akinbostanci/E+ via Getty Images

Investment thesis

Invesco Mortgage Capital Inc. (NYSE:IVR) has been struggling to grow its book value per share in the past 2 years and this trend is very likely to continue in the future. I do not expect great first-quarter results because in January and in February IVR experienced an almost 15% decline in its book value per share due to yield flattening and mortgage interest rate pressure. IVR has a whopping 18.46% dividend yield but all the risks are too much for this attractive yield for me to buy-in. I believe the current share price is justified and in addition, there is a 10% short interest in IVR which also makes me cautious.

Business Model

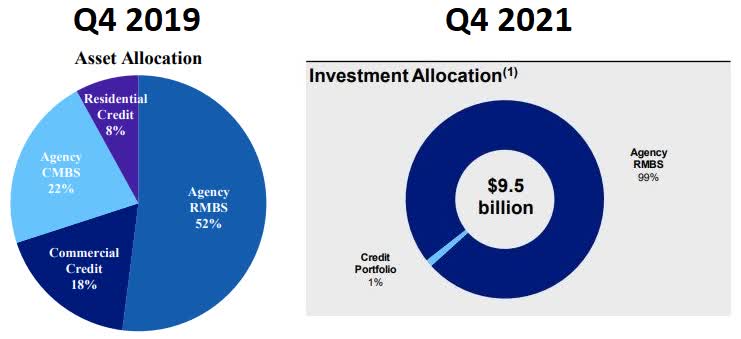

Invesco Mortgage Capital operates as a mortgage real estate investment trust that primarily focuses on investing in, financing, and managing mortgage-backed securities and other mortgage-related assets. The company has a simple investment portfolio because it invests almost entirely in Agency RMBS (99% of its portfolio consists of agency RMBS). This is a massive change compared to 2 years ago when the company had a wide variety of assets with a relatively large credit portfolio of 26% and also invested heavily in Agency CMBS. All of this is gone by the end of 2021 and only a tiny 1% of the credit portfolio remained.

Q4 2019 and Q4 2021 Presentations

Financials & Earnings

Q4 results and Q1 expectations

IVR reported relatively bad quarterly results. This is mainly due to the Fed’s more hawkish policy stance. Because of that, the yield curve flattened and IVR faced more challenging external market conditions. The book value per share declined by 10.46% compared to Q3 2021 from $3.25 per share to $2.91. The decline is more dramatic on a year-on-year basis, -24.61%. The company also reported a net loss per share of $0.23 and a negative economic return. And in January 2022 this trend continued.

“Our book value declined an additional 9% during January as the spread widening in Agency mortgages accelerated and the payouts on specified pool collateral collapsed amid much higher mortgage rates – John Anzalone – CEO.” In addition, in February they experienced another 5-6% decline in book value so based on these numbers I am not expecting great first-quarter results from IVR. The company will report its first-quarter earnings on May 3, 2022. The recent interest rate rise could help IVR’s second quarterly results in 2022 and the further planned interest rate rises will affect the mortgage rates as well. In the second half of 2022, the slowing prepayment rates can support the earnings power of IVR.

