Sean Gallup

After our Q2 analysis of STMicroelectronics (NYSE:STM), today it is time for Infineon Technologies AG (OTCQX:IFNNY) (OTCQX:IFNNF). The company just released its half-year report and we were just over with the analyst call.

Following STM results, Infineon delivered a strong quarter with top-line sales and margins ahead of the consensus expectations. Looking at the details, these positive results were achieved thanks to Infineon’s pricing power, improvement in the supply chain and favorable currency developments. In numbers, turnover and adjusted EBIT margin results were ahead of expectations by 5.5% and 15.5% respectively.

Why we are positive about Infineon? No buy case recap today. Here are the main links to our previous publications:

- Initiation of coverage with MACRO to MICRO reason to own the company;

- Q2 results analysis.

Q3 Results

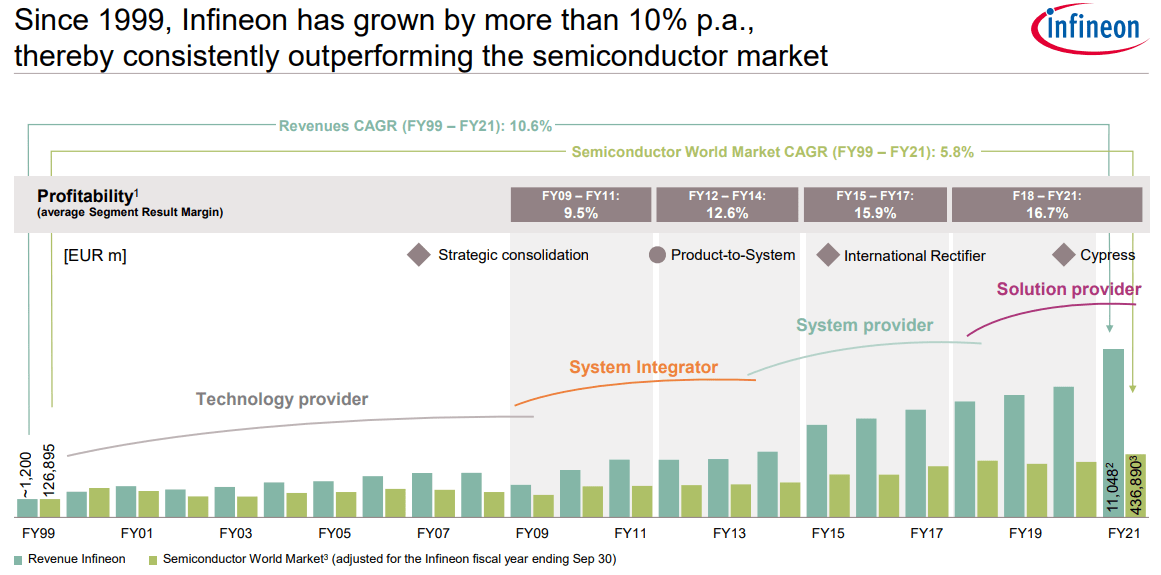

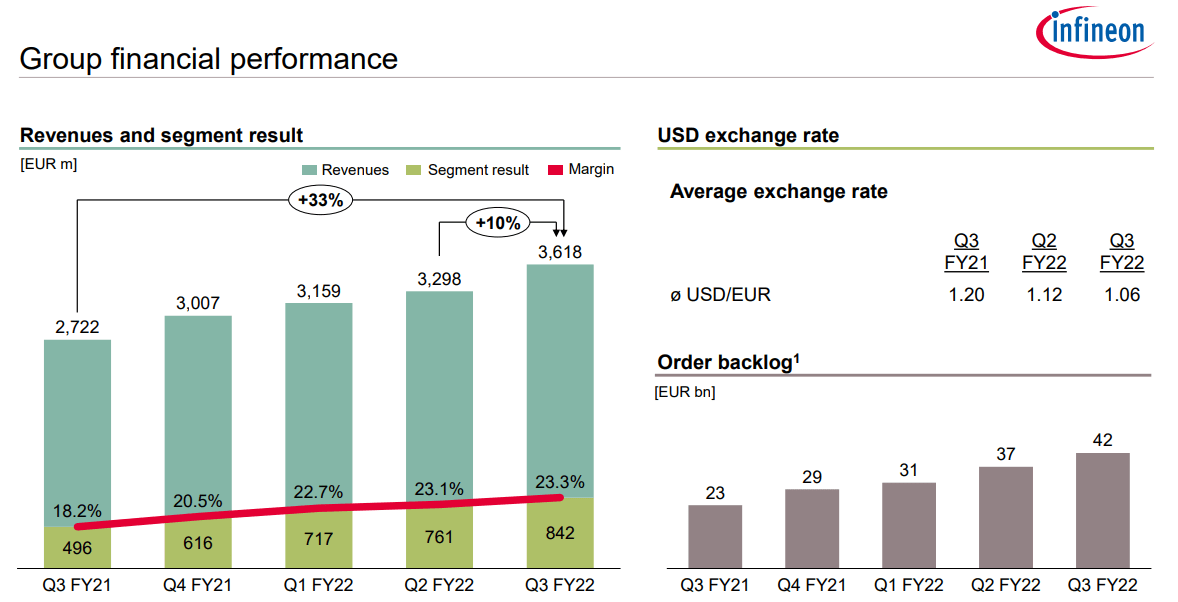

Below we present two snaps that are worth more than many explanations. The chip manufacturer has a strong track record within the sector and the Q3 financial result is just another proof of it.

Infineon track record

Source: Infineon Technologies AG Q3 results

Infineon financial snap

Source: Infineon Technologies AG Q3 results

During the earning season here at the Lab, we usually provide Wall Street expectation discrepancy. Not today, long story short Infineon not also beats consensus in every P&L line, but the company achieved a superior performance at the divisional level and raised the bar for future guidance.

