JHVEPhoto

Profile

In its most simplified form, Intertek (OTCPK:IKTSF) is an outsourced Quality Assurance or QA provider. They have operations across the globe, and operate using a network consisting of more than 1,000 labs in 100 different countries, supporting more than 400,000 companies with ensuring their products and services are up to scratch.

Intertek claims to provide a unique TQA (Total Quality Assurance) package consisting of the following main operations (ATIC):

- Assurance

- Testing.

- Inspection

- Certification

Business Segments (Company Filings)

Companies basically appoint Intertek to manage their QA-, supply chain- and related functions, either due to a lack of ability internally, due to cost advantages of outsourcing this function, or due to better compliance and less possibility for brand/reputational damage when QA is outsourced. (A good example of this is VW’s Diesel gate emissions scandal – where the ATIC functions listed above were conducted by VW internally). Had this been an outsourced function, VW would probably not have faced the same level of reputational or financial damage. Intertek’s services give their clients the ability to better concentrate on their core value-generating capabilities, while they know their Quality Assurance needs are covered.

The ATIC functions conducted by Intertek can be as diverse as testing new toys, inspecting power stations, certifying vaccines, auditing supply chains and vendor compliance, to conducting sustainability- and performance analysis. To do this, Intertek employs experts across a wide number of industries, and with a global footprint to ensure they can provide support in an effective manner.

Initiatives such as SourceClear™ provides customers with credibility and traceability relating to the sustainability of their supply chains, such as raw materials, social and environmental practices that maximises positive impacts. This gives their customers’ clients the assurance that they are doing their part and supporting a more sustainable process through their consumption.

CarbonClear™ is a similar initiative, but it allows companies to gain clarity on the carbon impact of their end-to-end operations. This will lead to consumers, be they retail or commercial, to make better decisions – which could lead to societal improvements in the processes and systems we use. This is an important consideration given the emphasis being placed on companies to improve their sustainability and energy transition efforts.

To ensure that their offering remains relevant, Intertek carries out about 6,000 Net Promotor Score (NPS) customer interviews each month to make sure they are up to speed in a more complex and integrated world which constantly introduces new opportunities, but also new risks. (NPS questionnaires measure the likelihood of customers to recommend Intertek’s services. This seems to be a big part of their strategy – making sure they keep their fingers on the pulse and build/maintain lasting relationships with clients.

The world today is more focussed on viable, sustainable solutions than ever before – this is true for all products and services we consume. This is only expected to increase going forward, and should serve as a lasting (albeit not explosive) catalyst for growth. The growth of the TIC (testing, inspection, certification) industry has been largely correlated with GDP growth.

Model

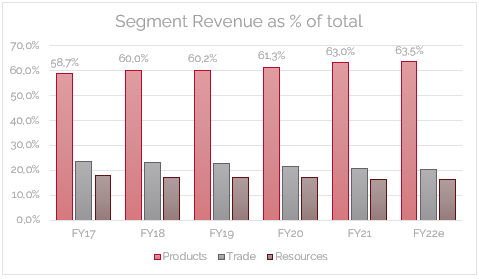

Intertek’s operations fall into 3 different groups. (Products, Trade, Resources). In the graph below, it is clear that products have increased as % of total revenue over the last 5 years.

Segment Breakdown (Company Filings) Segment Contributions (Company Filings)

Products:

The products division looks mainly at the quality and safety of physical components and products, as well as the related risk assessment and quality management systems.

Products, which accounts for the biggest portion of revenue and profits, has been under pressure for a lengthy time now as revenue from China has taken a big hit during and post pandemic. (China represents 20% of group revenue.)

The revenue from this segment is not recurring in the sense that there is some kind of subscription model – it is dependent on the constant development of a new range of products that need to be tested for different requirements. IR states that this is currently happening faster than before, as the innovation cycle has shortened technological advancement over the years.

This segment is not particularly cyclical – as the volume of goods sold does not affect them. They are not paid per unit sold/used. As long as there is a stream of new products, they can continue with their business. However global recessions, or shocks such as Covid 19 will impact new product launches.

This segment of the business is expected to grow at a GDP+ rate.

Trade:

They add value via analytical assessment, inspections and other technical services of goods during custody transfer processes (including storage and transportation)

Segments of the Trade Business:

- Cargo & Analytics (aka Caleb Brett business – cargo inspection and analytics services for oil, gas, chemical and commodity markets).

