-Oxford-

Intuit (NASDAQ:INTU) is a global software company that is on a mission to “power prosperity around the world”. In order to accomplish this, the company has created/acquired a number of market-leading financial products such as Quickbooks for SMB accounting and CreditKarma. Intuit has a strong leadership position and in Q1,FY23 the company beat both top and bottom-line estimates for growth. In this post, I’m going to break down its business model, financials, and valuation, let’s dive in.

Business Model & Strategy

Intuit is a financial software company that focuses on helping small-medium-sized businesses [SMBs] streamline their financials and accounting. Traditionally, keeping track of SMB financials is a messy and time-consuming process that involves multiple spreadsheets, folders of receipts, etc. Intuit solves this problem with its iconic “QuickBooks” platform. This product streamlines the entire accounting process and offers intuitive dashboards to help users run their businesses more effectively.

Quickbooks (Intuit/Quickbooks website)

The easy-to-use nature of the solution means it is no surprise that the QuickBooks product is the leading digital accounting platform for SMBs and has ~82% market share in the United States of America. Its product is deployed via multiple versions with its most popular being “QuickBooks Online”, followed by a desktop deployment, and a self-employed version. Over time management’s strategy is to convert all of its legacy desktop users to its more scalable cloud-native platform. In general, larger organizations that have used the platform for a long time are the ones that are slow to switch.

Intuit’s management realized a long time ago that a great way to scale the business is by helping small businesses and individuals with other financial solutions from getting loans to managing taxes and even marketing. This strategy led to Intuit acquiring Turbotax in 1993 and developing it into the easy-to-use tax solution it is today. In 2009, Intuit also acquired Mint.com for $171 million. This product offers an intuitive personal financial app and access to credit cards etc.

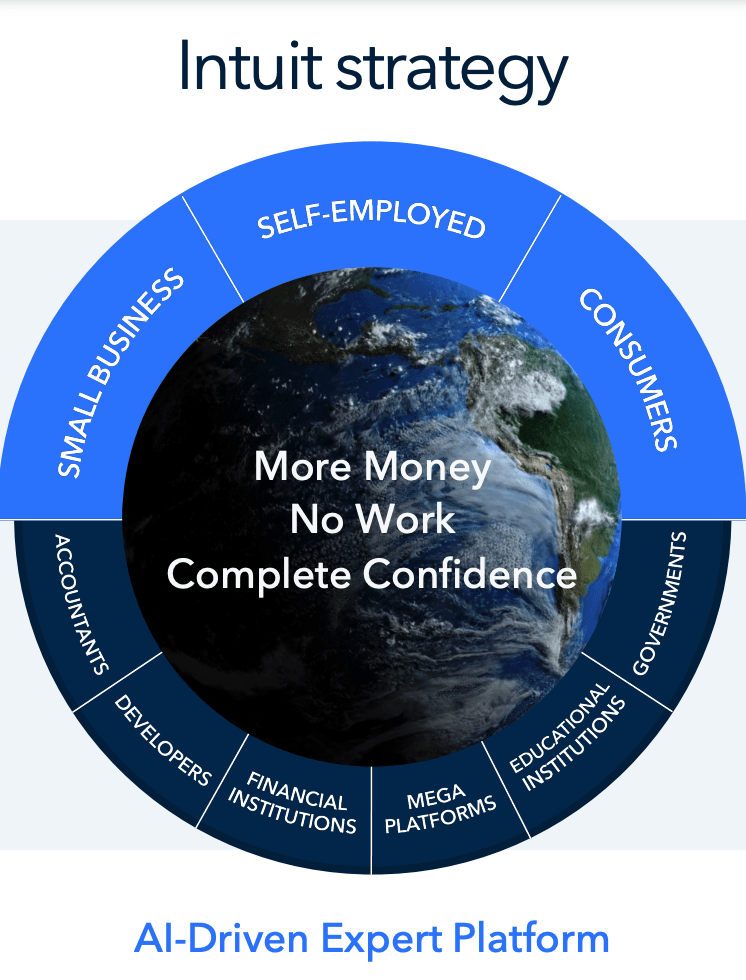

Intuit strategy (Investor Presentation)

In more recent times (2020), Intuit acquired CreditKarma for $3.3 billion in cash and $4.4 billion worth of stock. CreditKarma is a “personal finance assistant” which helps customers gain access to credit reports, improve credit scores and gain access to loans and credit through its partners. In 2021, the company acquired Mailchimp for $5.7 billion in cash and 10.1 million shares of stock. Mailchimp is an email automation platform and it is arguably the most diverse acquisition the company has made, away from its core financial products. However, there is a method to the perceived madness. 75% of small businesses surveyed rate finding new customers as their biggest obstacle, according to a study cited by Intuit.

