Coatesy/iStock via Getty Images

In retrospect, bad policy decisions would always come back to haunt us. The energy crisis was many decades in the making through a material underinvestment in the extractive industries. The rationale was clear; anthropogenic climate change is real so humanity has to restrict the rise is mean global temperature to well below 3.6 °F (2 °C) above pre-industrial levels. This goal became a non-binding climate deal on the back of the 2015 United Nations Climate Change Conference (COP 21) held in Paris just before the start of Winter in the same year.

A critical tenet of this agreement focused on making capital market flows more consistent with a pathway towards low greenhouse gas emissions and climate-resilient development. This meant ESG investing, a growing but still a somewhat obscure component of the financial markets, now had unprecedented political backing from the world’s largest economies.

ETFs Based on MSCI ESG Indexes

MSCI

In the following year, ETFs based on MSCI’s ESG indexes would jump 148% to reach 67 with AUM also more than doubling its year-ago figure. This rapid ramp of inflows into ESG funds and the resulting AUM growth would continue all throughout the pandemic and reach its apex just as the broader stock market peaked in the fourth quarter of 2021.

Critics of the rise of ESG say it is starving much-needed investments in the extractive industries, contributing to the energy crisis, and rendering the USA and Europe more dependent on a number of autocratic states. To its adherents, it was and remains a necessary financial tool to make capital market flows more sustainable.

Coal: The Antithesis Of ESG

St. Louis-based Arch Resources (NYSE:ARCH) is a coal mining and processing company focused on bituminous and sub-bituminous coal. The company produces metallurgical coal for steelmaking, it also produces thermal coal for sale to the domestic and international power generation markets. This has essentially made the company a toxic asset for a number of financial services firms in the ESG orthodoxy.

A plethora of pension funds, university endowments, and asset management firms have pledged to stop investing in fossil fuel companies. A number have gone further to liquidate all their holdings in such companies. Dutch pension fund Stichting Pensioenfonds ABP is closing out its nearly $16bn-worth of holdings in fossil fuel companies, Oxford University has announced plans to divest its endowment formally from the fossil fuel industry, and BlackRock has said sustainability would be at the heart of its investment decisions.

The New Energy Zeitgeist

All this happened in the era just before the pandemic. Then came Russia’s invasion of Ukraine. These two events have upended the global order and catalysed an energy crisis that looks set to get worse before it gets better.

The new energy zeitgeist is rapidly being defined by a near visceral need for energy security against the prospect of Russia weaponising gas supplies to Europe and the stream of sanctions implemented to try to starve the Russian war machine. The European Union in its fifth package of sanctions introduced an import ban on all forms of Russian coal. This was 7% of the globally traded market that now has to be met by other international suppliers.

Against what had been material flows of both public and private capital to renewables, the current situation seems surreal for many but renewables have always been intermittent. Hence, without a material investment in utility-scale battery storage, their suitability for powering developed economies will always be constrained. This feature was highlighted in 2021 when unusually low wind speeds worsened a power crunch and sent the continent scrambling for thermal coal. Coal-generated electricity supply increased in the region by 18% to 579 TWh, reversing a nearly decade-long trend of decline.

NextEra Energy (NYSE:NEE) was a key beneficiary of the old ESG orthodoxy. The Juno Beach-based company generates electricity mainly through solar and wind but also has a number of natural gas, oil, and coal-based generating capacity. For all intents, NextEra is classed as a renewable energy company and is the largest in the world.

Seeking Alpha

The orthodoxy saw the growing interest and a subsequent surge in liquidity towards ESG funds create an observed ‘green premium’ on relevant stocks. Indeed, ESG funds took $84 out of every $100 going into active equity funds from 2019 to 2020.

Seeking Alpha

So despite electricity being a fungible good, NextEra trades on a forward price to earnings multiple that is nearly 13x that of Arch Resources. To put this another way, if these PE multiples were analogous to electricity rates paid, you would pay $0.10 cents per kilowatt-hour for Arch Resources and $1.33 per kilowatt-hour for NextEra.

Critically, this spread between both stocks was heavily defined by the old orthodoxy of positive climate action. The narrative then was clear; the fossil fuel industry had to be set on a path of structural decline through boycotts and divestments in order to constrain the rise in mean global temperature. Coal happened to form a low-hanging for private institutions and governments eager to show that they were taking action. Coal-fired power plants do release more greenhouse gases per unit of energy produced than any other electricity source. There are also issues arising from acid rain, smog in developing nations, and the bioaccumulation of toxic elements like mercury in aquatic wildlife.

NextEra last released earnings for its fiscal 2022 first quarter which saw revenue come in at $2.89 billion, a 22.5% year-over-year decline and a miss of $2.27 billion on consensus estimates. A net loss of $451 million was mainly due to one-off charges with EPS coming in at $0.74, an increase from $0.67 in the year-ago quarter. Cash from operations came in at $1.96 billion and supported a $0.425 quarterly dividend payout for a forward yield of 2.41%.

With a price to fiscal 2022 cash flow multiple of 15.46x, NextEra is expensive. This is 84% more expensive than its sector peers and 122% more expensive than its 5-year historical average. This opens up a risk of retrenchment as large premiums during market downturns and recessions are not common and NextEra is still trading far above its historical average even with the recent market downturn.

There have also been delays to large utility-scale solar projects due to the Department of Commerce opening up an inquiry into the imports of solar cells and modules from Cambodia, Malaysia, Thailand and Vietnam. However, the impact of the investigation has been blunted by a White House move to allow solar panel parts to be imported free of tariffs from the four south-east Asian nations.