- Government and Trade (Supports trade compliance via assessment services to regulatory bodies on exports and imports).

- Agriworld (Inspection, testing, certification etc. across entire agriculture supply chain).

This segment is more cyclical than products, as it is dependent on the amount of the above shipped items. However, it is also less capital intensive than the products segment. There is less need for expensive machinery and materials than with product testing. Trade relies more on having a large, yet nimble network – the sooner a ship can move and offload its cargo, the sooner it can enter into a new trade. IR noted that the cost of this function is for clients is relatively small, but absolutely mission critical.

This segment of the business is expected to grow roughly in line with regional GDP.

Resources:

Resources is the smallest segment of the business, both by revenue and profits. Intertek is focussed on optimizing the use of assets in the oil, gas and nuclear business. This is done via inspections, asset integrity management, and training services.

- Industry services focusses on knowledge of lines like oil and gas, nuclear- and other power industries. Intertek is involved with inspection, materials testing, and asset performance management.

- Minerals (consists of a broad range of services to the mining exploration industry).

According to discussions with IR, the resources part of the business is also more capital light than the products segment. It primarily involves the inspection of new facilities such as mines and power stations.

This segment of the business is mainly dependent on the level of CAPEX that is spent by customers. 2021 has seen somewhat of a boom for O&G capex, and there are views that this could be sustained a little more. Longer term, this will need to transition to more sustainable and green solutions.

Industry Overview:

Intertek’s main drivers have always been, and will remain – regulatory requirements, along with global GDP expansion.

From a regulatory perspective, certain tests and procedures are non-negotiable, while others are good industry operating practices that are basically expected of companies. The brand/reputational risk they face from non-compliance is far greater than the cost to have their products/processes certified. One newspaper headline that paints a company in a bad light due to deliberate non-compliance can wipe billions off their market cap.

Growth of the TIC market is also linked to global GDP. A slowdown in trade, mineral or energy consumption and product launches directly impact the industry. Hence, it is also unlikely to grow dramatically faster than overriding GDP permits.

New drivers are, however, gaining more traction in the industry. Things like increased focused on sustainability, clean and renewable energy consumption, and increased reliance on more connected world (and the datacentres and warehouses supporting this) all create additional demand for testing, inspection, and verification.

TAM:

Intertek believes that the current market of £50 billion is only about 25% of the £250 billion pie, with the remaining 200 currently being insourced. This is more or less in line with estimates from 3rd party researchers such as Markets and Markets.

These numbers differ somewhat from those supplied by BVI – who also sees the market in the range of €200 billion, but believes only 60% of this is still insourced, with the remaining 40% already available/outsourced. (i.e., 80 billion outsourced and 120 billion insourced.)

Via a Guidepoint Expert Network call, David Prince – ex COO of BV, was more or less in agreement with the Intertek number, but points out that the $50 billion is a function of the variables and markets in which the specific provider plays (in other words, more than $50 b might already be outsourced, but Intertek only plays in $50 billion of that, as they have no exposure to marine TIC, as an example.

The large players all have some commonality, but they also all have their different niches and aspects. So mostly when companies report their version of TAM, it is specified on their areas of expertise. It seems to be a bit of a moving target depending on where and when you look at the data.

I would not place too much emphasis on any potential TAM numbers, and would rather focus on the growth trends that have been largely in the GDP+ area in recent history.

Competitors:

Intertek’s biggest competitors are Bureau Veritas (OTCPK:BVRDF), SGS (OTCPK:SGSOF) and Eurofins Scientific (OTCPK:ERFSF). These companies all have different areas of expertise. IR also pointed out in our meeting that the overlap in between the big players was actually quite small – and thus they don’t really have direct competitors. They also indicate that geography is a large differentiator between the companies. Everything taken into consideration, they regard SGS as their biggest competitor.

Notably, Intertek has less exposure to Trade and Resources when compared to both BVI and SGS, which should mean they experience less cyclicality.

SWOT ANALYSIS:

Strengths:

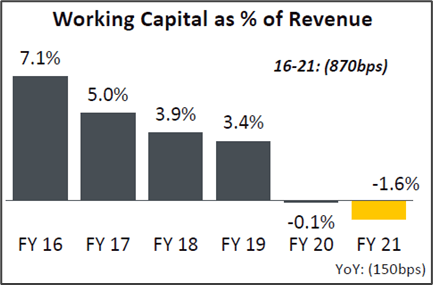

Negative Working Cap Cycle. Intertek has shown good execution in achieving a negative working capital cycle – indicating they basically don’t need any capital on hand to run the business, as gathering happens faster than payments.

