jetcityimage/iStock Editorial via Getty Images

Infosys (NYSE:INFY), India’s second-largest consulting and IT services provider, recently held an investor meeting outlining the next phase of CEO Salil Parekh’s strategic plan. Unsurprisingly, the focus revolved around digital initiatives and capabilities across emerging growth areas like the cloud, metaverse, and quantum computing. While the structural growth drivers discussed during the meeting could prove relevant over the medium term, management did not account for a potential cyclical slowdown in the next year or so, and therefore, I see downside risk to near-term estimates. In addition, it remains unclear how margins will develop in light of the ongoing talent shortage situation, which has driven a wave of promotions and wage hikes in recent quarters to bring down attrition rates. While shares have corrected from prior highs, valuations remain expensive at a c. 20x EPS, leaving INFY vulnerable to further downside in the upcoming months.

Looking Ahead to the Next Era of CEO Salil Parekh’s Reign

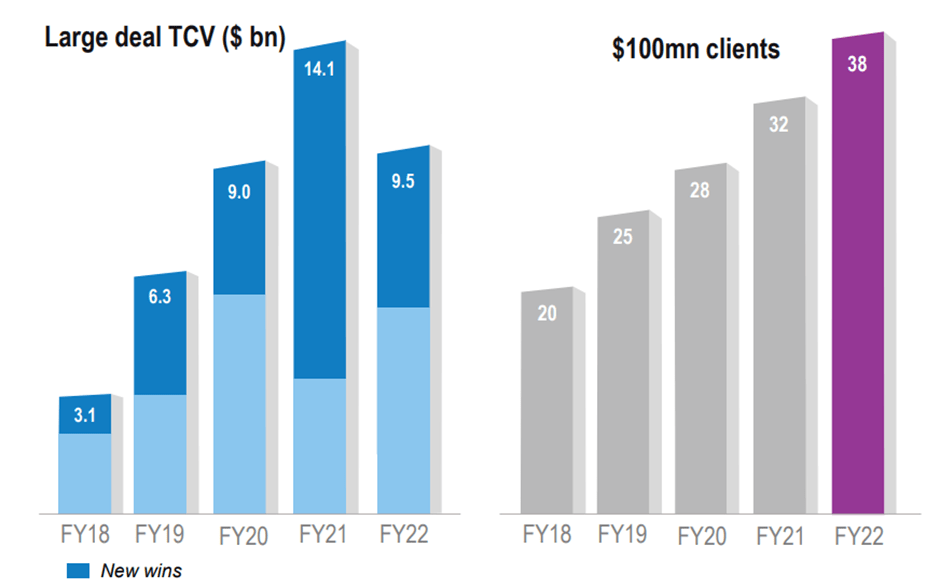

The latest INFY investor meeting kicked off with CEO Salil Parekh’s performance report card on the strategic road map laid out in 2018. On all three counts (“Stabilize” in fiscal 2019, “Build Momentum” in fiscal 2020, and “Accelerate” in fiscal 2021), Mr. Parekh has passed with flying colors. The headline numbers bear this out as well – INFY has seen a significant growth acceleration to an industry-leading +20% Y/Y in fiscal 2022 on the back of increasing large customer ($100+ million accounts) wins. For its next leg of growth, INFY will focus on scaling cloud, building up its capabilities in digital and new technologies (e.g., Metaverse, Web 3.0), along with expanding into Europe. Internally, INFY also is pushing for more automation and modernization of its processes and improving its people care and development (e.g., through faster career progression and leadership development). Interestingly, INFY management does not see growth slowing anytime soon. Having added 94 large deals ($50+ million contract value) and $9.5 billion in total contract value in fiscal 2022, management has guided to these accounts driving further growth and account expansion heading into fiscal 2023/2024.

Infosys (Investor Presentation Slides 2022)

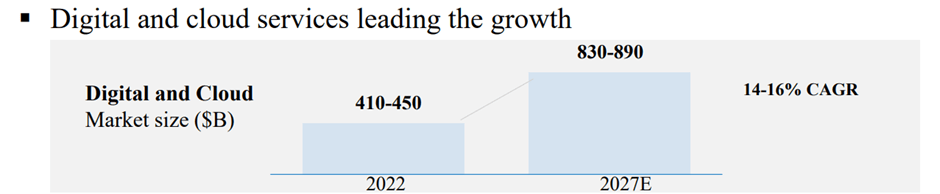

Compared to the medium-term outlook for global tech spending growth of 5-6%, INFY also cited cloud and digital market growth at 14%-16% and rising to $830-890 billion by fiscal 2027. Its Cobalt cloud offering was singled out as the flywheel to scale digital, with over 300 industry solutions and 35k cloud assets providing it an edge in the market. Thus far, 25 of its 60 digital services generate a $100 million revenue run rate annually, and therefore, management has prioritized scaling up all 60 services to a c. 100 million run rate with its Cobalt 2.0 strategy. Europe will also be a key growth driver and source of diversification- major EU companies have been more willing to explore digital transformation and a global delivery model, providing INFY the opportunity to accelerate its expansion into key European territories.

