Solskin

A Quick Take On EMulate Therapeutics

EMulate Therapeutics, Inc. (EMTX) has filed proposed terms for a $12.5 million IPO of its common stock, according to an amended S-1/A registration statement.

The company is developing medical device technologies for the treatment of various serious health conditions.

EMTX is thinly capitalized, so I’m on Hold for the IPO.

EMulate Therapeutics Overview

Bellevue, Washington-based EMulate was founded to develop its ulRFE low-to-ultra-low radio frequency energy device to regulate “signaling and metabolic pathways on the molecular and genetic levels – without chemicals, radiation or drugs.”

Management is headed by Chairman, CEO and president Chris E. Rivera, who has been with the firm since 2014 and was previously founder, CEO and president of Hyperion Therapeutics and head of Commercial Operations at Genzyme Therapeutics, “where he built and ran Genzyme’s US renal Commercial Operations.”

The firm says its electromagnetic field technology has “produced substantially similar molecular effects as the paclitaxel drug at the cellular level.”

Below is a chart from the firm detailing the status of its device studies:

Company Status (SEC)

Management says it is “pivotal trial ready” for various treatment indications but is not currently conducting trials, and it is unclear to what extent Phase 1 or Phase 2 trials have been conducted and accepted by the U.S. FDA.

The company operates through a number of subsidiary entities depending on the specific health focus.

EMulate has booked fair market value investment of $19.2 million as of September 30, 2022 from investors, including The Butters Family Revocable Trust and individuals.

EMulate’s Market & Competition

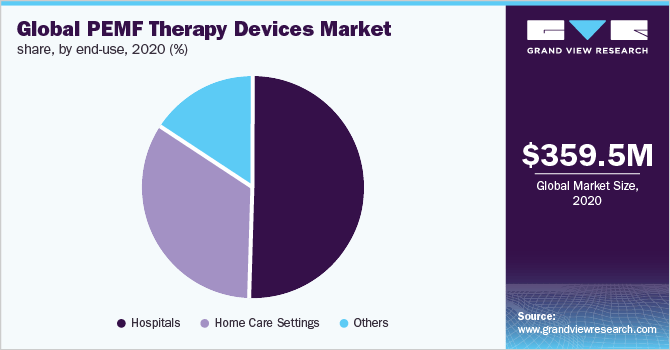

According to a 2021 market research report by Grand View Research, the global market for pulse electromagnetic field therapy [PEMF] devices was an estimated $360 million in 2020 and is forecast to reach $656 million by 2028.

This represents a forecast CAGR (Compound Annual Growth Rate) of CAGR of 7.8% from 2021 to 2028.

Key elements driving this expected growth are improvements in PEMF device technologies, miniaturization and increasing bone fractures and diseases associated with aging populations.

Also, the pie chart below shows the breakdown of PEMF devices by market use:

Global PEMF Devices Market (Grand View Research)

Major competitive vendors that provide or are developing related treatments include:

-

Novocure

-

Bedfont Scientific

-

Orthofix Holdings

-

I-Tech Medical Division

-

OSKA

-

Medithera

-

NiuDeSai

-

Nuage Health

-

Oxford Medical Instruments Health

-

Bemer, LLC.

