TSchon/iStock via Getty Images

After two extremely strong days of performance for the major market averages, I would call yesterday’s muted returns a win, especially in light of the deluge of earnings reports that were mixed at best. Some were pretty good, but others were downright awful. The guidance was mixed as well. What surprised me was that the response from stock prices was not worse. That means that investors were expecting numbers and guidance to be even more dismal than reported, or they are looking beyond the first half of this year to better days ahead. Financial markets have a tendency to discount future events, but they have been under the influence of a manipulative monetary policy for so long that most investors have forgotten this. With more than one third of the S&P 500 reporting this week, we will have a much better idea of whether this is a pattern that will hold or not.

Finviz

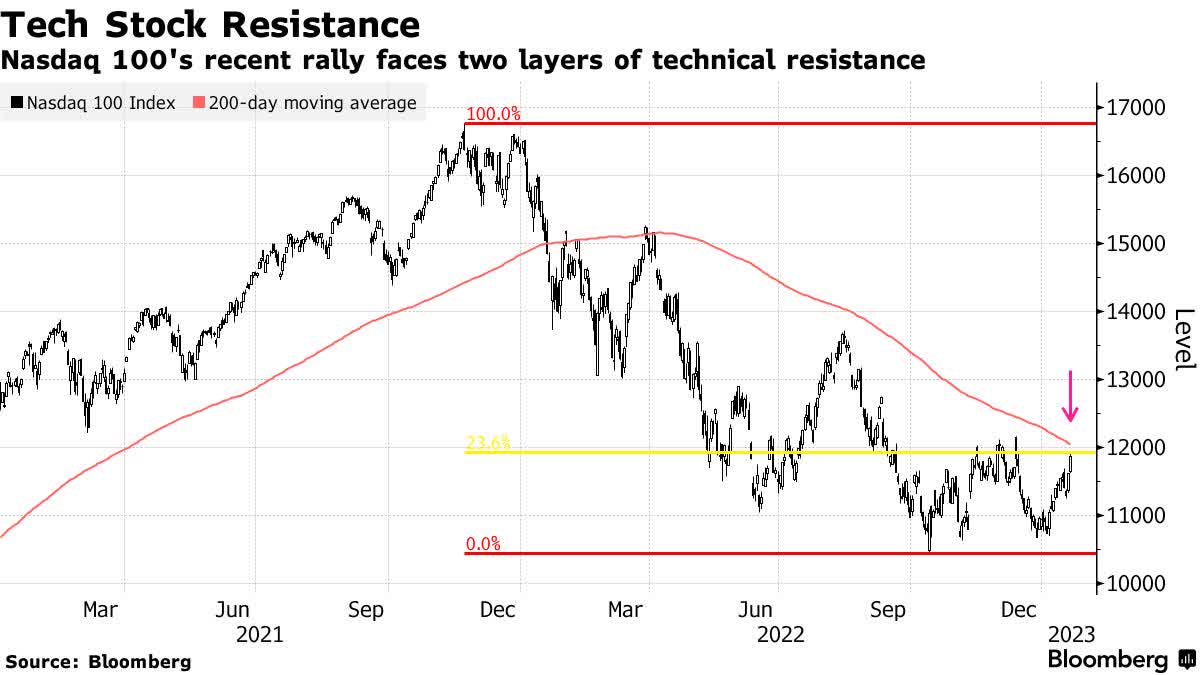

Microsoft’s (MSFT) earnings report is a microcosm of what I am talking about. There was a small beat on the bottom line, but a small miss on the top line. Its cloud and business-related products saw solid growth, yet its consumer-related product sales fell sharply. The stock rose higher after yesterday’s close, but it is lower prior to this morning’s open. Again, a mixed bag. Let us see how it trades today. The Nasdaq Composite has a similar chart and sits at a significant level of overhead resistance just beneath its long-term moving average , which coincides with a statistically significant 23.6% retracement level (Fibonacci) from its 2021 high. This is the weakest of all the indexes, so if it can pierce this level it makes the 2023 outlook appear a whole lot brighter.

Bloomberg

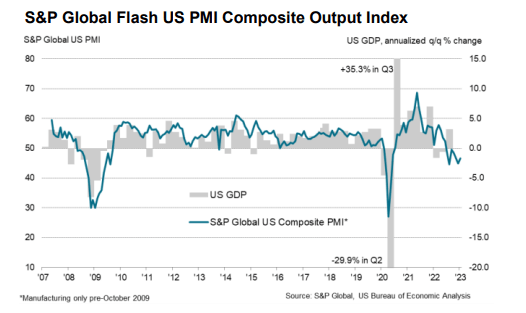

We had another economic report yesterday that was less bad than expected, which is what I want to see. I am operating under the premise that rates of change are more important than absolute numbers. S&P Global’s mid-month read (Flash) of its US Purchasing Managers Composite Index (PMI), which includes services and manufacturing, rose from 45 in December to 46.6 in January. That is not as positive as it appears, because any number below 50 indicates a contraction in activity or output. Yet the contraction is lessening to a level that equates to a three-month high. The current level is consistent with the recessionary periods we saw in 2008 and 2020, but there is one caveat. This index does not include energy companies or government-provided services, which have been the strongest as of late. The Institute for Supply Management’s similar survey includes both, which is why it shows more strength.

S&P Global

Still, a three-month high is modest improvement from the private sector at a time when the consensus is looking for a more significant downturn. Furthermore, business confidence strengthened in January to a level of optimism that was a four-month high, which is another sign of potential positive momentum ahead.

I know the bears are getting restless when the grandfather of them all comes out of hibernation to pound his chest. I am a big fan of famed-investor Jeremy Grantham’s accomplishments, but the billionaire’s dire outlooks for the US stock market since the Great Financial Crisis have led me astray more than once. Therefore, I take his relentlessly bearish outlooks with a grain of salt. The market’s resiliency over the past three months has led him to assert that we will see another 20%-plus decline in the S&P 500 this year to a level of 3,000-3,200.

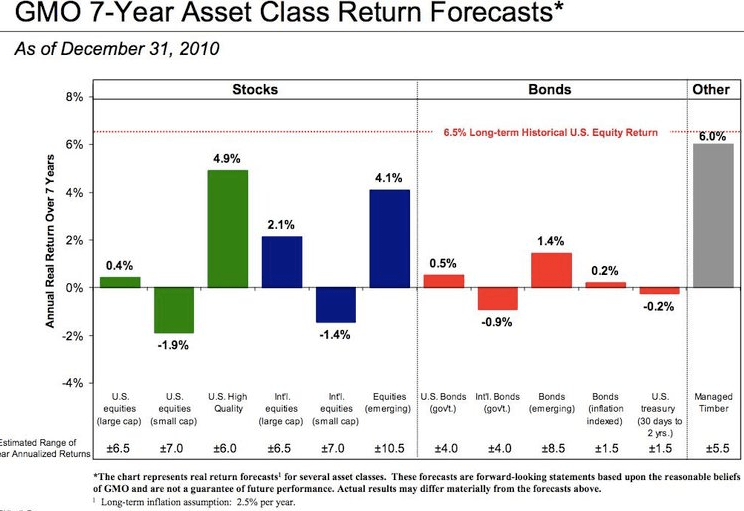

He claims that “the range of problems is greater than it usually is-maybe as great as I’ve ever seen,” in an interview this week. My issue with Mr. Grantham’s outlooks is that they have been more a function of what he thinks should happen rather than what is likely to happen. He also focuses on the very long term, which is problematic for me when he makes short-term calls. Especially since his long-term outlooks have been abysmal in recent years. For example, he has been expecting outperformance from emerging markets for more than a decade in his rolling 7-year asset class return forecasts, largely based on valuations, but to no avail.

AWealthOfCommonSense

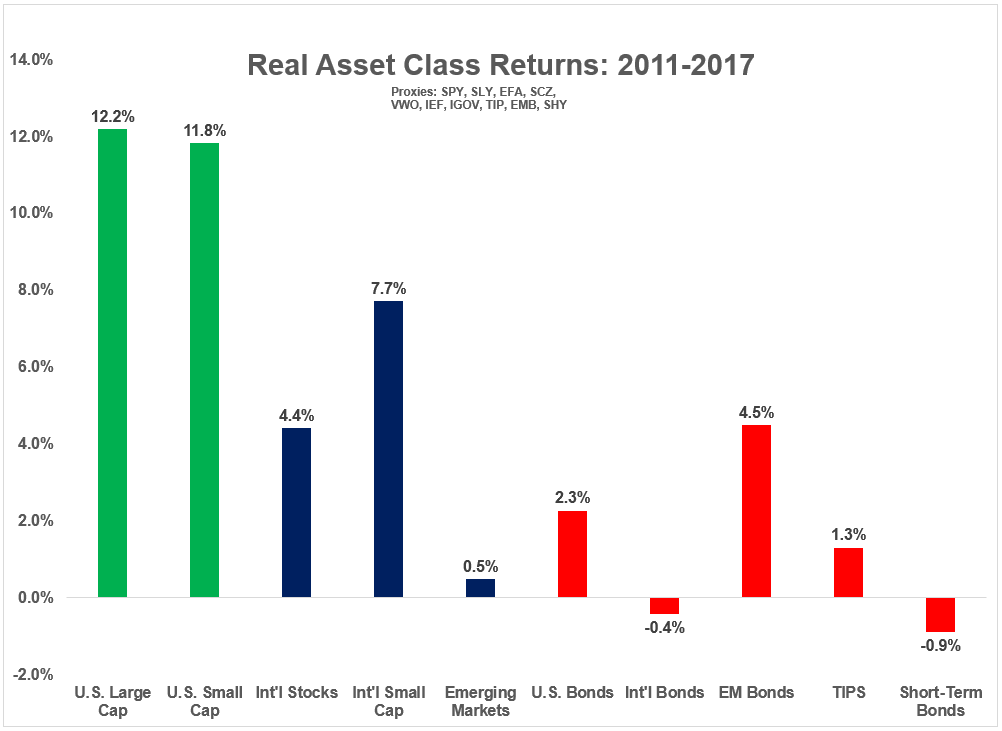

The past decade was not a good one for him, but I think that was largely because he was vehemently opposed to the Federal Reserve’s monetary policy of near-zero interest rates and quantitative easing. He emphasized value as well, which significantly underperformed growth. I am sure he will have his day in the sun at some point, because markets always have bear-market declines, but I think the one he is forecasting happened last year.

AWealthOfCommonSense

Be the first to comment