JuSun

There are plenty of stocks that have fallen by the wayside this year. While that may be a bitter pill to swallow, it also means an opportunity for those with dry powder on hand to capitalize on cheap high yielding stocks. Getting a great starting valuation and yield is one of the key contributors to total returns, and now is not a bad time to start harvesting dividend stocks.

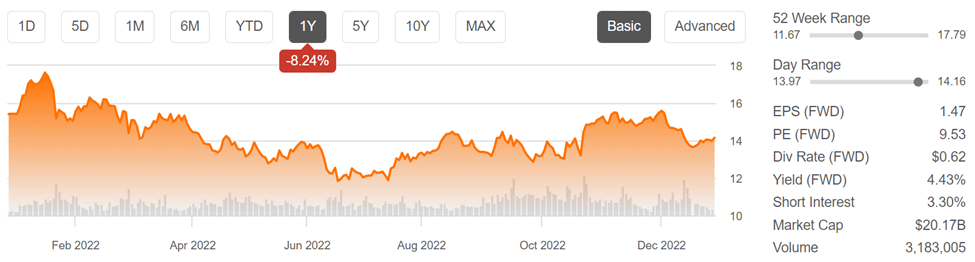

This brings me to Huntington Bancshares (NASDAQ:HBAN), whose stock has struggled for much of the year. As shown below, it sits well below the midpoint of its 52-week range and recently has taken a dip in sympathy with the rest of the market, pushing the dividend to 4.4%. This article highlights why now may be an opportune time to layer into the stock.

HBAN Stock (Seeking Alpha)

Why HBAN?

Huntington Bancshares is a large regional bank and one of the oldest in the U.S., having been founded in 1866. It’s headquartered in Columbus, Ohio, and has a presence in 11 states with over 1,000 branches, and $179 billion in total assets.

HBAN had a rocky time during the great financial crisis of 2008-2009, after it made an untimely acquisition of Sky Financial in 2007, which exposed it to losses associated with subprime mortgages and bad commercial loans. It’s since re-focused itself on middle-market lending and retail clients, greatly improving its balance sheet over the past decade. More recently, HBAN has returned to growth, especially with its 2021 acquisition of TCF Financial, which had operated in some of the same markets as HBAN, enabling cost efficiencies for the combined banks.

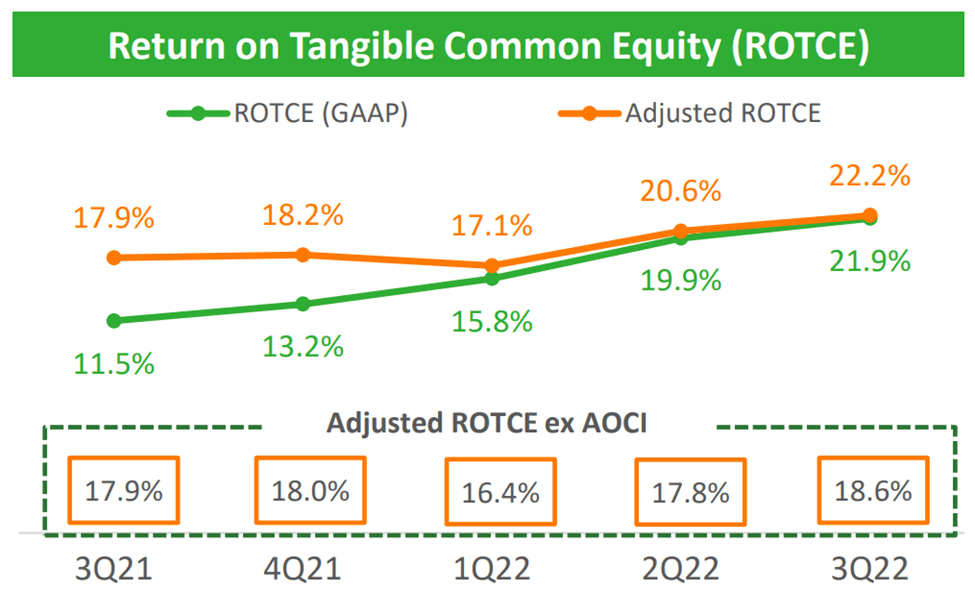

Since the acquisition, HBAN has delivered solid operating results, with adjusted EPS growing by 11% YoY to $0.39 in the third quarter. Moreover, HBAN has seen a meaningful improvement in its return on tangible equity. As shown below, both adjusted ROTCE, with and without AOCI, have demonstrated improvement over the past year. For reference, accumulated other comprehensive income (AOCI) is the bucket that’s designated for unrealized profits or losses.

HBAN ROTCE (Investor Presentation)

HBAN’s increased scale is also driving an efficient platform. This is reflected by HBAN’s efficiency ratio declining by 290 basis points sequentially to 54.4%. Moreover, HBAN is maintaining a conservative financial profile, with ACL (allowance for credit losses) to loans ratio of 1.89%, which is among the highest in its peer group. At the same time, net charge-offs remain low, at a 0.15% rate, which is down five basis points from last year.

Looking forward, HBAN should continue to see growth, as it’s seen total loan balances grow nearly 7% compared to last year to $117 billion, with growth more or less evenly spread between commercial and consumer lines of business. I also see reasons to be optimistic around HBAN’s wealth management expansion, which generally comes with higher returns compared to cost. Management highlighted on this expansion into new markets during the recent conference call:

The launch of Wealth Management in the Twin Cities continues to track better than our initial projections. The team has been fully built out, and we are pleased with the caliber of talent we were able to add in this market. While it’s still early, the team is already contributing to relationship growth.

Building pipelines reflect a significant customer opportunity even against a difficult market backdrop. Based on early successes we are seeing in the Twin Cities, we’ve expanded the wealth management business to Denver with key hires added during the third quarter.

Meanwhile, HBAN maintains a healthy BBB+ rated balance sheet and has a CET1 ratio of 9.3%, sitting within management’s target range of 9% to 10%, and above the 4.5% set by the Federal Reserve for large banks. It also pays an attractive 4.4% dividend yield that’s well protected by a 43% payout ratio.

HBAN has also raised its dividend for 12 consecutive years and has an impressive 5-year dividend CAGR of 12%. While dividend growth has been muted in recent years, I would expect growth to ramp up again after the economic picture brightens, and cost synergies are fully realized.

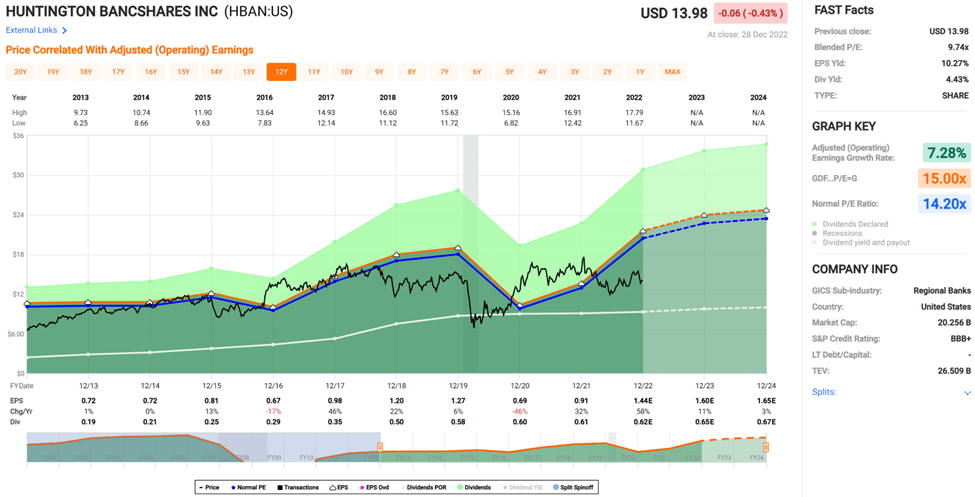

Lastly, I find value in HBAN at the current price of $14.10 with a forward PE of 9.6, sitting well below its normal PE of 14.2 over the past decade. Analysts have an average price target of $16.21, which translates to a potential total return in the high teens.

HBAN Valuation (FAST Graphs)

Investor Takeaway

Huntington Bancshares is a well-run and regional bank that’s currently attractively valued. The company has seen strong growth over the past year, driven by increased scale and efficiency after its acquisition of TCF Financial. It also maintains a healthy balance sheet and pays an attractive dividend that’s well covered. Its expansion into new wealth management markets could be a meaningful growth driver going forward. HBAN is currently a Buy for income and growth.

Be the first to comment