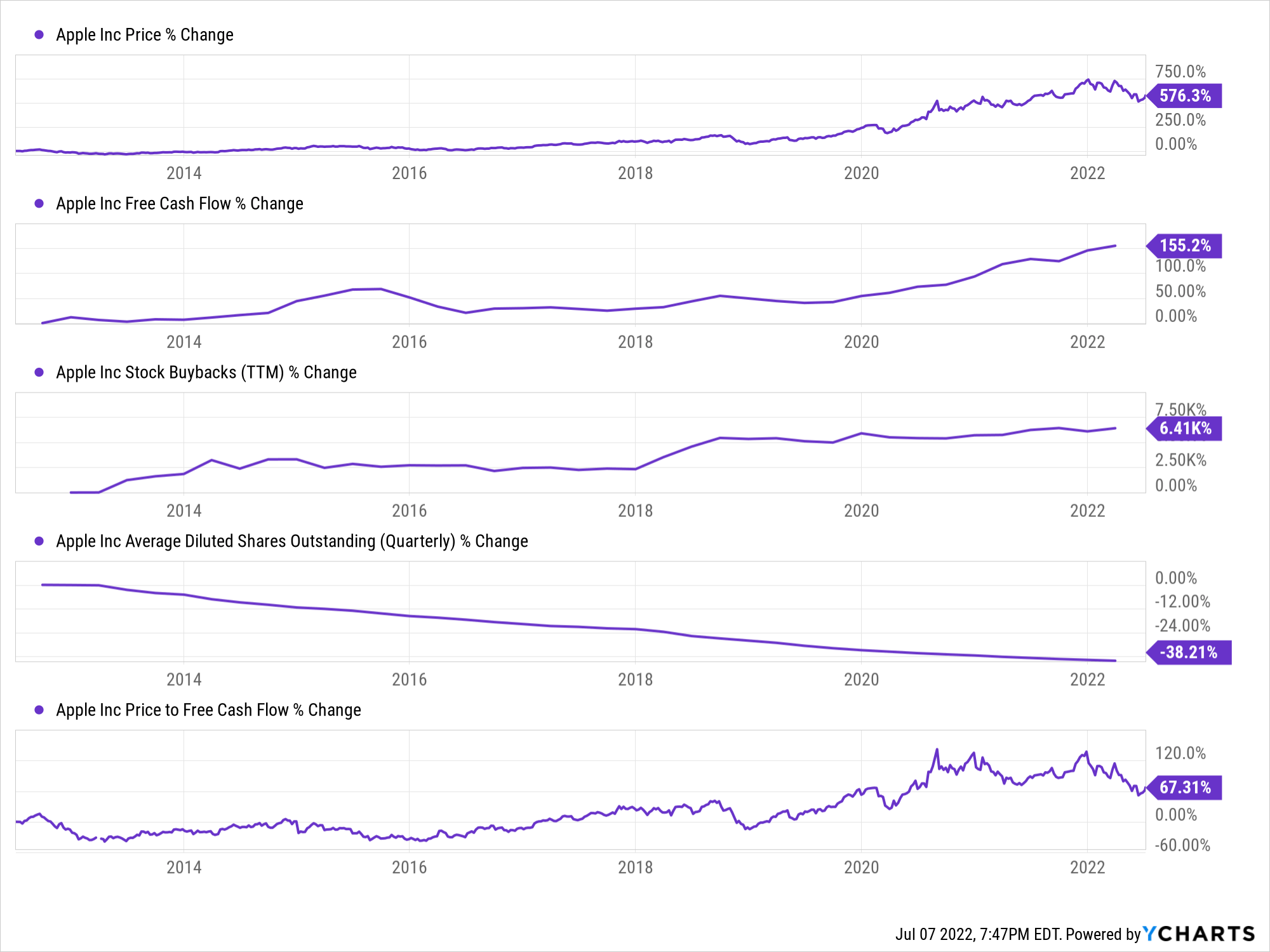

I am sure you see the similarities between Apple from Mar-2013 and Meta from Mar-2022. Apple is a tremendously innovative company that has transformed into a well-diversified conglomerate (of consumer hardware and software services) under the leadership of Tim Cook; however, a lot of the returns (~576% in the last ten years) generated by its stock have more to do with the financial engineering Cook and Co have applied at the Cupertino tech giant than to improvement in business fundamentals.

YCharts

Over the last decade, Apple’s free cash flows grew by ~155%; however, its stock went up by ~576%. Clearly, Apple’s market multiple has expanded. Now, most bulls would point towards Apple’s transformation into a services business as the major driver of this multiple expansion. I don’t agree with this idea because Domino’s Pizza (DPZ), a highly-commoditized business in a mature industry, has generated a 1200% return during the same period. The common factors between Apple and Domino’s (in 2012) were low starting valuations, robust balance sheet and free cash flow generation, and massive stock buybacks. The outsized returns generated by these companies result from financial engineering employed by their respective management teams. As we can see on the chart above, Apple reduced its share count by ~38.2% (over the last ten years). A massive decline in share count and steady free cash flow growth is a recipe for tremendous share price appreciation.

Trading at just 10-12x P/FCF, Meta is a deeply undervalued value stock that reminds me of Apple from 2012-13. Considering Meta’s robust balance sheet, free cash flow generation, humongous capital return program, and ability to grow sales (and free cash flow) at 10-15% CAGR, I can’t see how the stock could be lower five years out than where it is today. There’s nowhere to go but up. In my view, META is a no-brainer buy for Value and GARP investors with a long-term orientation (investment horizon of 3+ years).

Key Takeaway: I rate META a strong buy at $168

Housekeeping Note: I’ll soon be launching a Marketplace service on Seeking Alpha focused on generating long-term outperformance through financial engineering. While “The Quantamental Investor” won’t be live until early September, we are already building an exclusive (and free) community for retail investors at TQI Network. You can find more details in my profile bio. Stay tuned for more updates!

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment