designer491

Introduction

So far, 2022 was a tough year for investors. The S&P 500 entered a bear market, tech stocks that did well in the past got clubbed, and even bonds did extremely poorly. The worst part is that this could last well into 2023 as macroeconomic challenges are persistent.

The good news is that conservative dividend growth investors did rather well this year. Investors in conservative and low-volatility dividend growth stocks outperformed the market and were able to put money to work at more attractive valuations.

In this article, I want to briefly talk about the macro environment and the need to buy quality dividend growth stocks. Moreover, as the title suggests, I want to give investors three of the highest-quality dividend stocks money can buy.

Especially in light of lower stock prices, I frequently get asked where people should put their money. Often, we’re talking about $10-$20K portfolios.

To incorporate this, I put $10,000 in the title. It’s a value a lot of retail investors start with. It’s also the first target of many, as $10,000 in a single stock is a great start to an investing journey.

Hence, the focus of this article is on quality. We’re talking about three stocks that I would even recommend to investors with very limited financial market knowledge. Three stocks that won’t keep people up at night. Three stocks with fantastic balance sheets, decent yields, and great dividend growth.

In other words, three of the best stocks money can buy.

So, let’s get to it!

Market Turmoil & Nobody Has A Clue

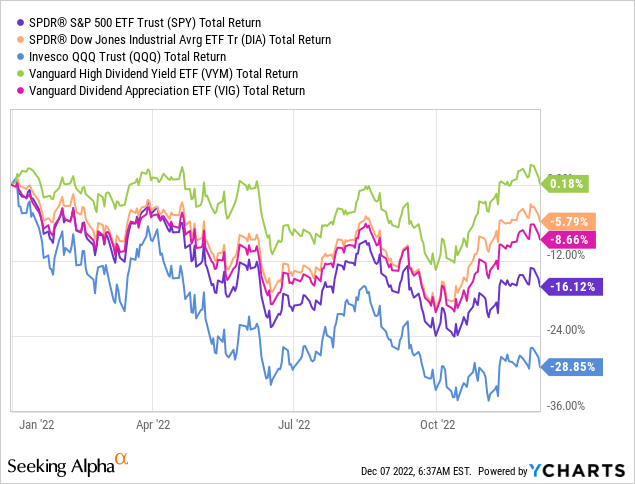

This year, the S&P 500 is down 16% including dividends. That’s up from a 24% loss in October and well above the -29% performance of the tech-heavy ETF (QQQ). What’s interesting is that the Dow Jones is down less than 6%. High-yield dividend stocks are in positive territory!

This year showed the difference between growth and value stocks. A higher-rate environment, slower economic growth, and an aggressive Fed have caused investors to turn their backs on so-called growth stocks.

While a lot of growth stocks that do poorly in 2022 did very well in the past, we’re once again finding out what investing is all about: buying stocks that do well in bull markets, while protecting investors against the downside in bear markets.

Once you find stocks that have that ability, you’re all set.

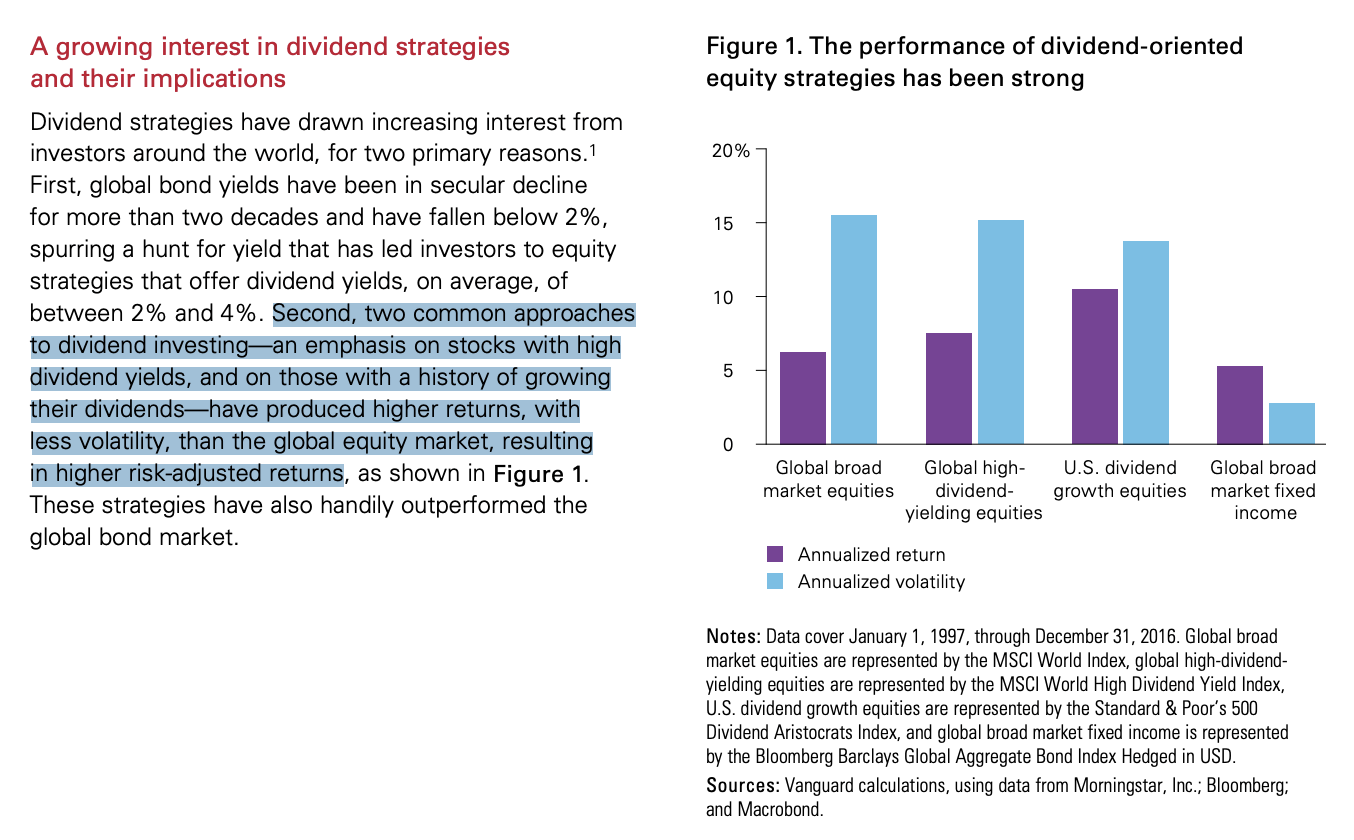

Vanguard hit the nail on the head as it made the case that buying quality dividend growth means having the ability to generate higher returns than the market with less volatility. The chart on the right side of the screenshot below shows that dividend growth equities perform better than the market with lower volatility. Even high-yield stocks do better than the market.

Vanguard

Essentially, it’s all about doing better than the market during bear markets. After all, protecting the downside when things go south is a perfect basis for long-term outperformance, even if stocks fail to beat the market during every bull market.

While nobody knows how a stock will perform during a bear market, we can put the odds in our favor if we focus on stocks with strong business models, healthy balance sheets, and a high likelihood of dividend growth, even when economic growth disappoints.

