RomoloTavani/iStock via Getty Images

Co-produced with Treading Softly

I’m not kidding. 40% of the Gross Domestic Product and employing 40% of America’s workforce is directly tied to Middle Market firms. Another fun fact? Only 20% of all middle-market firms are publicly traded. This means that 80% of these firms are not readily investable for the average retail investor.

These firms are highly attractive to private equity for a reason – they are often less well known, trade at attractive return multiples, and are in the middle of their growth. Unlike micro-caps, or start-ups looking for venture capital, most middle-market firms are firmly generating positive cash flow and working on expanding. They often are filled with the classic strong entrepreneurial spirit that helped make the U.S. economy the powerhouse it has been globally for decades.

So “the why” investors want exposure to these companies is simple:

- More attractive values

- Positive cashflow

- Looking to expand or grow their operations.

So how can I, or you, start buying up our portion of this American economic engine?

That’s a great question.

Let’s take a look at two routes to do so:

Pick #1: RVT, Yield +9%

With the Fed raising rates and the market fearing a recession, fear is in the air and driving prices lower. As long-term investors, we know that such fear never lasts forever. You want to be buying so that you own more shares when the rebound occurs. With strong fundamentals supporting them, we expect value stocks to outperform growth during the rebound. To capitalize on the rebound, with a focus on small-cap Value stocks, Royce Value Trust (RVT) is an excellent option. RVT is a CEF (Closed-End Fund) built as an amalgamation of elements that position your portfolio for soaring investment returns as the markets recover.

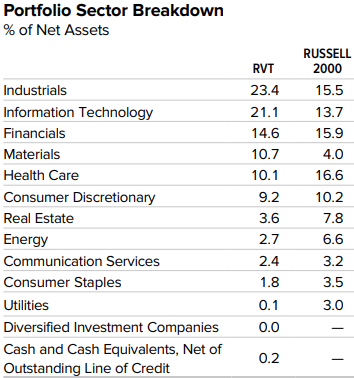

RVT is built to last, with a highly diversified portfolio of over 489 securities in the small-cap value segment. Industrials and Information Technology represent the largest portion of this CEF (almost 45%), and we saw earlier that these sectors tend to do well in a market recovery.

Fact Sheet

RVT’s portfolio is built overwhelmingly with U.S.-based companies (90% of the portfolio). Canadian securities represent ~7%, and companies from all other countries do not individually form more than 0.5% of RVT’s portfolio. The U.S. is home to the largest stock exchanges globally and continues to be the investment oasis of the investment world. Strong exposure to U.S. companies positions RVT for better and quicker recovery when the bearish streak ends.

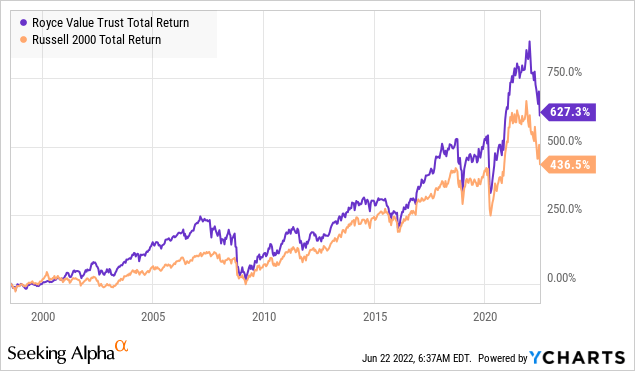

No matter how experienced the fund managers are and how carefully they craft RVT’s portfolio, its stock price movement will correlate with the broader market. The CEF isn’t immune to bear markets and steep corrections. However, we discussed before that RVT is one of the best amalgamations of those sectors that outperform during a broader market recovery. As such, the CEF has demonstrated consistent outperformance following past bear markets and steep corrections. Over the long haul, RVT has a proven ability to outperform the Russell 2000 index.

RVT’s distributions are variable due to its managed distribution policy. The quarterly distributions are calculated at an annual rate of 7% of the average of the prior four quarter-end NAVs. In the fourth quarter, RVT will pay out extra if it is required by IRS regulations as a year-end special distribution. These are most common in years following a crash as RVT has excess gains during the recovery.

RVT is an ideal CEF for sustainable distributions through NAV preservation over time. When NAV is high, shareholders are rewarded immediately. When NAV declines, the distribution will reduce ensuring that RVT is not forced to sell shares in a down market, protecting NAV so they benefit the most from the rebound. At the same time, the strategy of using an average of the past four quarters means that there is reasonable stability. The dividend doesn’t simply collapse because of one bad quarter, it will drift down, and then when NAV recovers it will start drifting back up.

Shareholders can be assured that the dividend is not eating NAV into oblivion, while also knowing that when the good times come, they will be rewarded with a generous rising dividend.

Pick #2: ARCC, Yield +10%

When the market starts getting fearful over recession risk, it isn’t much of a surprise that “credit risk” investments like BDCs (Business Development Companies) join the sell-off.

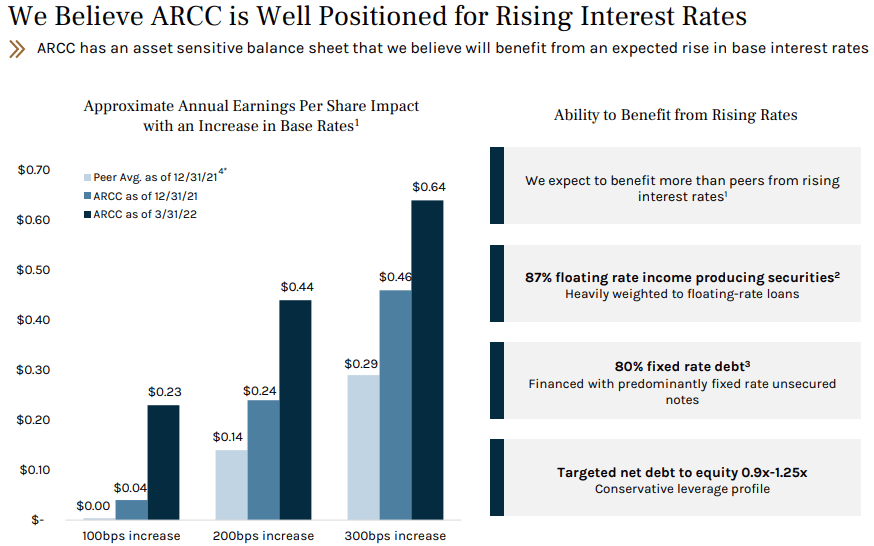

Ares Capital (ARCC) is holding up much better than the market indexes, year-to-date, but is still about 20% off of highs. The irony is that this decline occurred at a time the market is fearful of rising rates. For ARCC’s business, rising rates are a boon that will drive higher profits. (Source: Ares Capital Corporation’s 2022 Analyst Day)

Ares Capital Corporation’s 2022 Analyst Day

Let’s put ourselves in the shoes of the bears. With interest rates rising, why would you sell off a company that directly benefits from rising rates? Well, ARCC is in the business of lending money, and so if you are worried that companies might default, then you might want to avoid lenders in general.

This recession fear is likely what has caused ARCC to sell off. Is that a good reason to sell? I don’t think so. ARCC is absolutely the kind of BDC that I want to hold through a recession.

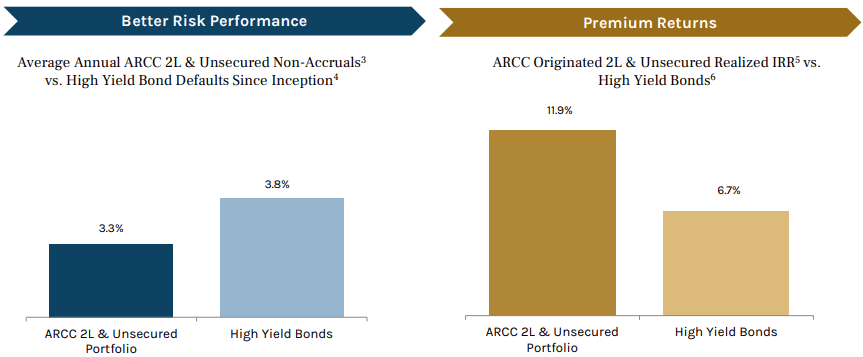

ARCC is the largest publicly traded BDC. As such, it has the scale to pursue deals with larger companies. Their average portfolio company has an EBITDA of $129 million. Investing in larger companies that are well established with regional or even national brands, reduces risk. ARCC’s results since its inception in 2004, which includes the disruptions of the Great Financial Crisis and COVID, are nothing short of stellar.

