Spencer Platt/Getty Images News

BlackRock, Inc. (BLK) is the world’s largest asset manager and has benefited from the rise of index-based investing and the strong financial market performance over the last several years. Indeed, BlackRock just reported its latest quarterly results highlighted by assets under management crossing a milestone of $10 trillion, driving overall solid operating and financial momentum. Overall, there’s a lot to like about BLK as a high-quality leader with a positive long-term outlook. That said, some headwinds into 2022 between rising market volatility and a changing interest rate environment warrant some caution. A plan to expand headcount while wages are rising is already pressuring margins and may limit the near-term upside in the stock.

Seeking Alpha

BlackRock Stock Earnings

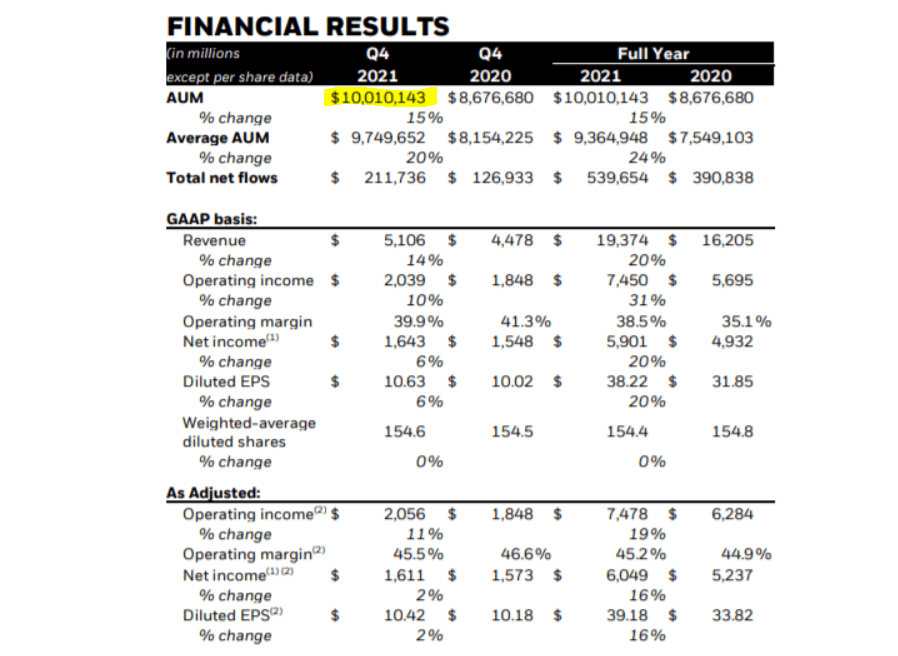

The company reported its Q4 2021 earnings on January 14th with non-GAAP EPS of $10.42 which was $0.28 ahead of the consensus. Revenue of $5.1 billion climbed 14% year over year, and reached $19.4 billion for the year, up 20% compared to 2020. As mentioned, total net inflows representing new client assets into AUM have been strong with Q4 bringing in $212 billion pushing AUM to $10.01 trillion, up 15% y/y.

Within AUM, ETFs that represent 33% of the total saw $104 billion of inflows in Q4 and this was a record for the company which considers both the seasonality of year-end rebalancing as well as organic demand. This is important because the base fees generated from AUM are the core financial driver for the company representing 75% of total revenues. In other words, there is a direct relationship between the AUM level and the financial results across base fees.

Management notes that nearly 60% of the organic base-fee increase in 2021 was driven by new types of products including active strategies which remain a strategic focus for the company. The effort has also supported growth in other revenue drivers like related distribution fees, and the smaller advisory business. There is also momentum from the technology services businesses, including the “Aladdin” portfolio management platform that generated annual contract value (ACV) 13% year over year.