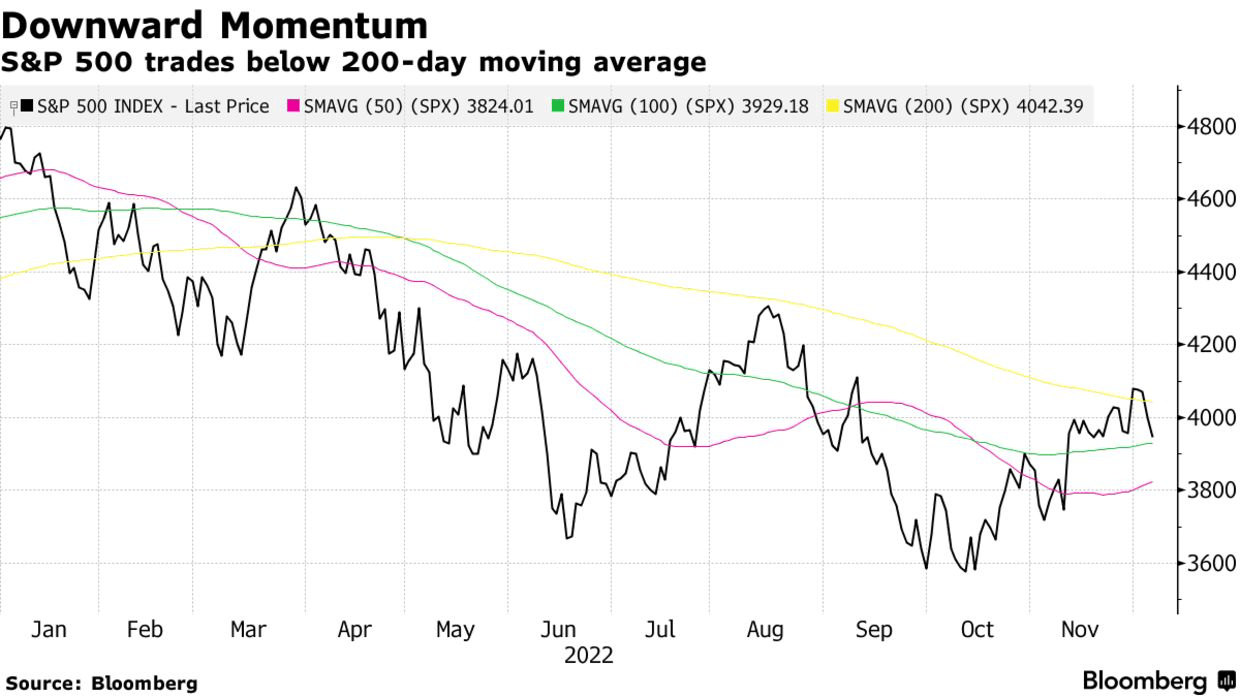

Now, before I tell you which stocks I want people to focus on, let’s take a quick look ahead. We’re once again in a situation of high uncertainty. Inflation is high, economic growth is rapidly falling, and the Fed is still eager to continue its hiking cycle to normalize the aforementioned inflation.

We’re now seeing cracks in the housing market, labor market, and everything else that supported the bull market since 2009.

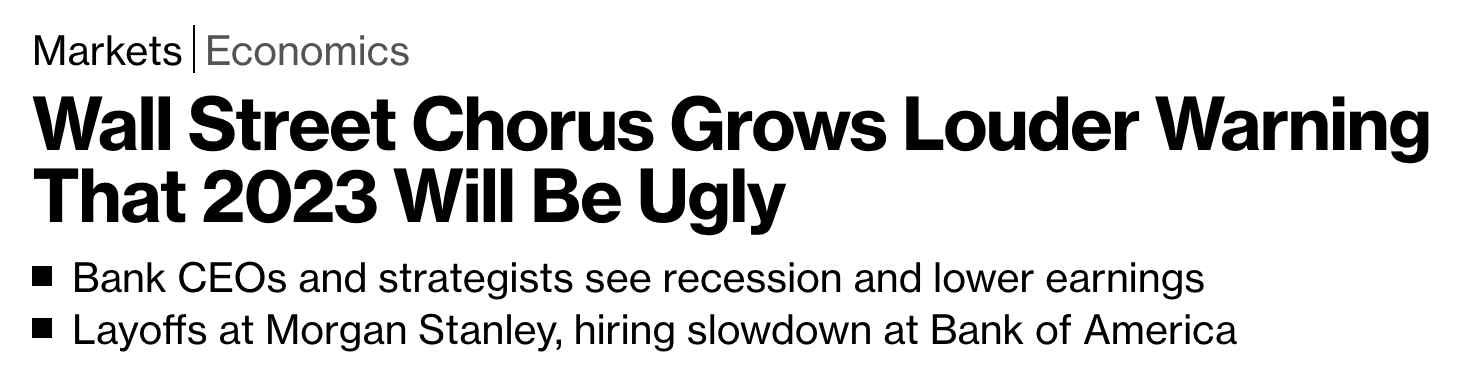

Bloomberg

According to Bloomberg:

From Goldman Sachs Group Inc.’s David Solomon caution that the economy faces “bumpy times ahead,” to JPMorgan Chase & Co.’s Jamie Dimon grimmer view that this would be a “mild to hard recession,” and Morgan Stanley Wealth Management’s Lisa Shalett, who told Bloomberg Television that corporations are facing a “rude awakening” on earnings, the messages have become increasingly dire.

While I’m not necessarily bearish (especially not on a long-term basis), my thesis is that stocks need to weaken more to price in economic risks and to eventually force the Fed to pivot.

Bloomberg

However, there’s one major risk: nobody can predict what the market is up to.

On the one side, we have experts calling for a bottom as the Fed funds rate may be close to peaking. On the other side, we have experts who make the case that we’re not out of the woods yet.

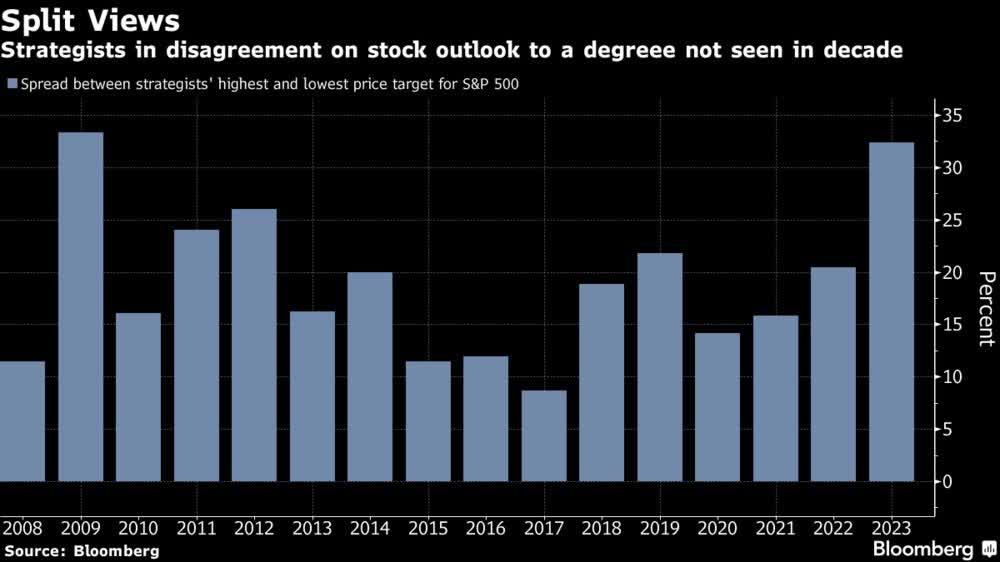

The result is that the lowest and highest S&P 500 expectations for 2023 haven’t been this far apart since 2009.

Bloomberg

2023 could get bad. However, it could also be an average year if the Fed pivots and maybe even restarts QE – depending on how bad things get.

In other words, my strategy remains the same. I buy the stocks on my watchlist whenever I like the valuation. If stocks continue to fall, I average down. The only thing I changed is that my savings rate is higher and my cash reserves are higher. *If* things get ugly, I will be able to invest more.

With all of this in mind, let me show you the three stocks that I would recommend to everyone as they come with safety, dividends, and a high likelihood of long-term outperformance.

Stocks that will allow everyone ranging from mom-and-pop investors to financial heavyweights to beat the market and earn an income along the way.

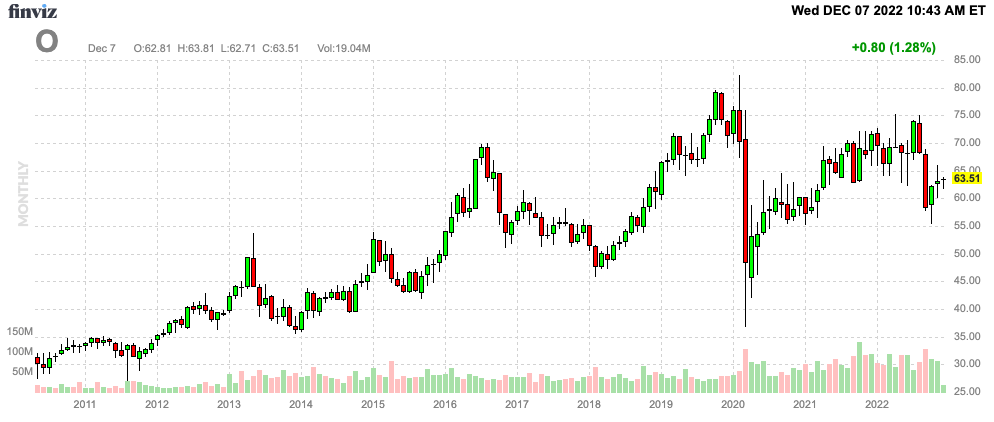

1. Realty Income (O) – 4.7% Yield

FINVIZ

Realty Income isn’t a part of my portfolio as I never focused on high-yield investments. However, due to tax reasons, I increasingly need to incorporate high-yield. And that’s not an issue as the market offers us some tremendous opportunities in that space. Realty Income is one of them.

