onurdongel

Investment Thesis: I take a bullish view on InterContinental Hotels Group (NYSE:IHG) due to continued growth in RevPAR despite inflationary pressures.

In a previous article back in November, I made the argument that InterContinental Hotels Group has continued to see strong RevPAR growth, but further earnings growth and a reduction in long-term debt could be significant catalysts for further upside going forward.

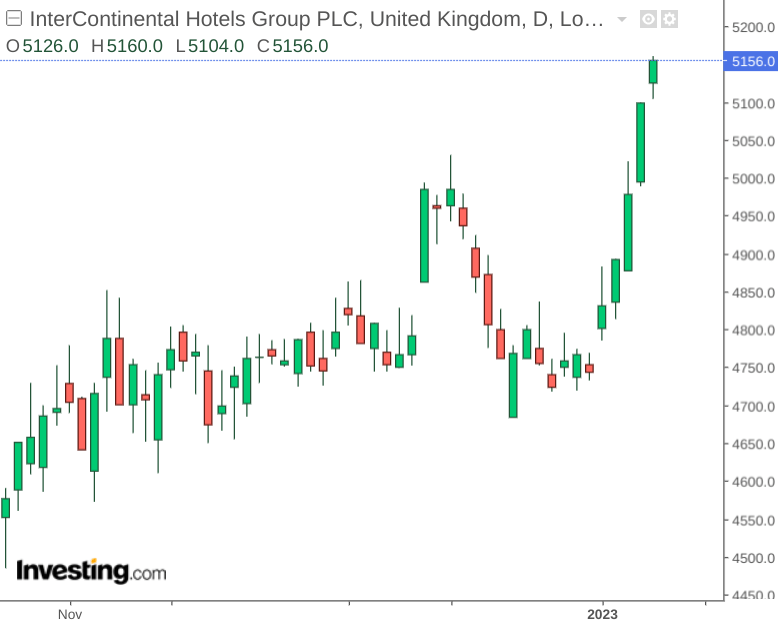

The stock has continued to perform well, up by just over 12% since my last article:

investing.com

The purpose of this article is to assess whether the upside that we have been seeing in the stock can continue from here.

Performance

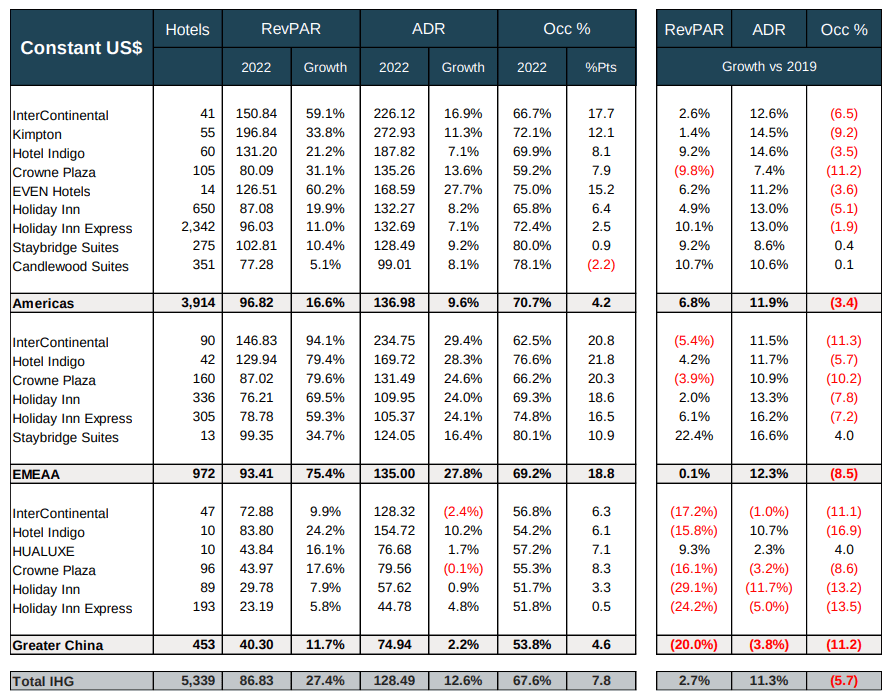

While I had previously stated that RevPAR (or revenue per available room) across the EMEAA and Greater China regions had largely caught up with performance across the Americas, the Americas still remains IHG’s largest market – with over 70% of the company’s hotel portfolio based there as of Q3 2022.

IHG Supplementary Information – Q3 2022

From this standpoint, I decided to conduct a deeper analysis of brand performance across the Americas. Specifically, I decided to compare performance for both 2019 and 2022 (Q1 to Q3) by analysing the average RevPAR across brands from lowest to highest across each brand.

Please note that the original RevPAR figures for each quarter were sourced from historical quarterly reports, with the below averages calculated using SQL – calculations and original data can be found here.

2019 Q1 to Q3: Average RevPAR by brand

| Brand | Average RevPAR from Q1 to Q3 |

| Candlewood Suites | 64.23 |

| Holiday Inn | 76.88 |

| Holiday Inn Express | 80.90 |

| Crowne Plaza | 86.78 |

| Staybridge Suites | 93.42 |

| Hotel Indigo | 123.43 |

| EVEN Hotels | 139.37 |

| InterContinental | 153.31 |

| Kimpton | 195.90 |

Source: Average RevPAR calculated by author using SQL using data sourced from historical quarterly reports for InterContinental Hotels Group (2019 Q1 to Q3).