Valuation

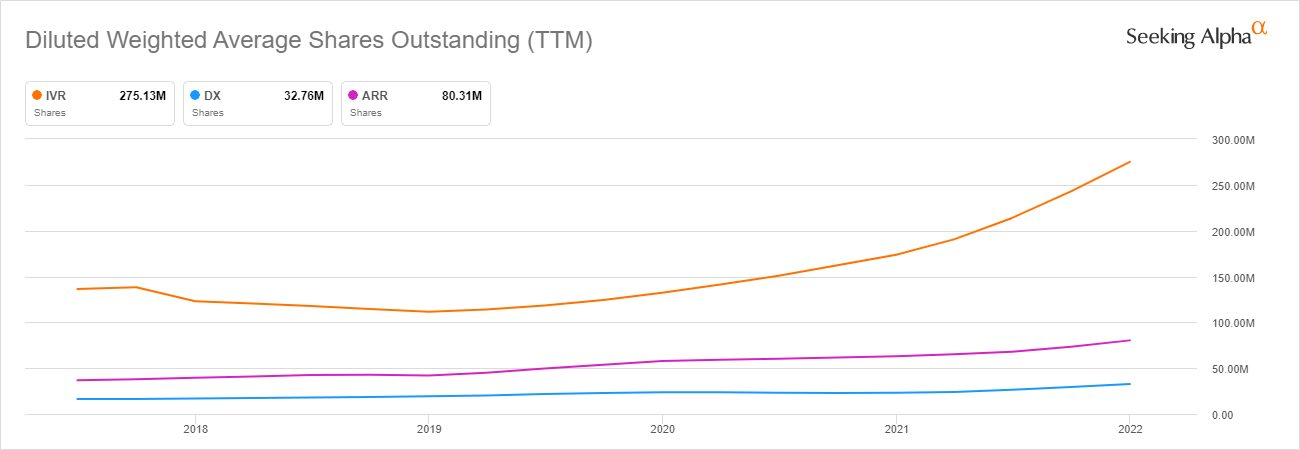

The management has been issuing shares aggressively to finance its operations. In just 2 short years they almost doubled the number of diluted weighted average shares. You can say that all mREITs do the same however, the scale is different. Two of IVR’s closest peers based on market cap also issued new shares but Dynex Capital Inc. (DX) only increased the number of shares by approximately 40% while Armour Residential REIT Inc (ARR) increased its shares outstanding by approximately 35%.

Seeking Alpha

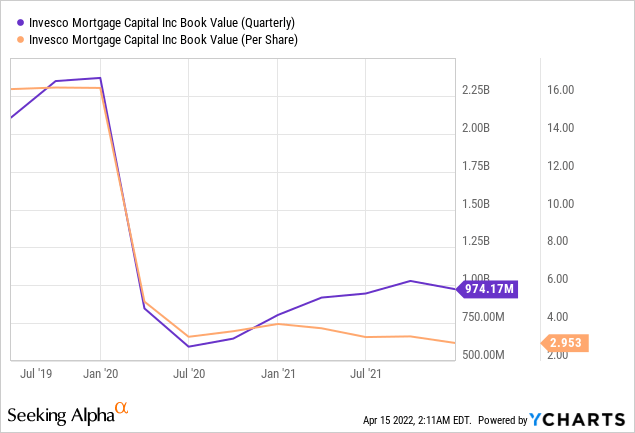

IVR’s book value per share is slowly but steadily declining. The management could increase IVR’s book value after the COVID-19 crisis but it is far from pre-pandemic levels and now it seems almost impossible to return to those levels. I am not sure I want to become an owner in a company that destroys shareholder value over time and its book value per share is steadily on the decline.

Company-specific Risks

The COVID-19 pandemic has created an uncertain and volatile interest rate environment and general fixed income patterns have deviated widely from historical trends. In just a short period we saw an inflation spike and the Fed is struggling to tackle it fast without risking a recession. In addition, IVR experienced historically larger spreads to benchmark rates in the repurchase markets for certain target assets and the availability of repurchase financing has been limited.

Rising interest rates generally reduce the demand for mortgage loans because of the higher cost of borrowing. A reduction in the volume of mortgage loans originated will likely affect the volume of target assets available to IVR, which could adversely affect the management’s ability to acquire assets that satisfy the investment objectives. Rising interest rates could make IVR unable to acquire a sufficient volume of their target assets with a yield that is above the borrowing cost, which will eventually affect the bottom line and IVR could struggle to generate income and maintain its current dividend.

My take on IVR’s dividend

Current dividend

IVR currently has a whopping 18.46% dividend yield. The company has been paying consecutive dividends for 12 years and has no consecutive dividend growth history because of the pandemic. IVR experienced a rapid decline in its assets and the management had no other choice but to cut the dividend drastically from $0.5 per share to $0.02 in 2020. At the moment IVR pays $0.09 per share quarterly.

Future sustainability

When I see dividend yields over 15% that always makes me think about sustainability. According to my experience dividend yields over 15% are unsustainable in the long term nine out of ten times. IVR has a payout ratio close to 100%, in some quarters well over 100%. Analysts’ estimates suggest that there could be no dividend increase in 2022 but a possible cut in 2023. The management might be forced to cut the dividend because of interest income struggles from the current $0.09 to $0.085 per share according to the consensus yield.

The table is created by the author. All figures are from the company’s financial statements and SA Earnings Estimates.

Final thoughts

IVR offers an 18+% dividend yield but that’s a trap in my opinion. The current share price is justified and the company has been destroying shareholder value in recent years by issuing a ton of new common shares to finance its operations. Because of this, the book value per share has been declining and I see no evidence that it will change shortly. This is the main reason why I am neutral on IVR at the moment.

Be the first to comment