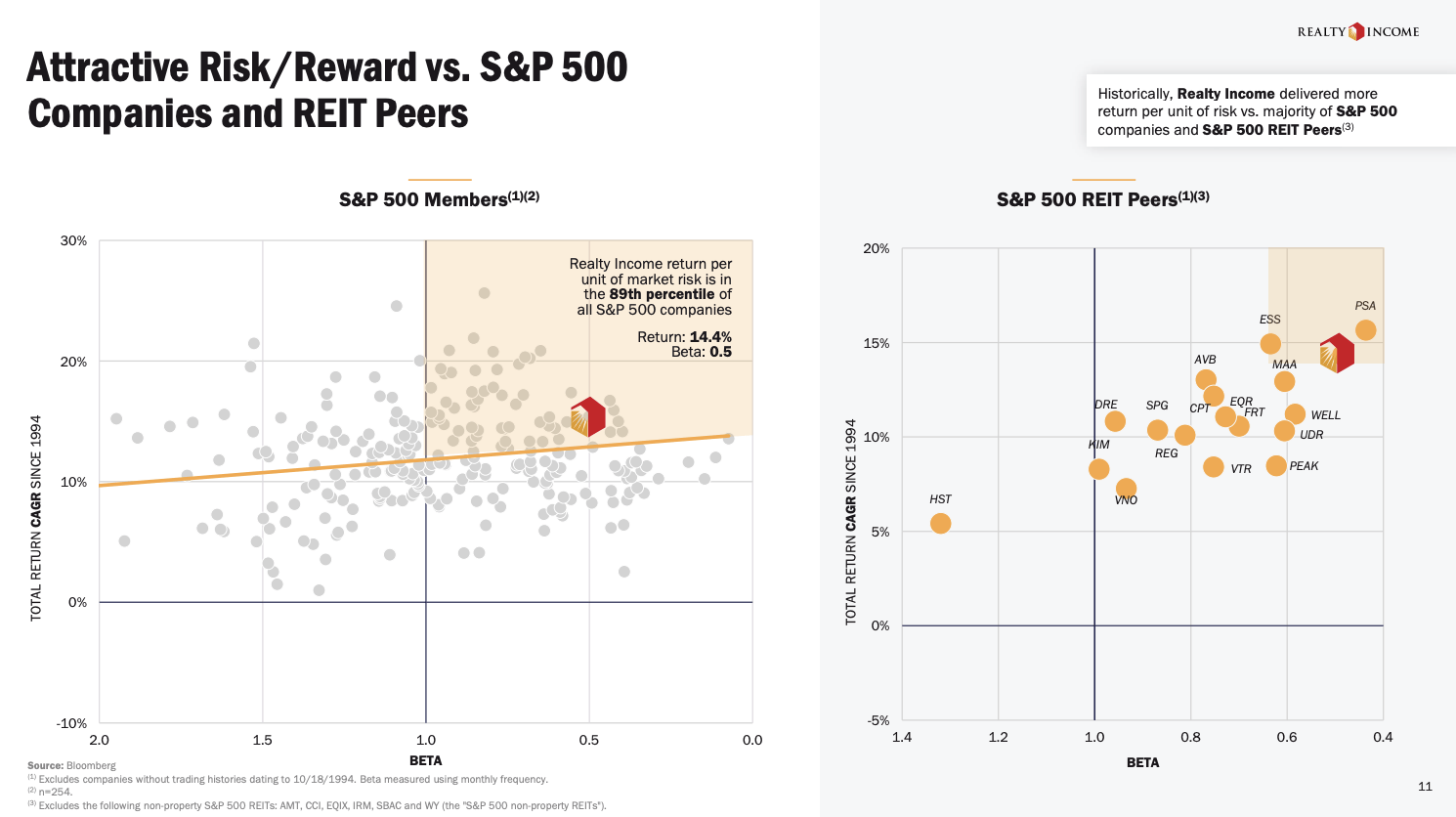

Known as the monthly dividend company, Realty Income is one of the top 5 global REITs. The company is a dividend aristocrat with 14.6% compounding annual total returns since 1994. Since 1994, the company has hiked its dividend by 4.4% per year.

The company has had a compounded annual return of 14.4% since 1994. On top of that, it has a beta of just 0.5. This means the company is performing extremely well on a volatility-adjusted basis. The company is also performing extremely well compared to its REIT peers. It has subdued volatility and high long-term returns.