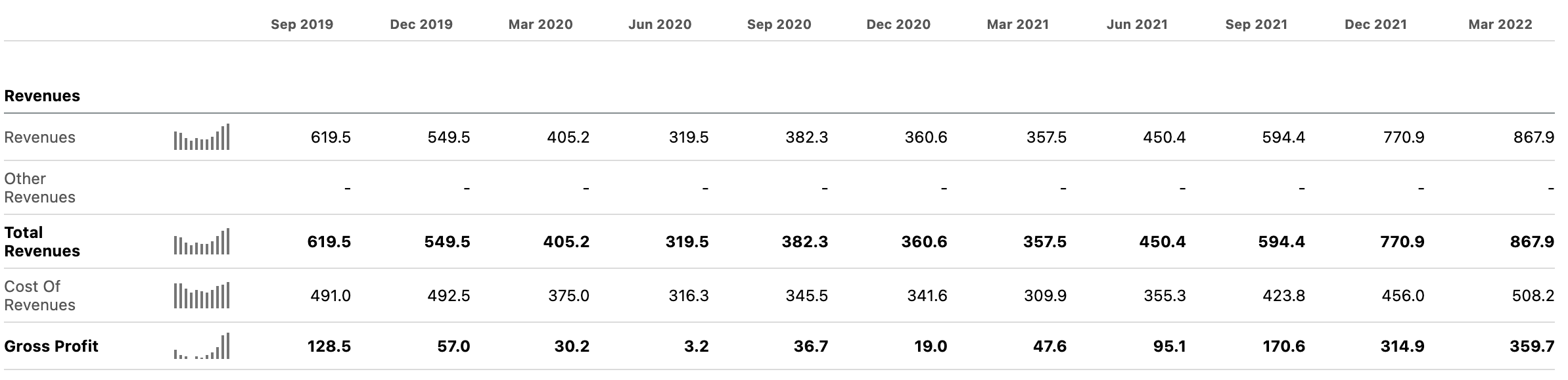

Rising Free Cash Flows Set Against Record Coal Prices

Seeking Alpha

Coal prices have exploded upwards. This has driven significant revenue and gross profit accrual for Arch Resources.

Seeking Alpha

The company last released earnings for its fiscal 2022 first quarter which saw revenue come in at $887.94 million, a 147.8% increase from the year-ago quarter and a beat of $142.61 million on consensus estimates. Gross profit also grew to $360 million, a year-over-year increase of 656% as margins expanded to reach 41.5% from 13.3%. The quarter was simply outstanding as not only did Arch Resources realize adjusted EBITDA of $321 million, outperforming consensus estimates of $308 million, the company also generated $268 million in free cash flow.

This helped management to pay a special dividend of $7.86 in addition to the normal quarterly $0.25 dividend. You might be right in thinking that these are exceptional results borne as a result of temporary conditions that cannot possibly be sustained in the quarters ahead. Certainly, the spectre of a global recession is already weighing down on the prices of oil and gas companies. But as expertly stated by Lyn Alden Schwartzer in her article exploring demand destruction attempts by central banks; “Destroying demand in the face of supply constraints is like running away and hiding from a monster in a closet, so the monster just sits outside and waits for you to come out again. Until the monster is actually dealt with, it’s still there, waiting.”

Arch Resources has no plans to increase Capex which stood at just $22.3 million for its most recently reported quarter. Management expects greater rail availability to drive further volume increase and subsequent revenue and profitability growth as unit economics improve. The company expects to outperform its fiscal 2022 first quarter results and is set to payout at least half of future free cash flows to shareholders as a special dividend.

With the company’s current market cap at $2.66 billion, the current price to forecasted fiscal 2022 cash flow stands at 2x. The risk of investing in a thermal coal company continues to coalesce around the continued lack of long-term political support and competition from natural gas. If the latter collapses on the back of greater Capex spending from OPEC and the Oil Majors, thermal coal prices would face a strong level of selling pressure.

A Zero Carbon World

We might be at the beginning of a protracted new Cold War with Russia. This would make it difficult to stem runaway inflation without a partial reversal of the ESG orthodoxy. Governments will also find it hard to meet their climate targets whilst ensuring energy security against sanctions. In this new zeitgeist, the green premium currently enjoyed by NextEra might melt away.

The rhetoric from national governments is already shifting. The UK, on the heels of COP 26, is set to approve a new coal mine. The country is also negotiating the extension of a coal-fired power plant that was originally set to close this year. In Germany, a bill providing a legal basis to burn more coal for electricity is making its way through the Bundestag. This has set the context for long-term international demand for US thermal coal with Arch Resources already receiving inbound requests for thermal coal exports to Europe for the first time.

The decarbonisation of our planet is still a significant investment trend but perhaps the transition was too punitive in its scope toward the extractive industries. The current energy crisis is hurting the world’s poorest and most vulnerable populations and has led to an erosion in living standards in developed countries. It was never meant to be this way. Positive climate action was envisioned to eventually usher in a zero-carbon world, not wholesale poverty.

This article is not to denigrate calls for greater climate action or to be better stewards of our planet. Government decision at that time was not done in the shadow of the greatest land war in Europe since WW2 and a once-in-a-century pandemic. But the world has changed drastically, and efforts to correct bad policy decisions will likely help see Arch Resources outperform NextEra over the next year at the very least. Shorting through options continues to present more outsized risks than it’s worth so a simply short sale through shares.

Be the first to comment