Leestat

The means of defense against foreign danger, have been always the instruments of tyranny at home.”― James Madison.

One of the themes of the past half decade is how many and how quickly myriad “false narratives” have imploded in this country. I could easily list a dozen of these events, but I will not do so as I want to avoid making this any sort of a politically focused article. However, I do want to broach one topic that I believe the current “consensus” is potentially wrong about and that could have significant political, market and economic impacts if things go south.

That is this narrative that Ukraine is “winning” the war with Russia will be busted by the end of this spring. If this turns out to be the case, this reversal will obviously have significant impacts on energy, the markets, numerous commodities, as well as potentially huge domestic political and geopolitical ramifications. Here are a few reasons I think this is at least a potential possibility.

NY Times

Ukraine’s army has to be exhausted by now. They have been largely on the offensive for months and have managed to claw back an impressive amount of lost Ukrainian territory. That said, from a historical perspective, when two sides are roughly equally matched, the attacker usually takes two to three times more casualties than the entrenched defender. So if Russia’s casualties are said to be over 100,000 men and 3,000 tanks now, I hesitate to estimate what kind of losses Ukrainian forces are taking, especially given the massive Russian artillery batteries facing them. No one in the western media appears willing to post even a guess or ask this obvious question. A major Russian offensive, especially when the ground is frozen hard could puncture Ukrainian forces quickly, if done right. This is a big “if” given the Russian military’s lack of coordination and communications between air, ground and artillery forces to this point in the conflict.

NY Post Article – 01/17/2023

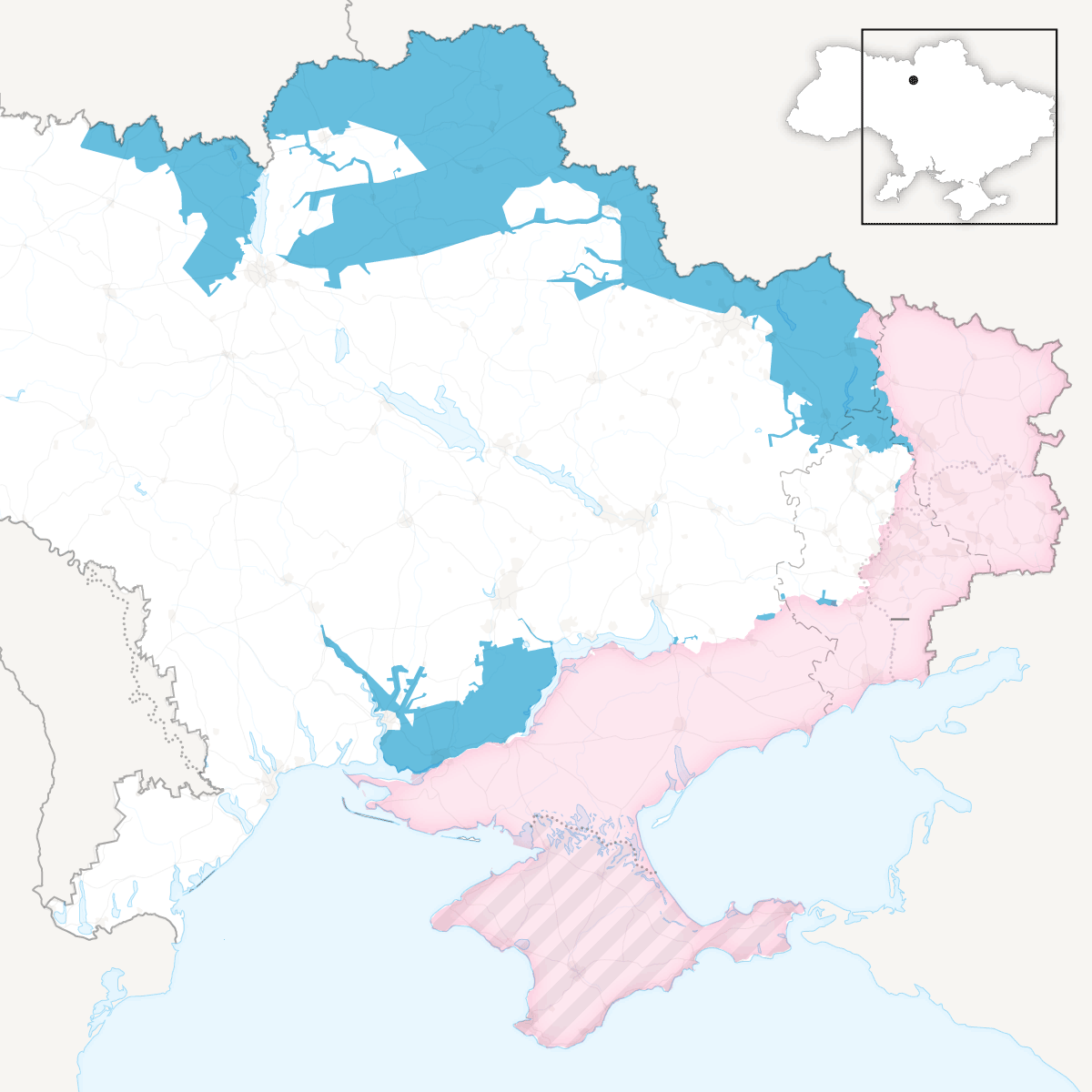

Russian invaded Ukraine with a force of approximately 190,000 defense personnel, just over 150,000 frontline troops. This was never enough to take over Ukraine, whose population was just over 40 million people before the war, let alone hold this territory or threaten other countries as some government and military pundits projected.

In retrospect, the goals of this invasion seem to have been to decapitate the country’s political leadership in Kyiv quickly, establish a pro-Russian puppet government, fully conquer the largely Russian speaking and mineral/energy rich eastern provinces, as well as establish a land bridge to Crimea. Short-term goals might have also included taking the city of Odessa if all went well. This would cede control of most of the access to the Black Sea to Russia, which is important given the Russian navy has so few warm water ports to operate out of currently. This strategy didn’t bear fruition for the most part thanks to the bravery and resilience of the Ukrainian forces and people. Not to mention the large stores of weapons and ammunition sent by the West soon after the conflict began or the poor performance of the Russian armed forces to this point.

However, it seems Russia is on the possible verge of committing significantly more troops to the battle, as Russia now plans to enlarge their armed forces by some 350,000 and new conscriptions have already started. This event should it occur could very well be a game changer, even if the additional forces are poorly trained. If Putin launches a large offensive this winter/spring, the Russian forces are likely going to take huge casualties (never a show stopper for this country historically) but they could gain considerable territory and substantial leverage for negotiations with Ukraine, if nothing else.

This is especially possible given how drained weapon stockpiles have become both here and in Europe. It will take years to replace what the United States has already given Ukraine, let alone provide more ammunition and arms. The NY Times just reported the U.S is now tapping into its arsenal in Israel to supply artillery shells to Ukraine. Raytheon Technologies Corporation (RTX) stopped producing shoulder-fired Stingers for years, but now has been asked by the Pentagon to ramp up production as thousands have been shipped to Ukraine. Europe seems in a worse position on that front. How long the current pace of arms and ammo shipments to Ukraine can continue is in question at this point.

Obviously I am spit-balling a bit here, but what are the ramifications if this occurs? On energy supplies? The prospects for peace negotiations when the narrative Ukraine can win this conflict implodes? Doe this failure embolden China to invade Taiwan, especially since a good portion of the $19 billion in arms we have promised the island nation to date have been diverted “temporarily” to Ukraine? How big a blow does the economy and the markets suffer if that scenario occurs?

Hopefully, this remains a black swan event that never happens, but one that should be at least contemplated in my opinion. My initial thoughts are this would be good for domestic energy stocks like HighPeak Energy (HPK), which I recently profiled. Escalation of the war in Ukraine in this way would likely bring a call for total sanctions on all Russian energy supplies. This, in turn, would push up the prices for oil and natural gas globally.

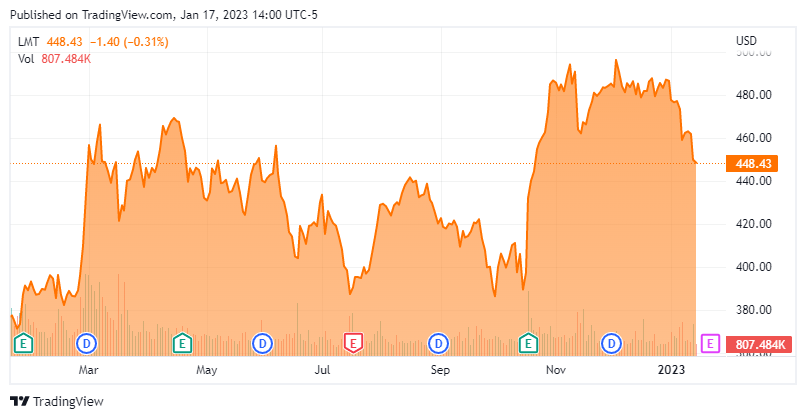

I also believe it would be neutral for defense stocks, as if Russia managed to use gains to leverage a peace settlement, that would negate a large source of demand for American-made weapon systems and ammunition from the Ukraine front. However, contractors like Lockheed Martin (LMT) would be kept quite busy replacing arms and ammunition stores we have already sent Ukraine at an accelerated pace, not to mention the needs for Taiwan. The defense sector was one of the few parts of the market to post gains in 2022.

Seeking Alpha

Finally, a surge in energy prices and this conflict escalating on the borders of Europe would hardly be good for the global economic outlook. Recession at some point in 2023 already seems a good possibility, a reversal of the Ukrainian narrative would make that scenario almost a slam dunk.

This is one of many reasons I remain wary on the overall market and have a much higher allocation to cash than I normally do within my own portfolio. Something that is likely to remain the case until we see more certainty on both the economic and geopolitical fronts.

Note: This article in no way, shape or form excuses any of Putin’s barbarity in Ukraine. It is meant only as a thought provoking piece for investors. Given that, please feel free to comment on how likely you believe the scenario painted above could actually play out, and what ramifications to the market and economy you envision should that occur.

There is nothing that war has ever achieved that we could not better achieve without it.”― Havelock Ellis.

Be the first to comment