Realty Income

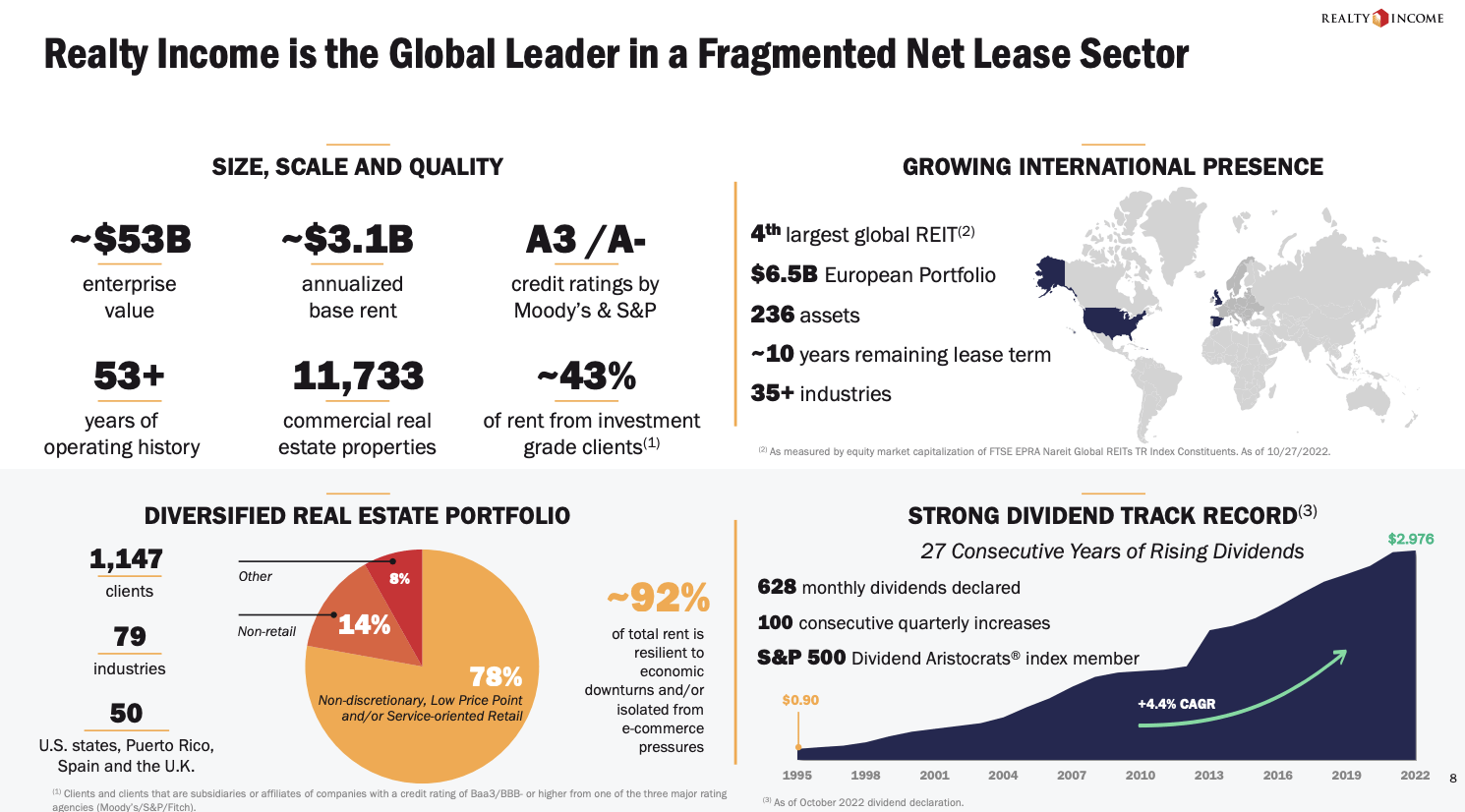

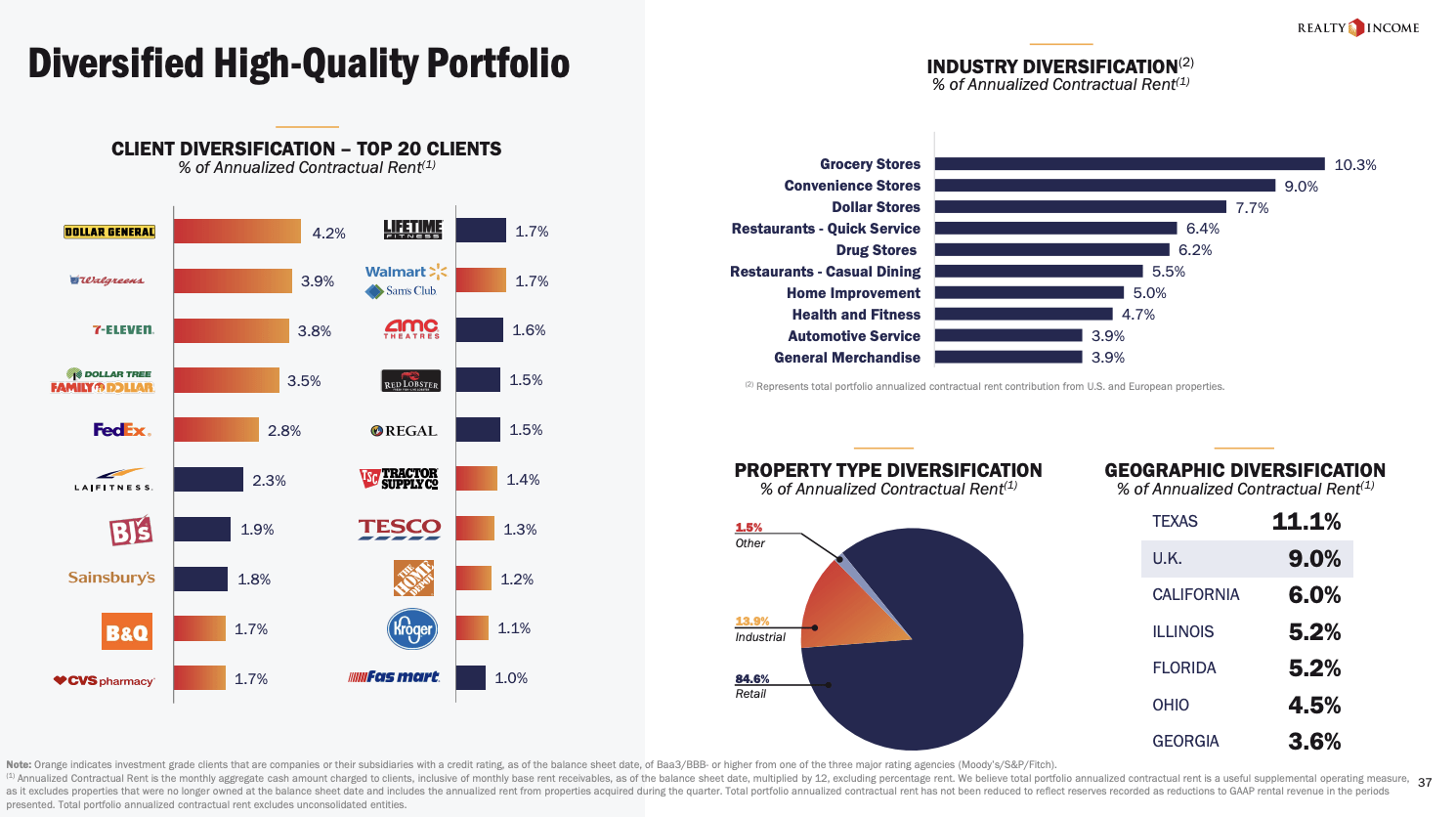

Moreover, the company is one of the few REITs with an A-rated balance sheet. 43% of its 1,147 clients are investment-grade. It owns assets in 79 different industries and 50 states.

Realty Income

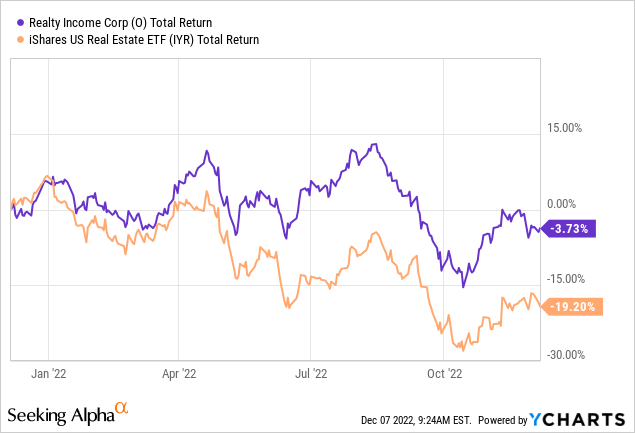

While a high-interest environment is providing some headwinds for REITs, Realty Income benefits from a strong sale and leaseback trend. Large companies are outsourcing real estate. For example, Realty Income is purchasing the Encore Boston Harbor Resort and Casino for $1.7 billion at a 5.9% cash cap rate from Wynn Resorts (WYNN). It’s the first casino property in Realty Income’s portfolio.

It also shows that the company is willing to go well beyond traditional retail assets as it diversifies its portfolio wherever sale and leaseback opportunities present themselves.

Moreover, one of the reasons why I wasn’t a huge fan of O in the past is the fact that there is tremendous pressure on smaller stores. The pandemic made that so much worse. However, Realty Income has top-tier tenants and high exposure in defensive sectors that rely on brick-and-mortar stores. That’s extremely important.

Realty Income

Moreover, there’s another reason why the O ticker is outperforming its peers.

The company’s balance sheet is stellar. As I already mentioned, it’s A-rated by both Moody’s and S&P Global. The company’s leverage ratio is just 5.2x, it has 95% unsecured debt, 88% fixed-rate debt, and an average of 6.3 years of maturity for notes and bonds.

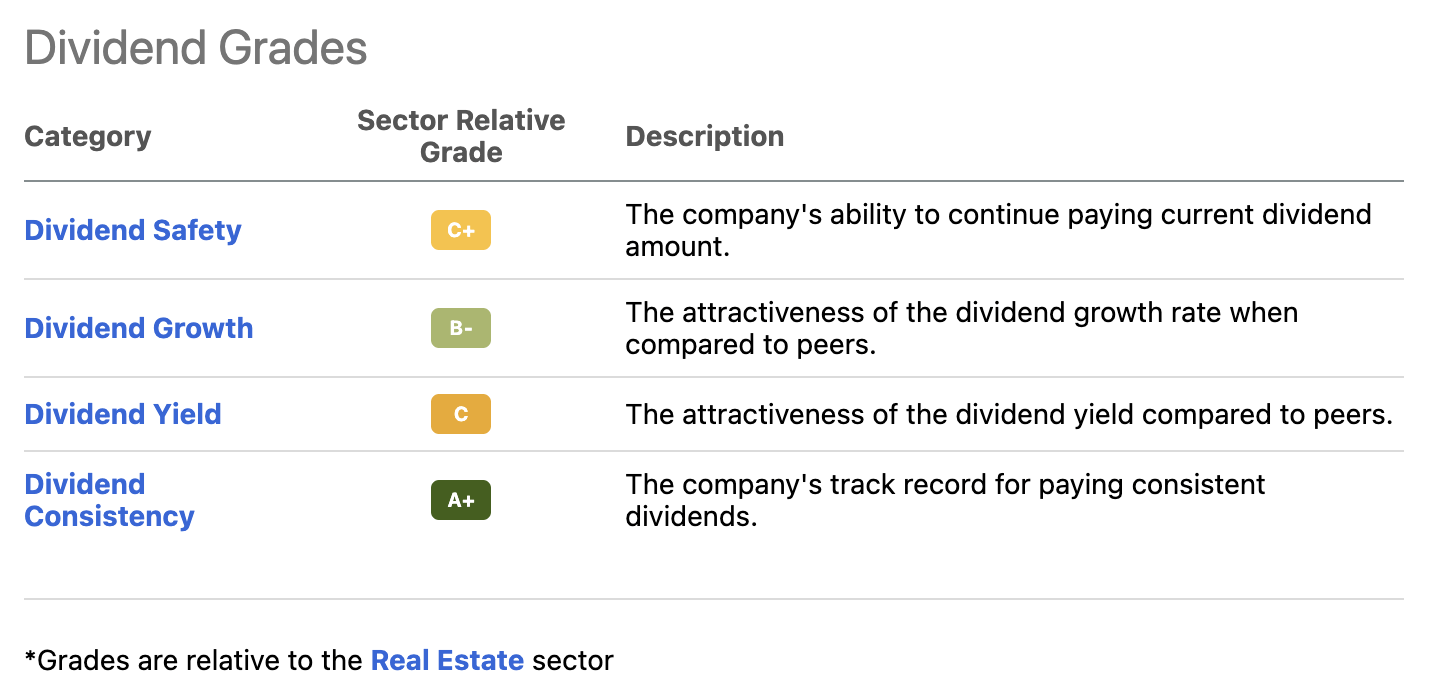

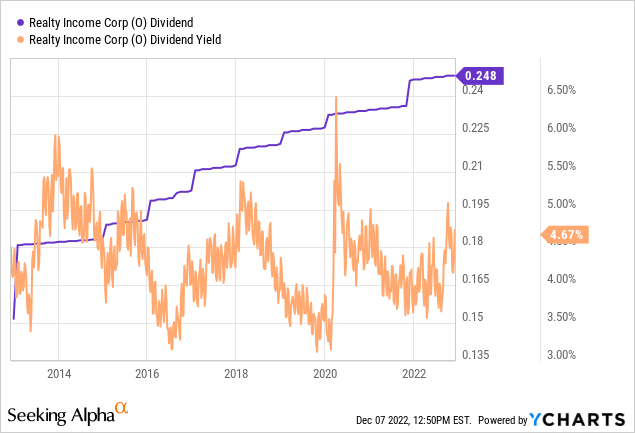

Moreover, the company has a decent Seeking Alpha dividend scorecard. The company is yielding 4.7% based on a $0.248 monthly (per share) dividend.