Ares Capital Corporation’s 2022 Analyst Day

ARCC has managed to have fewer loans stop paying while receiving a materially higher return than seen with high-yield bonds. Clearly, ARCC has a history of very solid underwriting.

Yet even that is not ARCC’s true strength. What sets BDCs apart from other lenders is the practice of making equity co-investments. A BDC is not just a lender that will run to bankruptcy court and be looking only to “mitigate” losses. BDCs are part equity owners in their portfolio companies. When things get tough, and borrowers stop paying, is precisely the time when ARCC’s business model shines.

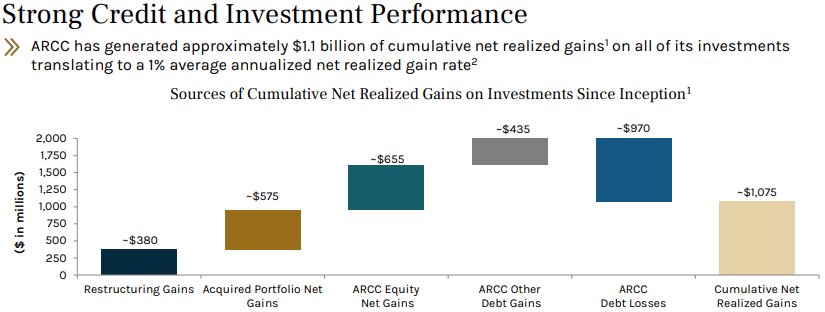

Since its inception, ARCC has netted nearly $1.1 billion in gains after accounting for debt losses.

Ares Capital Corporation’s 2022 Analyst Day

Banks and bondholders don’t even try to get these gains. A borrower defaults, and they simply start trying to grab money, often when the borrower needs it the most to survive. ARCC doesn’t look at the situation through a lender’s lens, just looking to get back capital. ARCC looks at it as an investor. The question is not “how can we get our principal back.” it is “how do we maximize our total return”?

ARCC will assess the business and take the steps that will maximize its return. Sometimes that means convincing the majority shareholders (usually a private equity sponsor) to sell the company, where ARCC gets to collect first as a lender. Other times, it means taking ownership of the company through bankruptcy or voluntary restructuring and recapitalizing it with ARCC as the primary equity holder. In less severe cases, ARCC will negotiate with the Private Equity Sponsor to contribute more equity, or will restructure the debt in a way that helps immediate cash flow but pays ARCC more in the future.

The bottom line is that ARCC lends to companies that they believe in, both in their ability to repay the loans, but also that they will thrive as sustainable businesses. When the economy provides lemons, ARCC looks for ways to create lemonade. Something that it has a long history of doing successfully.

So when ARCC’s price dips, I go on the offense and buy more, knowing that this is a blue-chip BDC that can handle any environment.

Dreamstime

Conclusion

With RVT and ARCC, we can invest directly in the middle-market business sector of the U.S. economy. RVT covers the portion that are publicly traded, while ARCC focuses on those that are private.

RVT has a long and storied history of strong returns and great income. It is a variable payer and investors need to be aware its dividend will grow or shrink solely based on its underlying NAV.

ARCC is one of, if not the best, top-notch BDCs available to purchase in today’s market. They have a proven track record of success and returning large sums of cash to their shareholders.

I have long learned it is a mistake to vote against the American work ethic found within the U.S. economy. With middle-market firms, individual employees can still see the impact their efforts make while also being part of a company with a proven track record – the sweet spot between higher risk and little return left to see.

This allows my income portfolio to enjoy high levels of income now, while still supporting the economy I benefit from day to day. Retirement will pay for itself and my hobbies via dividends. Will yours?

I’m investing in the engine that drives 40% of the U.S. GDP, you should too.

Be the first to comment