gchutka/E+ via Getty Images

Elevator Pitch

I have a Hold rating assigned to FuelCell Energy, Inc. (NASDAQ:FCEL) shares.

In my prior January 19, 2022 article for FCEL, I wrote that “FuelCell Energy stock is a Hold, considering both its valuations and business outlook.” FuelCell Energy’s recently announced below-expectations Q2 FY 2022 (YE October 31) financial results have prompted me to publish an update considering whether FCEL deserves to be downgraded to a Sell rating.

I don’t see FCEL as a Sell, as the company should deliver a turnaround in its financial performance for the second half of fiscal 2022. On the flip side, a Buy rating won’t be appropriate based on a review of the stock’s current valuations. Therefore, I have decided to keep my Hold rating for FCEL unchanged.

Did FuelCell Energy Beat Earnings?

FuelCell Energy didn’t managed to beat market expectations relating to its second-quarter bottom line.

Prior to FCEL’s Q2 FY 2022 financial results release on June 9, 2022 before the market opened, investors were anticipating that FuelCell Energy could narrow its losses on a YoY basis. The Wall Street analysts’ consensus Q2 FY 2022 net loss per share estimate for FuelCell Energy was -$0.05, as compared to the company’s actual Q2 FY 2021 net loss per share of -$0.06.

But FCEL saw its net loss per share widen on a YoY basis to -$0.08 in the second quarter of fiscal 2022. The below-expectations bottom line for FuelCell Energy was a disappointment for investors, and this sent its shares falling by -7% from $4.07 as of June 8, 2022 to $3.80 as of June 9, 2022. FCEL’s shares declined by another -1% to close at $3.76 on June 10, 2022.

FCEL Stock Key Metrics

FCEL’s two other key financial metrics for Q2 FY 2022, revenue and operating losses, didn’t send positive signals as well, on top of the bottom line miss.

FuelCell Energy’s top line expanded from $14.0 million in Q2 FY 2021 to $16.4 million in Q2 FY 2022. This suggests that FCEL’s YoY revenue growth has decelerated from +114% (as per S&P Capital IQ data) in the second quarter of fiscal 2022 to +17% in Q2 FY 2022. FCEL’s Q2 FY 2022 revenue was -49% below the sell-side’s consensus second-quarter top line forecast of $32.3 million.

In my earlier January 2022 write-up for FuelCell Energy, I had highlighted that “FCEL is expected to record $60 million of product sales from Posco Energy in 2022” with respect to “an order for 20 modules.” At the company’s Q2 FY 2022 investor call on June 9, 2022, FuelCell Energy disclosed that “six (of the 20) modules were delivered last quarter (Q1 FY 2022)” and “none (of the remaining 14 modules) were delivered this quarter.” Zero module deliveries for FuelCell Energy in relation to the Posco Energy deal were below expectations, and a key factor leading to the revenue mix for the company.

The widening of FuelCell Energy’s losses at the operating level in the recent quarter was also discouraging for investors.

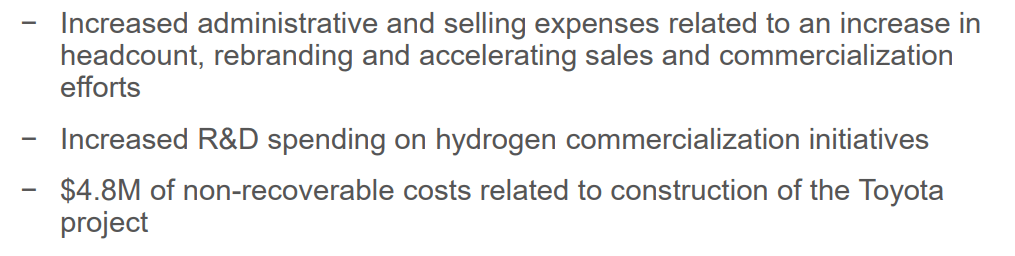

FCEL’s operating losses went from -$17.4 million in the second quarter of fiscal 2021 to -$28.2 million in Q2 FY 2022. The chart below highlights the key reasons for FuelCell Energy’s deterioration in profitability for the most recent quarter.

Factors Contributing To The Wider Losses From Operations For FCEL

Seeking Alpha

In the subsequent section, I discuss if there will be a turnaround in FuelCell Energy’s financial performance in the next few quarters.

What To Expect After Earnings

Investors should expect a substantial improvement in FuelCell Energy’s financial results in the coming quarters.

FCEL’s revenue miss in the recent quarter is likely due to a timing difference (as touched on in the preceding section), with revenue expected to be derived from the Posco Energy transaction deferred to subsequent quarters. This is validated by the sell-side’s consensus forecasts (as per S&P Capital IQ) which point to FuelCell Energy’s revenue growing to $35.5 million and $42.4 million in Q3 FY 2022 and Q4 FY 2022, respectively.

Similarly, sell-side analysts see FuelCell Energy’s non-GAAP adjusted EBITDA loss narrowing from -$21.2 million in the second quarter of fiscal 2022 to -$13.7 million and -$14.0 million for the third quarter and the fourth quarter, respectively.