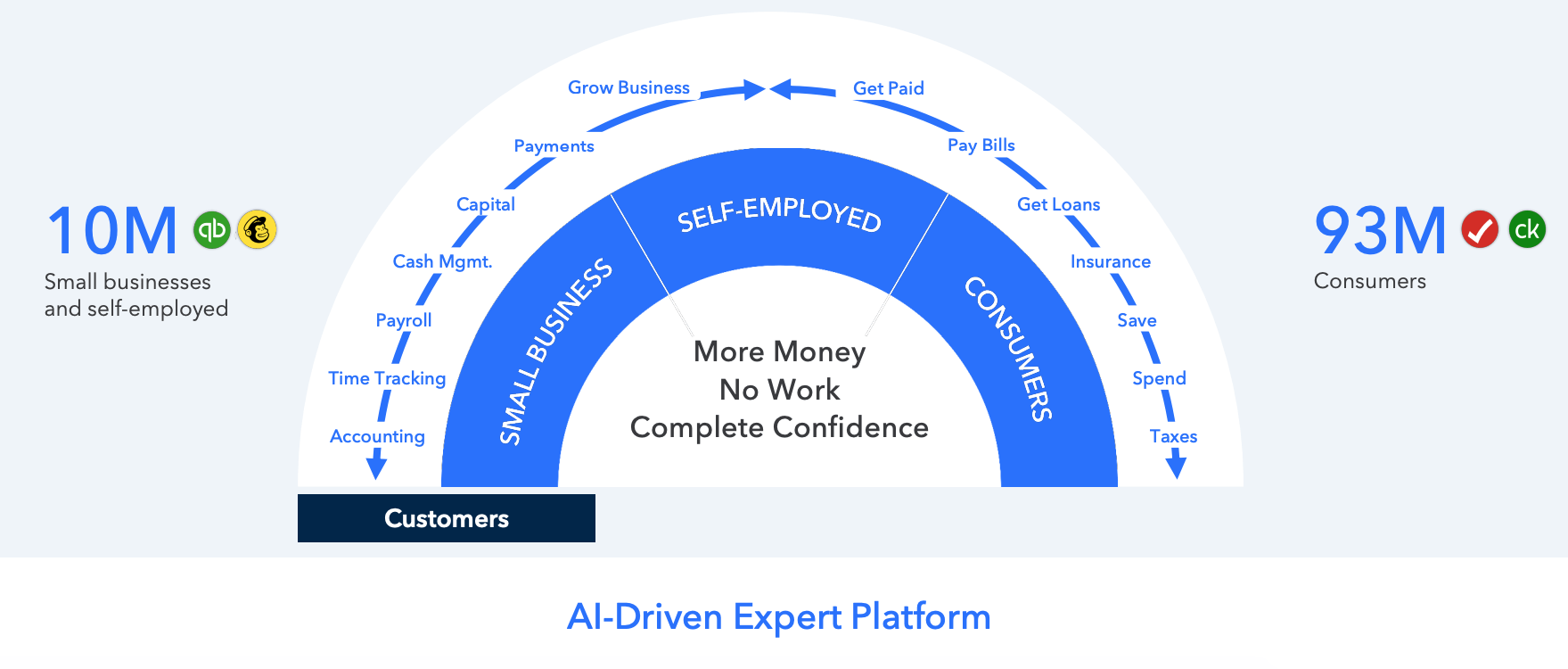

As Intuit aims to solve problems for its SMB customers, there are synergies and huge cross-selling opportunities. Thus it’s no surprise that QuickBooks and Mailchimp have approximately 10 million SMB & self-employed customers. In addition, Intuit’s Credit Karma and Turbo Tax platform cater to over 93 million consumers. Part of Intuit’s strategy is to also focus on being “expert-driven” with the power of Artificial intelligence [AI]. AI is a growing industry and has recently exploded in popularity, thanks to viral platforms such as ChatGPT created by the Open AI institute. The power of an AI model is dictated by the quantity and accuracy of its training data. In this case, Intuit has access to over 400,000 customer/financial attributes per SMB. Thus it can train its AI models with this vast data set. The company generates ~58 billion machine learning predictions per day, which helps drive over 730 million customer interactions.