Seeking Alpha

Over the past ten years, the average annual dividend growth rate was 5.6%. That’s above the long-term average of 4.4% since its 1994 IPO.

Now, onto number two.

2. Procter & Gamble (PG) – 2.4% Yield

FINVIZ

If we want a stellar business model, a decent yield, sustainable dividend growth, a healthy balance sheet, and long-term outperforming capital gains, there’s no way around P&G.

Headquartered in Cincinnati, Ohio, Procter & Gamble is one of the oldest consumer stocks in the world. Founded in 1837, the company has become a $359 billion market cap heavyweight.

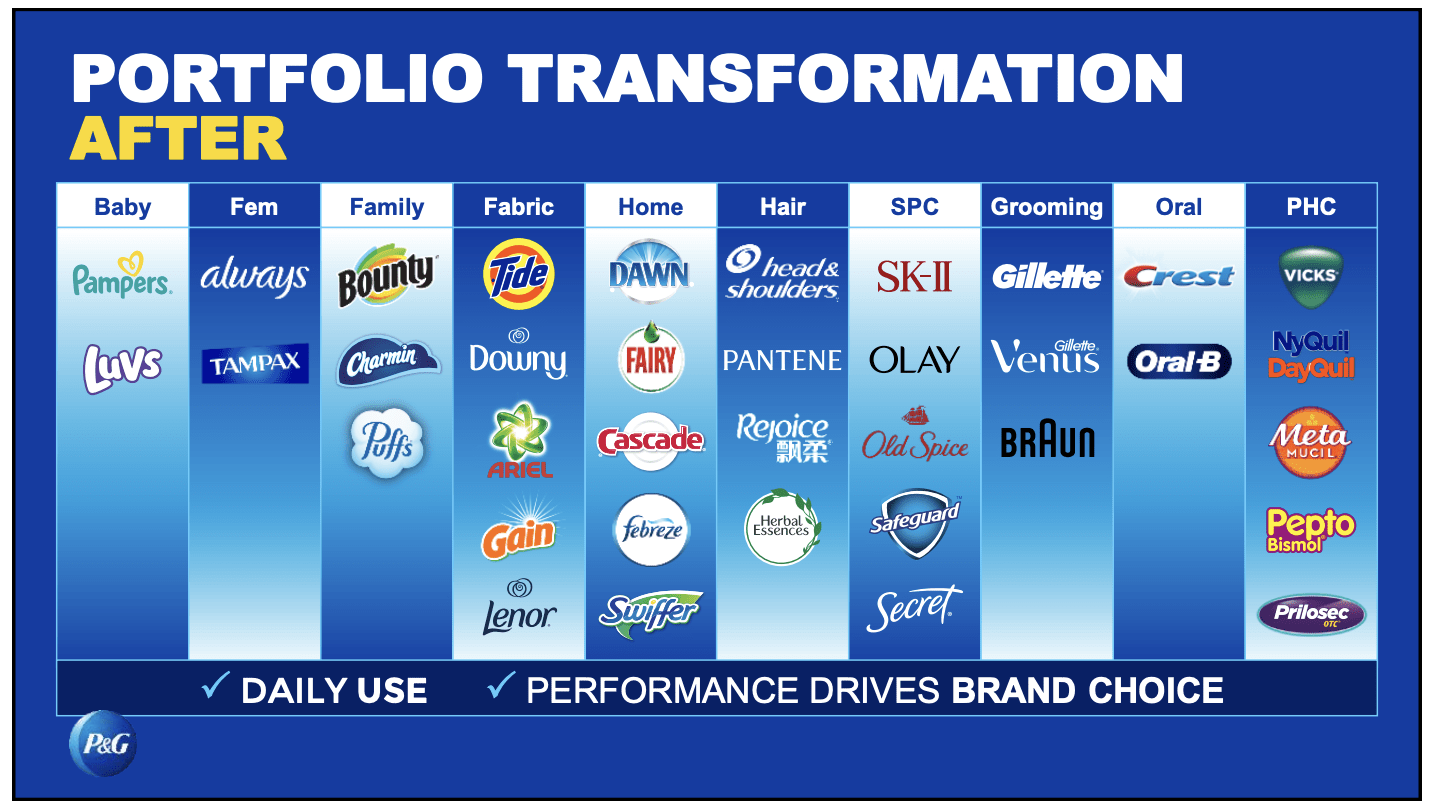

The company owns some of the world’s most famous consumer brands in various categories ranging from Baby products like Papers to Tide fabric softener and Oral-B oral care.

Procter & Gamble

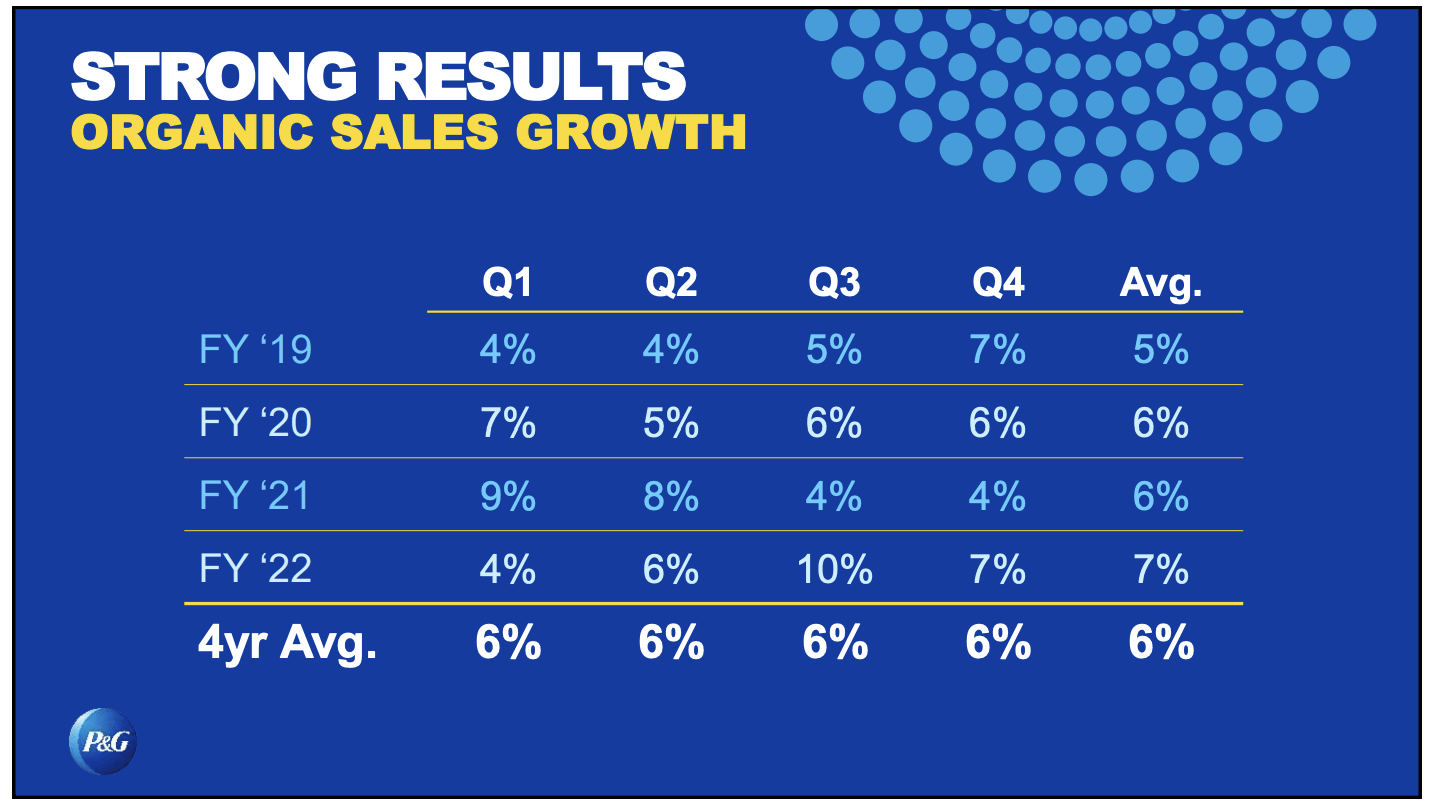

These products have provided the company with 3% annual organic volume growth over the past four years. Including pricing, organic sales growth was 6% per year. Higher margins provided 9% annual core EPS growth during this period, which is impressive.

