alvarez/E+ via Getty Images

A Quick Take On Iris Energy

Iris Energy (NASDAQ:IREN) went public in November 2021, raising approximately $232 million in gross proceeds from an IPO priced at $28.00 per share.

The firm operates as a Bitcoin mining company using primarily renewable energy to power its mining operations.

Given the extremely unfavorable bitcoin mining market and the company’s apparent SPV financing default status, my opinion on IREN is to Sell the stock.

Iris Energy Overview

Sydney, Australia-based Iris was founded to operate Bitcoin mining computers that seek to use renewable energy as a power source.

Management is headed by co-founder and co-CEO Daniel Roberts, who has been with the firm since inception and was previously employed at Macquarie Group and PricewaterhouseCoopers with experience in the finance, renewables and infrastructure industries.

The firm has been mining Bitcoin since 2019 and does not hold Bitcoin on its balance sheet.

The market value for mining depends on the price of Bitcoin, since the majority of value going to the miner is a function of the current Bitcoin reward rate of 6.25 Bitcoin per successfully mined block.

At a price of $25,000 per Bitcoin, the annual mining rewards for the entire industry would be approximately $8 billion.

Major competitive or other industry participants include:

-

Bitfarms

-

Argo Blockchain

-

DMG Blockchain

-

Hive Blockchain

-

Hut 8 Mining

-

HashChain Technology

-

DPW Holdings

-

Layer1 Technologies

-

Riot Blockchain

-

Marathon Patent Corp.

-

Core Scientific

-

Others

Iris’s Recent Financial Performance

-

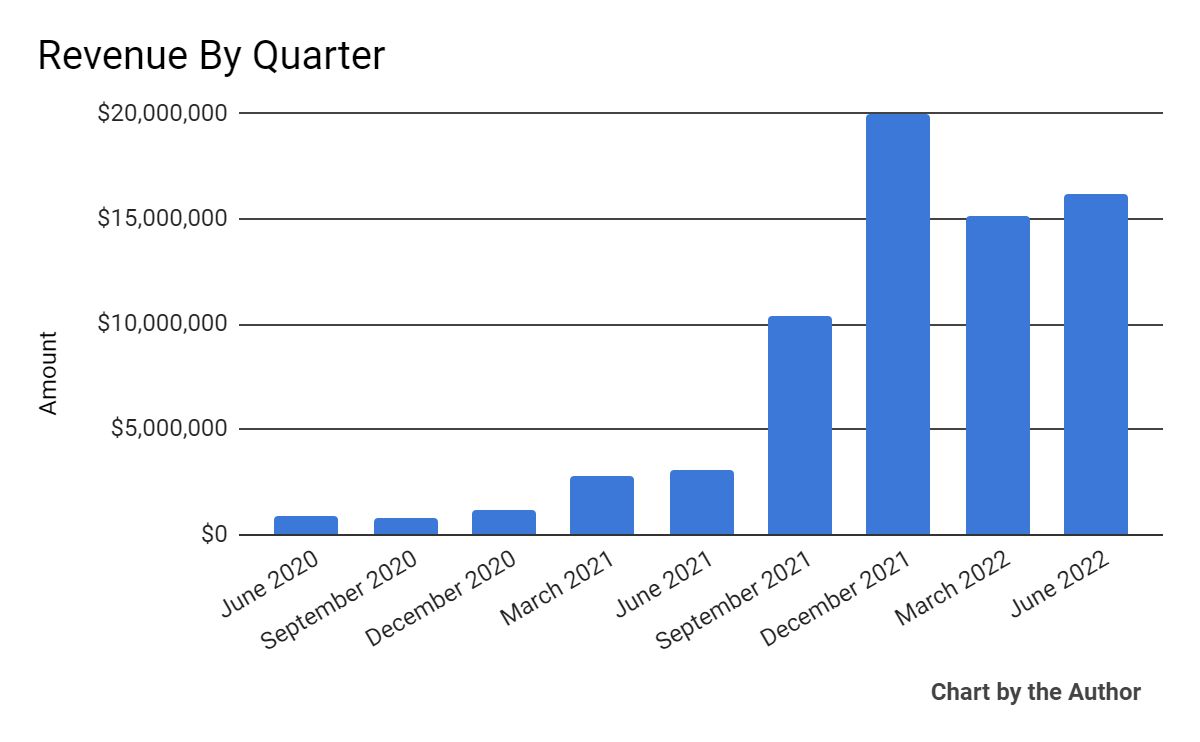

Total revenue by quarter has risen as the company’s bitcoin mining computers have come online:

9 Quarter Total Revenue (Seeking Alpha)

-

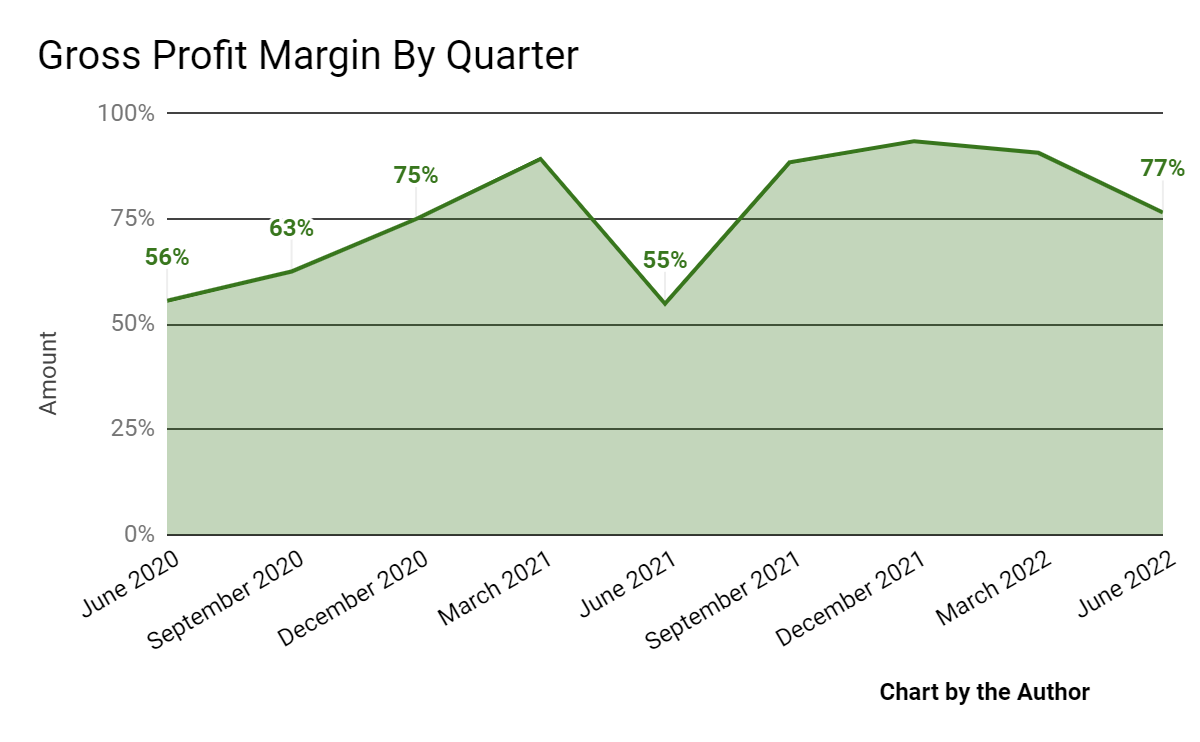

Gross profit margin by quarter has varied significantly in recent quarters:

9 Quarter Gross Profit Margin (Seeking Alpha)

-

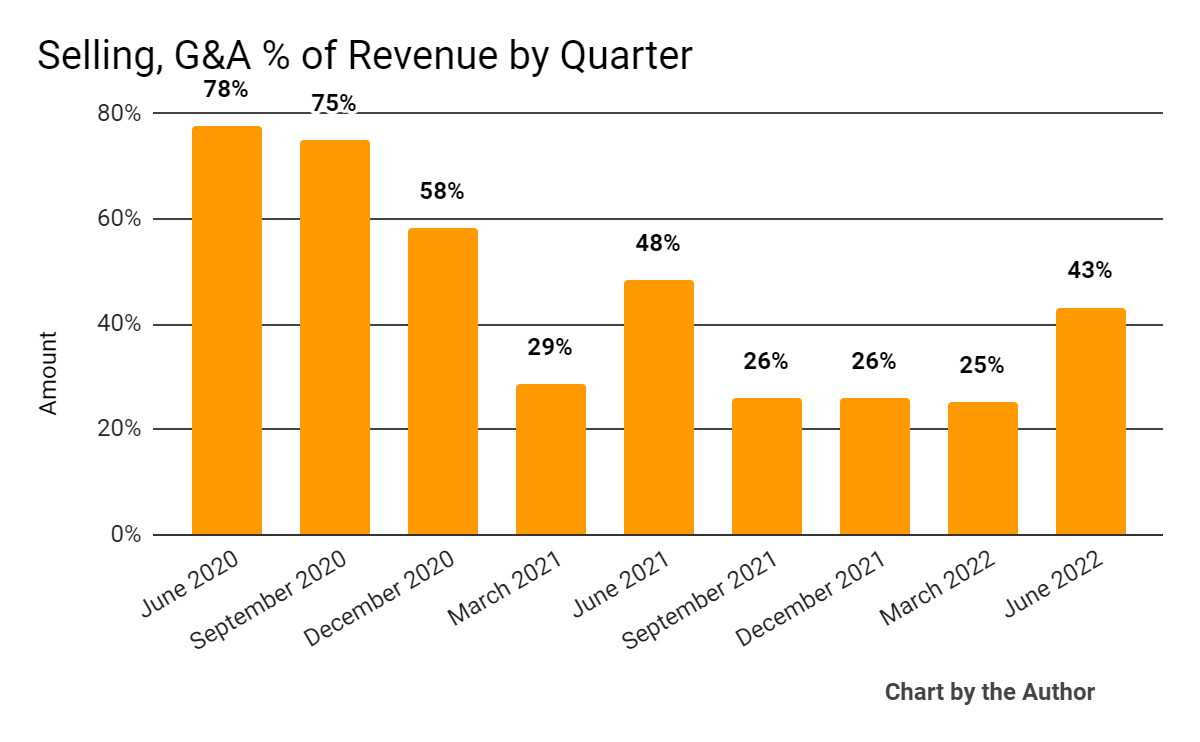

Selling, G&A expenses as a percentage of total revenue by quarter have dropped as revenue has climbed:

9 Quarter Selling, G&A % Of Revenue (Seeking Alpha)

-

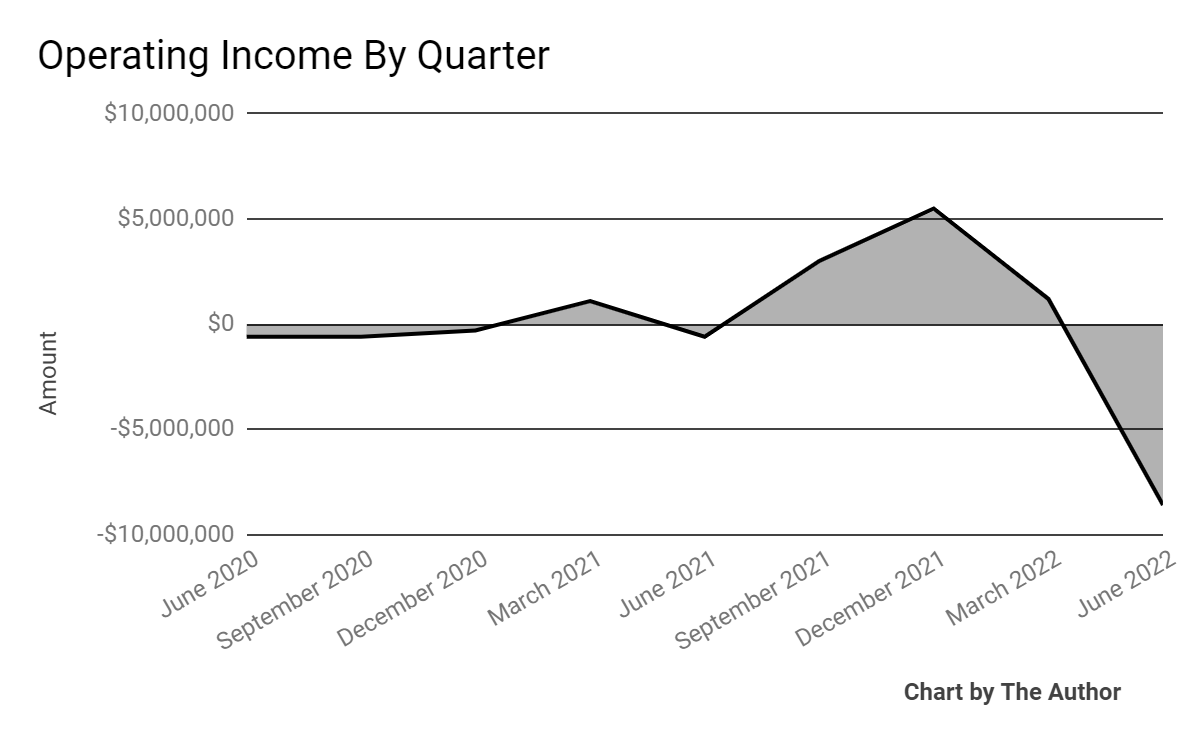

Operating income by quarter has turned substantially negative in recent quarters:

9 Quarter Operating Income (Seeking Alpha)

-

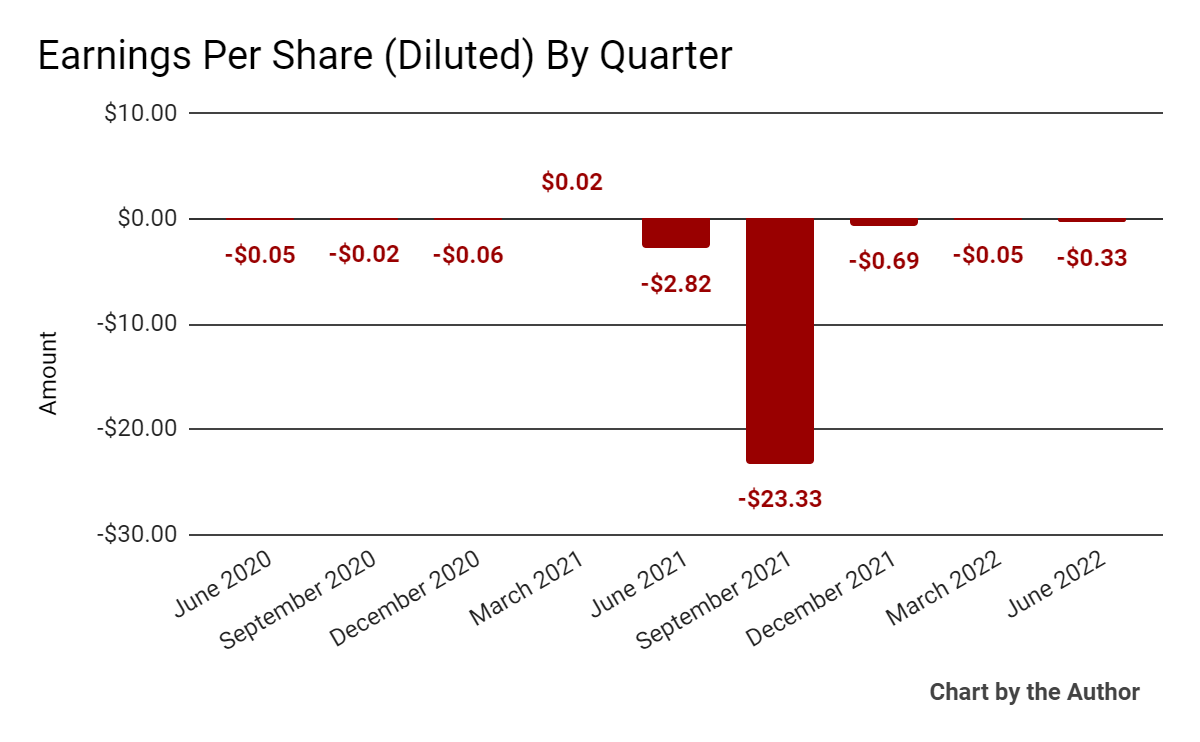

Earnings per share (Diluted) have remained heavily negative in recent quarters:

9 Quarter Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

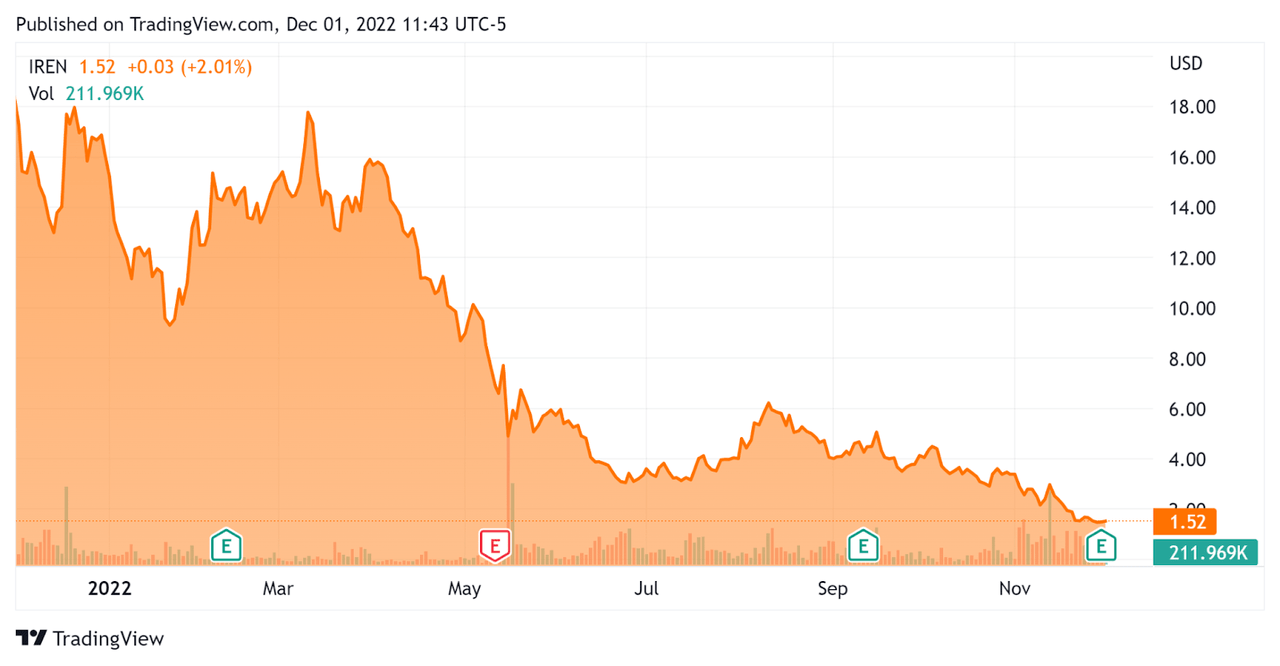

Since its IPO, IREN’s stock price has fallen 91.7% vs. the U.S. S&P 500 index’ drop of around 9.6%, as the chart below indicates:

52 Week Stock Price (Seeking Alpha)

Valuation And Other Metrics For Iris Energy

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

1.3 |

|

Enterprise Value / EBITDA |

9.7 |

|

Revenue Growth Rate |

647.5% |

|

Net Income Margin |

0.0% |

|

GAAP EBITDA % |

13.8% |

|

Market Capitalization |

$80,820,000 |

|

Enterprise Value |

$79,140,000 |

|

Operating Cash Flow |

$21,560,000 |

|

Earnings Per Share (Fully Diluted) |

-$24.40 |

(Source – Seeking Alpha)

As a reference, a relevant partial public comparable would be Hut 8 Mining (HUT); shown below is a comparison of their primary valuation metrics:

|

Metric [TTM] |

Hut 8 Mining |

Iris Energy |

Variance |

|

Enterprise Value / Sales |

1.7 |

1.3 |

-22.1% |

|

Enterprise Value / EBITDA |

6.0 |

9.7 |

62.8% |

|

Revenue Growth Rate |

44.9% |

647.5% |

1341.1% |

|

Net Income Margin |

-89.6% |

0.0% |

–% |

|

Operating Cash Flow |

-$79,120,000 |

$21,560,000 |

–% |

(Source – Seeking Alpha)

A complete comparison of the two companies’ available performance metrics may be viewed here.

Commentary On Iris Energy

In its last earnings call (Source – Seeking Alpha), covering FQ4 2022’s results, management highlighted the shift in bitcoin mining from a previous emphasis on the computing component to a current emphasis on energy and infrastructure.

Iris hasn’t held bitcoin on its balance sheet as a matter of policy, liquidating its bitcoin rewards on a daily basis.

In recent quarters, the company has energized its large purchases of mining computers, so revenue from bitcoin mining has risen despite the fall in the price of each bitcoin.

As to its financial results, however, with the fall of bitcoin’s price, the firm has yet to make a profit.

Furthermore, operating income has turned negative in the most recent reporting period.

Additionally, the company holds its bitcoin mining fleet inside subsidiaries [SPVs] that are financed by lenders that have limited recourse to the main corporate entity. Instead, they have recourse to the mining equipment itself, subject to the terms of those financing agreements.

The company recently published an update on the status of those SPVs, indicating that the two larger SPVs are not generating enough cash to pay their debt obligations and their value is well below lending agreement requirements.

Management is seeking to negotiate additional terms to those agreements but has not divulged the current status of those negotiations.

In the meantime, the company has sold some pre-paid miners to a third party for net cash of $8.6 million.

The stock was recently downgraded by Cantor Fitzgerald as the firm believes Iris will not be able to renegotiate its financing arrangements and revenue will fall precipitously once those mining computers are repossessed by the lenders.

The primary risk to the company’s outlook is the continued low price of bitcoin combined with an enormous overhang in hash power, resulting in an unprofitable net hash price.

Given the extremely unfavorable near-term bitcoin mining market and the company’s apparent SPV financing default status, my opinion on IREN is to sell the stock.

Be the first to comment