asiandelight/iStock via Getty Images

A Quick Take On Clear Secure

Clear Secure (NYSE:YOU) reported its Q3 2022 financial results on November 14, 2022, beating revenue and EPS estimates.

The firm provides identity management security technologies to organizations responsible for venues located in North America and other regions.

Given a slowing macroeconomic picture and my cautious attitude about its ability to sustain positive operating income, I’m on Hold for YOU in the near term.

Clear Secure Overview

New York-based Clear Secure was founded to create a security platform enabling subscribers to demonstrate their identity and receive faster or more convenient access to venues and transportation systems in the U.S. and the broader Americas region.

Management is headed by Chair and CEO Caryn Seidman-Becker, who has been with the firm since 2010 and was previously founder of Arience Capital and managing director at Iridian Asset Management.

The company’s primary offerings include:

-

CLEAR – venue access subscription service

-

CLEAR Plus – CLEAR plus aviation system access subscription service

-

Health Pass – health identity connected to digital health credential

-

Atlas Certified – professional license verification

The firm has focused its direct sales & marketing efforts on U.S. airports, stadiums, major venues and enterprises.

Clear Secure’s Market & Competition

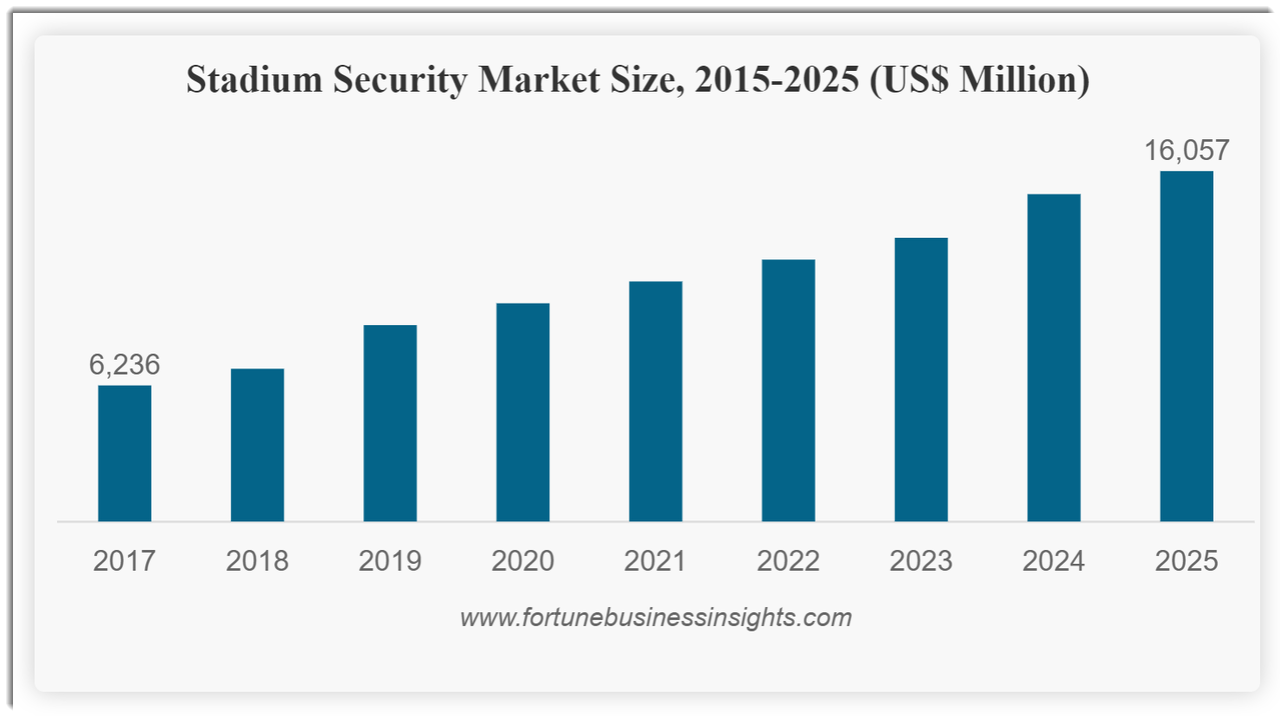

According to a 2018 market research report by Fortune Business Insights, the global stadium security market was an estimated $6.2 billion in 2017 and is forecast to reach $16 billion by 2025.