Procter & Gamble

The company hasn’t reported a single quarter of negative organic sales growth since the start of the data in the table above.

Even in the current environment of high inflation and poor consumer health, the company is doing well. In its 2023 fiscal year, the company is expected to generate between 0% and 4% in core EPS growth. Organic sales growth is expected to be at least 3%. Adjusted for currency translations, core EPS is estimated to be up at least 9%.

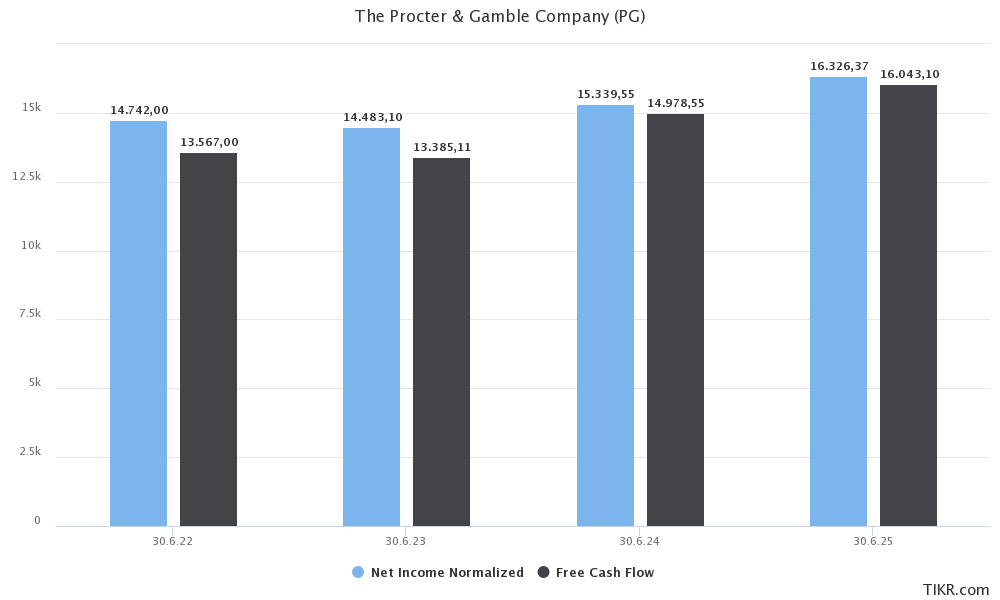

Moreover, cash generation is strong. Free cash flow is consistently close to 100% of net income. Moreover, free cash flow is relatively high. In its 2024 fiscal year, the company is expected to do $15.0 billion in free cash flow. That would translate to a 4.2% free cash flow yield (based on its $359 billion market cap).

TIKR.com

The company has paid a dividend for 132 years. It has 66 consecutive years of dividend increases. Over the past 10 years, total dividends and stock repurchases were $141 billion.

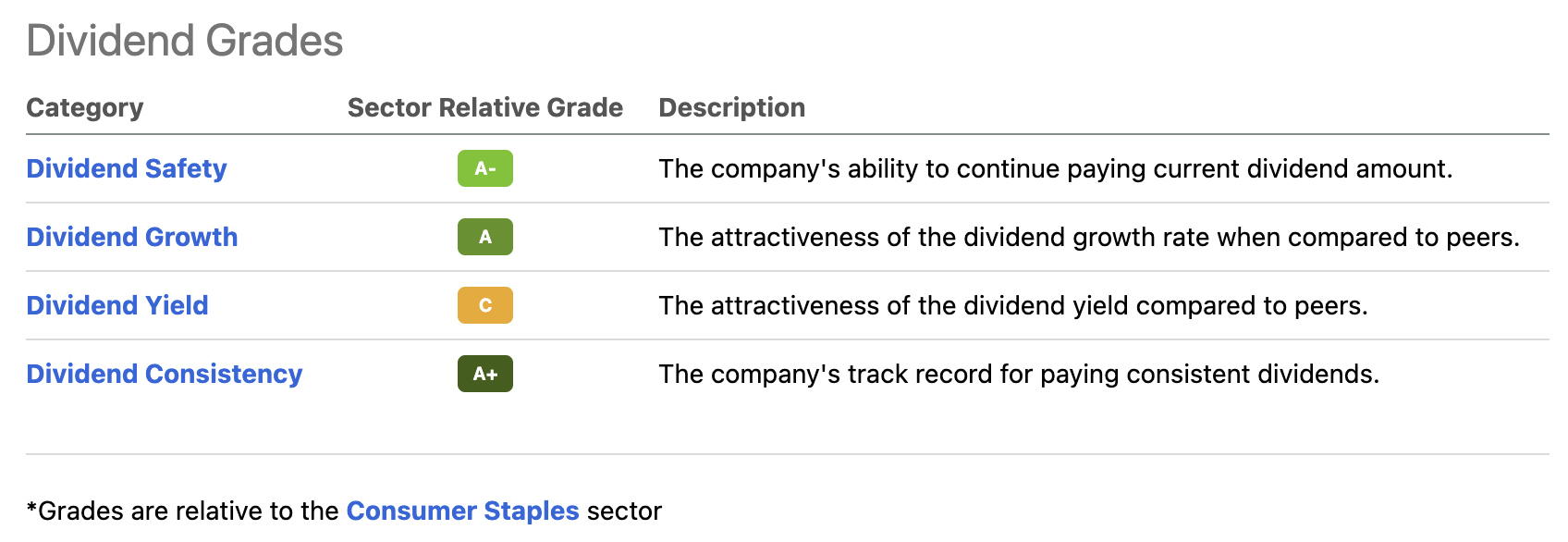

With that said, the company’s Seeking Alpha dividend scorecard is highly attractive. Only the dividend yield scores somewhat low as the company is compared to the consumer staples sector. This sector is filled with slow-growing high-yielding stocks. I prefer growth over a high yield – in most cases.

Seeking Alpha

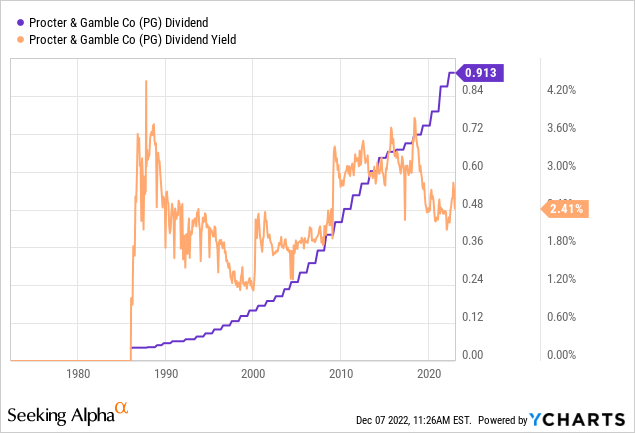

In the case of P&G, we’re dealing with a quarterly dividend of $0.9133 per share. This translates to a yield of 2.4%. This yield is below pre-pandemic levels.

Over the past ten years, the dividend has been hiked by 5.0% per year. Over the past three years, the average has grown to 6.9%.

The most recent hike was announced in April of this year when management hiked by 5.0%.

The cash flow payout ratio is 50%. Net debt is expected to end the current fiscal year at $25.8 billion. That’s just 1.2x EBITDA.

As a result of its business model, high free cash flow, and low debt load, the company has an Aa3 credit rating. That’s higher than some developed nations.

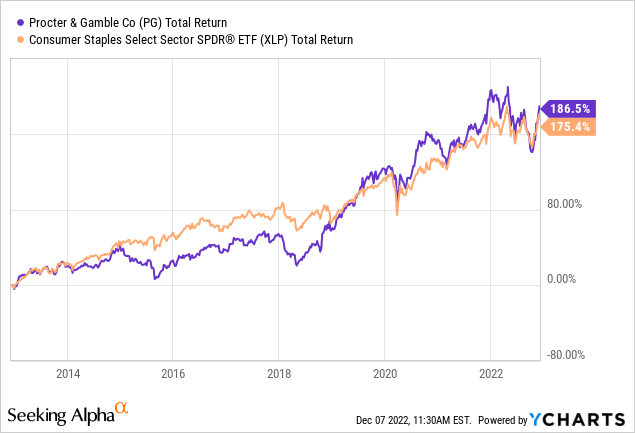

Moreover, the company has outperformed the Consumer Staples ETF (XLP) by more than 10 points over the past ten years.

Before we discuss P&G’s volatility-adjusted performance, let us look at stock number three. It’s a stock I’ve owned since 2020.