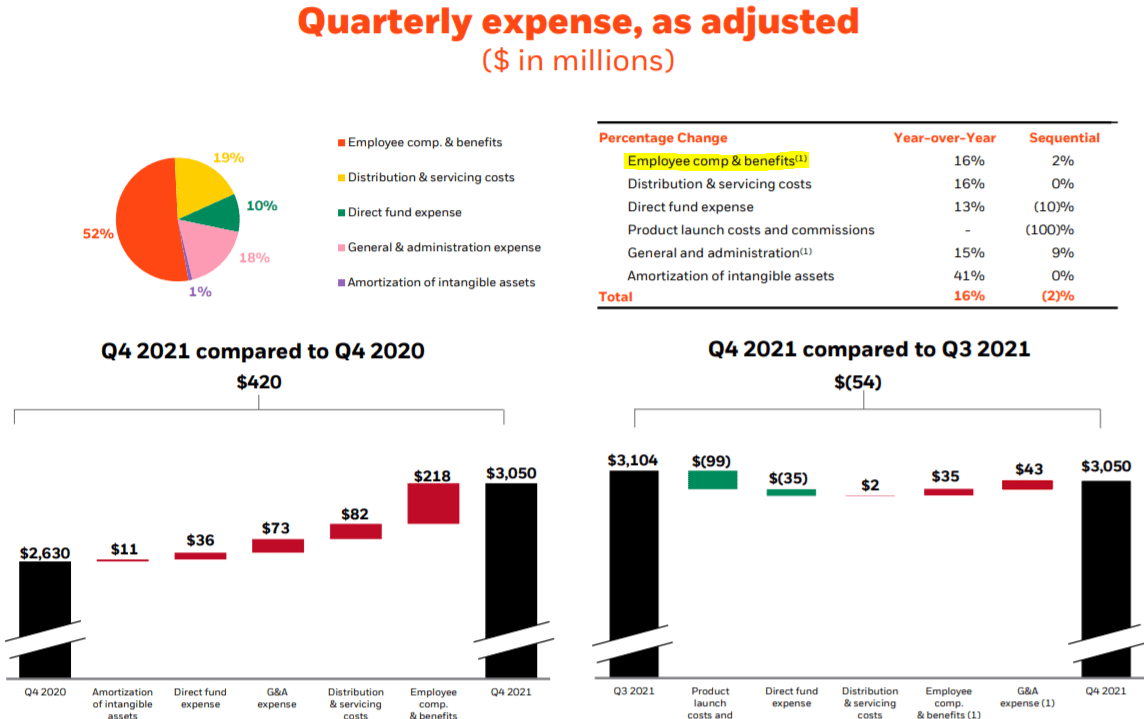

While full-year 2021 adjusted EPS at $39.18 climbed 16% compared to 2020, Q4 was defined by moderating financial trends as the Q4 adjusted operating margin at 45.5% narrowed from 46.6% in the period last year. Part of the challenge has been climbing employee compensation and benefits consistent with headline-making inflationary pressures and the tight labor market.

For context, employee comp represents nearly 52% of total operating expenses and climbed 16% y/y in Q4. The result was that the adjusted EPS this quarter was up just 2% compared to Q4 2020. Management made comments during the conference call explaining the intention of increasing headcount by 10% through 2022 to support continued growth.

While BlackRock is not issuing specific financial guidance or earnings targets, there was a sense of optimism for the year ahead noting important trends like the company’s climbing market share in key segments given growth above the industry. Another positive development is that products like ETFs are still gaining momentum as a worldwide theme within investment management. BlackRock has been expanding into more active products including alternative investments to drive growth. The company also sees significant opportunities related to a transition into a “net-zero” carbon world driving demand for ESG focused financial products.

BLK as a High-Quality Dividend Growth Stock

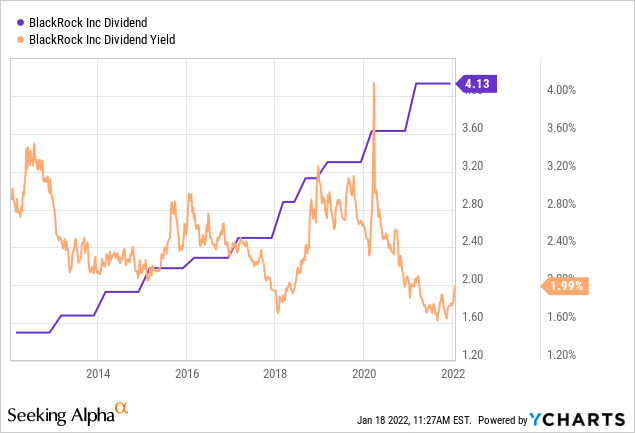

BlackRock has been able to translate what has been consistent growth and solid profitability into a generous shareholder distribution policy. With the Q4 earnings release, the company hiked its quarterly dividend rate by an impressive 18% y/y to $4.88, from the old $4.13 per-share amount.

