Mary Wandler/iStock via Getty Images

Introduction

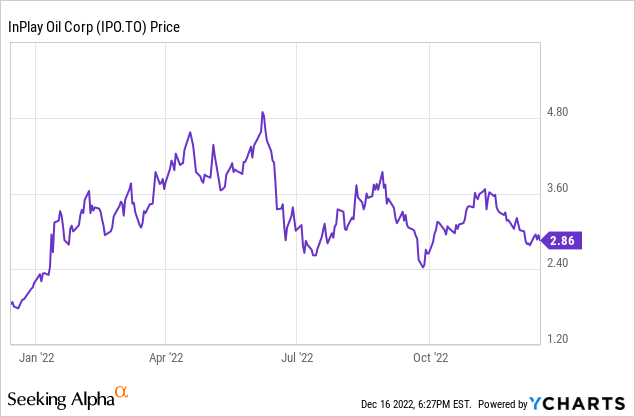

I have been following InPlay Oil (TSX:IPO:CA) (OTCQX:IPOOF) for quite a while now here on Seeking Alpha and although I just ‘accidentally’ ended up with a long position after InPlay acquired Prairie Storm Resources in a cash-and-stock deal, I actually added to my position throughout 2022. Anytime I wanted to sell the position, I just looked at the numbers and not only did I decide to not sell, I added to my position and I believe the current share price below C$3 offers an excellent entry point.

The third quarter was good and even Q4 should be reasonable

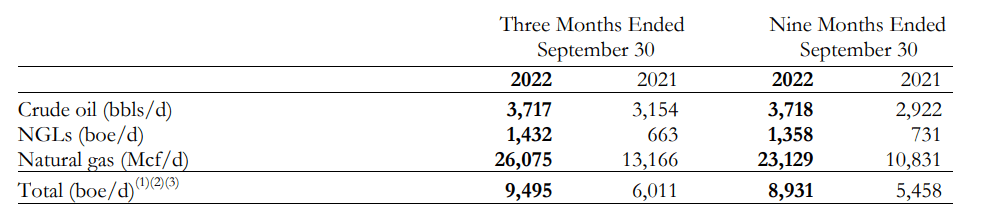

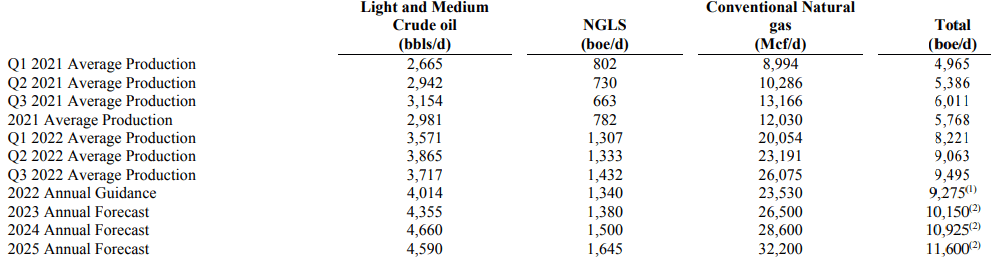

InPlay Oil produced just under 9,500 barrels of oil-equivalent per day during the third quarter and approximately 46% of these oil-equivalent barrels actually consisted of natural gas.

InPlay Oil Investor Relations

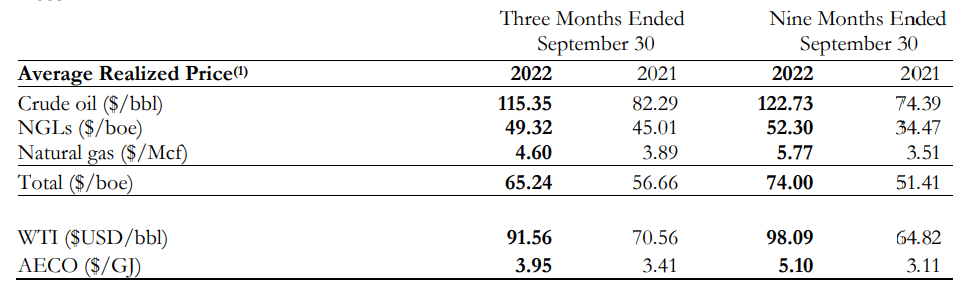

During the quarter, InPlay reported a realized revenue of just over C$115 per barrel of oil while the realized natural gas price came in at C$4.60. While that’s substantially lower than the in excess of C$6 in the first semester, this actually provides a more realistic long-term natural gas price, not unlike the natgas price in the mid C$4 range InPlay is using in its own long-term guidance.