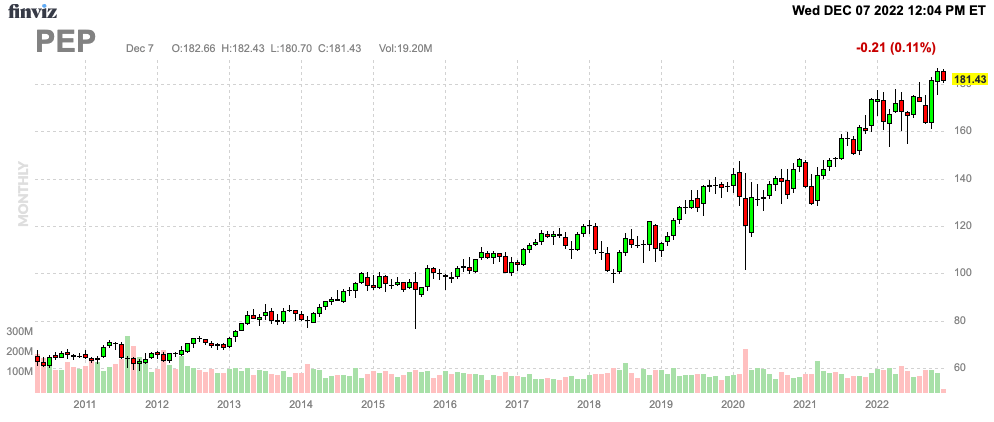

3. PepsiCo (PEP) – 2.5% Yield

FINVIZ

PepsiCo is one of the first five stocks I bought when I started my dividend growth portfolio in 2020. With a market cap of $253 billion, it’s another giant in the consumer staples sector. However, unlike Procter & Gamble, it produces beverages and snacks.

In September, I wrote an article titled “2 All-Weather Dividend Stocks You Should Own”.

One of them was PepsiCo because of its pricing power and ability to deliver consistent value. Despite high inflation, poor consumer health, and an aggressive Fed, PEP shares are up almost 5% year-to-date.

The company has an A+ credit rating and a business model that enjoys pricing power.

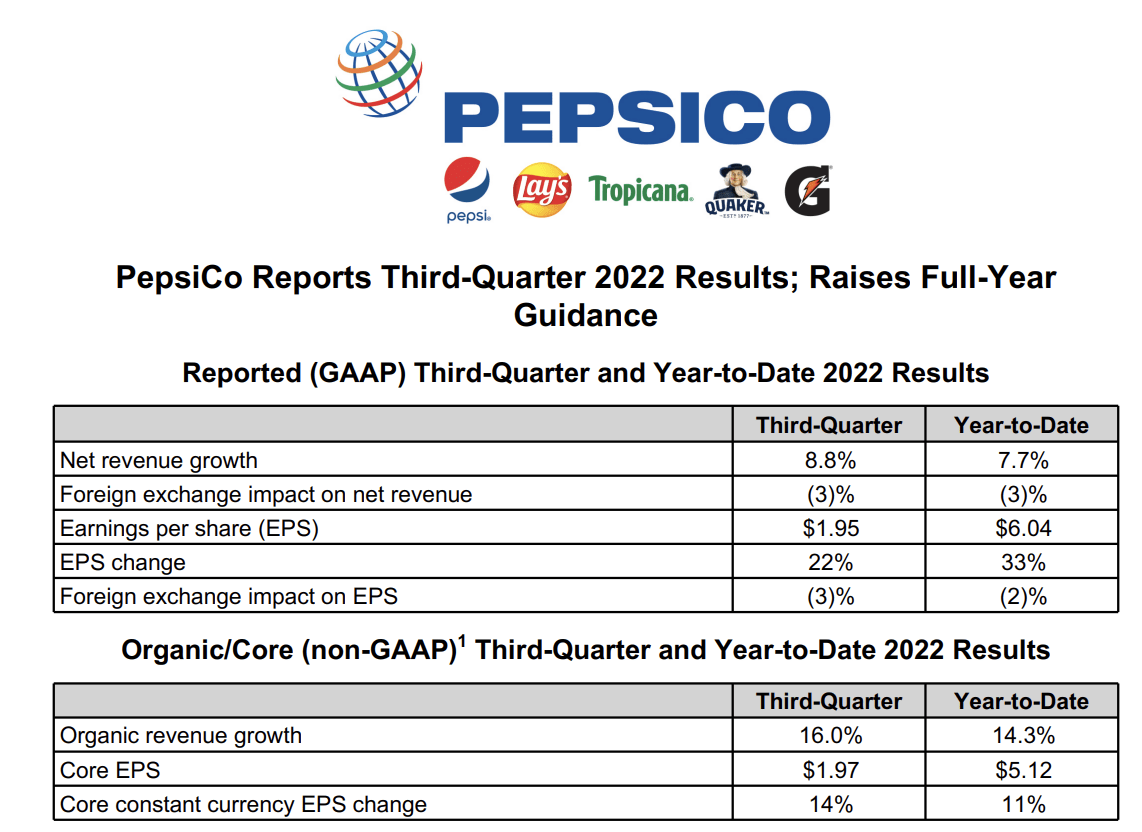

PepsiCo, which owns brands like Lay’s, Tropicana, Pepsi, and Quaker, generated 16.0% organic revenue growth in the third quarter. Frito-Lay North America saw 20% organic sales growth. The company had no segment with negative organic revenue growth.

PepsiCo

A big part of revenue growth was pricing. Volume growth in convenience foods was down 1.5% while beverage volumes were up 3%. In Europe, food volumes were down 5%, while beverage volumes were down 8%. This is the result of shoppers prioritizing groceries over snacks. For now, pricing is able to offset these headwinds. Competition is not a major issue as the company has top-tier brands that generic products can barely compete with.

Moreover, pricing was able to offset high operating costs. On a constant currency basis, the company reported 14% higher EPS growth in the third quarter.

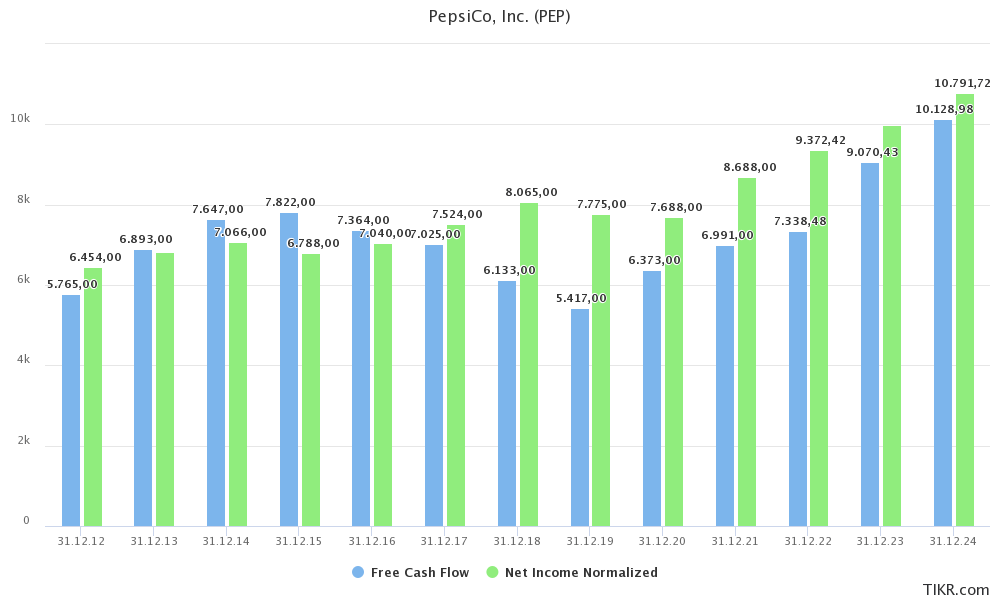

Between 2012 and 2024E, the company is growing net income by 4.4%. EPS growth is higher at 5.6%. The difference is caused by share buybacks. Compounded annual free cash flow growth was 4.8% during this period.

TIKR.com

Note that the numbers above include the years prior to 2020 when PepsiCo was struggling with profitability.