This represents a forecast CAGR of 12.8% from 2018 to 2025.

The main drivers for this expected growth are a rise in terrorist threat scenarios as well as a need to handle large crowds in a safe manner.

Also, stadium and venue owners are seeking advanced security measures as more options become available.

Below is a chart showing the stadium security market’s historical and forecast growth trajectory:

Stadium Security Market (Fortune Business Insights)

Notably, the software & services segment was expected to grow at the fastest rate through 2025.

Major competitive or other industry participants include:

-

Telos Identity

-

Idemia Identity & Security

-

Avigilon

-

AxxonSoft

-

BOSCH Security Systems

-

Honeywell International

The company operates in other markets, including professional license and certification verification and airport security.

Clear Secure’s Recent Financial Performance

-

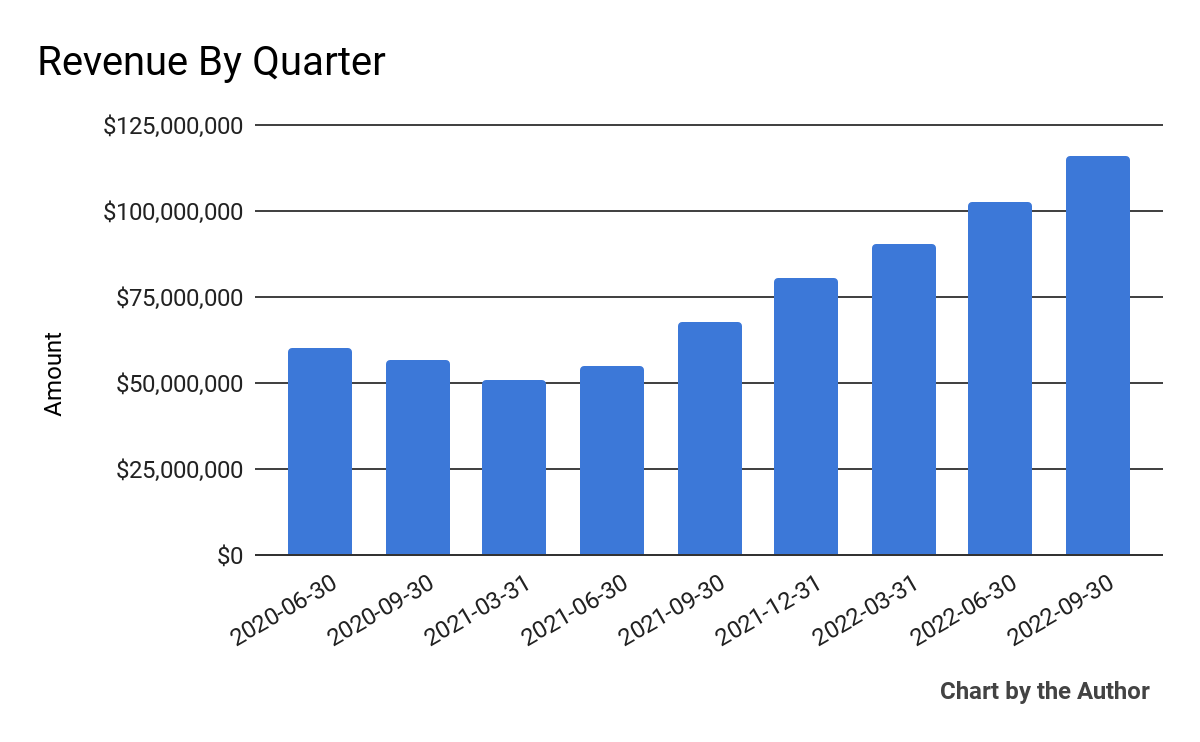

Total revenue by quarter has risen sharply in recent quarters:

9 Quarter Total Revenue (Financial Modeling Prep)

-

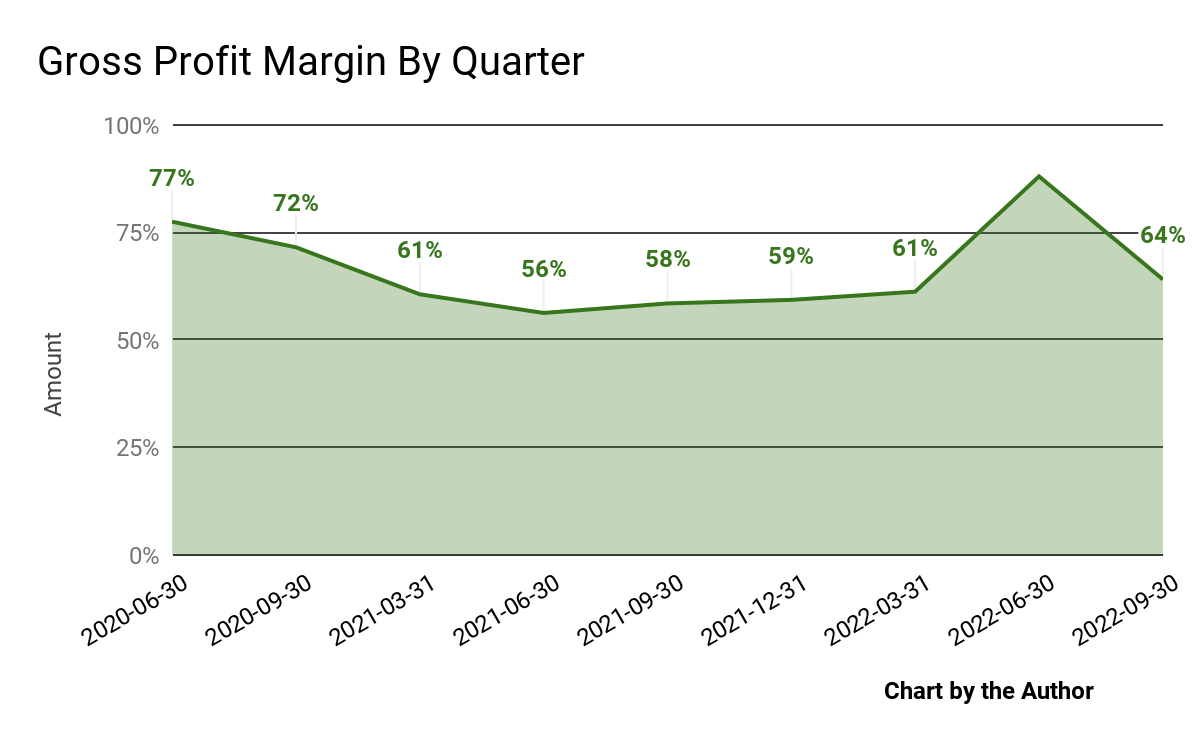

Gross profit margin by quarter has trended higher recently:

9 Quarter Gross Profit Margin (Financial Modeling Prep)

-

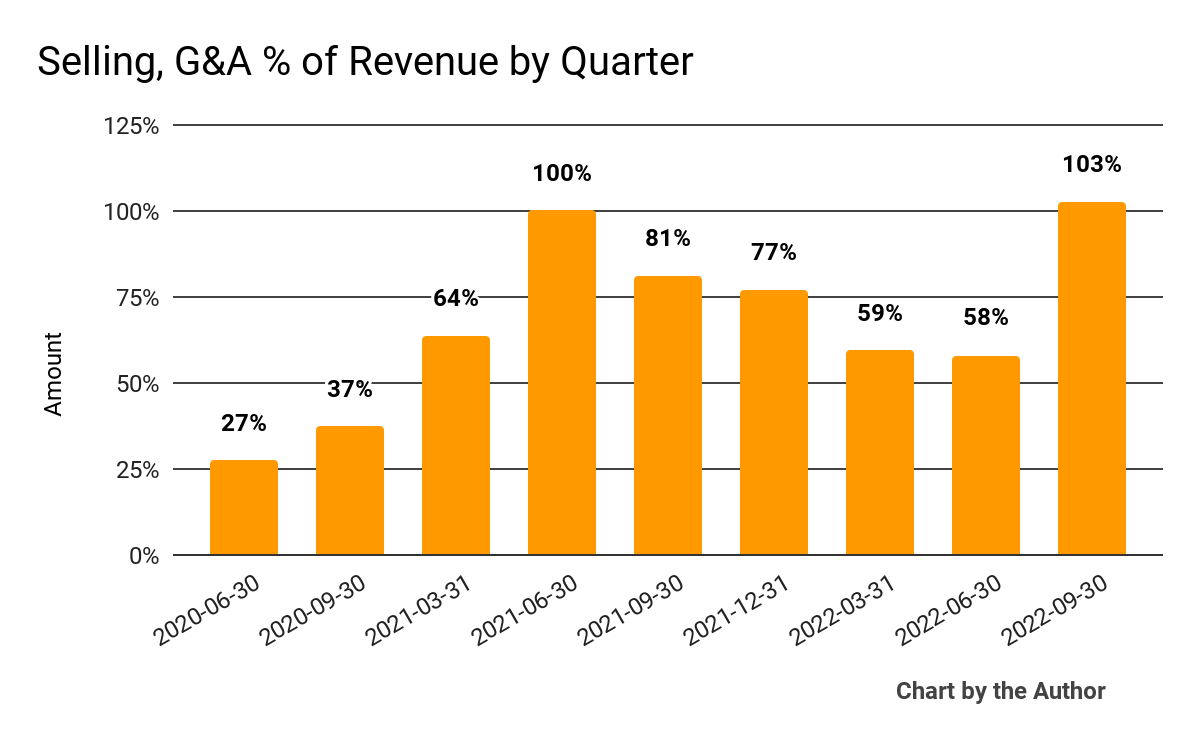

Selling, G&A expenses as a percentage of total revenue by quarter have fluctuated materially in recent reporting periods:

9 Quarter Selling, G&A % Of Revenue (Financial Modeling Prep)

-

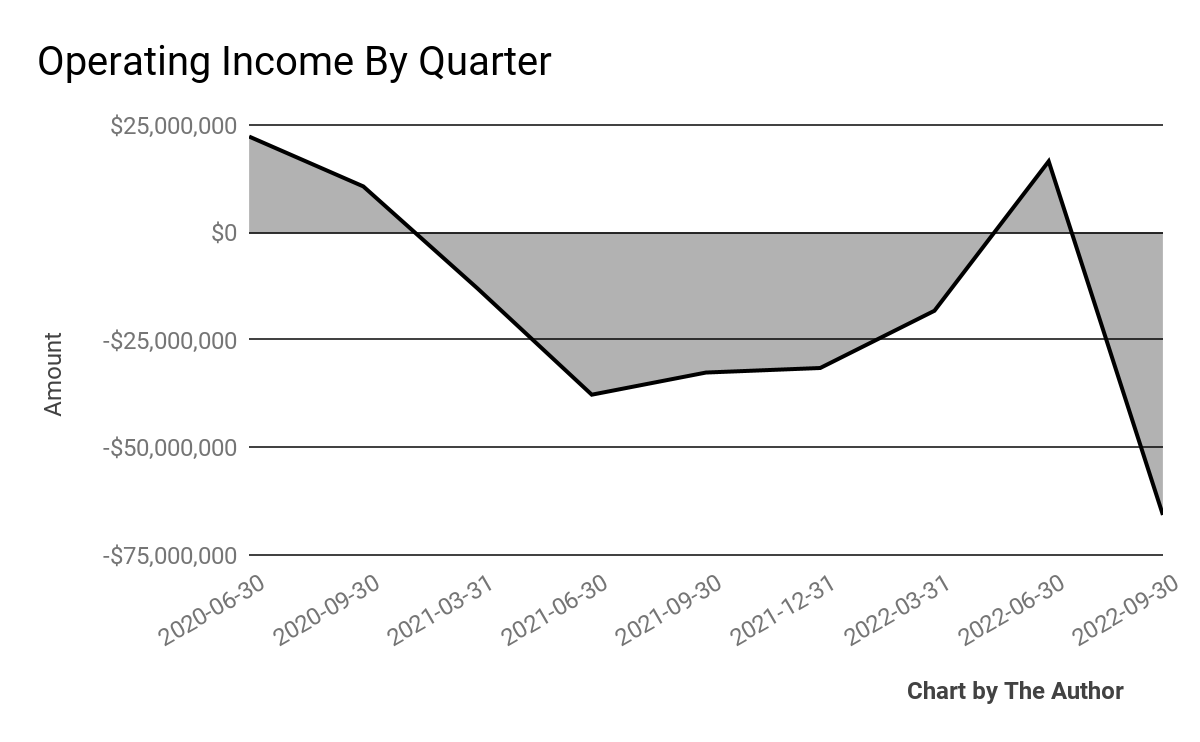

Operating income by quarter has been predominantly negative, dropping sharply in the most recent quarter:

9 Quarter Operating Income (Financial Modeling Prep)

-

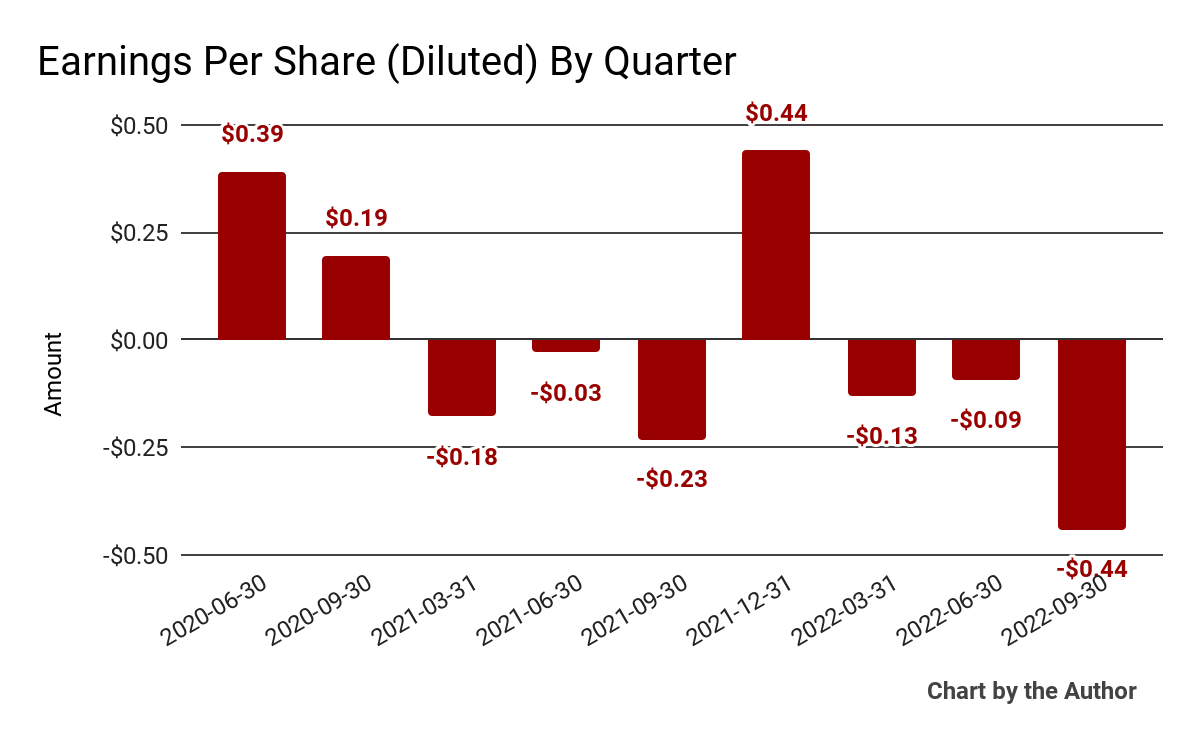

Earnings per share (Diluted) have also varied substantially, dropping to a nine-quarter low in Q3 2022:

9 Quarter Earnings Per Share (Financial Modeling Prep)

(All data in the above charts is GAAP)

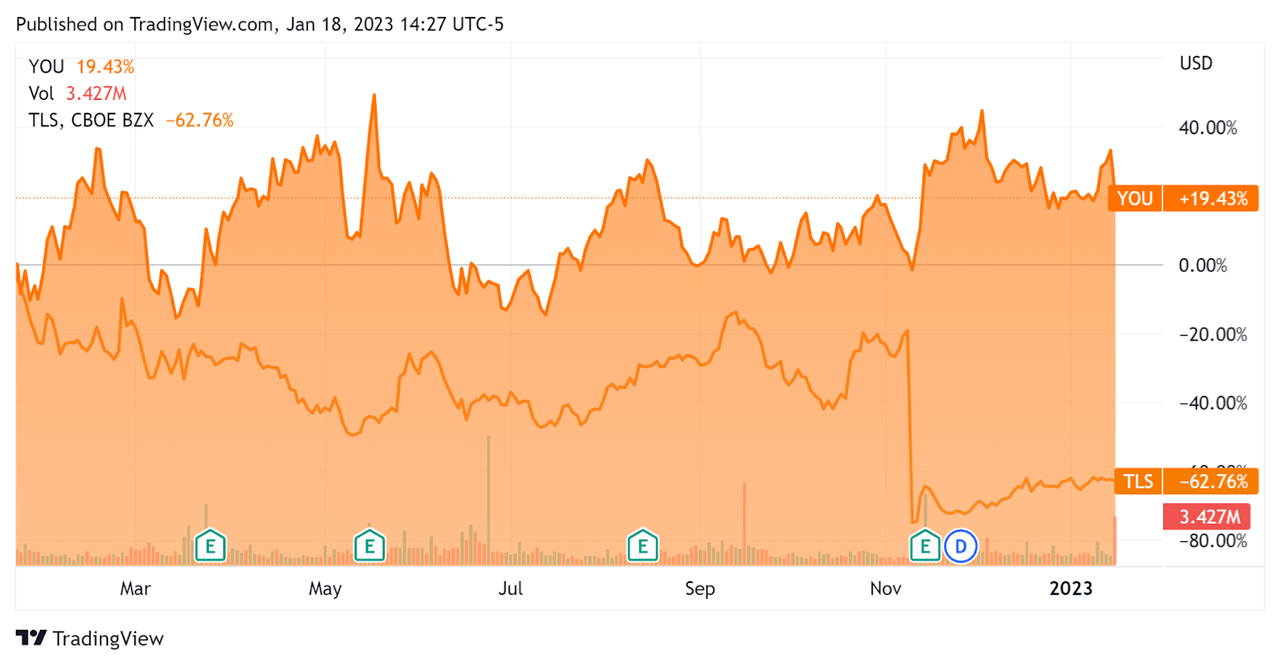

In the past 12 months, YOU’s stock price has risen 19.4% vs. that of partial competitor Telos Corporation’s (TLS) drop of around 62.8%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Clear Secure

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

5.6 |

|

Enterprise Value / EBITDA |

-40.9 |

|

Revenue Growth Rate |

69.7% |

|

Net Income Margin |

-18.3% |

|

GAAP EBITDA % |

-13.7% |

|

Market Capitalization |

$4,545,432,576 |

|

Enterprise Value |

$2,180,561,802 |

|

Operating Cash Flow |

$120,760,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.22 |

(Source – Financial Modeling Prep)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

YOU’s most recent GAAP Rule of 40 calculation was 56.1% as of Q3 2022, so the firm has performed well in this regard, per the table below:

|

Rule of 40 – GAAP [TTM] |

Calculation |

|

Recent Rev. Growth % |

69.7% |

|

GAAP EBITDA % |

-13.7% |

|

Total |

56.1% |

(Source – Financial Modeling Prep)

Commentary On Clear Secure

In its last earnings call (Source – Seeking Alpha), covering Q3 2022’s results, management highlighted its strong revenue growth due in part to platform expansion to enterprise partners.