Negative Working Capital (Company Filings)

FCF Margin

FCF margin has more than doubled over the last 10 years. FCF conversion is also particularly strong, well in excess of a 100%.

FCF Margin (Created by Author, info from public filings)

Large global network

One of Intertek’s strengths is its broad geographical presence. They have industry specific auditors, inspectors, and other knowledge workers available whenever and wherever. This gives customers the peace of mind that they can run operations without disruptions.

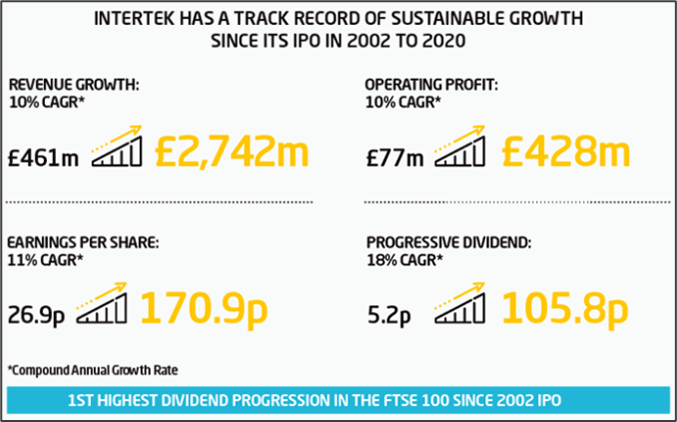

Progressive Dividend

For the period 2003 to 2019, Intertek has been the FTSE’s leading company in terms of dividend progression, achieving a strong CAGR of 17% over this period.

Superior profit growth vs peers

During the period 2012 to 2019 (in between recessions), Intertek achieved profit growth that was superior to that of peers. Intertek grew at a CAGR of 7%, vs BVI at 5% and SGS at 2%.

Strength during recession

Intertek’s business model might be more durable during a recession, as their ATIC services are in most cases mission critical to clients. They also generate revenue ins 17 industries and across more than 100 countries. This diversified base insulates them to a certain extent if any particular region experiences a recession. In 2009 they delivered 3.5% LFL revenue growth, at a margin of 16.9%, and 26.5% ROIC.

Weaknesses:

Slower growth over the last couple of years

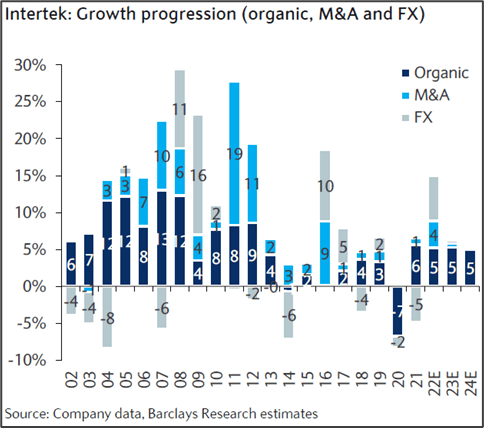

Barclays points out that Intertek’s growth rate has slowed in recent years compared to peers, this after a decade of relative outperformance.

This change in growth is more pronounced when looking at Intertek’s breakdown in isolation, as seen below. Also note that the 2 best years over the last decade had significant contributions from FX moves.

Growth Breakdown (Barclays Research)

Absence of organic growth levers

Not just Intertek, but the entire TIC industry is quite closely linked to global GDP growth. is quite highly dependent on global GDP growth. I don’t believe they many other levers to pull in order to stimulate growth.

Recent margin guidance downgrade

Intertek has lowered their margin guidance twice within the last year. This also follows margin disappointment at peer SGS – indicating that there might be more pressure on the industry than previously though. 2021 margins benefitted from government subsidies, so 2022 would be lower in any case, however the slowdown in the products section means there is less operational leverage.

Exposure to high wage growth economies

Intertek has significant exposure to countries that have seen high levels of wage inflation over the last year. This has contributed to their guidance for margin erosion. Barclays states that their exposure to these economies is higher than peers.