EMulate Therapeutics Financial Status

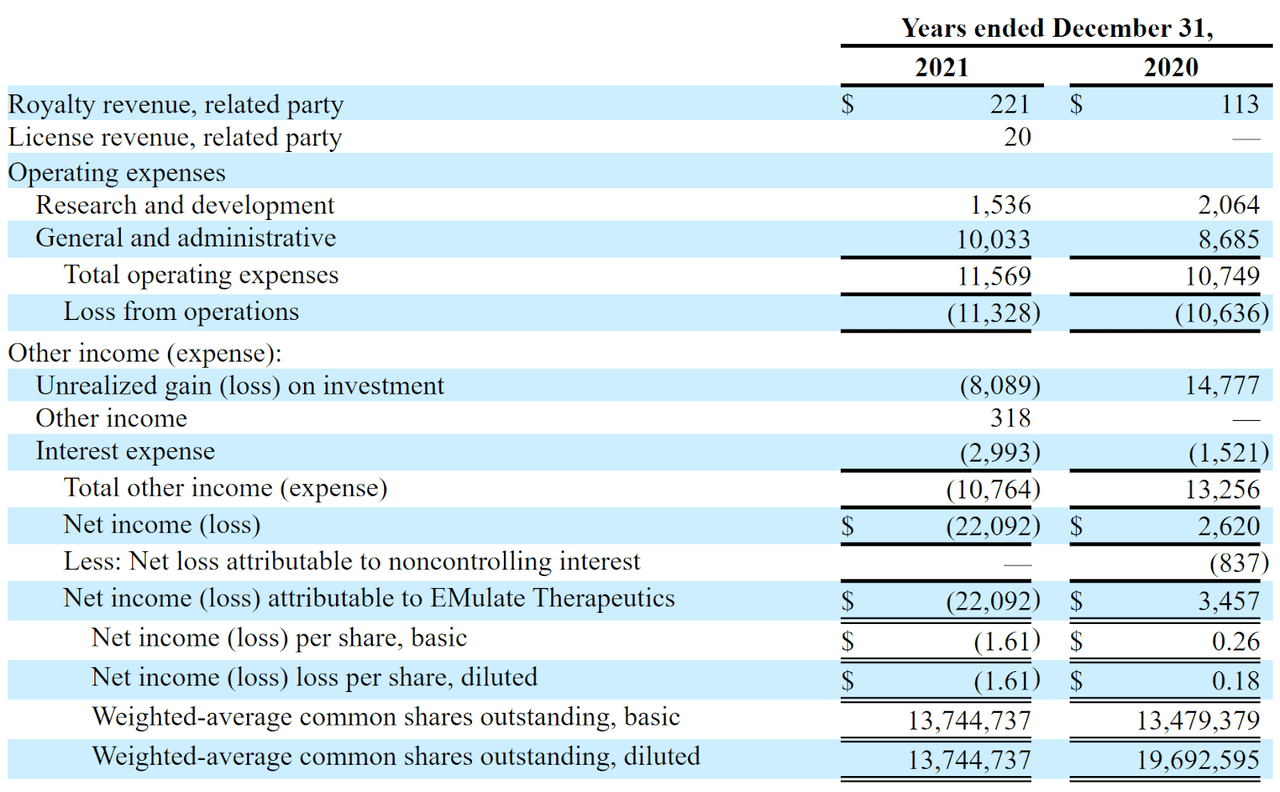

The firm’s recent financial results are typical of a development-stage life science firm, with little in the way of revenue and significant R&D and G&A costs associated with its product development efforts.

Below are the company’s financial results for the past two calendar years:

Statement Of Operations (SEC)

As of September 30, 2022, the company had $11,000 in cash and $27.2 million in total liabilities. (Unaudited, interim)

EMulate’s IPO Details

EMTX intends to sell 2.5 million shares of common stock at a proposed midpoint price of $5.00 per share for gross proceeds of approximately $12.5 million, not including the sale of customary underwriter options.

No existing or potentially new shareholders have indicated an interest in purchasing shares at the IPO price.

Assuming a successful IPO at the midpoint of the proposed price range, the company’s enterprise value at IPO (excluding underwriter options) would approximate $75.6 million.

The float to outstanding shares ratio (excluding underwriter options) will be approximately 16.3%. A figure under 10% is generally considered a ‘low float’ stock which can be subject to significant price volatility.

Per the firm’s most recent regulatory filing, it plans to use the net proceeds as follows:

We intend to use the net proceeds of this Offering primarily for general corporate purposes, including clinical trials, preclinical research and development, technology development, outstanding accounts payable and working capital.

(Source – SEC)

Management’s presentation of the company roadshow is not available.

Regarding outstanding legal proceedings, management stated,

“pursuant to an arbitrated settlement in 2016 with two former employees and founders of the Company regarding the severance amounts payable under their respective employment agreements, we are obligated for the payment of a severance amount to these individuals. Payment of the full amount has to date been deferred pursuant to a series of agreements, and we remain current in our scheduled payment obligations under those deferral agreements. The unpaid aggregate severance amount as of December 31, 2022 is approximately $5.7 million and interest accrued as of December 31, 2022 is approximately $0.4 million. We are in discussions with the former employees and founders. The ultimate outcome of this matter cannot be predicted at this time.” (Source – SEC.)

The sole listed bookrunner of the IPO is EF Hutton.

Commentary About EMulate Therapeutics

EMTX is seeking U.S. public market capital to fund its continued product development and corporate plans.

The firm’s lead candidate has “produced substantially similar molecular effects as the paclitaxel drug at the cellular level,” although management is not currently in trials, and it is unclear what approvals the company has received from the FDA for trial purposes.

The market opportunities for PEMF treatment options for various indications is potentially large but is difficult to quantify as to their applicability to the firm’s treatment approach.

Management has not disclosed any major pharma or medical device firm collaboration relationships.

The company’s investor syndicate doesn’t include any well-known institutional life science venture capital firms or strategic medical device investors.

EF Hutton is the lead underwriter, and IPOs led by the firm over the last 12-month period have generated an average return of negative (67.2%) since their IPO. This is a bottom-tier performance for all significant underwriters during the period.

As for valuation, EMulate Therapeutics, Inc. management is asking investors to pay an enterprise value at IPO of approximately $75.6 million, well below the typical range for a mainline, institutional venture capital-backed biopharma.

Management’s strategy is to pursue treatment approvals for a wide range of conditions, so the firm has set up subsidiaries in specific areas to better enable partnering and financing options.

I favor a more focused approach, as it is difficult and time-consuming enough to get one device for one indication approved and successfully commercialized, let alone ten of them.

Also, the “$5.00” IPO share price is typical of many current thinly-capitalized IPO candidates, so the EMulate Therapeutics, Inc. IPO is likely aimed at retail investors rather than institutional investors.

My outlook on the IPO is on Hold.

Expected IPO Pricing Date: To be announced

Be the first to comment