Spencer Platt/Getty Images News

Investors should buy shares of The Bank of New York BNY Mellon (NYSE:BK).

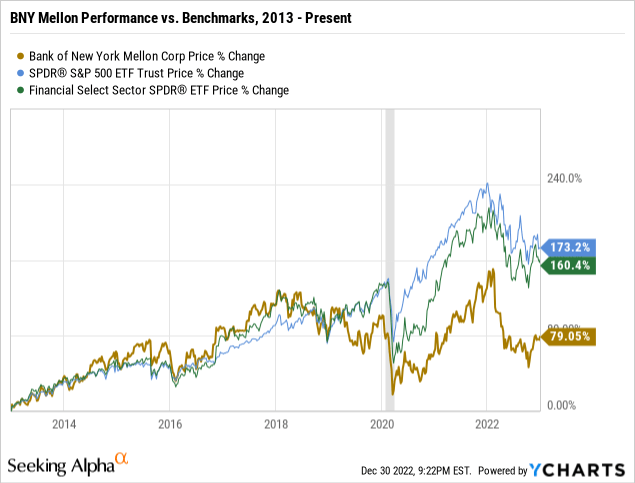

BNY Mellon presents an interesting value opportunity for investors. The stock struggled throughout 2022, down 22% YTD. Moreover, Q2 and Q3 earnings misses have further hampered the stock’s performance. BNY Mellon has also substantially underperformed the S&P 500 since 2013. The question is merely whether or not BNY Mellon has fallen out of favor or is fundamentally unsound.

BNY Mellon Background

BNY Mellon traces its roots back to Alexander Hamilton’s Bank of New York. Founded in 1784, the Bank of New York has engaged in a series of firsts. It made the first loan to the U.S. government in 1789, was the first company traded on the New York Stock Exchange in 1792 and created the first trust in the United States in 1804.

In late 2006, the Bank of New York announced a merger with Mellon Financial Corporation. Mellon Financial, founded in 1870, became a major financial institution under the leadership of industry titan Andrew Mellon. Today, BNY Mellon is led by Chief Executive Robin Vince. The firm employs over 51,000 people, and has been lauded as one of the world’s safest banks.

BNY Mellon has a multitude of strategic buyers that influence the performance of its stock. Institutional shareholders currently own 85% of the firm’s outstanding shares. Vanguard, Berkshire Hathaway (BRK.B), Dodge & Cox, and BlackRock (BLK) are the largest of these institutional shareholders. With respect to insider ownership, there have not been any major insider buys since early 2021.

Business Description

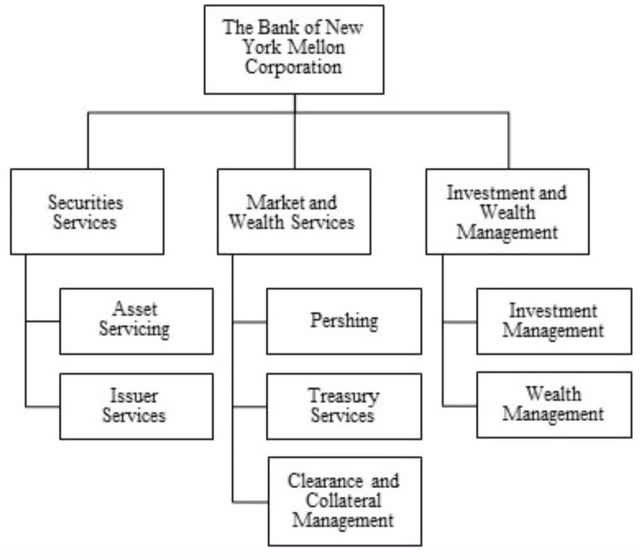

BNY Mellon operates through three business segments: Securities Services, Market and Wealth Services, and Investment and Wealth Management. Securities Services accounted for $2.07 billion of BNY Mellon’s Q3 2022 revenue, Market and Wealth Services accounted for $1.37 billion, and Investment and Wealth Management accounted for $862 million. The below chart represents an in-depth overview of BNY Mellon’s business segments.

BNY Mellon Q3 2022 10Q filing

BNY Mellon is currently the world’s largest custodian bank with over $43 trillion in assets under custody. Custodian banks are concerned with the protection of client assets. Despite finding its niche as a custodian, BNY Mellon also has a sizable presence in the asset management industry. The firm has over $1 trillion in assets under management, and has developed a notable line of low expense exchange traded funds. BNY Mellon also has a global presence in 35 countries.