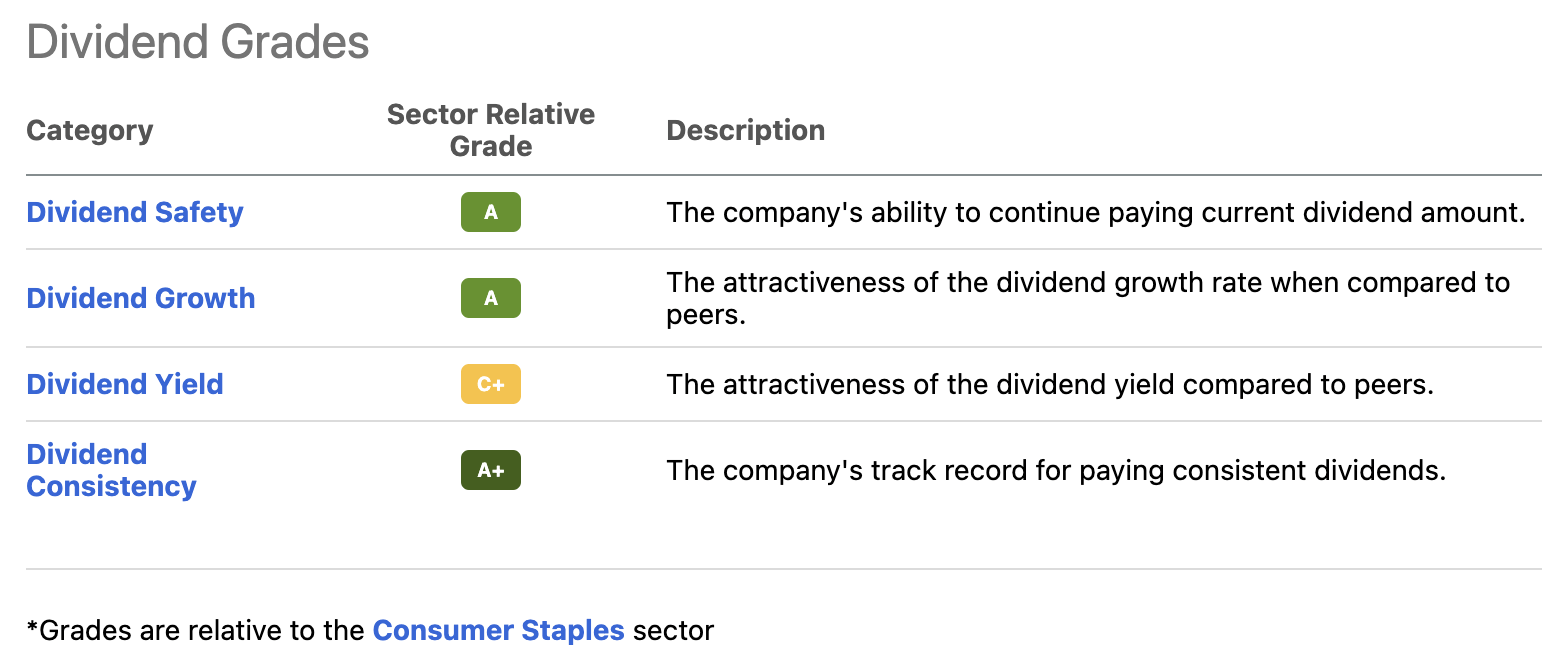

Thanks to its financial performance, PepsiCo has a fantastic Seeking Alpha dividend scorecard. It scores high on safety, growth, and consistency. Just like the first two stocks, PepsiCo is a dividend aristocrat.

Seeking Alpha

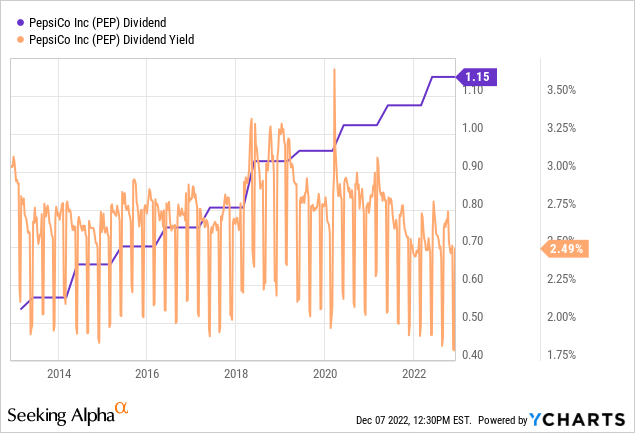

The company pays a $1.15 dividend per quarter. This translates to a 2.5% yield. Over the past ten years, the average annual dividend growth rate was 7.8%. That’s a very decent number.

The most recent hike was announced on May 3, when management hiked by 7.0%.

Now, let’s put all three in a row.

Takeaway

In this article, we discussed stocks that have it all. Great business models, decent yields, satisfying and consistent dividend growth, healthy balance sheets, and more.

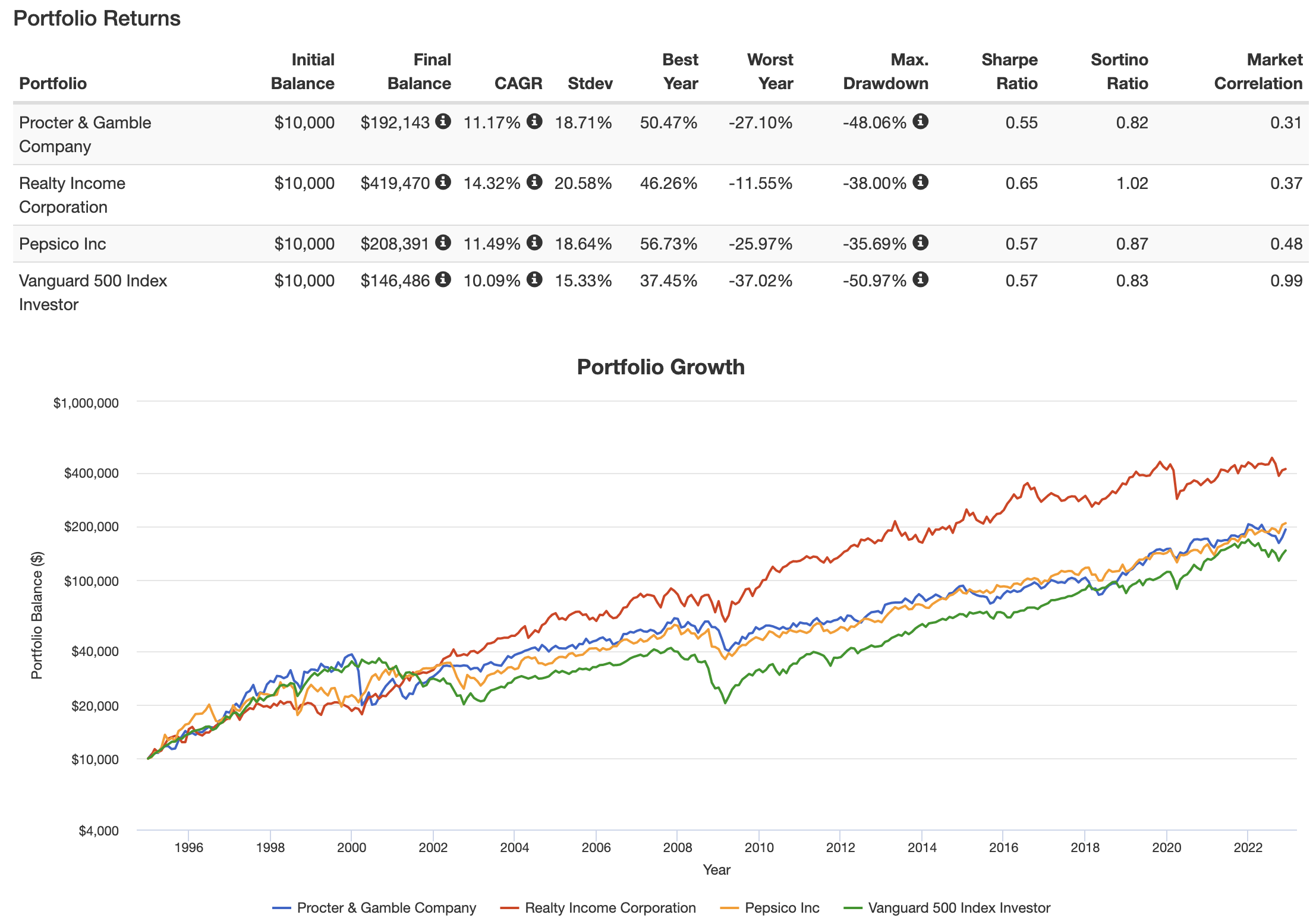

According to the theories we discussed in the first half of this article, all three stocks should do really well compared to the market. That is indeed what we are observing. All three stocks have outperformed the market on a consistent basis. Max drawdowns were less severe, annual compounding returns were higher, and volatility was subdued.

Portfolio Visualizer

All things considered, the three stocks in this article are stocks that I would recommend to inexperienced investors (excluding ETFs). All three stocks are great places to put $10K to start a dividend growth portfolio.

Moreover, all stocks pay a decent yield, which adds to the attractiveness of the selection. After all, investors want some “juice”. Especially inexperienced investors.

Also, these stocks are great as investors can continue to pour money into them on weakness. That’s why I did not go with cyclical stocks in this article. Most cyclical stocks come with some aspect of timing, which is NOT what starting investors should worry about.

That said, I’m looking to add Realty Income to my portfolio in 2023. The stock is a great fit for my portfolio and a great source of high yield. And, as the title says, I will start with $10K and rapidly add to that down the road.

(Dis)agree? Let me know in the comments!

Be the first to comment