Ceri Breeze

British Airways owner, the International Consolidated Airlines Group (OTCPK:ICAGY), also called IAG, has made a smart recovery at the stock markets in the past year. Its ADRs are now only 6.3% below where they were a year ago. For context, this is a bigger recovery than that for the S&P 500 (SP500) which is still 8.2% below where it started last year.

Interestingly much of the recovery has been seen in 2023. Year-to-date [YTD], it’s up by a huge 33.4%. There are many reasons for this, starting with a broad stock market recovery. Stocks that had been particularly affected in the past year, have seen a sharp improvement this year so far. A come-off in inflation and the reduced risks of a recession have contributed to this buoyancy. More specifically, the fact that COVID-19 has stayed under control during this winter season is a boost for travel stocks.

The question now is, how high can ICAGY go? It’s still nowhere near its pre-pandemic highs. In fact, it’s trading at a fourth of its price then. That said, its financial situation is also very different. Here I take a closer look at its financials, to assess both the good and the bad to understand what could be in store next for the airlines’ operator.

Headway in 2022

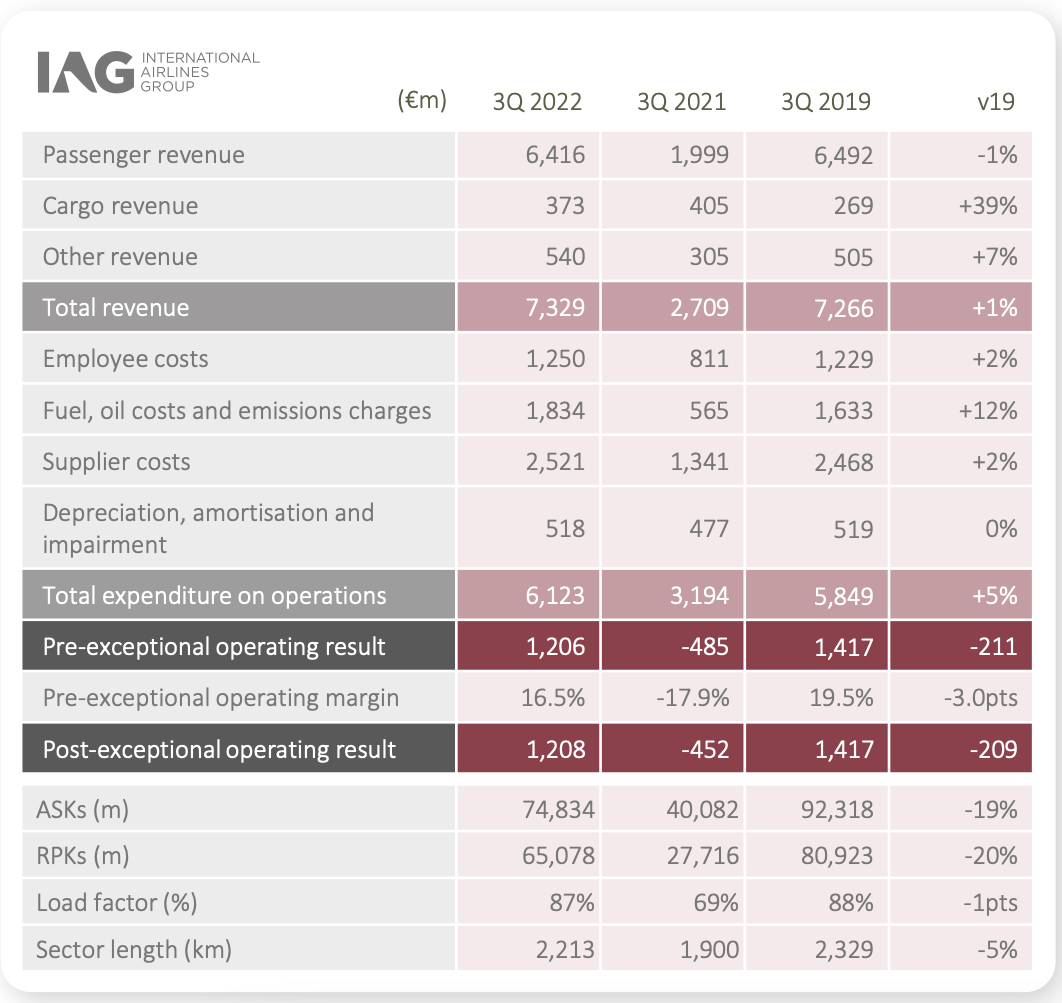

The company has reported two consecutive quarters of profits in 2022, after running losses for nine quarters, which covers the pandemic period and then some. This is a good place to start. Its year-on-year (YoY) revenue growth has been positive for an even longer period of six quarters. Even its latest gross profit margin isn’t bad at 31.5%. Despite a double-digit increase in operating costs because of high fuel costs, its operating profit has risen by threefold in Q3 2022 from the quarter before alone. It looks like the company is recovering well from the setback of the two years before 2022.

Note: ASK refers to Available Seat Kilometres and RPK refers to Revenue Passenger Kilometres (Source: IAG)

Even more heartening are its latest numbers for the third quarter of 2022 (Q3 2022) compared with the last pre-pandemic period of Q3 2019. Its revenue is actually up by 1% since to EUR 7.3 billion. The company’s available seat kilometres [ASKs] are still lagging behind by 19%, but these are recovering fast too, having more than doubled since the same quarter last year.

Mixed liquidity picture

The company’s liquidity, as measured by its interest coverage ratio, has also seen impressive improvement. With an increase in operating profit in Q3 2022 the ratio now stands at 5.5x, up from a sub-optimal 1.7x for Q2 2022. The company took on debt during the pandemic, so this is an important ratio to note, especially since it wasn’t even making an operating profit until two quarters ago so there was no coverage at all.