InPlay Oil Investor Relations

Unfortunately – as far as I’m aware – InPlay sells all of its natural gas into the AECO market and there’s no real diversification to take advantage of the US prices for the natural gas.

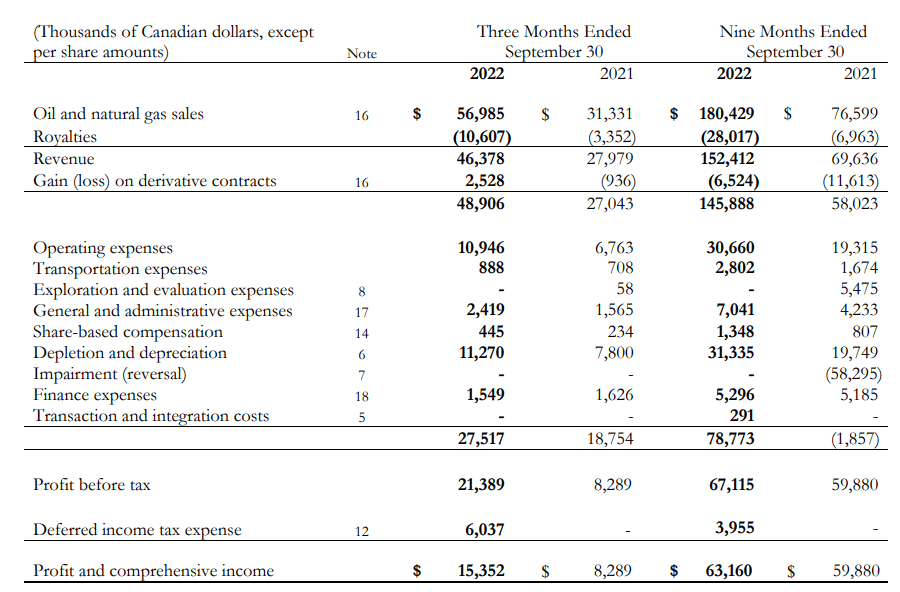

The total revenue in the third quarter was approximately C$57M and after deducting the royalties and adding the net gain of C$2.5M on the hedge book back to the equation, the reported net revenue was just under C$49M.

InPlay Oil Investor Relations

The total production and operating expenses remained low at approximately C$27.5M. approximately 40% of all operating expenses were related to the depletion and depreciation expenses and as you can also see in the income statement above, the transportation expenses are very low and this helps InPlay Oil to report very strong margins despite the lower natural gas price.

Indeed, the net income came in at C$15.4M, for an EPS of C$0.18 per share. The 9M 2022 EPS was C$0.73 per share and the full-year EPS will now likely come in at around C$0.95-1.00 per share as the impact of the lower oil price should be compensated with the higher realized natural gas price.

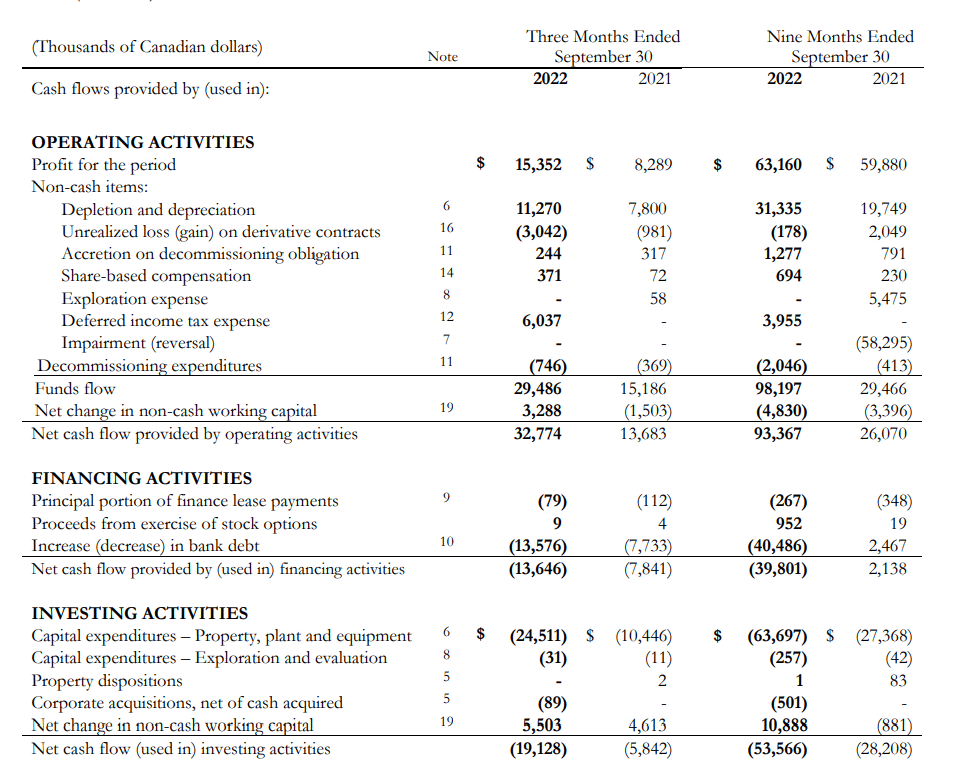

The cash flow statement is more reliable as it ignores the impact of the hedge gain. The reported funds flow before changes in the working capital position was C$29.5M. This excludes the C$6M in taxes as InPlay Oil won’t have to pay taxes in the near future, but includes the C$0.5M realized hedging loss (while the unrealized C$3M hedging gain was deducted from the cash flow statement).

InPlay Oil Investor Relations

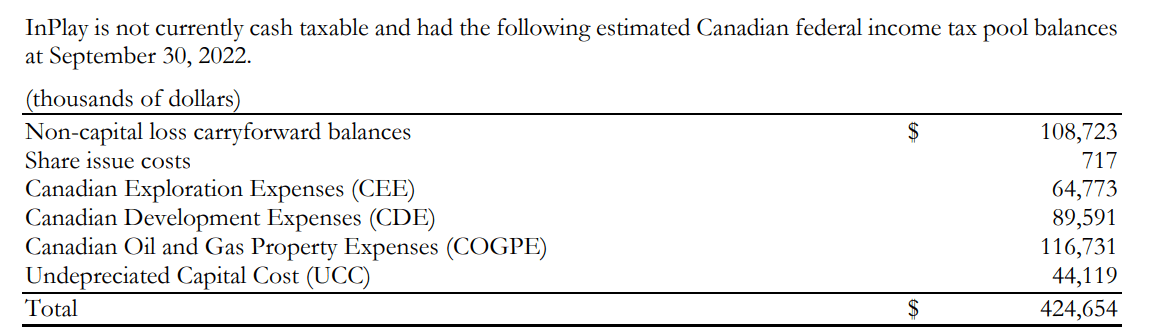

As the company confirmed it still has plenty of tax pools available (see below) which should shield InPlay from having to make substantial income tax payments in the next few years, I will – for now- accept the C$29M in adjusted funds flow as ‘base case scenario’ for the third quarter.

InPlay Oil Investor Relations

The total capex was C$24.5M but keep in mind that’s mainly because InPlay accelerated its drilling and development plans during the third quarter. The full-year capex is anticipated to be C$70-72M, which represents just C$18M per quarter on average. And as you’ll be able to see in the overview below, the capex will remain relatively stable: it will decrease in 2023 before slightly increasing again in 2024 and 2025. This means the Q4 capex will be less than C$10M, indicating InPlay Oil will likely generate approximately C$20M in free cash flow in the final quarter of this year. Perhaps even more if the production rate indeed comes in at 10,000 boe/day or even slightly higher.

As the strong cash flow this year has helped InPlay Oil to strengthen its balance sheet (the net debt has decreased to just C$38M and should drop below C$20M by the end of this year), InPlay has now started to pay a monthly dividend of 1.5 cents per month. This will cost the company approximately C$16M per year and requires just a small portion of the anticipated free cash flow.

I’m particularly charmed by the longer-term outlook provided by the company

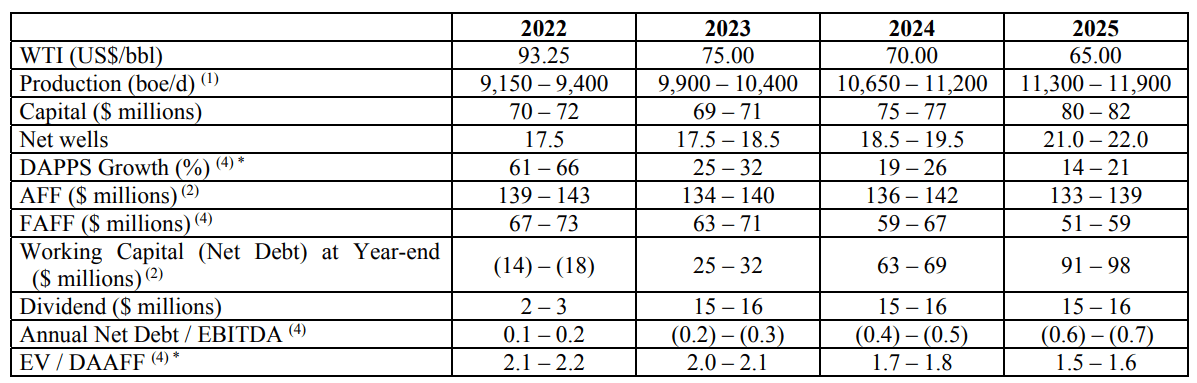

The main reason why I recently added to my InPlay position wasn’t the strong Q3 result or the new monthly dividend. It was the 2023-2025 outlook that convinced me to increase my exposure. Not only because it is a realistic mid-single digit production growth program, but mainly because I was charmed by InPlay’s decision to use conservative oil prices for the next few years.

InPlay Oil Investor Relations

As you can see in the table above, InPlay is using a gradually decreasing oil price. In 2024 for instance, IPO uses an average WTI oil price of $70 per barrel and yet it still expects to generate C$136-142M in adjusted funds flow resulting in C$59-67M in free cash flow after deducting the C$75-77M in planned capex (which includes the growth capex).

Based on the guidance for 2025 with an oil price of $65 per barrel and a free cash flow of C$51-59M, even the lower end of that guidance with a free cash flow of C$51M would still represent a free cash flow result of C$0.59 per share. That makes the current share price of roughly C$2.80 undervalued from pretty much any perspective. Especially as the balance sheet would contain in excess of C$1/share in net cash at that point.

There’s only one caveat here: unfortunately InPlay only released a sensitivity analysis based on changing oil prices. While the US$65 WTI oil price used for 2025 may be conservative, readers are warned the company used an average AECO natural gas price of C$4.65 for that year (and C$4.50 for 2024). Considering about 46% of the anticipated 2025 production (and 44% of the 2024 production estimate) will consist of natural gas, it’s important to know what natural gas price InPlay used for its guidance.

InPlay Oil Investor Relations

Investment thesis

I think InPlay Oil remains exceptionally cheap at the current levels. Considering the stock is trading at less than 5 times the anticipated free cash flow result in 2025 using $65 oil and C$4.5 natural gas and considering 1/3rd of the current market cap will consist of net cash by then, the stock is attractively priced. The current dividend yield is in excess of 6%, which is a nice compensation while waiting for a higher share price.

I am looking forward to seeing the updated reserve calculation at the end of this year and the 1P and 2P NAV/share as I expect the 1P NAV to be higher than the current share price while the 2P NAV could easily be three times the current share price.

I have a long position in InPlay Oil and I continue to add on weakness as long as the oil and gas prices don’t completely collapse.

Be the first to comment