Opportunities/Drivers:

Lasting changes post-Covid

Covid likely served as a catalyst for increased supply chain strength/resilience. A Gartner study from 2021 estimates that 87% of companies will need to strengthen their operations in this regard.

China reopening

There has been a significant disruption to normal business operations in China over the last 2+ years. The complete reopening of China should enable strong YoY growth for Intertek’s products segment.

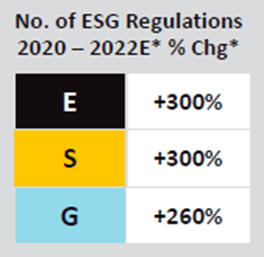

Increased regulatory focus on sustainability

All elements of society are placing an increased focus on all things green and sustainable. This ranges from our energy sources to utilizing more sustainable practices for production, across all industries. This is placing an emphasis on the type of service provided by Intertek. The data on the right is based on a global estimate from DataMaran conducted in May 2022.

ESG Increases (DataMaran)

Emerging middle class in China, India, Africa

While the middle-class market in the US, which has a relatively high level of consumption, has remained fairly stable even though the population is not rapidly growing – this is the case in large “emerging” markets like China and India. Increased consumption as more people reach middle class will be beneficial. The products segment (Intertek’s largest) in these markets are therefore expected to experience increased demand.

Deglobalization

Some analysts seem to be of the view that because globalization was good for quality assurers like Intertek, deglobalization must be bad. I do not agree. More, smaller regional suppliers/chains etc. would all still require the same level of testing/certification etc.

Threats:

Reputational/Brand Risk

I believe this is the single biggest risk that Intertek faces. This is expanded on in the segment below.

Prolonged recession

A deep, global, and prolonged recession would be detrimental to Intertek. Trade and Resource activity would both be expected to decline, and although products are not dependent on the volume sold, companies will likely delay new product launches.

Financial Overview:

Since IPO, Intertek has grown revenue and earnings at the same rate (±10% CAGR), however expectations are that this rate will slow down going forward.

Company Overview (Company Filings)

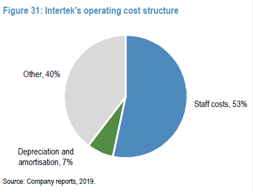

Costs:

A 2019 report from JPMorgan provided the following breakdown of Intertek’s cost base. Given the nature of their business, salaries are by far the dominant expense, and the structure for major peers BVI and SGS has the same breakdown (in fact about 60% of their total costs relate to staff).

Cost Basis Breakdown (JP Morgan Research)

Debt:

Intertek has a net debt to EBITDA ratio of around 1.3x. This ratio has been steadily decreasing until they raised capital for the acquisitions of SAI Global Assurance (Australia) and JLA (Brazil) in 2021. Both firms operate in the Food, Agri and Environmental testing industries.

Debt maturity looks well structured, with an average maturity of 4.5 years, and the average rate of 2.7% is low given the current rate environment. The majority of Intertek’s debt is USD denominated.

The above, along with an interest coverage ratio of around 15x (EBIT/interest expense) leads me to the conclusion that Intertek’s debt is well managed and not a cause for concern.

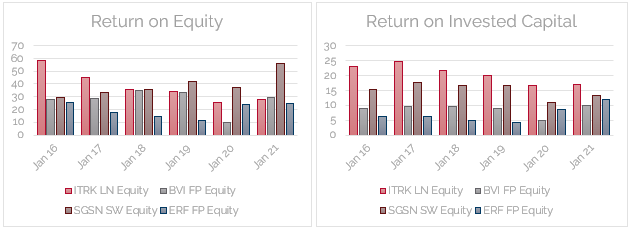

Returns:

Intertek has sustained high return levels over the last couple of years, and brokers mention that this has regularly been higher than their peers.

From the graphs below, however, it is clear that over the last 6 years, most of their profitability metrics have decreased to some extent.

Created by Author (Company Filings)

Valuation:

Absolute:

At group level, Intertek aims to growth at GDP+ organically over the long term in real terms. I have grown the product segment of the business at a CAGR of 5% over the forecast period, with trade and resources grown at3.5% each. This leads to a CAGR of 4.5% overall – slightly higher than expected GDP growth.