2022 Q1 to Q3: Average RevPAR by brand

| Brand | Average RevPAR from Q1 to Q3 |

| Crowne Plaza | 72.39 |

| Candlewood Suites | 72.75 |

| Holiday Inn | 75.60 |

| Holiday Inn Express | 85.60 |

| Staybridge Suites | 95.04 |

| EVEN Hotels | 106.64 |

| Hotel Indigo | 116.86 |

| InterContinental | 133.70 |

| Kimpton | 188.68 |

Source: Average RevPAR calculated by author using SQL using data sourced from historical quarterly reports for InterContinental Hotels Group (2022 Q1 to Q3).

From the above, we can see that the Kimpton brand has yielded the highest average RevPAR across both periods, with 2022 levels having almost reached levels seen in 2019.

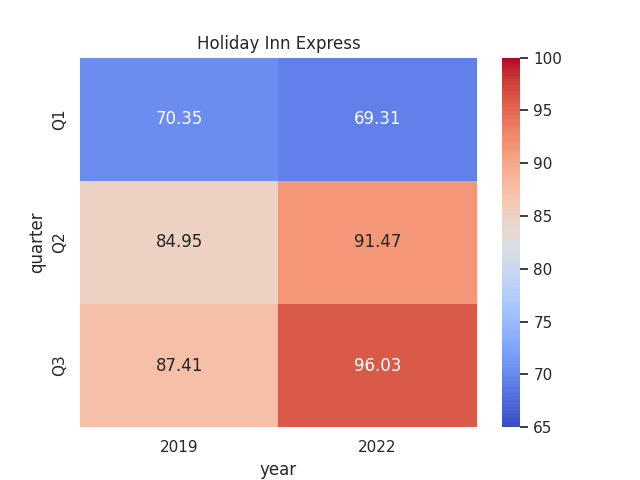

That said, the Holiday Inn Express brand (which is the largest brand for the Americas by number of hotels) has seen its average RevPAR in 2022 exceed that of 2019 levels.

Overall, the data is encouraging, as it indicates that customers still have a high propensity to spend on hotel bookings in spite of inflationary pressures.

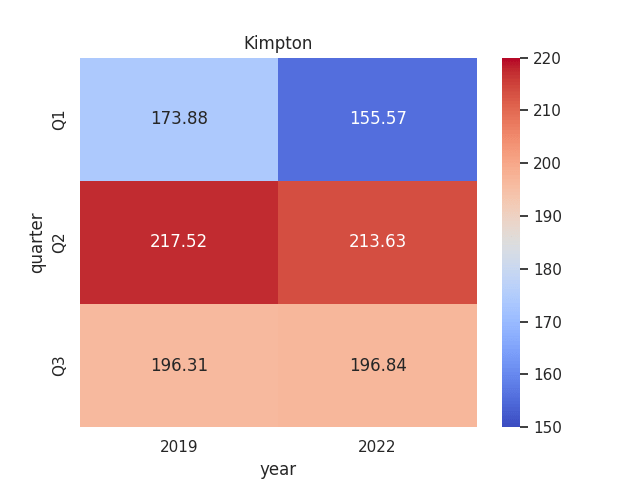

For instance, when we look at a heatmap of RevPAR by quarter for both the Kimpton and Holiday Inn Express brands, we can see that Q3 2022 RevPAR has rebounded to Q3 2019 RevPAR in the case of Kimpton, and exceeded Q3 2019 levels in the case of Holiday Inn Express.

Kimpton – RevPAR by quarter

Figures sourced from previous InterContinental Hotels Group Quarterly Reports. Heatmap generated by author using Python’s seaborn library.

Holiday Inn Express – RevPAR by quarter

Figures sourced from previous InterContinental Hotels Group Quarterly Reports. Heatmap generated by author using Python’s seaborn library.

From this standpoint, I am optimistic that RevPAR still has further room to grow. Particularly, even if we start to see pressure on mid-priced brands as a result of macroeconomic pressures – the Kimpton brand has shown strong RevPAR growth even when this brand has the highest ADR (average daily rate). This indicates that customers booking such luxury brands are not as price-sensitive and thus we can expect that this segment of the market will continue to see growth.

Looking Forward

Going forward, should we see continued RevPAR growth across major brands in Q4, then this could be a catalyst for further upside as InterContinental Hotels Group would be further demonstrating that the company is capable of boosting revenues even during periods of seasonally lower travel demand.

Additionally, while COVID lockdowns in China have previously been a concern for InterContinental Hotels Group – the lifting of COVID restrictions in that country as well as the resumption of travel abroad by Chinese citizens is expected to allow for a significant boost in RevPAR across the Chinese market – and the reopening of international travel for China could also result in a revenue boost across the Americas and EMEAA.

With regards to my previous point about investors ultimately expecting higher earnings and a reduction in long-term debt to drive growth for the stock going forward, I take the view that the continued RevPAR growth that we have been seeing should ultimately allow the company to reduce long-term debt while also outpacing inflationary pressures in order to lift overall earnings.

Conclusion

To conclude, InterContinental Hotels Group has seen strong growth in RevPAR, and this trend has continued even in the face of rising prices.

From this standpoint, I continue to take a long-term bullish view on InterContinental Hotels Group.

Be the first to comment