The next payout set for March 23rd will be applied to shareholders of record as of March 7th. This means that investors must buy or own the stock before the ex-dividend date on March 4th to be eligible for the payment. On an annualized basis, the forward dividend yield is now 2.3% compared to 2.0% on a trailing twelve-month basis. This is the 13th consecutive year of a dividend hike going back to 2010.

Overall, the dividend payout ratio representing about 40% of earnings is well supported by underlying cash flows. The company has also been active with share buybacks, repurchasing $300 million in stock in Q4 and $1.2 billion over the past year. The effect has balanced some stock-based compensation while reducing the share count by about 0.5% compared to the end of 2020, adding incrementally to the total shareholder returns.

Is BlackRock A Good Long-Term Stock?

Any bullish case for BLK is going to be dependent on an expectation that AUM continues to climb higher as a driver of the top-line revenue through the core base fees. Going back to the depths of the Covid crisis in 2020, the company has benefited from an impressive market performance of financial assets considering major equity indexes like the S&P 500 (SPY) and global benchmarks that ended 2021 at or near their all-time highs. The result has directly translated into higher fees as the values of investments and client portfolios climb, while also supporting positive sentiment for new capital flows.

High-level themes like global GDP growth including increasing levels of financialization, particularly among emerging markets, support significant long-term growth opportunities. We can expect BlackRock to continue gaining and consolidating its market share as a positive tailwind for earnings.

On the other hand, markets have started 2022 with increasing levels of volatility including a deep sell-off in bonds with rising interest rates adding to weakness in risk assets. This setup is concerning with the understanding that poor returns either in stocks, fixed income, or alternative investments represent a poor backdrop for new capital flows into investment products which can pressure BlackRock’s operating environment. The point here is that softer returns across all asset classes going forward, compared to 2020 and 2021, can imply a weaker growth environment for the company.

According to consensus estimates, the market is expecting BlackRock revenue and earnings growth to average about 9% per year through 2024. We can argue there is some downside to these estimates in a scenario where financial market conditions deteriorate into weaker returns across all asset classes.

Seeking Alpha

Compared to the EPS estimate of $42.60 for 2022, a case can be made that the Q4 trends that already included some weaker operating margins can open the door for BLK to underperform going forward. What’s unique about BLK as an asset manager compared to other types of businesses is the importance of employee wages representing nearly half of all costs.

Salaries on Wall Street overall have been hot amid intense competition for “talent”. Other financial sector leaders that have already reported Q4 results have echoed these trends, including JPMorgan Chase & Co. (JPM) which have guided for higher expenses. While investment and commercial banks stand to benefit from rising interest rates through a higher net interest margin spread, the relationship is less clear with BlackRock. Rising rates can limit sentiment towards fixed-income investment products while declining fixed-income fund values directly hit some of the base fees through a lower AUM.

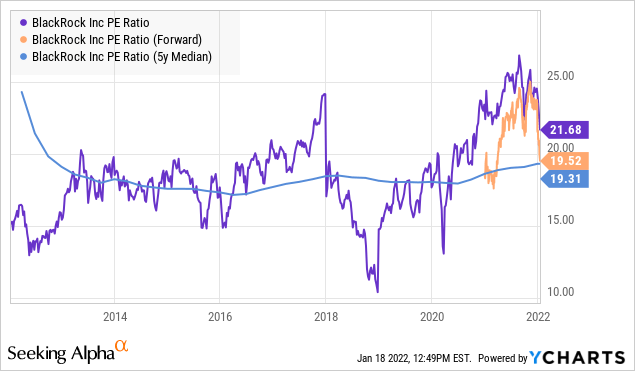

In terms of valuation, the forward P/E of 19.5x is right around the company’s 5-year average for the multiple. By this measure, the stock is not necessarily expensive although it has traded with a P/E multiple around 15x several times over the past decade. We typically like to see stocks with rising multiple in an environment where growth and earnings are accelerating, which is not the case here.

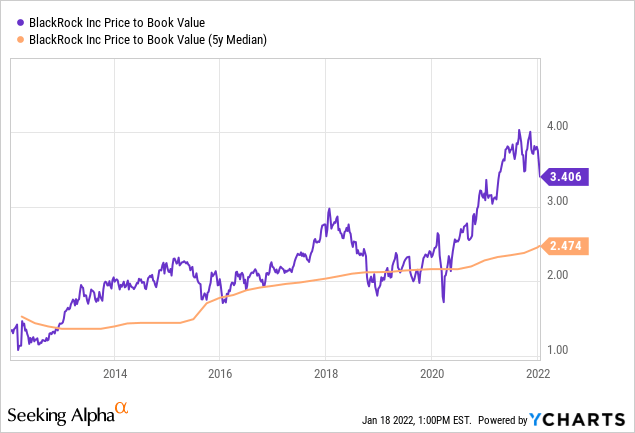

We can also highlight BLK’s price to book ratio at 3.4x represents a premium to the company’s 5-year average for the multiple closer to 2.5x. We sense that BlackRock’s leadership, particularly since the pandemic, included its close relationship with the Federal Reserve. The company was given the mandate to manage the Fed’s portfolios of corporate bonds and debt ETFs in 2020, and that added a layer of quality to the stock supporting a higher valuation. Nevertheless, the stock is relatively expensive by the P/B measurement.

Is BLK Stock A Buy, Sell, or Hold?

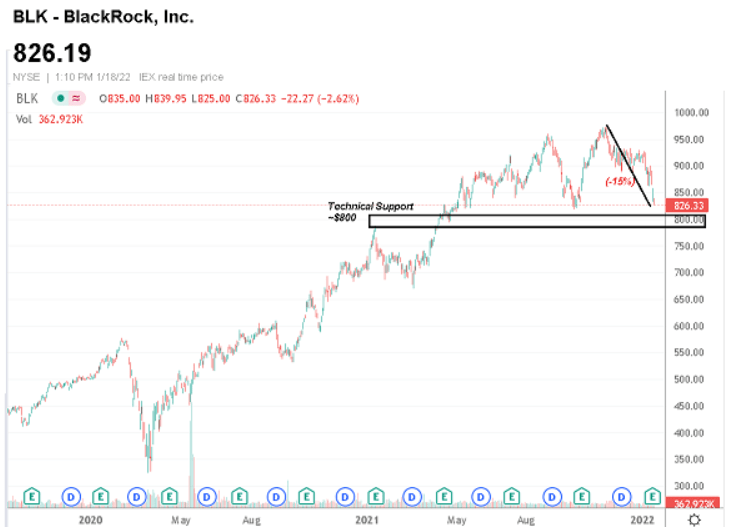

We rate BLK as a hold with an $800 price target for the year ahead implying a forward P/E of 19x on the consensus EPS. Our thinking here is that with shares of BLK currently down around 15% from its all-high reached in November, the market may have already priced in some of the near-term headwinds. We expect continued volatility over the near term into ongoing macro concerns and broader financial market uncertainties related to Fed policy. That said, in our opinion, it’s probably too late to sell for current investors while the hold rating implies a neutral view for traders on the sidelines.

Seeking Alpha (author annotation)

While our target is a few percentage points lower than the current stock price, the core business is fine and maintains a positive long-term outlook. We would be tactical buyers on any correction under $750 with a more attractive reward to risk setup. The company likely has some room to adjust its hiring plans for 2022 if market conditions deteriorate which can provide some support to financial margins and earnings. Significantly higher interest rates down the line will make fixed-income relatively more attractive for new capital flows through higher yields as a new tailwind for the business.

Again, the main risk to watch would be for a more concerning deterioration of the macro outlook. Weaker than expected economic growth including the possibility of a slowdown in consumer spending would further pressure the investing environment and challenge BlackRock’s financial momentum. Key monitoring points in the upcoming quarters include AUM trends along with the adjusted operating margin.

Be the first to comment