However, the same cannot be said for another significant liquidity indicator, the current ratio. At 0.8x, it indicates that if push comes to shove, the company won’t be able to meet its financial obligations. To be fair, the latest numbers we have are for Q2 2022, which is now seven months ago. ICAGY has seen substantial progress since, going by the Q3 2022 numbers, so this could have changed. Still, it’s worth highlighting.

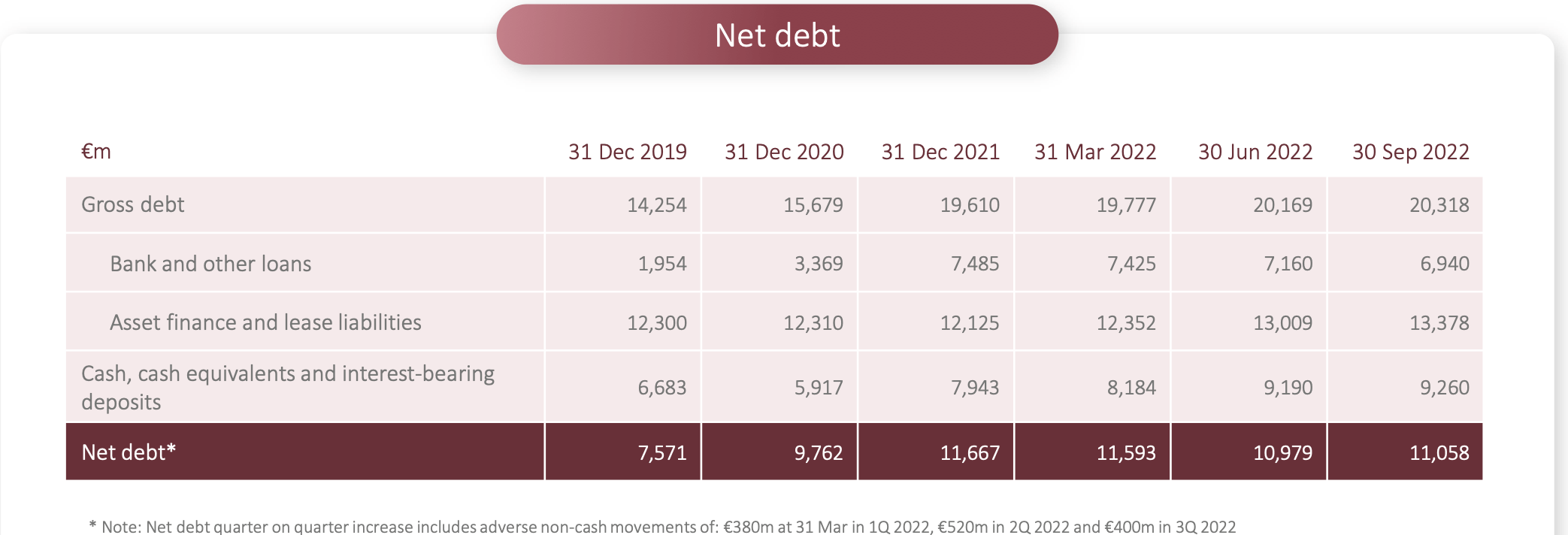

Increased debt, but in check

The company’s debt had doubled already by the end of 2019 from the year before to EUR 14.3 billion. Its net debt was lower of course and comfortably under the company’s net debt-to-EBITDA ceiling of 1.8x. However, come 2020 and there was nothing comfortable about its debt. At the end of 2021, it was 37.5% higher than that in 2019. And there was no EBITDA to speak of for the obvious reason of travel restrictions during the time.

Source: IAG

By September 2022, debt was even higher, rising by 42.5% from 2019. At least it is positive EBITDA now, even if the actual number was small for Q2 2022, which indicates that the company is on the path to improvement. Also, it needs to be pointed out that despite everything its debt ratio isn’t bad at all at just over 0.5x.

Optimistic outlook

With this kind of recovery, it’s hardly surprising that IAG is optimistic about its full-year results due later this month. It is “Confident in returning to pre-COVID levels of operating profit”. It also expects to clock a third straight quarter of net profit. Further net cash flow is “expected to be significantly positive for FY22”.

A high P/E ratio

It follows then that its price is rising now that the broader macro picture has cleared up a bit. Moreover, market multiples like price-to-sales (P/S) and price-to-cash flow (P/CF) are also way lower than that for the industrials sector. The P/S is at 0.51x compared to 1.4x for the sector, while P/CF is at 2.72x versus 16.65x for industrials.

However, the price-to-earnings (P/E), which I like to consider most closely, is more than just a small hiccup. Its twelve months trailing [TTM] figure doesn’t come into play because earnings are still negative for the past year. So I consider the forward P/E instead, which is trading at a huge 42.9x compared to 19.9x for industrials. It’s also significantly higher than that of its immediate peers like American Airlines (AAL) and Deutsche Lufthansa (OTCQX:DLAKY) at 10.7x and 13.3x respectively. And these other airline companies’ P/S and P/CF aren’t particularly different than that for IAG either.

What next?

There’s little doubt that IAG has come a long way from the pandemic. Its revenues are back to pre-pandemic levels and it hopes to achieve similar operating profits soon too. Its liquidity situation can be better, but with improving figures in Q3 2022, that should look better by its next results release. Its debt situation, all said and done, is not too bad either.

The challenge as I see it, is its P/E, which indicates that the price has run ahead of itself. But we will know that for sure only when the company’s full-year results are released later this month. If they turn out to be substantially better than expected, its forward P/E could adjust downward accordingly. I like IAG, I even hold shares in it. But then I bought them a long time ago. I’d wait for its next financial statements before buying for now.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment