Funtap

Introduction to IBHD

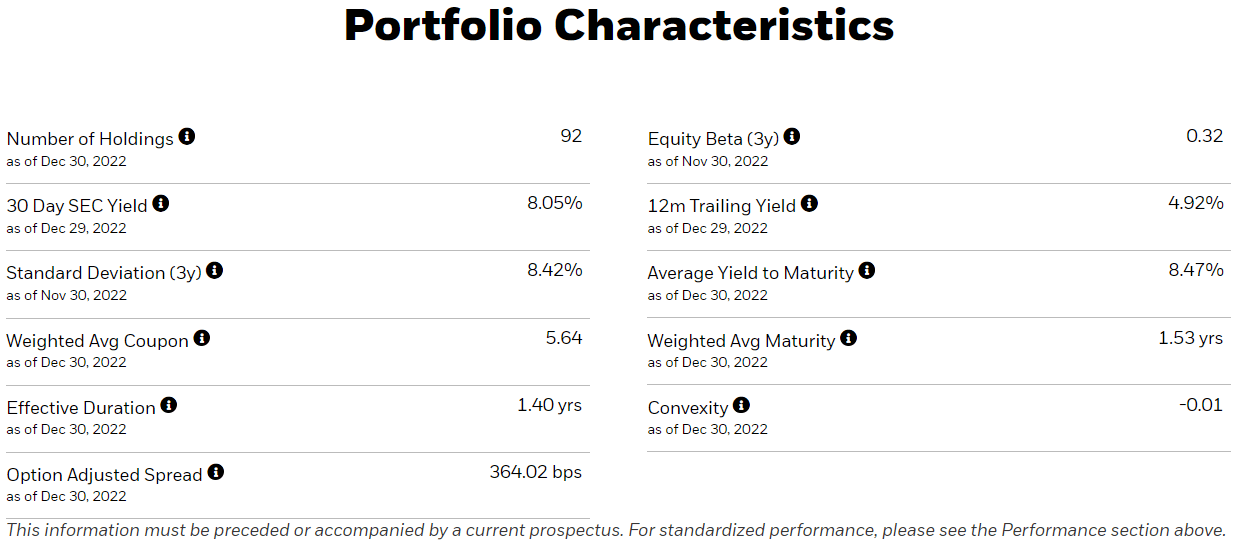

(BATS:IBHD) is iShares iBonds 2024 Term High Yield and Income ETF. IBHD holds a portfolio of high-yield bonds maturing between January 1, 2024 and December 15, 2024. By December 15, 2024, the net assets will be almost entirely in cash and will be returned to shareholders. The average yield to maturity of IBHD is ~8.5% with a weighted average maturity of ~1.5 years.

Put simply, this ETF looks at every North American high-yield bond that matures sometime in 2024, applies some exclusion rule, and holds them passively subject to some weight limits and monthly rebalancing.

iShares

Merits

Given the inverted yield curve, I was looking for front-end bonds with embedded capital gains. The issue with other front-end focused ETFs (like SHYG and IGSB) is that they roll forward perpetually, so you are always subject to the front-end/belly of the yield curve movements (i.e., repricing risk). I like IBHD’s self-liquidating feature so that the shareholders can “lock up” the return, subject to credit loss.

The other feature that I find interesting is that over time, this ETF will upgrade its credit quality naturally. According to the prospectus, in the last 1.5 years but before the last 6 months (i.e., between July 2023 and July 2024), when the underlying high-yield bonds are called, the proceeds will be reinvested into investment grade bonds that mature sometime in 2024. Therefore, the credit quality of this ETF will improve closer to the liquidation date of December 15, 2024. Note that companies generally don’t want to let long-term liabilities go current (i.e., wait until the bond has less than one year to mature) so I expect a large portion of the 2024 maturities will be taken out sometime in 2023, subject to market condition.

Lastly, similar to other ETFs, IBHD gives you a diversified basket of bonds that’s impossible for retail investors to replicate.

Risks

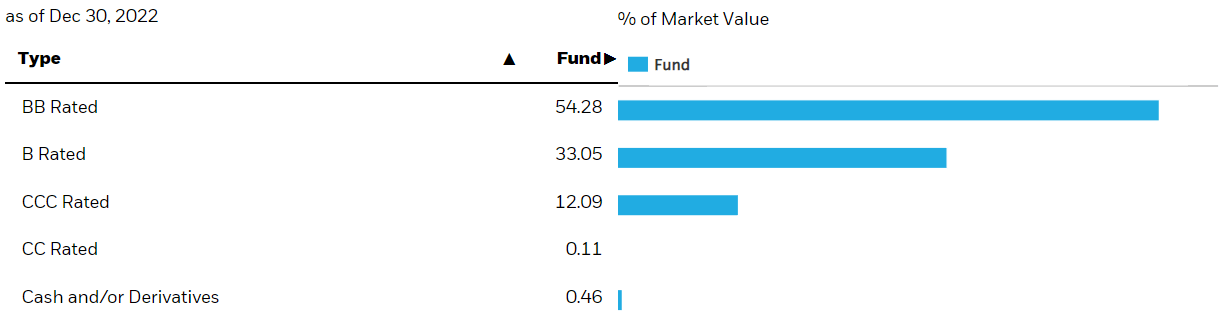

With the upside well-defined, the main risk is credit loss (or in anticipation of the credit loss, the bond trading substantially below par). At first glance, this is a double-B heavy portfolio (~55% of the total weight) and CCC takes up 12% of the portfolio, so the credit quality is on the higher end of the spectrum.

Rating Buckets (iShares)

There are also a few ways that the portfolio tries to mitigate the impact of credit events such as issuer concentration (3% max) and minimum issuance size ($250 million outstanding at the time of purchase). Furthermore, bonds trading below $60 are excluded and subject to a 3-month lock-out period before they are eligible for inclusion again at rebalance.

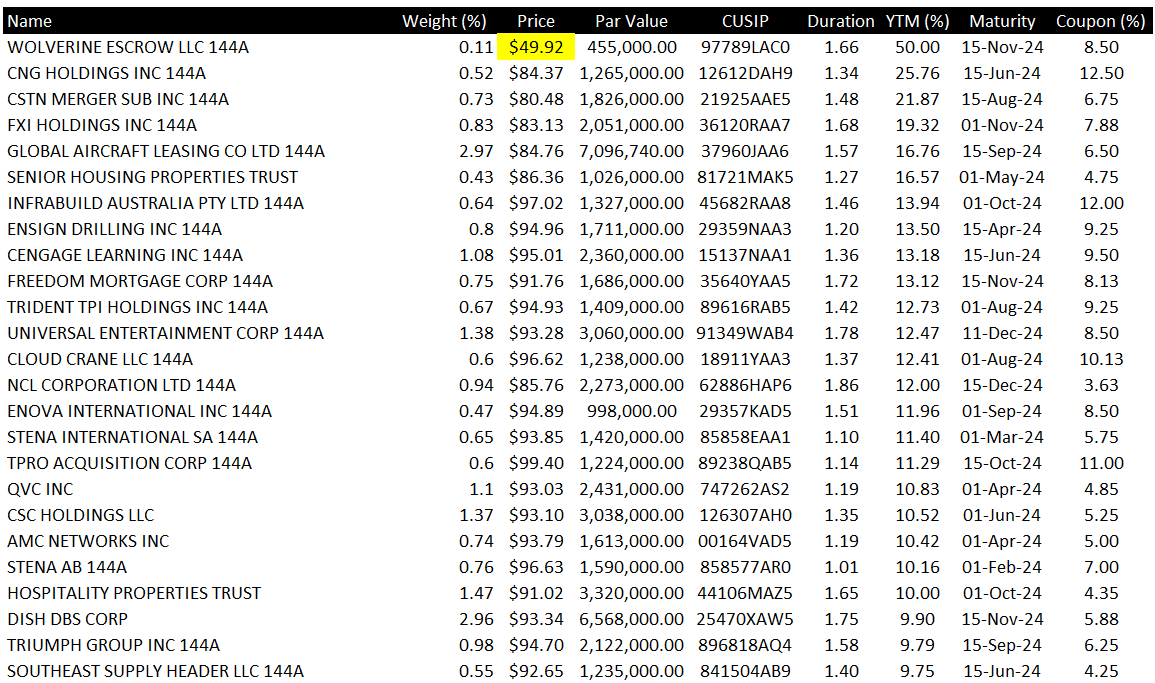

Below is a sample of the holding ranked by highest YTM. Wolverine Escrow 8.5% should be kicked out of the portfolio soon as the bond is trading below $60. While I don’t know every one of the ~90 holdings, I’m reasonably comfortable with even some of the higher-yielding names such as Ensign Drilling, Cengage, and Senior Housing Property Trust.

Holdings (iShares)

Fitch is calling 2023-2024 US high yield default rate to be in the range of 3-4%. Let’s take the default rate up to 5%, which means roughly 5 issuers will default out of the ~90 issuers in the portfolio (90 x 5%). Assume the high YTM reflects a higher probability of default, the top 5 highest yielding names take up ~5.5% of the portfolio weight, which means even if all of these 5 names go to zero (which is a conservative approach as the ETF will have sold these bonds when the prices drop below $60, but above $0), the total return should still be positive given a ~8.5 YTM.

Top 5 Yielding Holdings (iShares)

Another “risk” is that if the credit market condition somehow improves and a lot of the issuers in the portfolio refinance their 2024 bonds early, the subsequent holding period return will be low as the portfolio will likely be investment grade heavy at that time. However, this is actually a shareholder-friendly scenario as the bonds are pulled to par before their stated maturity dates, resulting in a higher IRR and the NAV should reflect this.

Conclusion

In a highly volatile and uncertain environment, return of capital is much more important than return on capital. With IBHD I know what I’m going to get on the upside and I can get reasonably comfortable with the downside scenario (without accounting for a potential rate cut and/or federal government fiscal stimulus), and I can also pretend to ignore the mark-to-market volatility.

Be the first to comment