Intuit solutions (Investor presentation)

Growing Financials

Intuit reported strong financial results for the first quarter of the fiscal year 2023. Revenue was $2.6 billion which increased by a rapid 29.4% year over year and beat analyst estimates by $97.15 million.

Breaking down revenue by segment, Small business & self-employed revenue increased by 38% to ~$2 billion. $264 million of this revenue can be attributed to Mailchimp and thus excluding this revenue increased by a steady 19% year over year. Credit Karma grew at a slow rate of 2% year over year to $425 million. This platform looks to have been impacted by macroeconomic headwinds, as high-interest rates impacted loans. Consumer group revenue increased by 25% year over year to $150 million. This was followed by “ProTax” group revenue which rose by 30.7% year over year to $34 million.

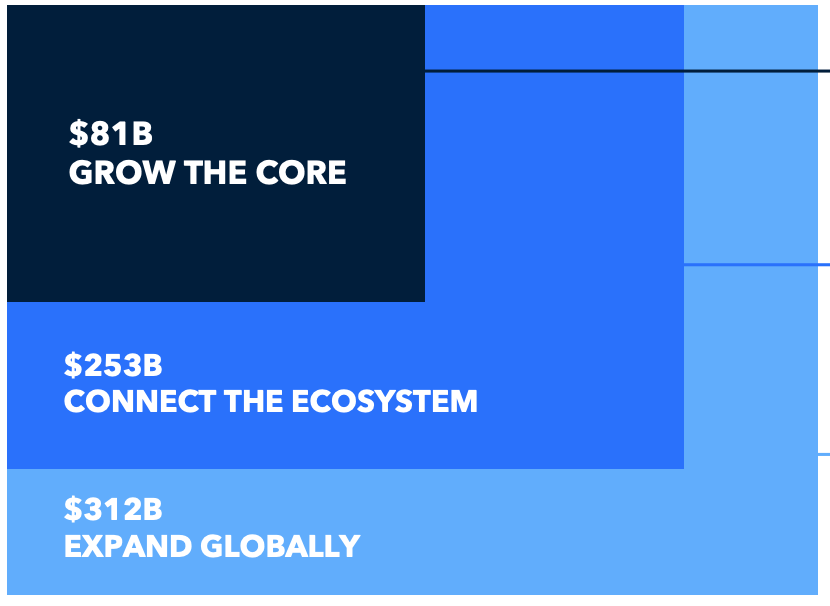

Intuit’s growth strategy focuses on three core elements; growing the core, connecting the ecosystem, and expanding globally. Its estimated Total addressable market for growing the core alone is ~$81 billion. In addition, the company estimates a $312 billion global expansion market size. So far, the company has been executing its strategy to a tee. Its “core” QuickBooks platform reported solid online growth of 29% year over year. SaaS accounting platforms are fairly “sticky” with customers because once a user starts to upload all their financials, there are fairly high “switching costs” in the form of admin. Therefore it was no surprise to discover that Intuit has raised the price of its QuickBooks solution. Its customers are unlikely to leave assuming the price raise isn’t egregious, this is great news in a high inflation environment.

Intuit TAM (Investor presentation)

Intuit has also been executed the second pillar of its growth strategy well which is to “connect the ecosystem”. As I discussed in the business model section, Intuit has made a series of acquisitions with a related customer base. This means cross-selling opportunities are abundant. Intuit’s overall “Online services” revenue increased by a blistering 109%. This includes a $264 million contribution from Mailchimp. Its Payroll product also contributed to growth, as SMBs look for an easier way to pay employees.