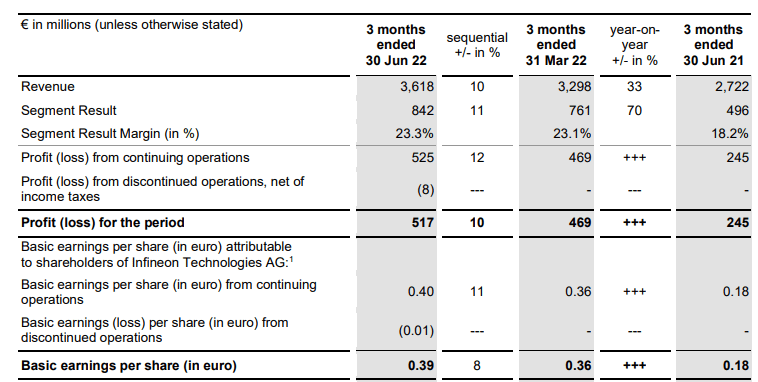

Looking at the Group performance, revenue increased by 10% compared to the previous year’s end quarter. This was driven by the Automotive and Power & Sensor Systems division, but a good performance was also achieved in the Connected Secure Systems and Industrial Power Control division. The strong outcome achieved in the gross margin and also in the adjusted operating profit margin were the results of higher selling prices over raw material inflationary pressure. Thus, despite the period, Infineon recorded an adj. EBIT margin of 23.3% compared to the 23.1% achieved in the same quarter last year. Thanks to the company’s pricing power we are even more confident in our base case scenario valuation.

Infineon P&L numbers

Source: Infineon Technologies AG Q3 press release

Aside from the financial consideration, the management has provided more color for the company’s future estimates. In details:

- The client’s inventories are at a normal level;

- Supply chain constraints are easing around the globe;

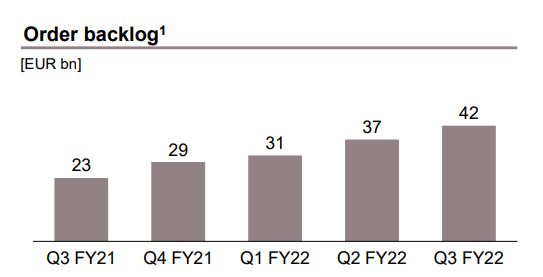

- Order backlog is very supportive and there are positive trends by end markets – in fig. 1, we see a 13% increase on a quarterly basis, but if we do the math on a yearly basis, we derive a plus 82%. That’s incredible.

- Despite the energy turmoil, the company will be a beneficiary of new renewable projects coming online;

- There are assured expectations for the Automotive sector;

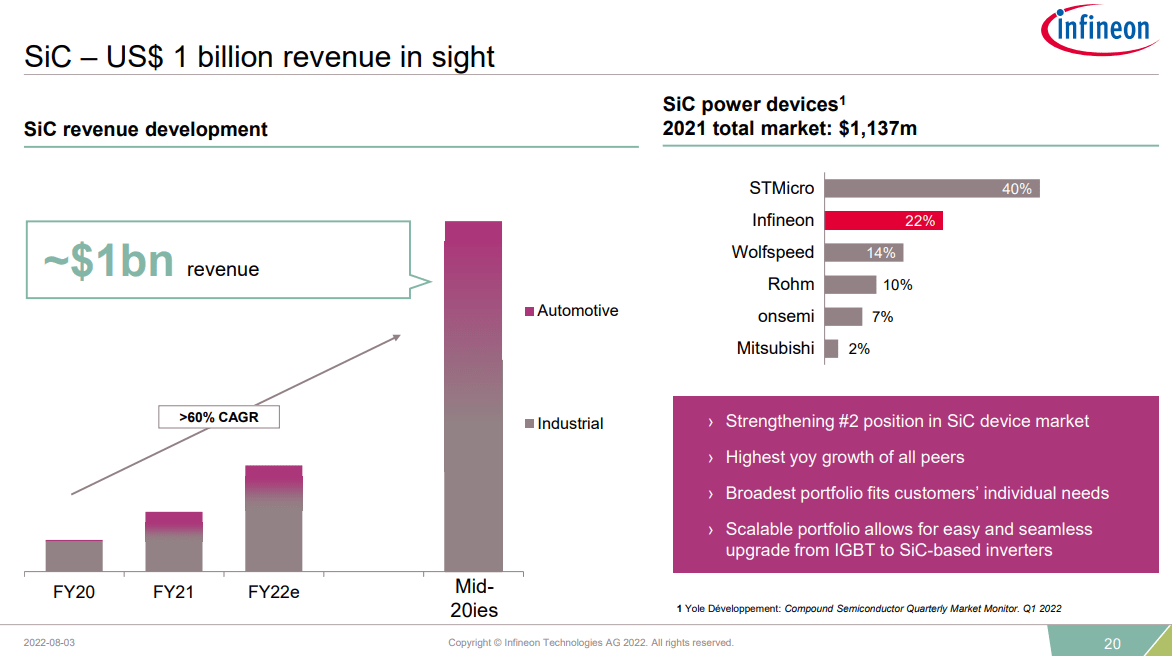

- Thanks to the just updated presentation, we see supportive news on SiC’s new wins (Fig 2).

Infineon order backlog

Source: Fig 1 – Infineon Technologies AG Q3 results

Infineon SiC wins

Source: Fig 2 – Infineon Technologies AG Q3 results

Conclusion and Valuation

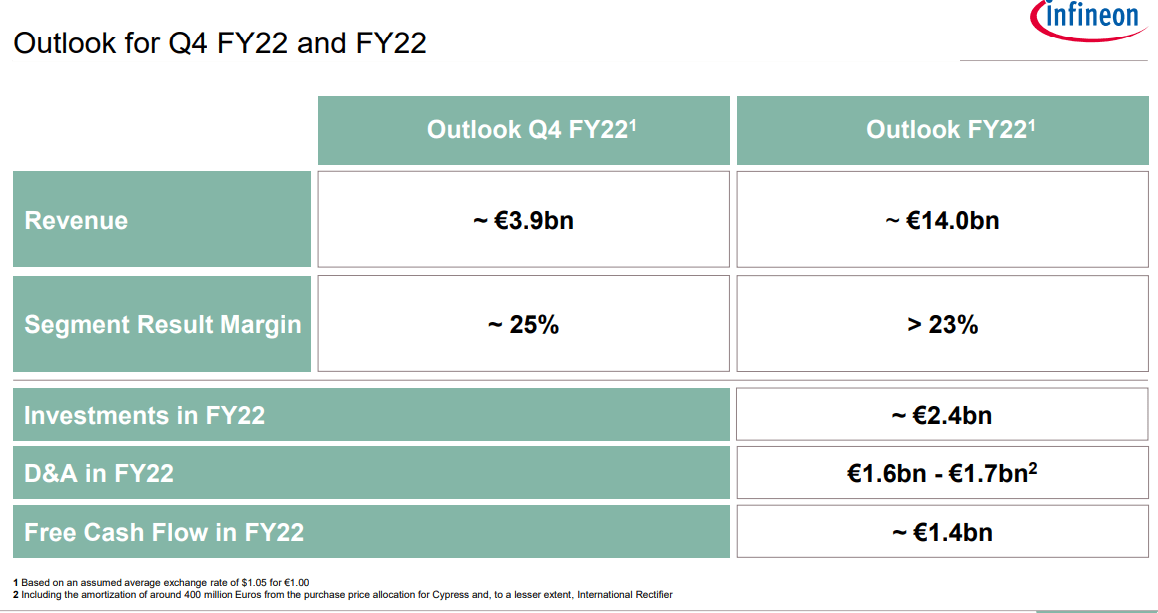

For the year, the German chip manufacturer raised its revenue forecast from €13.5 billion to €14 billion and more importantly raised the adj. operating margin from 23% to 22%. The adjusted EBIT outlook is now at €3.2 billion. Infineon is trading at a 2023 adj. P/E of 14x. With this super order backlog and a higher FCF generation (previous estimate at €1.1 billion), we reaffirm our valuation. This discount versus its historical average is totally not justified.

Infineon future guidance

Source: Infineon Technologies AG Q3 results

Be the first to comment