Blue Planet Studio/iStock via Getty Images

Thesis and Background

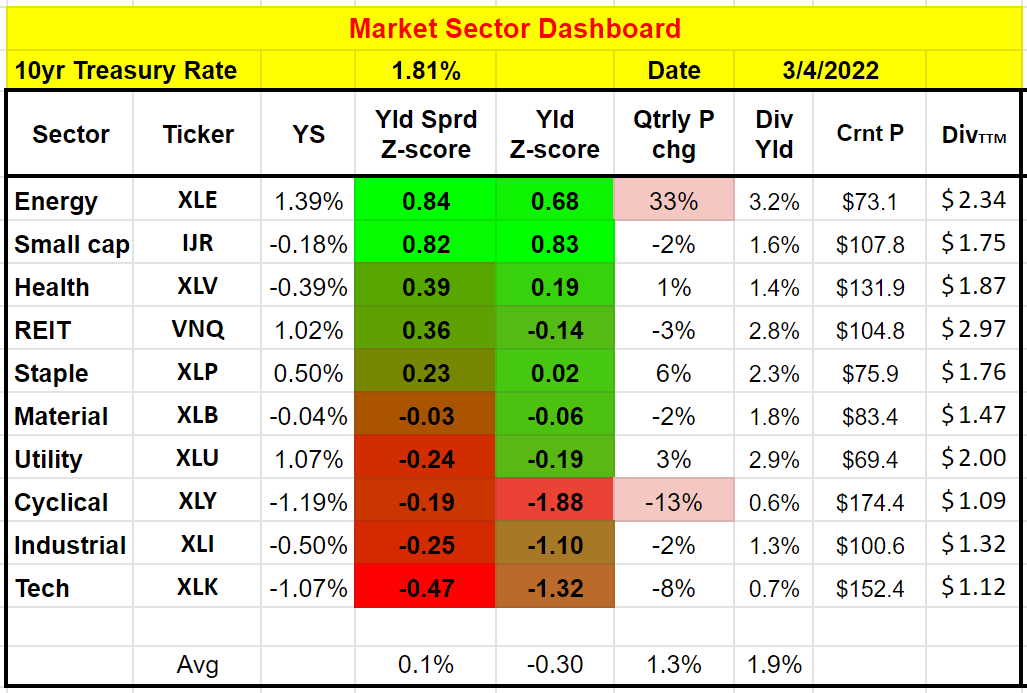

We use the following market sector dashboard to put our finger on the pulse of the market and its major sectors. Especially, the simple YS (yield spread, defined as the TTM dividend yield minus the 10-year Treasury rates) is the first thing we look at. They give us a 30,000 feet view of where to look further – which sector, growth stocks, value stocks, bonds, or precious metals, et al. We will detail the meaning of each entry in the next section, and we update the dashboard monthly. Feel free to download or export the Google-sheet via the following link too: Market Sector Dashboard.

A few overall impressions on the market and the iShares Core S&P Small-Cap ETF (IJR) this month:

- The yield spread between IJR and risk-free rates is at a very attractive level currently. With a YS Z-score near 0.82, IJR (and the small-cap sector) is at a very attractive valuation in a decade – actually, only next to the 2020 COVID panic sale.

- The dashboard also shows that IJR is also attractively valued compared with other sectors. And besides the small-cap sector, the energy sector is equally undervalued, then followed by the health sector.

- Surprisingly, the overall market (represented by a simple average of the sectors in the dashboard) features a slightly positive yield spread relative to the treasury risk (Z-score about 0.1%). For us, this signals that equity, especially high-quality stocks with a reasonable valuation, are more favorable than bonds.

- Lastly, the results and dashboard apply to other similar funds too, such as the Vanguard Small-Cap Index Fund ETF Shares (VB) and the iShares Trust – iShares Russell 2000 ETF (IWM), because these funds are quite similar and their valuation closely correlated.

With the above overall discussion, we now move on to the specifics of the dashboard and IJR.

Source: author Source: Portfoliovisualizer.com

The dashboard explained

Note: if you are familiar with our Market Sector Dashboard already, you can skip this section. It describes the mechanics of the dashboard.

- The yield spread Z-score. It gauges the dividend yield of a given sector relative to the 10-year treasury rates. How the yield spread is calculated will be detailed in the next section. A larger Z-score suggests larger undervaluation compared to the historical record and treasury rates. And vice versa.

- A Z-score that is closer to 1 means the yield spread is near the thickest level of the historical spectrum and is color-coded by bright green. And vice versa.

- The yield spread Z-score. Similar to the yield spread Z-score, it gauges the dividend yield of a given sector relative to its own historical record. A larger Z-score (greener) suggests a larger undervaluation compared to its own historical record. And vice versa.

Yield spread and yield spread Z-score

For bond-like equities fund IJR, an effective way to evaluate their valuation with interest rates adjusted is to calculate the yield spread. Details of the calculation and application of the yield spread have been provided in our earlier article. The yield spread is an indicator we first check before we make investment decisions. We’ve fortunately had very good success with this indicator because of:

- Its simplicity – it only relies on the most simple and reliable data points (treasury rates and dividends). In investing, we always prefer a simpler method that relies on fewer and unambiguous data points rather than a more complicated method that depends on more ambiguous data points.

- Its timeless intuition – no matter how times change, the risk-free rate serves as the gravity on all asset valuations and consequently, the spread ALWAYS provides a measurement of the risk premium investors are paying relative to risk-free rates. A large spread provides a higher margin of safety and vice versa.

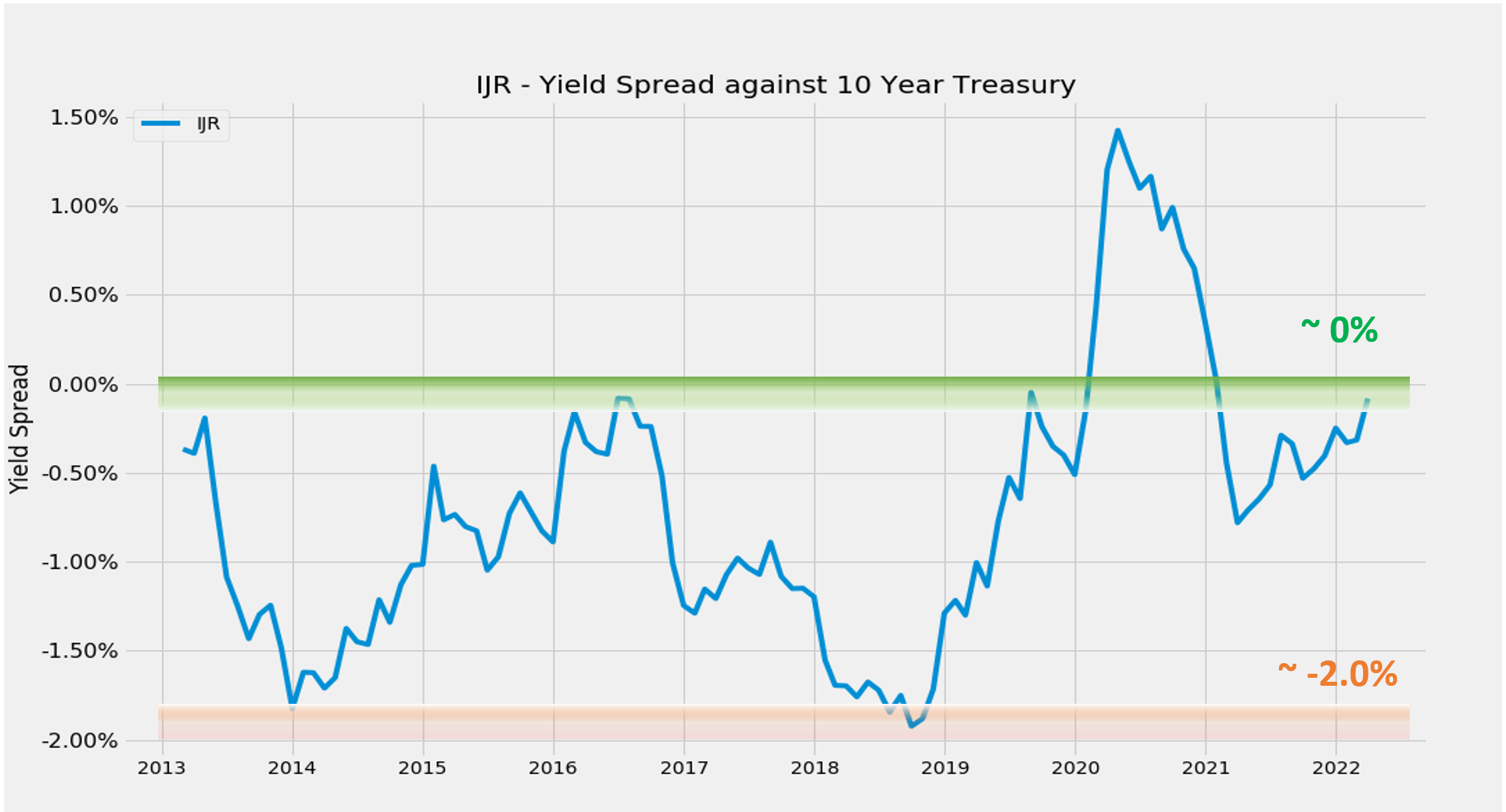

With this background, you will see below that when adjusted for interest rates, IJR’s current valuation is at an attractive level.

The following chart shows the yield spread between IJR and the 10-year treasury. The dividend yield is calculated based on the TTM dividends. As can be seen, the spread is bounded and tractable most of the time. The spread has been in the range between about -2.0% and 0% the majority of the time during the past decade. Such a tractable YS suggests that when the spread is near or above 0%, IJR is significantly undervalued relative to the 10-year Treasury bond (i.e., I would sell treasury bond and buy IJR). In another word, sellers of IJR are willing to sell it (essentially an equity bond with growth built-in) to me at a yield on par with the risk-free yield. So it is a good bargain for me. And vice versa.

You can see the screaming signal in 2020 when the yield spread surged to the 1.5% level – and this is why this dashboard is the first thing we look at when we make our investment decisions.

As of this writing, the spread is about -0.18% as you can see. It is a level that is close to the widest end of the historical spectrum and is above the historical average by a wide margin. Such a wide yield spread provides a healthy cushion for investors in the near future.

Author based on Seeking Alpha data

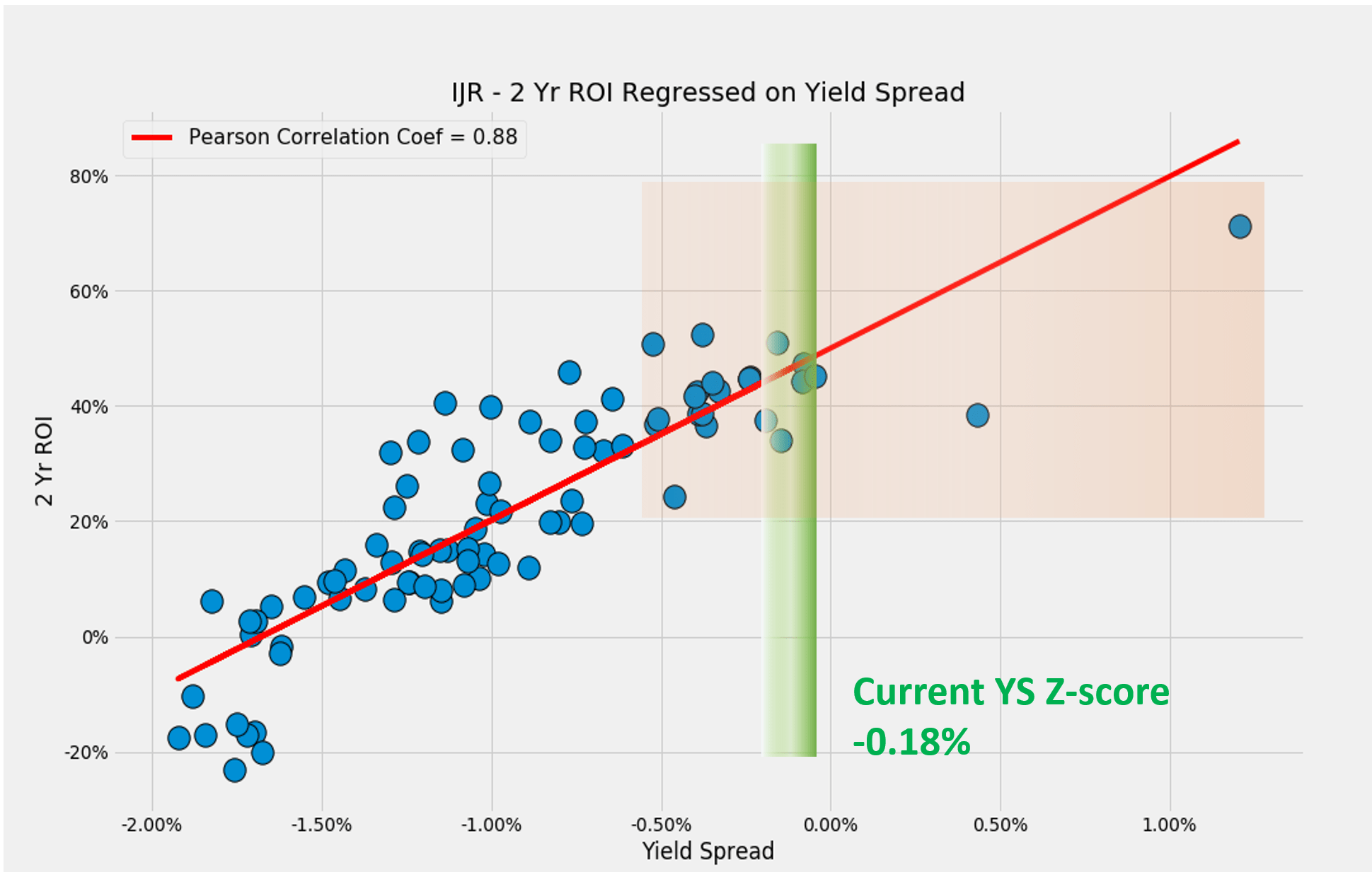

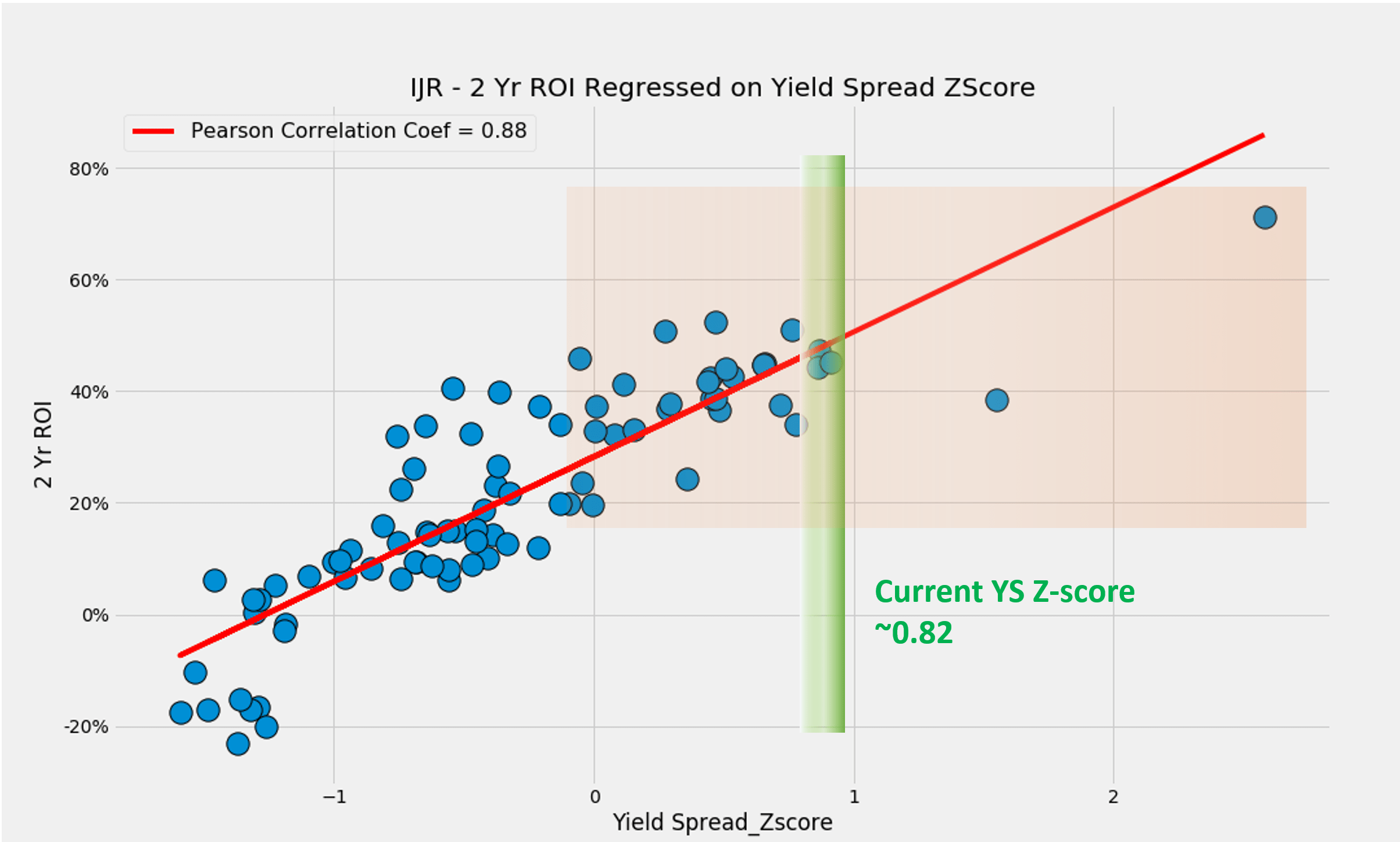

For readers familiar with our analyses, you know that the short-term returns are closely correlated with the yield spread for many of the funds and stocks. And as you can see from the chart below, it is especially so for IJR. This chart shows the two-year total return on IJR (including price appreciation and dividend) when the purchase was made under different yield spread. There is a positive trend and a quite strong one, with a Pearson correlation coefficient of 0.88.

Again, the screaming buying opportunities in 2020 are shown by the two data points on the far-right side of the charts. And you see the outsized return in the next 2 years.

In general, also shown in the orange box, when the spread is about -0.5% or when the YS Z-score is positive, the total returns in the next two years have been all positive and quite large (all above ~20% in all cases).

As of this writing, the yield spread is -0.18 and the YS Z-score is 0.82, close to the widest end of the historical spectrum, actually only next to the extreme conditions that occurred during the 2020 COVID crash. Such wide YS and large Z-score suggest very manageable valuation risks in the near future and very favorable odds for sizable returns.

Author based on Seeking Alpha data Author based on Seeking Alpha data

Conclusions and final thoughts

We use a Market Sector Dashboard to put a finger on the pulse of the market and its major sectors. For this month, our key observations are:

- IJR (and the small-cap sector) now features a very attractive valuation in terms of the YS relative to risk-free treasury rates. Its yield spread is -0.18 and the YS Z-score is 0.82, close to the widest end of the historical spectrum, actually only next to the extreme conditions that occurred during the 2020 COVID crash. Such wide YS and large Z-score suggest very manageable valuation risks in the near future and very favorable odds for sizable returns.

- The above dashboard and conclusions apply to other small-cap funds too, such as VB and IWM because of their similar indexing.

- Other than the small-caps, the energy sector is equally attractively valued too, followed by the health sector.

Thanks for reading and look forward to your comments!

Be the first to comment