Industry Leaders

I found it challenging to find quality comparable companies. State Street Corporation (STT) struck me as a good comparable due to its sizable asset management business and SPDR ETF lineup. State Street also has over $40 trillion in assets under custody. However, outside of State Street, JPMorgan Chase (JPM) seemed to be the best remaining comparable company. JP Morgan has a substantial asset servicing business as well as a prominent wealth management subsidiary. However, it also offers many additional services including commercial banking and investment banking. The firm is not the best comparable to BNY Mellon and State Street, but I wanted to illustrate how BNY Mellon matches up to one of the world’s top banks.

|

Ticker |

Founded |

Headquarters |

Employees |

Market Cap |

Fortune Global 500 |

|

BK |

1784 |

New York, USA |

51,100 |

$36.23B |

266 |

| STT | 1792 | Boston, USA | 41,354 | $28.75B | 379 |

| JPM | 1799 | New York, USA | 288,474 | $393.34B | 63 |

Relative Valuation

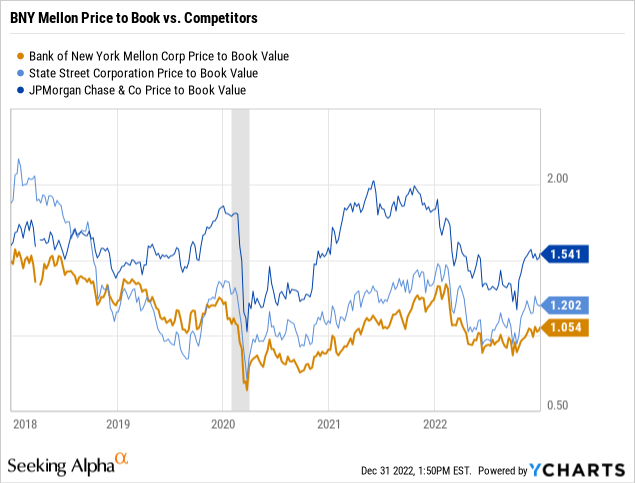

Price to book value is a key metric to consider when valuing financial services companies. Since many of these firm’s assets are carried on the balance sheet at their fair values, book value is a reliable valuation indicator. I selected a relatively small peer group to provide context to BNY Mellon’s price to book ratio of 1.05. Investors can currently buy the firm’s assets at “par,” meaning that a $45 cash outlay for one BNY Mellon share provides the investor with approximately $43 of the firm’s assets. Moreover, price to book ratio can be an indicator of the market’s growth expectations of a financial services firm. A lower ratio indicates lower growth expectations.

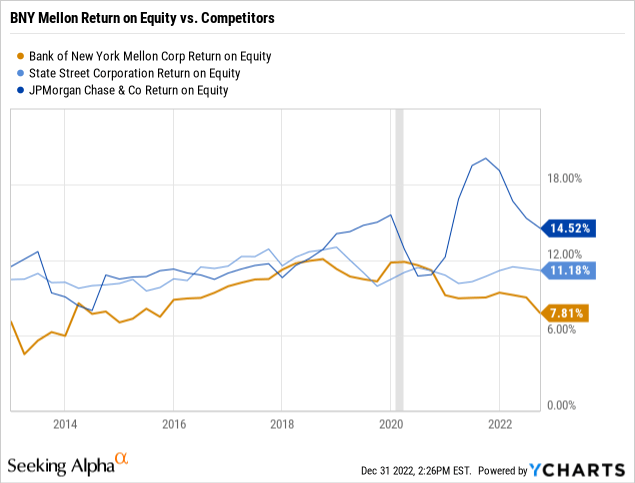

Return on equity is another indicator of a financial services firm’s growth potential. A higher return on equity indicates a more efficient use of a firm’s existing equity financing. BNY Mellon currently lags both JP Morgan and State Street with respect to ROE.

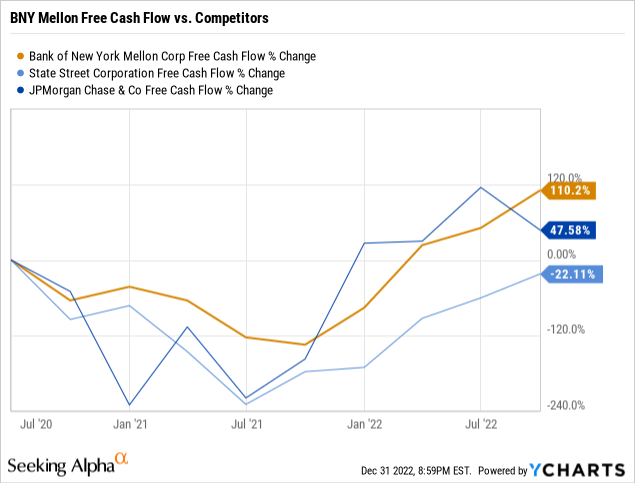

In absolute terms, JP Morgan has much more free cash flow than either State Street or BNY Mellon. However, BNY Mellon still has over $10 billion of free cash flow. Moreover, the firm has experienced immense growth in free cash flow since the COVID-19 pandemic of March 2020.