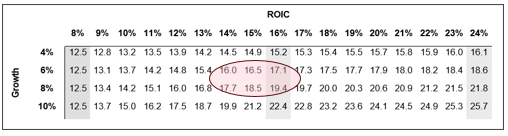

Fair Multiple Assumption:

In my base case, I apply a multiple of 18x. This is well below the average of 23.9 and median of 23.2. Based on a ROIC of ±15% from my model, and earnings growth of between 6 and 8% – I believe a range of 16-20 is more applicable. This also represent a premium of 13% over the normal developed country multiple. Given Intertek’s high (100% +) FCF conversion rate, negative working capital cycle, and pretty bulletproof business model, I believe this premium is warranted.

P/E vs ROIC Table (Market Research)

These assumptions lead to a FV of around GBP 44, pretty much bang on the current share price. Adjusting growth assumptions by 1% up or down leads to up/downside of about 20% in each direction.

Relative:

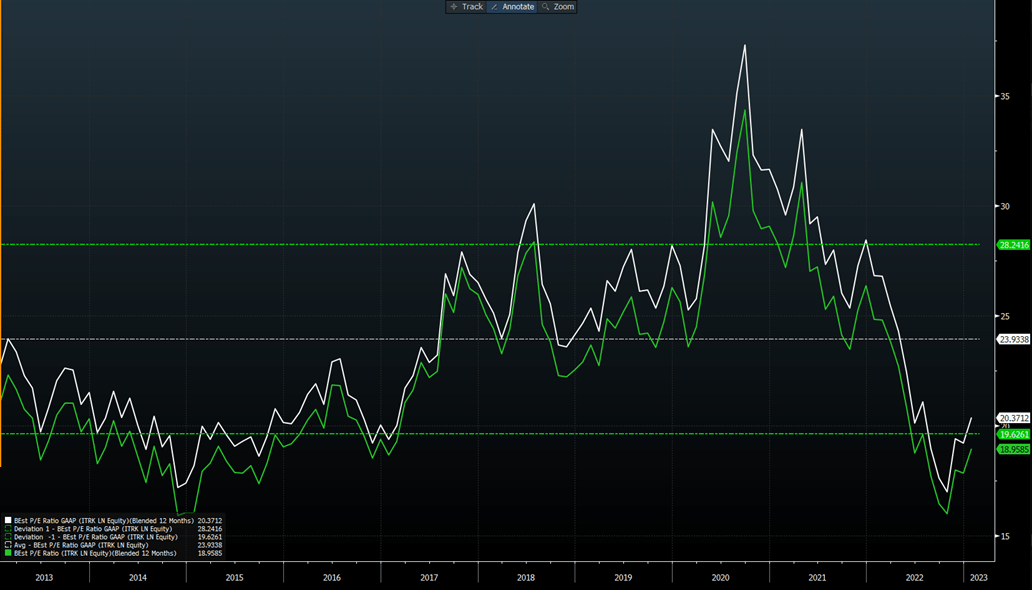

Intertek is currently trading on a BF P/E of 20.4, vs 10-year average of 23.9, and thus at a discount relative to its own history. A belief in reversion to the mean would therefore mean a P increase of about 18%.

(Note that GAAP (white) & Adjusted (green) numbers are very similar, as there is not a large effect from SBC etc.).

Intertek forward P/E Ratio (Bloomberg Terminal)