Intuit’s third growth pillar growing internationally, has also been executed well. Its Online Ecosystem revenue increased by a blistering 172% year over year, or 19% year over year excluding Mailchimp.

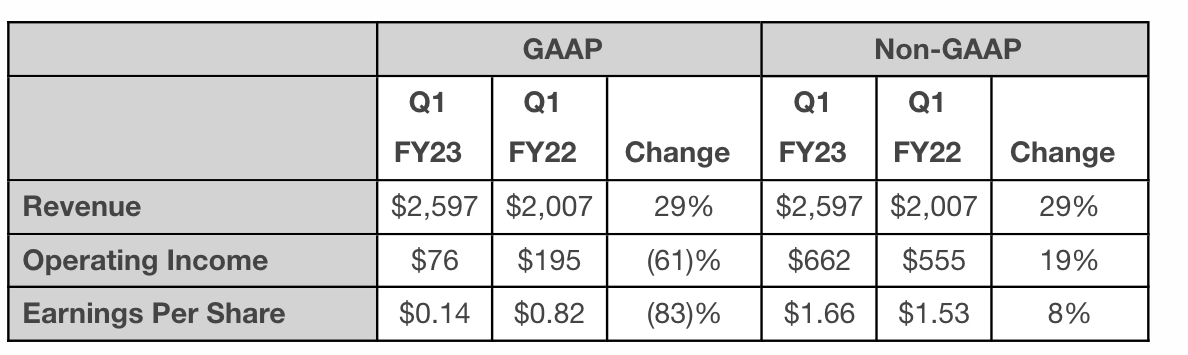

Onto profitability, Intuit reported $662 million in Non-GAAP operating income, which increased by 19% year over year. Overall Earnings Per Share [EPS] was $0.14 which beat analyst estimates by $0.54.

Financials (Q1,FY23)

Intuit has a solid balance sheet with $2.7 billion in cash and marketable securities. The company does have fairly high debt of ~$7 billion in debt, but the majority of this debt $6.48 billion is long-term debt and thus manageable.

Intuit bought back a substantial $519 million worth of stock in Q1,FY23, which is a positive sign and shows management has faith in the business strategy. The company also pays a 0.81% forward dividend, which isn’t very high but it did increase by 15% year over year.

For the full fiscal year 2023, management has forecast revenue growth of between 10% to 12%, which is slower than prior growth rates. This looks to be mainly impacted by a forecasted (10% to 15%) decline in Credit Karma revenue, which is expected to be driven by the high-interest rate environment and forecasted recession.