Infosys (Analyst Meet 2022 (CEO Presentation))

Walking the Growth/Margin Tightrope

In light of the current demand strength, INFY has been rightly prioritizing growth over margins to capitalize on opportunities in this stage of the demand cycle. As a result, the company has seen a downtrend in utilization levels, increased usage of sub-contractors, and increased lateral hiring, all of which have resulted in margin pressures. Encouragingly, management has cited improvements in the onsite mix, pyramid rationalization, lower subcontracting costs, increased automation, and operating leverage as key margin levers to offset further wage increases.

Infosys (Analyst Meet 2022 (HR Presentation))

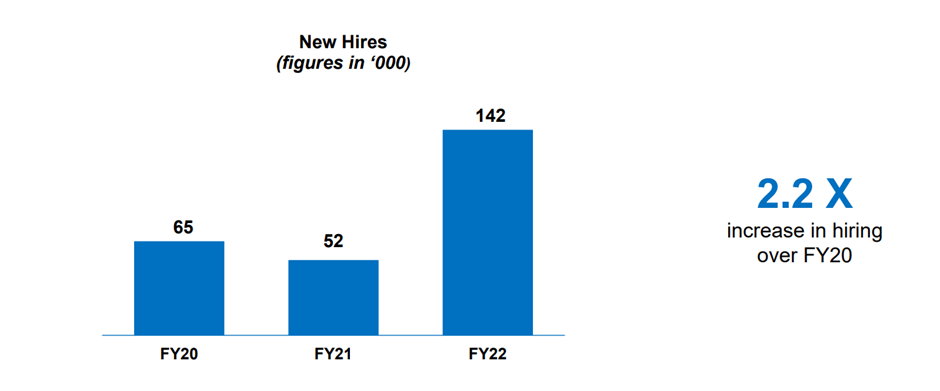

However, I would note that INFY’s significantly higher hiring in fiscal 2022 is cause for concern – the 142k employees added in fiscal 2022 (including its highest ever intake of freshers at 85k) is almost triple fiscal 2021 levels. Furthermore, to meet the higher demand and offset elevated attrition levels, INFY has been forced to tap into additional geographies through its localization efforts to access additional talent pools. Thus far, the company has opened new centers in four additional locations in India. While the ability to scale hiring is crucial to being able to keep pace with the strong demand environment, it also could prove to be a drag on margins in a weaker demand backdrop. Longer term, the use of automation and AI to improve productivity and efficiency internally could pay off, but for now, I remain concerned INFY’s emphasis on growth over margins could backfire as enterprise budgets suffer massive cuts in the upcoming months.

Riding the Industry-Wide Turbulence Ahead

The Indian IT services industry has seen some very rosy numbers in recent years, with record contract value and deal pipeline numbers driving shares to new highs. However, global economic growth is slowing, and this could translate into enterprise budget cuts amid significant earnings pressure across key end markets. With tighter spending, expect recalibration of digital spending in the upcoming months as clients reprioritize. Note that this does not account for a recession scenario in fiscal 2023/2024, which could result in an even bigger reset.

Infosys (Analyst Meet 2022 (President Presentation))

Through the turbulence, INFY should outperform – while customers tend to be more open to new vendors in the initial phase of a new tech cycle, vendors with scale tend to benefit as the cycle matures and the industry consolidates. As such, in times of uncertainty, I would favor Tier-1 players like INFY and Tata Consulting, as they stand to benefit from vendor consolidation and cost optimization-related opportunities. Over the long run, INFY also is better positioned to serve customers looking for revolutionary transformation considering its multi-vertical exposure and deeper domain expertise, boosting its value proposition.

Final Take

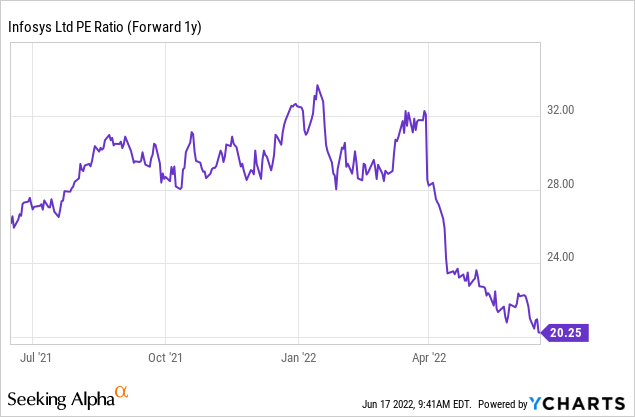

As the industry leader in Indian IT services, INFY is well-positioned for industry-leading growth and further share gains as it continues to build out strong digital business capabilities in the upcoming years. However, I’m concerned about the demand risk ahead amid potential macro headwinds from a prolonged economic slowdown/recession scenario in client markets. This could manifest in lower client profits as soon as fiscal 2023/2024 and consequently drive downward revisions to consensus revenue growth and EPS estimates ahead. Furthermore, as INFY management has emphasized no risk to its 13%-15% constant currency revenue growth guidance for fiscal 2023, expectations have likely not been appropriately reset. Overall, I’m neutral on INFY shares – even though valuations have de-rated considerably from prior peak levels, at c. 20x forward EPS numbers, the shares remain vulnerable to downside risk in the upcoming months.

Be the first to comment