Leadership believes that despite a slowing macroeconomic environment, ‘the demand for experiences, including travel, will sustain.’

Notably, the company is sensing a blurring of the lines between leisure and business travel since the waning of the pandemic, as hybrid work patterns increase in use.

As to its financial results, total revenue rose 71.4% year-over-year, while gross profit margin increased by 6 percentage points.

The company’s net member retention rate was 92.2%, above ‘long-term expectations of the upper 80s.’

The firm’s Rule of 40 results were impressive, with a strong revenue growth result offset only slightly by a negative operating result contributing to a high figure for this metric.

However, operating losses were substantial due to high stock-based compensation.

For the balance sheet, the company ended the quarter with $671.4 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash flow was $91.6 million, of which capital expenditures accounted for $29.2 million. The company paid a hefty $114.4 million in stock-based compensation.

Looking ahead, management believes that its growing bundle of services for travelers can operate as a virtuous cycle, a ‘flywheel effect’ of one service enhancing the value of others.

The company expects to be operational in 50 airports soon and ultimately to be in ‘60 to 75 airports in the U.S.’

Regarding valuation, the market is valuing YOU at an EV/Revenue multiple of 5.6x for a company that is growing revenue rapidly.

However, the primary risk to the company’s outlook is a slowing macroeconomic outlook which may reduce discretionary travel and related spending, dampening revenue growth in 2023.

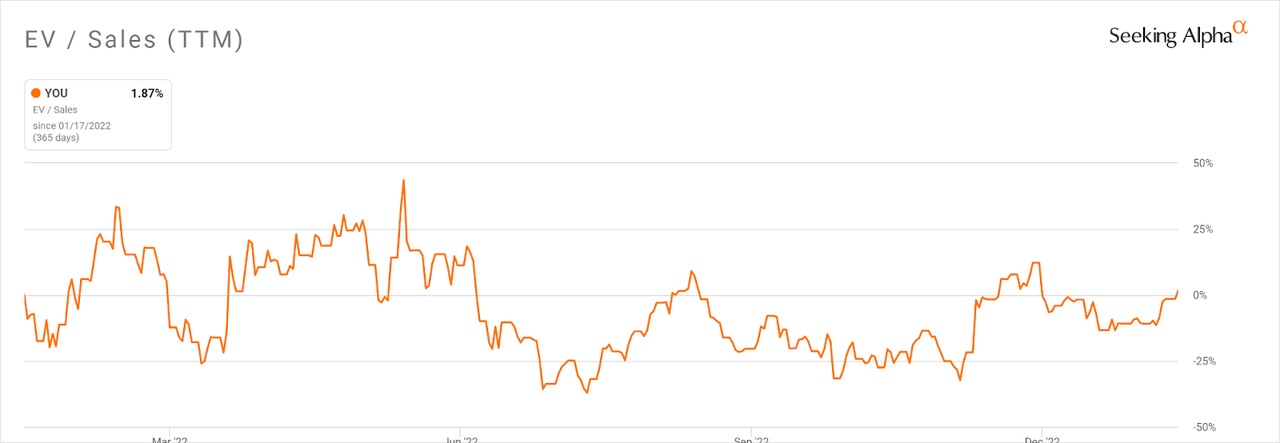

YOU’s EV/Sales multiple [TTM] has risen slightly, by 1.87% in the past twelve months, as the Seeking Alpha chart shows here:

Enterprise Value / Sales Multiple (Seeking Alpha)

A potential upside catalyst to the stock could include a particularly strong launch of its PreCheck service in the future.

While Clear Secure has an interesting story to tell and revenue is certainly growing impressively, the firm largely has a history of operating losses and negative earnings.

Management needs to prove it can beat operating breakeven for the stock to exit the typical beaten-down tech category and move up.

Given a slowing macroeconomic picture and my cautious attitude about its ability to sustain positive operating income, I’m on Hold for YOU in the near term.

Be the first to comment