Advanced Valuation

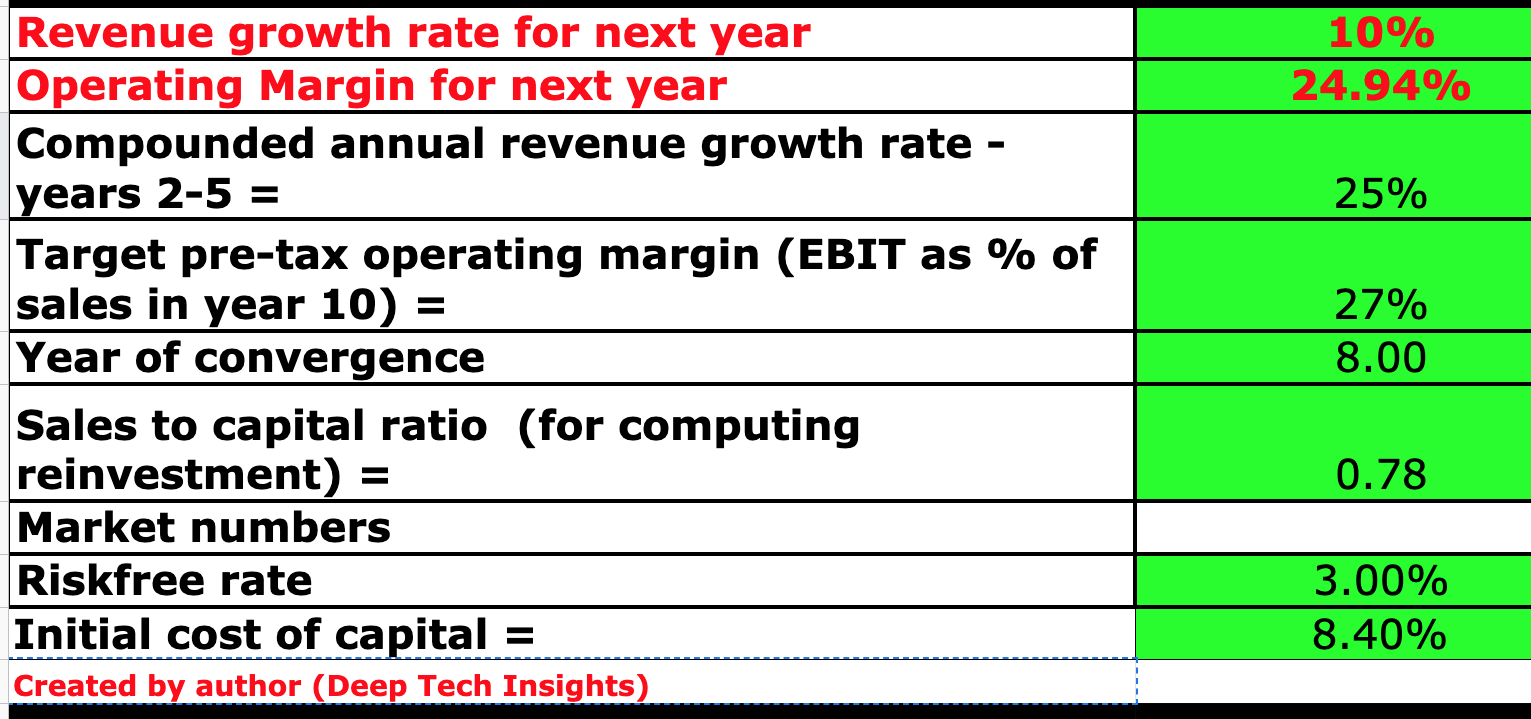

In order to value Intuit, I have plugged its latest financials into my discounted cash flow model. I have forecast 10% revenue growth for “next year”, which includes the next three quarters in my model and is aligned with management’s tepid expectations, due to the macroeconomic environment. In years 2 to 5, I have forecast a greater 25% revenue growth per year, as economic conditions are forecast to improve and Intuit benefits from multiproduct growth.

Intuit stock valuation 1 (created by author (Deep Tech Insights))

To increase the accuracy of the valuation model, I have capitalized R&D expenses which has lifted net income. In addition, I have forecast a 2% increase in operating margin over the next 8 years, as the business benefits from increased scale and cross-selling.

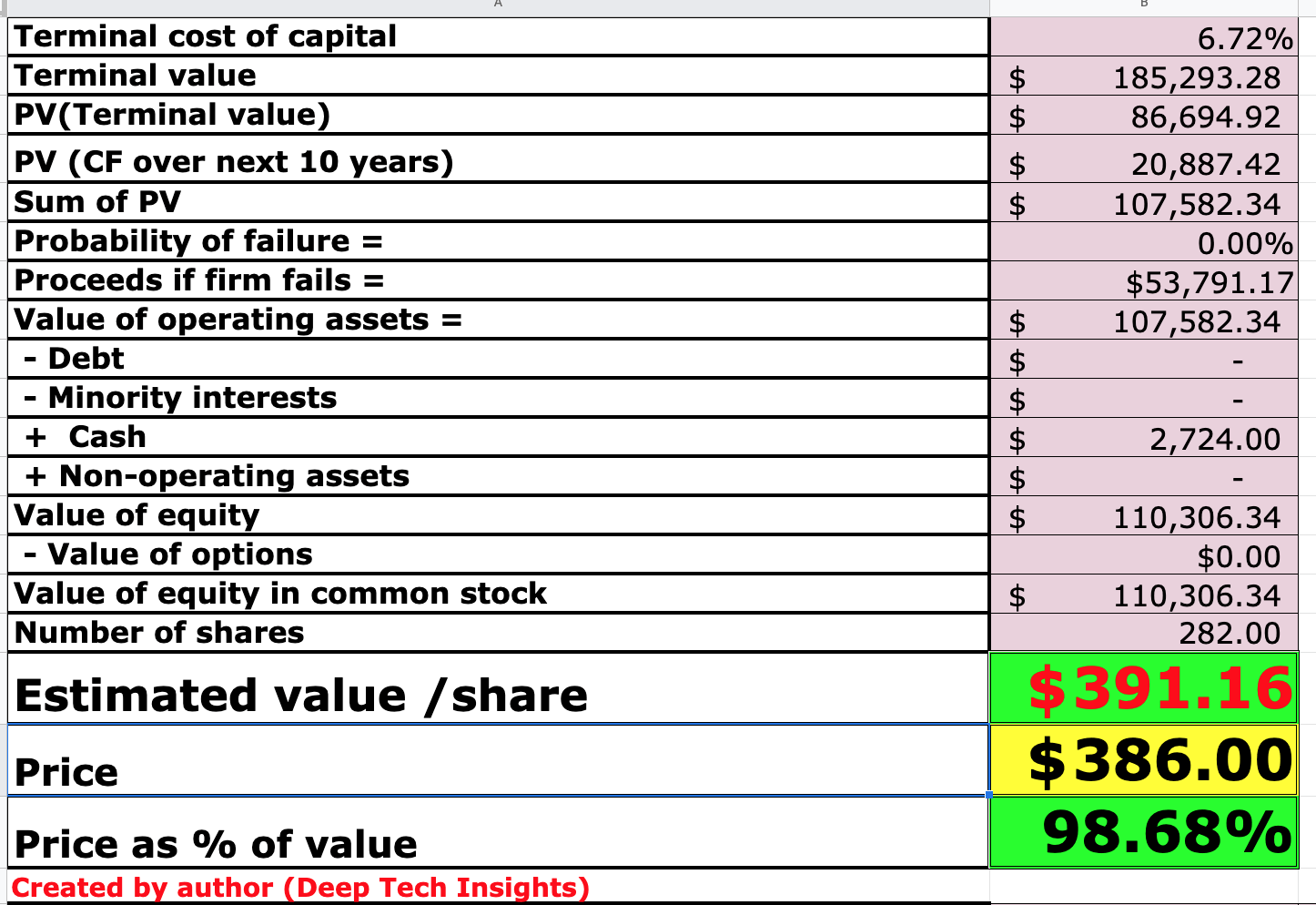

Intuit stock valuation 2 (Created by author Deep Tech Insights)

Given these factors I get a fair value of $391.16 per share, its stock is trading at ~$386 per share at the time of writing and thus is “fairly valued”. This valuation is expected as the company has a strong leadership position, with growth opportunities and a high-quality business model.

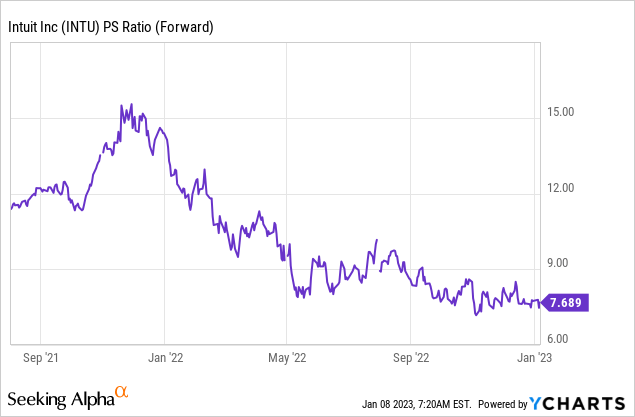

A positive is Intuit trades at a Price to Sales ratio = 8.19, which is 24% cheaper than its 5 year average.

Risks

Recession/slowing growth

Many analysts have forecast a recession and thus I expect longer sales cycles, and slowing growth for Intuit. A positive is I don’t believe the company’s market position will be impacted and I don’t expect them to lose SMB customers.

Final Thoughts

Intuit is a market-leading fintech company and offers a range of iconic products with high “stickiness” among its customer base. Its three-pillar strategy has been executed well so far as the company continues to grow its core. In addition to cross-selling its products to its related consumer base. Its stock is fairly valued intrinsically and undervalued relative to historic multiples at the time of writing and thus it could be a great long-term investment.

Be the first to comment