DDM Valuation

It is challenging to find an appropriate valuation model, especially when analyzing a financial services firm. I have used discounted cash flow models for many of my past analyses, but I think that a dividend discount model will work best for BNY Mellon.

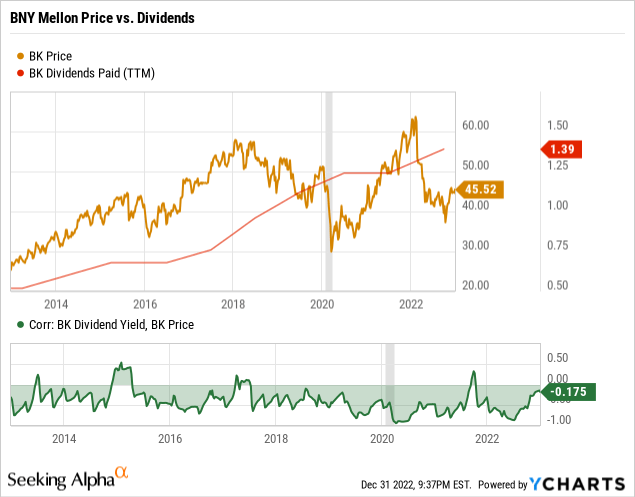

Over the past decade, BNY Mellon has implemented a steady dividend increase from $0.15 per share to $0.37 per share. The firm’s ability to pay a steady dividend has been a key support for its stock price. All else constant, BNY Mellon’s ability to keep its dividend strong during the COVID-19 financial decline helped support the stock’s subsequent resurgence. Moreover, there has been a slight negative correlation between BNY Mellon’s dividend yield and its price since 2013. This should be considered when considering the efficacy of analyzing BNY Mellon’s value based on its dividend payments alone. However, due to the unpredictable nature of the firm’s earnings, it seems more reasonable to focus on its stable dividend payments as proxies for the firm’s cash flows.

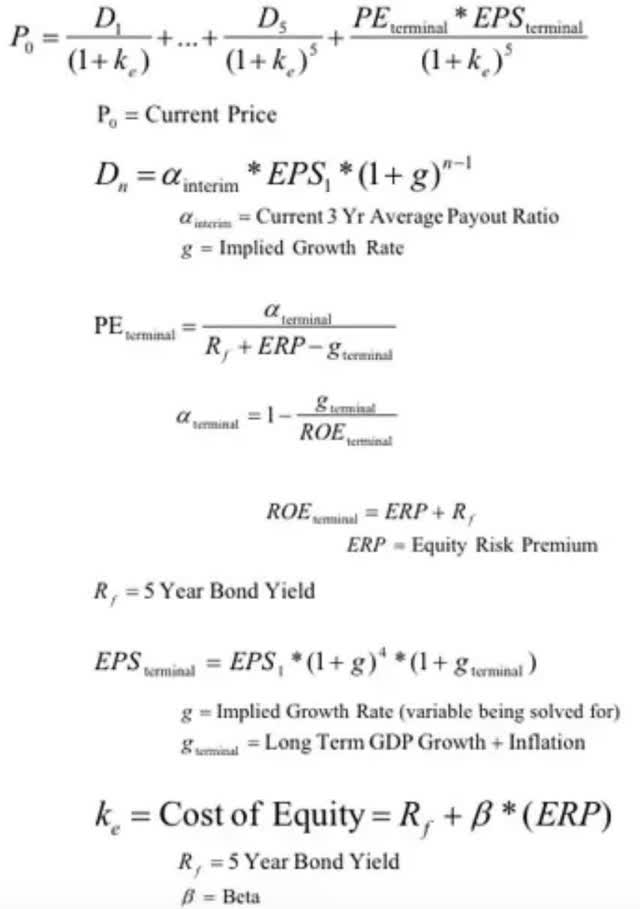

I have included a chart below describing the various assumptions to be used in BNY Mellon’s dividend discount model. Each dividend payment is assumed to be the respective value to be received by shareholders during the fourth quarter of each fiscal year. Moreover, I assumed that BNY Mellon has to briefly pause dividend payments between 2023 and 2024 due to a global financial downturn.