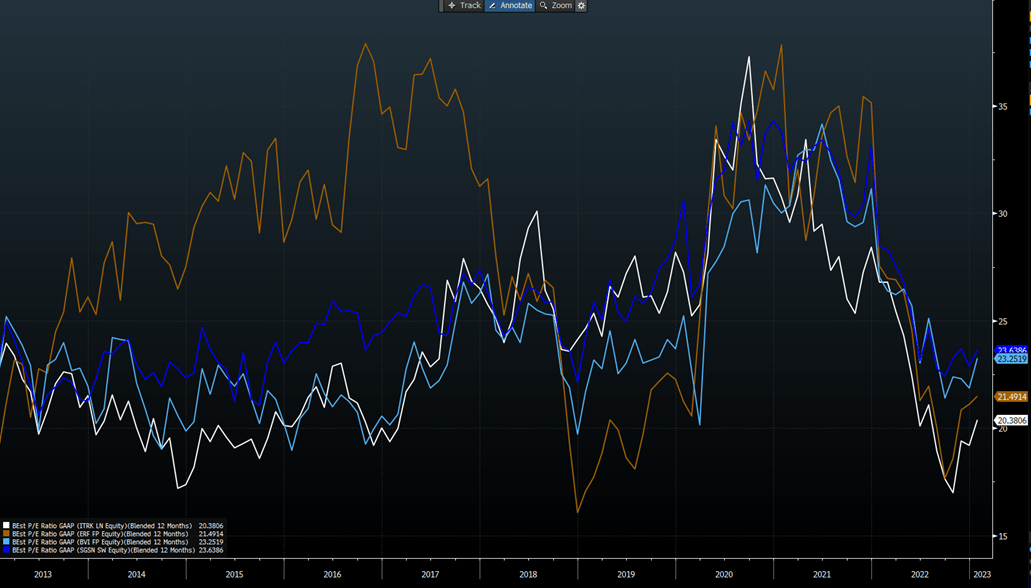

Compared to peers SGS and BVI, Intertek trades at a bit of a discount, but movements in the multiple have been similar over the last 10 years (including recent contraction, although Intertek did derate slightly more due to relative under performance). Note that Eurofins’ multiple has been a bit more erratic, experiencing steeper movements.

Intertek vs Peers forward P/E Ratio (Bloomberg Terminal)

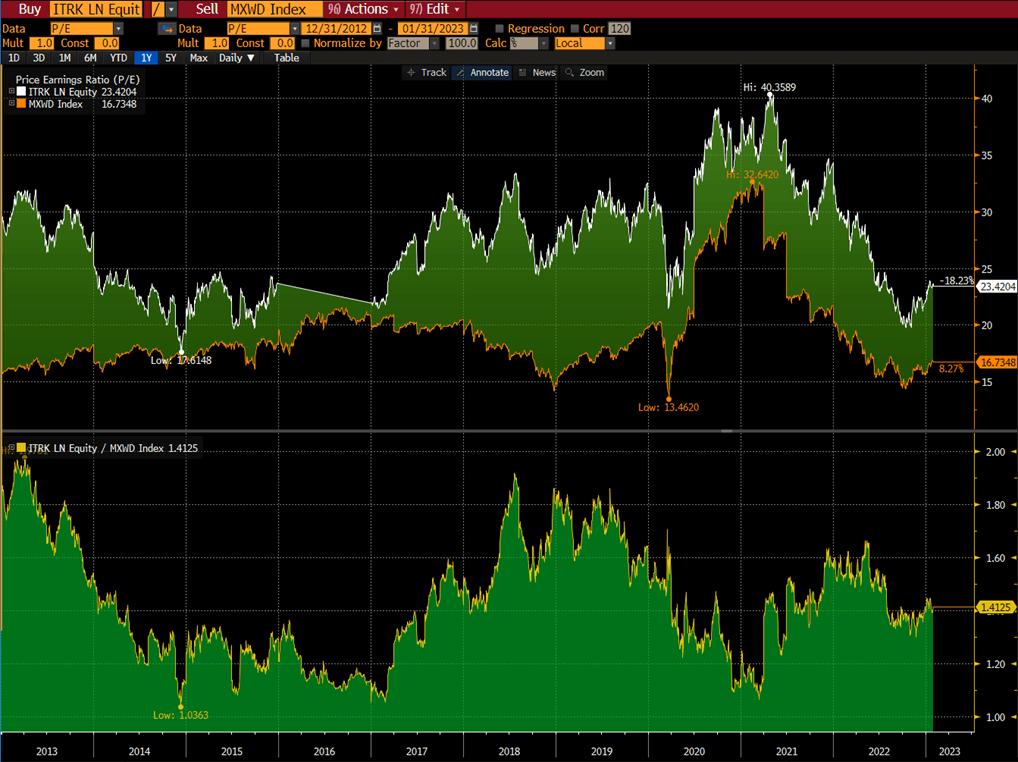

Compared to the TTM P/E of the MSCI ACWI over the last 10 years, Intertek has always traded at a premium. There is currently no substantial deviation from this trend. The relationship currently (1.41x) is more or less equal to the long term mean of 1.43x.

Intertek vs MSCI Acwi P/E Ratio (Bloomberg Terminal)

Conclusion:

Intertek has a reasonably bulletproof business model, and long term trends should prove to be a tailwind to their operations. Growth, however, will not be explosive, and will always be fairly closely linked to global GDP growth. I believe the current share price is fair, and thus does not offer the upside required to start building a position. Any substantial slide from current levels could be seen as possible buying opportunity.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment