FatCamera

Article Thesis

Innovative Industrial Properties (NYSE:IIPR) is a specialized REIT that has seen its shares come crashing down over the last year. Today, in the low $90s, the REIT offers a dividend yield of 7.5%. Not a lot of growth is needed for a stock to be a solid longer-term investment when the dividend yield is this high. IIPR isn’t a low-risk REIT, but the total return potential is compelling.

Overview

Innovative Industrial Properties is a REIT specializing in the cannabis industry. Its assets primarily include facilities where state-licensed operators can grow cannabis. Cannabis companies, even in states where doing business is fully legal for them, can oftentimes not access traditional financing easily. In many cases, accessing debt is not possible for them at all, as banks are still barred from doing business with cannabis companies under federal law. This is why cannabis companies can’t easily borrow money to build out their own facilities, which is why a company like IIPR is important for the industry, as it allows cannabis companies to get access to specialized facilities without them needing to borrow from banks.

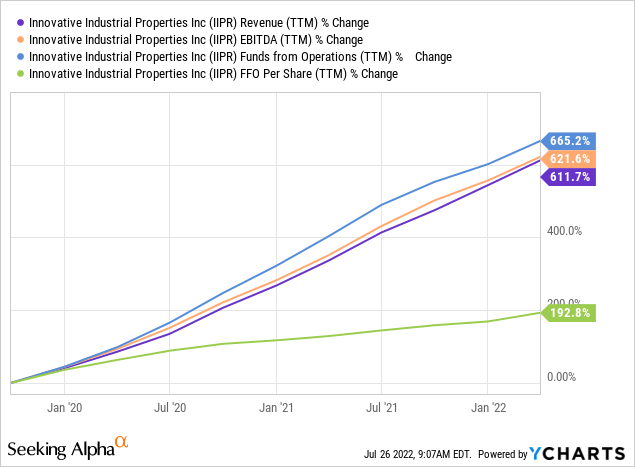

IIPR, in turn, benefits as well. Since cannabis companies oftentimes have no other viable way to get their hands on properties that are needed for their business, IIPR is able to demand high cap rates. The rent that Innovative Industrial Properties is able to demand is pretty high, relative to the cost of the properties that IIPR had to pay in the first place. At the same time, due to the relatively high growth rate of the cannabis industry in the United States, IIPR has ample growth potential. This combination of high profitability and a lot of growth potential is why IIPR has a compelling business and earnings growth track record:

Revenue, EBITDA, and funds from operations all rose by more than 600% over the last three years, which is outstanding. Funds from operations per share rose by 193%, which is significantly less, but still great — that pencils out to a 43% annual growth rate. The vast discrepancy between the company’s overall FFO growth of 670% and its per-share FFO growth of 193% can be explained by the fact that IIPR issued new shares in recent years. That is routine for many REITs, as the proceeds can then be used to acquire additional properties. Even strong and established REITs such as Realty Income (O) do so repeatedly, and as long as the acquisitions financed by share issuance are accretive, there’s no problem with this strategy. In IIPR’s case, the acquisitions clearly were very accretive, as FFO per share rose rapidly in recent years, despite the share issuance over that time frame.

Funds from operations hit a new record level over the last four quarters, both on a per-share basis as well as on a company-wide basis. And yet, Innovative Industrial Properties has seen its shares slump by almost 70% from the 52-week high that was reached in late 2021. There are several reasons for that. First, the valuation was pretty high one year ago. When IIPR traded at $288, it was valued at around 36x 2022’s FFO, which is a way-above-average valuation for a REIT. When one buys at a historically high valuation, multiple normalization naturally poses a threat to total returns.

Second, Innovative Industrial Properties was seen as an income investment by many investors. With interest rates rising, which makes treasuries more attractive, all else equal, some income stocks have come under pressure as investors are shifting some of their money out of income-producing equities. This likely has added to IIPR’s selling pressure in recent months.

Third, the company had some problems with tenants. King’s Garden, Inc., which is one of Innovative Industrial Properties’ tenants, has defaulted on rent payments on six properties in July. This resulted in a $2.2 million hit to IIPR’s cash flow, consisting of $1.8 million of rent and property management fees, and $400,000 of insurance premiums that were payable by the tenant as operating expenses. Now generally, a $2.2 million hit for a company worth $2.7 billion and generating $230 million in revenue over the last year is not a disaster. But the market naturally did not look at the $2.2 million in a vacuum.

Instead, the market value of IIPR declined due to two additional risks. It is, of course, possible that the tenant with problems, King’s Garden, will default on additional rent payments in the coming months, which could lead to added revenue hits in the coming months. King’s Garden’s rents make up around 8% of IIPR’s total rent proceeds, so a complete default on all future rent payments would have a more pronounced impact on IIPR’s cash flows. It should be noted, however, that IIPR would not get into liquidity problems in such a scenario, as 92% of rent would still get paid and since IIPR’s own debt levels are pretty low. The market is also looking at another risk, though. If King’s Garden is having problems paying contracted rent, then other tenants might have or get into similar issues in the coming months as well. There is no guarantee that all other tenants will forever be healthy.

In fact, the cannabis industry isn’t especially profitable, and even some of the largest players in the industry are having to cut back costs, are underperforming their own longer-term guidance/goals, and so on. Renting out facilities to cannabis companies that are oftentimes only marginally profitable or not profitable at all is not a low-risk business. In 2021, IIPR was priced like an ultra-low-risk REIT, but the market has changed course and is pricing some business risks into IIPR right now. To me, that makes sense, at least to some degree. Default risks, as well as regulation risks, are higher here, compared to many other REITs.

An Inexpensive Valuation And A Hefty Yield

That being said, following the selloff of almost 70%, IIPR is now trading at a rather low valuation. Based on current estimates, Innovative Industrial Properties is currently valued at 11.5x forward funds from operations. For a REIT that has grown its FFO per share by almost 200% over the last three years, that’s a pretty low valuation.

Since Innovative Industrial Properties pays out the majority of its FFO via dividends, investors get a pretty nice dividend yield of 7.5% at current prices. Even if that dividend were not to get raised in the coming years, the income stream would be compelling. Relative to the overall payout of $4.32 in 2021, Innovative Industrial Properties is on track to pay a 62% higher dividend per share this year, which is a hefty growth rate. I do not believe that dividend growth will continue at that level, but even a way lower dividend growth rate of 3% annually could result in 10%+ annual returns, before valuation changes. Since IIPR operates with average annual lease escalators of 3%, a 3% annual dividend growth rate could be achieved even if IIPR were to never make an acquisition again.

Takeaway

We can say that IIPR has compelling total return potential and offers a nice dividend yield. But since additional problems with other tenants might emerge over time, IIPR is not a low-risk REIT. The STATES Act (or something similar), if passed, could also improve the access to financing for cannabis companies. In that case, they could build out their own properties more easily and might be less inclined to pay the hefty cap rates that IIPR is demanding. IIPR thus has above-average business risks, I believe. But with higher risk, investors oftentimes get higher return potential, and that is indeed attractive for IIPR. The dividend yield alone makes for a compelling return, and between rent escalators, more property acquisitions, and potential multiple expansion from the current pretty low valuation, IIPR could have substantial longer-term upside potential. IIPR is forecasted to earn $9.30 next year — put a 14x multiple on that, which would be far from outrageous, and shares could climb by 40% over the next 18 months on top of offering a nice income stream.

For investors that have an appetite for risk, IIPR thus has merit. I do believe that it’s not a great sleep-well-at-night stock, however.

Be the first to comment