FCEL’s near-term margins will be boosted by the delivery of the remaining 14 modules for Posco Energy (the 6 modules delivered in Q1 FY 2022 boasted a 18% gross margin) and a turnaround in profitability for the Services segment. FuelCell Energy highlighted at the company’s Q2 FY 2022 results briefing that “as the fleet expands, we do expect positive margins” for Services which delivered “negative margin” in Q2 FY 2022.

Is FuelCell Energy Stock Expected To Go Up?

There are two key factors that drive a stock’s future share price performance. The first factor is better-than-expected financial performance. The second factor is a positive valuation re-rating. Taking into consideration these two factors, the stock price outlook for FCEL is mixed.

As mentioned in the previous section of the current article, I expect FCEL to deliver stronger revenue growth and narrower EBITDA losses in the next two quarters of this fiscal year. This should provide support for FuelCell Energy’s share price in the short term.

On the other hand, FCEL’s valuations are still not particularly attractive on an absolute and relative basis, despite the fact that its share price has dropped by -35% year-to-date in 2022. FuelCell Energy is currently valued by the market at a high single-digit consensus forward next twelve months’ Enterprise Value-to-Revenue multiple, or 7.8 times to be exact, as per S&P Capital IQ valuation data.

The market now values FCEL at a premium as compared to Plug Power Inc. (PLUG) which trades at 6.6 times consensus forward next twelve months’ Enterprise Value-to-Revenue. FuelCell Energy is also valued at a small discount to another of its peers, Ballard Power Systems Inc. (BLDP) that boasts a consensus forward next twelve months’ Enterprise Value-to-Revenue multiple of 8.3 times. Historically, FCEL has always traded at a cheaper multiple as compared to both PLUG and BLDP. As a reference, FCEL’s five-year mean consensus forward next twelve months’ Enterprise Value-to-Revenue multiple was -6% and -32% lower than that of PLUG and BLDP, respectively as per S&P Capital IQ data.

In summary, while an improvement in FuelCell Energy’s financial performance in 2H FY 2022 could boost its stock price, its unappealing valuations will place a cap on the shares’ capital appreciation potential. I don’t see FCEL’s share price going up significantly in the near term.

Is FuelCell Energy A Good Investment Long-Term?

A good long-term investment is one where the stock’s future prospects in the long run are not appropriately reflected in its valuations. I don’t think this is the case with FuelCell Energy.

FCEL noted at its recent Q2 FY 2022 earnings call that it has “established targets for revenue in excess of $300 million by the end of fiscal year 2025 and in excess of $1 billion by the end of fiscal year 2030.” FuelCell Energy’s trailing twelve months’ revenue was $88.9 million. This translates to revenue CAGRs of +42% and +33% based on the company’s FY 2025 and FY 2030 top line goals, respectively.

At its Virtual Investor Day on March 16, 2022, FuelCell Energy emphasized that “POSCO (Energy)’s installed fleet in Korea, it’s quite large, and there’s a large potential there” and also stressed that “we’ve obviously now opened up the Asian market and are actively marketing in Asia.” In other words, FCEL expects greater sales contribution from POSCO Energy and Asian markets in general, which should be a key factor in helping the company achieve its future revenue targets.

But I think that FCEL’s high single-digit forward Enterprise Value-to-Revenue multiples have already priced in the company’s strong top line growth outlook to a large extent.

More importantly, the current market environment is unfavorable for high-growth companies which are still struggling to be profitable like FCEL. A May 9, 2022 portfolio strategy research report (not publicly available) titled “The Postmodern Cycle” published by Goldman Sachs highlighted that “the gap in valuation between high sales growth and high margin companies has started to narrow”, because “top-line growth is less scarce” with investors placing a “greater value on margins” in “the current environment with higher inflation.”

According to S&P Capital IQ consensus data, Wall Street analysts expect FuelCell Energy to be only EBITDA positive (and still loss-making in terms of the bottom line) in FY 2025. As such, I don’t think FCEL is an attractive long-term investment now, as its current Enterprise-to-Revenue valuations are reasonably fair taking into account its expected future top line growth rates and the market environment (favoring profitable, high margin companies) now.

What Is The Price Target For FCEL?

The consensus price target for FCEL is $4.79 now, which implies an upside of +27% as compared to the stock’s last done price of $3.76 as of June 10, 2022.

But this is potentially misleading, as none of the 11 sell-side analysts covering FuelCell Energy’s shares have a Buy rating. Nine of them rate FCEL as a Hold, with the remaining two having either a Sell or Strong Sell rating for the stock.

It is likely that most of the analysts have yet to publish updated reports and new price targets for FuelCell Energy. Considering FCEL’s year-to-date share price weakness (-35% as highlighted above) and Q2 FY 2022 revenue miss, there is a high probability that analysts will revise their respective target prices for the stock downwards in time to come.

Instead of focusing on price targets (which could be outdated), I have outlined in my analysis above that I am of the view that FCEL is fairly valued and not undervalued.

Is FCEL Stock A Buy, Sell, or Hold?

FCEL stock is a Hold. FuelCell Energy should achieve better financial results in the quarters to come, but its relatively expensive valuations will limit the stock’s potential upside.

Be the first to comment