BNY Mellon’s dividend discount model was calculated using a formula from an old Goldman Sachs (GS) pitch deck. I did not include a traditional sensitivity analysis, and instead opted for an overly conservative scenario with limited dividend growth and limited terminal growth. These calculations yielded an intrinsic value of $59.38 per share.

Goldman Sachs Global Economics, Commodities, and Strategy Research

| Inputs | Values |

| D1 (2023) | 0.39 |

| D2 (2024) | 0.39 |

| D3 (2025) | 0.41 |

| D4 (2026) | 0.43 |

| D5 (2027) | 0.45 |

| k | 8.37% |

| g | 1.25% |

| PE (Terminal) | 12.5 |

| EPS (Terminal) | 7.1 |

| Implied Value | $59.38 |

Risk Factors

BNY Mellon has a history of being one of the safer global banks due to the firm’s solid performance during the 2008 Global Financial Crisis. However, the past is often not a great predictor of the future, and the nature of BNY Mellon’s business as a custodian and asset manager makes risk management paramount to the firm’s long term well-being.

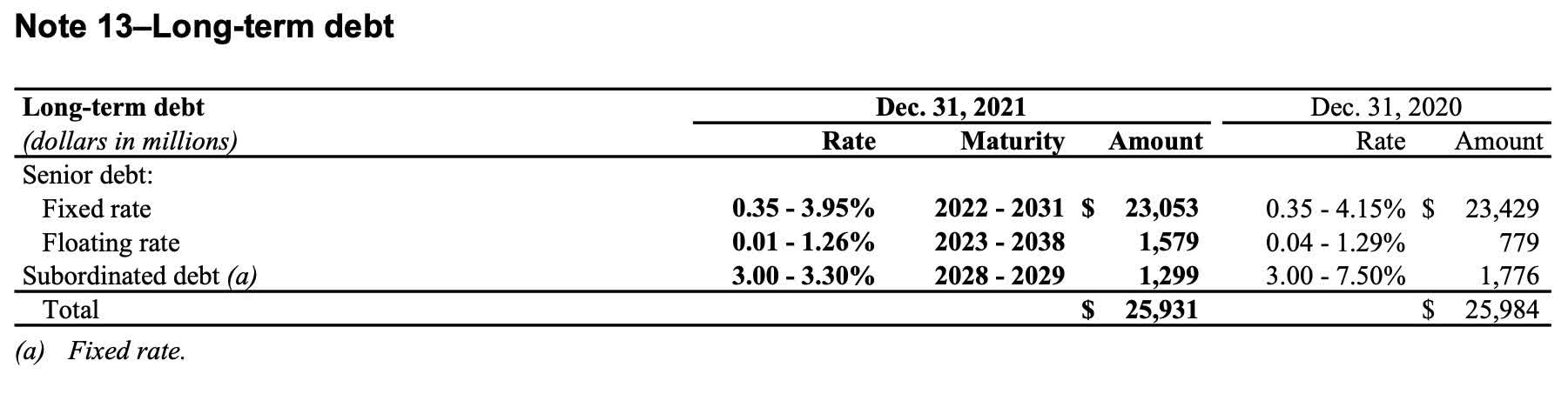

Maintaining a quality credit rating is a key component of BNY Mellon’s long-term success. The firm currently maintains an A1 rating from Moody’s, an A rating from S&P, and an AA- rating from Fitch. Moreover, in addition to its quality credit rating, BNY Mellon has made use of limited long-term debt. Its capital structure is not overly risky at the present moment, but investors must be mindful of future changes.

BNY Mellon 2021 10K Filing

BNY Mellon also faces a host of risks indicative of the financial services industry. Issues such as regulatory capital requirements and employee retention are key to BNY Mellon’s future success. Morningstar’s (MORN) Sustainalytics has identified BNY Mellon’s ESG risk to be moderate. Moreover, Sustainalytics has identified the firm’s management to be strong.

Investment Summary

BNY Mellon’s allure lies mostly in how its Q4 2022 and Q1 2023 earnings reports play out. The firm is strong with respect to its free cash flow, price to earnings ratio, price to book ratio, and capital structure. However, there are also a multitude of other securities across every industry that fit these criteria. My goal is to provide exceptional investment opportunities, and I think that BNY Mellon fits the definition of an out of favor value stock. It is often overlooked as a custodian bank, and is certainly not a “sexy” pick. Investors should not expect to get rich off BNY Mellon, but its proven ability to return value to shareholders via dividends and share repurchases makes it a low-risk play.

Be the first to comment